Good morning!

Markets are set to open little changed today.

Instead I can focus on some positive news: we have another exciting new writer joining me in the cockpit today: Edward Sheldon, CFA.

Ed writes for a variety of websites but is perhaps best known for his work at The Motley Fool. He will bring a new perspective, describing himself as an investor focused on quality, growth and thematic investing. Please do give him a warm welcome - I'm sure you will!

All done for today, have a great weekend! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Unite (LON:UTG) (£2.4bn | SR38) | Guidance reiterated for occupancy and rental growth at lower end of 93-96% and 2-3% ranges for 2026/27 academic year. On track to deliver guidance for £300-400 million of asset disposals in 2026. USAF portfolio value reduced by 1.7%. LSAV portfolio reduced by 2.2% (reason: yield expansion). | AMBER/GREEN ↑ (Graham) It’s a nice steady in-line update today from this provider of student accommodation. I’d like to think that a REIT with modest leverage, that’s already trading at 50% of net tangible assets, couldn’t fall much further than that. I guess the market will do its best to prove me wrong. But I am going to take a very contrarian, moderately positive stance on UTG today. | |

AO World (LON:AO.). (£507m | SR69) | FY March 2026: revenue growth c. 11%, adjusted PBT in line with previously upgraded guidance; at the top end of £45-£50m. Adjusted PBT growth c. 15%. CEO: “We continue to build momentum and all key metrics continue to improve, with an exciting pipeline of new initiatives ahead.” | AMBER/GREEN = (Ed S) A solid update from AO. Revenue growth is healthy, adjusted profit before tax is expected to be at the top end of guidance, liquidity is robust, and free cash flow is up. There are risks around consumer weakness but I am happy to keep the rating at AMBER/GREEN. | |

Metals Exploration (LON:MTL) (£417m | SR95) | Four highly prospective exploration concessions adjacent to the La India Gold Project (Nicaragua). Combined area of approximately 64,400 hectares. | ||

TT electronics (LON:TTG) (£211m | SR53) | Ian Ashton appointed CFO. Currently CFO at SIG. Notice period is up to a maximum of six months. | ||

Impax Asset Management (LON:IPX) (£160m | SR84) | At 31 March 2026, AUM totalled £22.3 billion, representing a decrease of 8.0% over the three-month period. Expects revenue of £109m - £113m for the financial year. Taking further steps to improve operating efficiency. | AMBER/RED ↓ (Graham - I hold) This is a very serious profit warning, with net income forecasts getting slashed by 50% due to persistent heavy outflows. I've decided not to go fully negative on it as it is still profitable and has strong balance sheet support, but there is no doubt that these outflows are unacceptable. | |

SIG (LON:SHI) (£102m | SR56) | Ian Ashton has resigned as CFO. He is moving to TTG. | RED = (Graham) [no section below] We’ve been negative on this building products supplier due to its poor results and shaky balance sheet, and the loss of its long-standing CFO does not bode well. He has been in this position since 2020. Full-year results for 2025 showed SIG generating an underlying pre-tax loss of £20m, a statutory pre-tax loss of £60m, and carrying net debt of £518m. That net debt figure is mostly (60%) in the form of leases but it also includes €300m of fixed notes maturing in October 2029. That’s a heavy burden for an unprofitable business, and the departing CFO will bring his deep understanding of that burden with him to TTG (a business where the leverage multiple was only 1.1x at the end of 2025). | |

| Steppe Cement (LON:STCM) (£42m | SR99) | Trading Update for the Quarter ended 31 March 2026 | In Q1 2025, Steppe sold 344,058 tonnes of cement for KZT 9,696 million compared with 276,217 tonnes of cement for KZT 6,465 million in Q1 2025. Steppe market share increased to 16.0% in the first quarter of 2026 compared with 13.5% in Q1 2025. | AMBER ↑ (Ed). This is a higher-risk penny stock but the company appears to have momentum at the moment. And the Stockopedia system views it very favourably, giving it a StockRank of 99. Weighing up the risks against the positives, I have given it an AMBER rating for now. |

Graham's Section

Impax Asset Management (LON:IPX)

Down 26% to 93p (£117m) - Q2 AUM update - Graham - AMBER/RED ↓

(At the time of writing, Graham has a long position in IPX)

Don’t feel bad for me owning this one - it was already less than half of one percent of my portfolio, before today’s update.

I’m pretty disciplined when it comes to opening new positions, and adding to existing ones. I generally don’t add to losing bets, and I have never added to this one.

Which is just as well:

AUM fell 8% in Q2 (Jan-March) to £22.3bn

Net outflows in the quarter were £2bn, not far off 10% of starting AUM. That’s a really terrible result for a single quarter.

Comment by CEO Ian Simm (emphasis added):

Since January, after a difficult three-year period for investment managers like Impax that focus on actively managed thematic strategies, markets have been considerably more favourable. During the second quarter, 63.4% of our AUM outperformed, notwithstanding the more recent market turbulence…

"As many asset owners base their investment decisions on historical numbers over at least one year, we were not surprised to see a continuation in net outflows, driven principally by redemptions from a small number of institutional investors…

So in essence: they had a strong quarter, but their clients are basing their decisions on a longer timeframe than that - which is sensible.

Impax Environmental Markets (IEM): this £800m trust has been caught up in the campaign by activist hedge fund Saba Capital to close the discounts to NAV at various UK-based investment trusts.

In response to Saba, the independent IEM Board has proposed an “Exit Tender Offer” offer (to be voted on next week). This event is likely to cause a hit of probably several hundred million pounds of AUM. Impax is hoping that IEM investors will switch over to an equivalent UCITS fund.

New guidance:

"Following the recent net outflows and these uncertain external tail risk factors, we expect that our revenue for the financial year will be in the region of £109m - £113m. Against this backdrop we are taking further steps to improve our operating efficiency.

"Longer term, the fundamentals that underpin our investment thesis continue to strengthen, particularly in the areas of renewable energy and energy efficiency, key components of energy security, which is already a priority globally in light of the currently elevated geopolitical tension."

This is quite a serious downgrade from existing consensus forecasts for £124m of revenues.

Estimates

My thanks as always to Equity Development for covering this one.

The changes to forecasts are sobering, as the (negative) effects of operational leverage kick in.

FY September 2026:

AUM forecast cut by 19% (from £28.1bn to £22.8bn)

Revenue forecast cut by 15%

Net income (PAT, profit after tax) cut by 50% from £22m to £11.1m

FY September 2027:

AUM forecast cut by 20% (from £32.2bn to £25.6bn)

Revenue forecast cut by 20%

Net income cut by 45% from £26.3m to £14.5m

Graham’s view

I was neutral on this in January, and I have to downgrade our view today after what is a very serious profit warning. The only question is whether I go fully negative, or moderately negative.

Outflows at this pace are simply unsustainable.

Prior to Q2's £2bn outflow, there was a £1.6bn outflow in Q1.

In the previous financial year, there were £10bn of outflows (more than a quarter of starting AUM).

Fund performance has evidently not impressed Impax's customers: their funds have been unable to compete with the returns of US mega-caps/technology and the passive indexes whose returns have been driven by them.

I've decided not to go fully RED on this today. My reasons are as follows:

The company is still expected to generate meaningful after-tax profits (>£10m p.a. for the next few years). It's not yet unprofitable.

Tangible balance sheet equity was £90m as of September 2025, supporting nearly 80% of the current market cap.

The latest forecast from Equity Development suggest the company will have net cash of £65m as of September 2026 (unchanged from September 2025).

Founder-CEO Ian Simm still owns 7.5% and will want to protect his legacy. He has announced “further steps to improve our operating efficiency”.

So I’m still finding quite a few positives here. The P/E multiple is now about 9x, falling to 7x based on the FY27 forecast.

But I do have to respect the fact that this is a serious profit warning, so I am AMBER/RED in the short-term. No fund manager can survive persistent outflows like this.

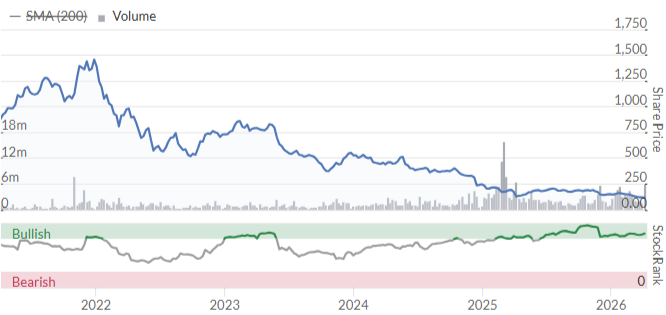

The 5-year chart tells quite a story:

Unite (LON:UTG)

Up 1% at 466.2p (£2.47bn) - Trading update and Q1 fund valuations - Graham - AMBER/GREEN

It’s a nice steady in-line update today from this provider of student accommodation:

Guidance reiterated for occupancy and rental growth at lower end of 93-96% and 2-3% ranges for 2026/27 academic year

This matches what the company said in February, at its full-year results.

Current trading:

74% of beds reserved for 2026/27 cycle

At last year’s Q1 update, they reported 75% of beds had been sold, so it’s a similar result this year.

This year, slightly more of the reservations are to the universities themselves rather than directly to students. I imagine that it’s less risky and simpler for Unite if they can offload beds to universities rather than individually to students? But then, that will have to come at a discount compared to what an individual student would pay.

Following the £700m acquisition of Empiric Student Property, which completed in early 2026, the integration of that business “continues to progress well”.

Disposals:

On track to deliver guidance for £300-400 million of asset disposals in 2026.

£300-400m is small relative to all of the properties owned or controlled by Unite. Balance sheet assets are £6bn+. So this is just an evolution, not a revolution.

They are seeking “to reposition towards higher-quality portfolio aligned to the strongest universities”, and have hired Goldman Sachs to help them make these disposals, while also retaining their existing advisors.

CEO comment:

Our strategy is focused on increasing our alignment to the UK's leading universities where we see the strongest prospects for housing demand and future rental growth. To achieve this, we have already increased our disposal programme and the Board is exploring options to further accelerate our transition to a more focused, higher-quality portfolio, which would release surplus capital for reinvestment into share buybacks or University Partnerships consistent with our capital allocation framework.

Valuation: there is bad news on this front but it’s outside of Unite’s control, being driven by interest rates.

The Unite Student Accommodation Fund (£2.8bn) and the London Student Accommodation Joint Venture (£2.0bn) have lost 1.7% and 2.4%, respectively, of their value, due to higher yields being applied to them.

Graham’s view

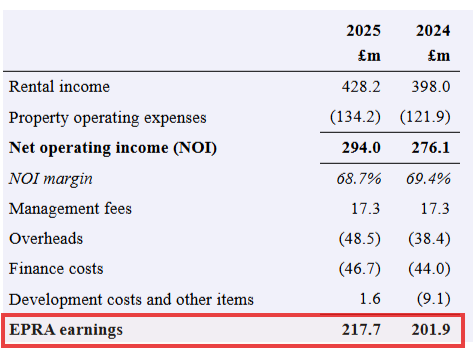

Checking the December 2025 results, I see that net tangible assets (NTA) per share were 955p, double the current share price. The calculation of NTA is done according to real estate or “EPRA” rules.

Leverage was modest with a loan to value of only 27%.

100% of debt had fixed or capped interest rates.

Given low leverage, I’m not sure why this is so cheap. I understand that a discount to NTA is to be expected, and there can be scepticism over valuation, but a 50% discount is not what I typically expect.

The £100m buyback this year will have futher increased assets per share (buying back shares at a discount increases the per-share value of remaining shares).

Last year, earnings were a solid £218m, using the EPRA method, and this is before the addition of Empiric.

The calculation of EPRA earnings looks sensible to me - it’s supposed to show recurring rental profits.

As a REIT, there is of course no corporation tax on these profits.

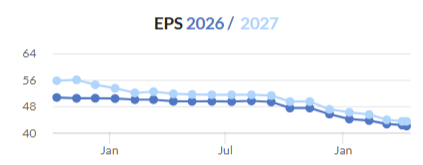

Forecasts suggest we might see EPS of 42p this year, and 43.4p next year.

In conclusion, I’m tempted to be fully positive on this, given the cheapness on offer, but I’ll resist the temptation. I note that Roland was merely neutral on it in January - and the company has warned on profits since then.

In February, the outlook statement was weak, due to a poor performance at Empiric.

And the overall trend in earnings forecasts is negative:

With all of that having been said: I was interested in an income stock, I’d be very tempted to go bottom-fishing here.

My experience with Impax shows that this is often a mistake. But I’d like to think that a REIT with modest leverage, that’s already trading at 50% of net tangible assets, couldn’t fall much further than that. I guess the market will do its best to prove me wrong. But I am going to take a very contrarian, moderately positive stance on UTG today.

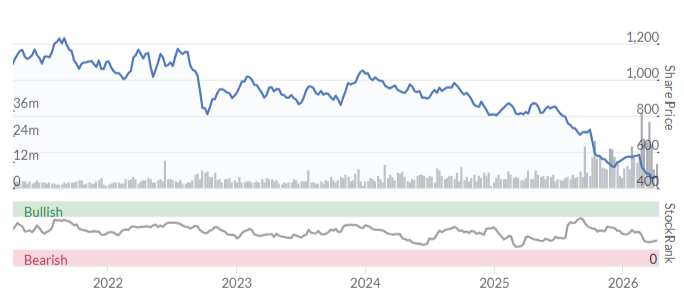

Underlining how contrarian this is, here is another uninspiring 5-year chart:

Ed S's Section

Steppe Cement (LON:STCM)

Up 16% at 22p (market cap £48m) – Q1 trading update – Ed S– AMBER ↑

Kazakh cement company Steppe has posted a trading update for Q1 (ended 31 March 2026).

The main financial highlights:

Steppe sold 344,058 tonnes of cement in Q1 for KZT 9,696 million (approx USD $19.5 million), compared with 276,217 tonnes for KZT 6,465 million (approx USD $12.7 million) in Q1 2025 (an increase in volume of 25% and an increase of 50% in respect of revenue generated in KZT).

The average price (excluding VAT) received by Steppe for delivered cement in Q1 was KZT 28,181 (approx USD $57) per tonne compared with KZT 23,404 (approx USD $47) per tonne in Q1 2025

Steppe’s market share increased to 16.0% in the first quarter of 2026 compared with 13.5% in the first quarter of 2025.

We also get an update on the market backdrop:

In Q1, cement sales in Kazakhstan reached 2.03 million tonnes, representing a 2% increase year on year. This reflected relatively strong demand despite the seasonal slowdown typically associated with winter months.

Cement exports from Kazakhstan declined by 48% year-on-year in Q1. At the same time, cement imports decreased, accounting for 6.3% of total market consumption, compared to 8.6% in the same period of the previous year.

The Company expects total cement consumption in Kazakhstan for 2026 to remain in line with 2025 levels, at approximately 14.5 million tonnes.

Finally, there is a project update:

As previously announced, the Company is expanding cement production to a total capacity of 2.5 million tonnes to enable it to meet increasing demand.

The Company has started implementation of the Project and aims to increase production by 0.5 million tonnes by Summer 2027.

The Project is expected to reduce energy consumption per tonne and improve emissions.

The total current estimated cost is USD $35 million.

Ed S’s View

I don’t think I’ve ever covered Steppe Cement and it hasn’t been covered here at Stockopedia for around two years (its last rank was AMBER/RED). But it looks interesting from a quantitative perspective – its Stock Rank is 99 at present (95 Quality, 81 Value, 83 Momentum).

The market clearly likes today’s update. As I write, the stock is up about 16%. But we’re talking about a very small company here (market cap of around £48m) and with this kind of stock, liquidity can be thin. Overall, the update looks positive to me though – not only do we have higher production volumes and strong selling prices but the company is gaining market share.

A few things to note about this company:

It seems to post its annual reports very late. It has not yet posted its full results for 2025 (last year the report for 2024 came in late June)

We don’t have broker forecasts currently. So, it’s hard to get a read on the P/E ratio.

It has a convoluted corporate structure – it’s a Malaysia-based holding company that operates in Kazakhstan.

It used to pay dividends but hasn’t in recent years.

Taking all this into consideration, it’s higher up on the risk spectrum.

That said, the company has been around for a while. It has been operating since the 1950s and came to the AIM market in 2005.

And recent updates have been encouraging. In January, it said that:

Revenue for 2025 was KZT 52,375 million (approx USD $100 million), up 33% (in KZT terms) on the KZT 39,244 million (approx USD $84 million) for 2024.

In 2025, cement sales volume was approximately 2.07 million tonnes, all sold domestically (21% higher than in 2024). The increase in production was the result of several years of incremental processing improvements.

If we take that 2025 sales figure, we get a price-to-sales ratio of just 0.70. That looks low but we can’t really compare this company to larger mainstream producers due to its size and structure.

As for the backdrop, the IMF forecasts Kazakhstan GDP growth of 4.4% in 2026. That’s a solid level of growth but a drop from the 6.5% growth recorded in 2025.

Overall, there's a lot to like here but also quite a few risks. I think it could be worthy of further research so I’ll give it an AMBER.

AO World (LON:AO.)

Up 9% at 96p (market cap £551m) – Full-Year Post Close Trading Update – Ed S – AMBER/GREEN =

UK electricals retailer AO World has posted a trading update for the 12 months to 31 March 2026.

STRONG REVENUE GROWTH AND PROFIT AT THE TOP OF PREVIOUS UPGRADE

The main highlights:

Total group revenue growth expected to be c. 11%.

B2C growth expected to be c. 9.5% underpinned by market share gains across all key categories.

Adjusted profit before tax is expected to be in line with previously upgraded guidance; at the top end of £45-£50m (it says there were no adjusting items in FY2026)

Profits are growing faster than sales – it expects c. 15% year-on-year adjusted PBT growth, despite material cost headwinds.

The group had hedging arrangements in place covering approximately 80% of forecast fuel usage and 100% of electricity usage for the FY2027 trading period.

It expects to have c. £200m of liquidity at the period end.

Profit is converting to cash, with free cash flow of c. £65m (FY2025 £23m) for FY2026.

Ed S’s View

Back in November, Roland rated AO World as AMBER/GREEN. I think that’s a fair rating in light of today’s update.

This is a solid update. Revenue growth is healthy (although Stockopedia forecasts suggest that analysts were looking for closer to 12% growth), adjusted profit before tax is expected to be at the top end of guidance, liquidity is robust, and free cash flow is up.

It’s great to see that the company has hedging arrangements in place for fuel and electricity. It is pretty much insulated from adverse price movement this financial year.

Note that in the update, AO's Founder and CEO John Roberts mentions the company’s ‘shared economics’ strategy. For those who don’t know what this is – it’s a business model in which companies aim to keep lowering their prices in order to increase customer loyalty and keep customers coming back for more.

It can be a really powerful strategy if executed well. Some other businesses that employ this model include Amazon (I hold), Costco (look at its share price over the long term), and Wise (I hold).

Roberts also says:

“In the coming weeks, AO will become the first company globally to reach one million Trustpilot reviews with a 4.9 rating from customers.”

That’s obviously a great Trustpilot rating. But it should be noted that there is some scepticism over the trustworthiness of reviews on that platform.

As for the valuation, if we take the earnings forecast for this year, we get a forward-looking P/E ratio of 13. That seems reasonable to me given the top-line growth.

I’ll point out that there’s no dividend. It would be good to see a dividend payout introduced in the years ahead but perhaps the priority is to focus on lowering prices for customers.

For me, the biggest risk here is consumer weakness (related to higher oil prices). AO does sell a lot of things that consumers may cut back on if their disposable income drops.

Examples include TVs, speakers, computers, and coffee machines. If the UK consumer weakens, demand for these kinds of products could fall.

I will point out that the StockRank here is a little underwhelming – it’s only 69 (Quality 95, Value 57, Momentum 35). For now though, I’m happy to keep AO at AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.