Good morning!

The FTSE is set to open litte changed, at 10,600.

Focus remains on Iran: Trump spoke very positively last night about the prospects of a permanent deal that would reopen the Strait of Hormuz. But markets don't seem to believe him, with oil prices and other commodities remaining at elevated levels.

If company news is quiet today, I intend to catch up on some stories that were missed during the week - let me know if you have any requests!

Today's Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Workspace (LON:WKP) (£718m | SR58) | Trading Profit after interest for FY March 2026 to be in line with market expectations. The decrease in rent roll and reduction in pricing in H2 will have a negative impact on portfolio valuation. | ||

ITM Power (LON:ITM) (£641m | SR26) | SP +42% The collaboration envisages the deployment of several hundred decentralised production plants for NATO armed forces, each with an electrolysis capacity of up to 50 MW. It will initially focus on the UK. | AMBER = (Graham) I acknowledge how exciting this announcement is, but the revenue and profit implications are impossible for me to guess at. For this reason, I’m leaving our neutral stance unchanged. I just don’t see how to value the company at this stage. But well done to holders. History shows that these shares can really take off - and maybe there is some real substance behind the hype this time? | |

Discoverie (LON:DSCV) (£607m | SR46) | Trading accelerated in Q4. Full year: orders up 9% CER and by 5% organically, growing faster than sales. “On-track to deliver another year of growth in adjusted earnings per share in-line with consensus market expectations” Pro forma leverage c.1.7x, “comfortably within our target range”. | ||

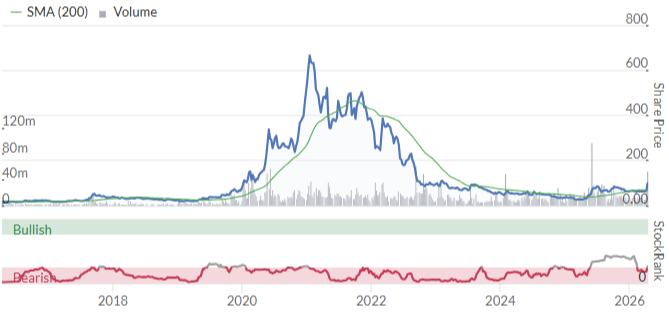

VP (LON:VP.). (£193m | SR49) | “In a challenging macroeconomic environment, Vp expects to report FY26 profits between £26-29m, in line with previous revised guidance.” Outlook: Board confidence in positioning and future performance. | AMBER = (Graham) The profit warning was still very recent, and it remains unclear where FY March 2026 profits are going to be within the range given. Therefore, despite the green shoots, I’m leaving our neutral stance unchanged. This is consistent with the StockRank: | |

Aew UK Reit (LON:AEWU) (£168m | SR61) | NAV of £171.97 million or 108.38 pence per share (December 2025: £173.47 million or 109.32 pence per share). NAV total return 0.96% for the quarter. “We are pleased to report a steady quarter of performance, with another period of positive NAV total return, and valuation gains seen across the Company's retail, industrial and office sectors…” | ||

Optima Health (LON:OPT) (£161m | SR76) | FY26 Adjusted EBITDA to be ahead of market expectations by c.10%. Consensus is £18.1m. | ||

Eurocell (LON:ECEL) (£109m | SR70) | Appointment of Matt Worster as the company's new CFO, starting in the Autumn. Matt is currently Finance Director of Travis Perkins General Merchant and has been Director of Investor Relations at Travis Perkins Plc. | ||

Cora Gold (LON:CORA) (£78m | SR26) | Binding US$120 million gold stream, removes future funding requirement for the Sanonkoro Gold Project, enabling CORA to move forward with pre-production workstreams with confidence. Eagle Eye Asset Holdings will be entitled to purchase 30.44% of gold produced at a price equal to 20% of the prevailing spot price. Cora can still replace 50% of the stream with traditional senior debt. | ||

Fevara (LON:FVA) (£71m | SR58) | Exclusive five-year agreement with Oceana Minerals to distribute LithoNutri in Great Britain and Ireland. | ||

Metals One (LON:MET1) (£21m | SR5) | The creditors of Barbrook have approved a plan under which LBR will acquire assets of Barbrook including 2.1Moz of gold resource for ZAR 279 million (US$17.0 million). MET1 owns 30% of LBR. | ||

essensys (LON:ESYS) (£11m | SR27) | Revenue down 25% “primarily due to the continued downsizing of a single large strategic customer”. Adj. EBITDA £0.1m (H1 last year: £0.8m). | PINK (offer from Mark Furness’ concert party at 17p). | |

Zinc Media (LON:ZIN) (£11m | SR33) | The Edge has continued to perform strongly, resulting in the achievement of the final earn-out targets. £1.43m payable to the vendors, £0.34m payable in cash with the remainder payable in new Zinc shares. |

Graham's Section

ITM Power (LON:ITM)

Up 42% to 133p (£919m) - Strategic collaboration with Rheinmetall - Graham - AMBER =

Even for those of us who have never bought German shares, it’s hard to avoid hearing about a giant like Rheinmetall AG (ETR:RHM). I think of it like Germany’s answer to BAE Systems (LON:BA.) .

Congrats to ITM shareholders for this deal:

The collaboration will focus on Rheinmetall's Giga PtX project, which aims to establish a Europe-wide network of decentralised synthetic fuel production plants for the NATO armed forces, designed to strengthen defence energy resilience, sovereign fuel capability and operational readiness.

The project envisages the deployment of several hundred decentralised production plants across Europe, each with an electrolysis capacity of up to 50 MW, capable of producing approximately 5,000 to 7,000 tonnes of e-fuel per annum per facility…

The collaboration will initially focus on the UK.

The CEO of ITM says “the Giga PtX project represents a repeatable deployment opportunity for large-scale electrolysers”.

The Head of Hydrogen Program at Rheinmetall says: “we are creating a scalable network that strengthens energy autonomy for Europe's defence forces.”

Financial implications?

The RNS does not attempt to give any new guidance. It doesn’t give any new financial details for this contract.

In theory, this partnership could see ITM selling hundreds of its hydrogen systems to Rheinmetall and NATO. It recently launched a standardised 50MW plant priced at c. €50m.

Given that the company’s total annual revenues haven’t yet crossed €50m, this would mark an explosive change.

Graham’s view

I’m sorry to any ITM fans, but I don’t feel able to make a high-conviction call on this one.

The historic financials aren't too exciting:

But today’s news is potentially transformational. And the timing is interesting: eight days ago, the UK government made a £40m equity investment into ITM, along with a £46.5m grant from the Department for Energy Security and Net Zero.

I do think the implications of this announcement are highly uncertain:

“The project envisages the deployment of several hundred decentralised production plants across Europe” - but how likely is this to happen? Might the plans change?

Will ITM be the only provider of hydrogen systems? How many other providers might there be?

Plants will have “an electrolysis capacity of up to 50 MW” - does this mean 50MW is the max, and that many plants could be much smaller than this?

What’s ITM’s expected profit margin at a 50MW plant and at smaller plants?

What's the expected timeframe for the rollout of these plants?

So from my perspective, even though I acknowledge how exciting this announcement is, the revenue and profit implications are impossible to guess at.

For this reason, I’m leaving our neutral stance unchanged. I just don’t see how to value the company at this stage.

But well done to holders. History shows that these shares can really take off - and maybe there is some real substance behind the hype this time?

I also note that its FY April 2026 cash guidance is £210-215m, so there are no balance sheet concerns at this time.

Short interest: it's worth noting that the stock is heavily shorted (at least 4.4% of shares borrowed), and today's gains could involve some distressed short-covering. ITM's share price has doubled since last week! So it wouldn't surprise me if the funds shorting it are now rushing for the exits.

VP (LON:VP.)

Up 1% at 483p (£194m) - Trading Update - Graham - AMBER =

This equipment rental provider issued a profit warning in February, cutting adjusted PBT expectations from £37m to £26-29m.

That guidance is reiterated today.

As FY March 2026 is already over, perhaps they could have narrowed down guidance a little?

Looking ahead, they’re sanguine on the outlook:

Despite tough market conditions, the Group continues to see long-term drivers of demand across its core sectors.

I was neutral on this stock in February as, despite the profit warning, they were still profitable and there appeared to be decent scope for recovery, e.g. in the water sector as delayed infrastructure spending would eventually kick in.

It now seems that there are a few green shoots of recovery: I’ve highlighted them in bold below.

Electricity transmission continues to see growth and strong demand in both the UK and Europe. Rail activity is steady but subdued, with good visibility on future project pipelines. There are positive lead indicators in Water as we enter Year 2 of AMP8, supporting our confidence in an improvement in revenues for FY27.

Within the Construction sector, the Specialist Construction market remains supportive, particularly in London and the Republic of Ireland. Housebuilding remains subdued, but with stronger prospects as Homes England's Social and Affordable Homes Programme (SAHP) 2026-2036 commences.

Mid East conflict: higher fuel costs have been “largely mitigated through customer pricing”.

Graham’s view: the profit warning was still very recent, and it remains unclear where FY March 2026 profits are going to be within the range given. Therefore, despite the green shoots, I’m leaving our neutral stance unchanged. This is consistent with the StockRank:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.