Good morning!

The FTSE is set to open lower this morning, below 10,500, after weakness yesterday afternoon..

The US-Iran ceasefire has been extended, but not in a very meaningful way:

- The two sides never met for face-to-face talks in Islamabad, with Iran stating that US demands were unreasonable.

- The Strait of Hormuz remains closed.

- The US blockade remains in force.

So why is the ceasefire still in place? Apparently because the government of Pakistan, which is mediating, asked Trump to hold off on fresh strikes. Brent crude is now at $98.

Live webinar on Thursday at 5pm: with results season over, Ed and I will be taking a fresh look at our favourite investment ideas tomorrow evening. Here's the registration link.

Today's summaries are complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BHP (LON:BHP) (£151bn | SR83) | Copper production is expected to be towards the top end of FY26 guidance. Iron ore production on track. | ||

Reckitt Benckiser (LON:RKT) (£32bn | SR74) | Revenue down 11.8% due to weakness in N. America & Mead Nutrition. LFL revenue +0.6%. FY revenue guidance unchanged for Core LFL revenue to be +4% to +5%. | AMBER/GREEN = (Roland) This trading update flags up a number of headwinds, most of which I believe are temporary. Although earnings forecasts have fallen recently, my impression is that the core business is probably performing well and looks unusually cheap on a forward P/E of 13 and 5% dividend yield. With the caveat that I see this as a long-term investment, I am leaving my broadly positive view unchanged today. | |

Fresnillo (LON:FRES) (£24.5bn | SR87) | Silver production -8.5% to 11.1moz vs Q4 25 due to lower grades and ore volumes. Gold production up 0.7% to 136.1koz. Performing in line with 2026 expectations. | ||

South32 (LON:S32) (£10.5bn | SR77) | Production guidance is unchanged for all operations except Australian Manganese, where elevated site water levels remain an issue. Net cash rose by $121m to $96m during the quarter, due to higher commodity prices. | ||

Bunzl (LON:BNZL) (£7.7bn | SR96) | Revenue up 1.5% in Q1 at constant exchange rates, supported by volume growth and tariff-related price increases. 2026 guidance unchanged. Continue to expect operating margin to be slightly down year-on-year. | ||

Croda International (LON:CRDA) (£4.2bn | SR86) | Revenue up 1% to £431m at constant currency. Strong growth in Beauty Actives and Fragrances & Flavours, lower sales in Crop Protection. No change to 2026 expectations. | ||

Aberdeen (LON:ABDN) (£3.9bn | SR93) | AUMA -1% to £547.7bn, with net outflows of £2.9bn. Interactive Investor customers +14% year-on-year, with net inflows of £3bn. Firmly committed to FY26 targets for adj op profit of at least £300m and net capital generation of c.£300m. | ||

JD Sports Fashion (LON:JD.) (£3.7bn | SR83) | Chair Andrew Higginson will stand down at July’s AGM. He’s been in the role since July 2022. A search for a replacement is underway. | ||

Hochschild Mining (LON:HOC) (£3.4bn | SR75) | Q1 26 attributable production in line with expectations: gold 55,252oz, silver 1.6moz. Mara Rosa turnaround on track. 2026 production guidance unchanged: 300-328k gold equivalent ounces & AISC of $2,157-$2,320/ge oz. | ||

Quilter (LON:QLT) (£2.5bn | SR72) | AuMA of £141.91bn at end March, +19% year-on-year. Net inflows of £3.0bn. | ||

Renewables Infrastructure (LON:TRIG) (£1.58bn | SR74) | Company notes a series of government policy announcements relating to energy. In particular, TRIG believes changes to Contract for Difference could “increase revenue stability for generators”. | ||

Senior (LON:SNR) (£1.20bn | SR76) | Revenue up 2.5% vs prior year at constant exchange rates with strong performance in aerospace. “... full year performance anticipated to be above the Board’s previous expectations”. | PINK | |

GB (LON:GBG) (£516m | SR69) | Strong growth in core Identity and Location segments. FY26 revenue up 3.2% to £285m, with H2 growth in “mid-single digits”. FY26 adj operating profit to be c.£67.6m (FY25: £67.0m). FY27 outlook unchanged. | ||

Cerillion (LON:CER) (£422m | SR45) | Signed Omantel in January as a major new client, with an expected contract value of c.£42.5m. FY results are expected to be “strongly weighted” to H2, with H1 revenue to be c.£18m and H1 EBITDA c.£6.2m. The Board believes Cerillion “remains well-positioned to meet market expectations” for the full year. | AMBER = (Roland) Today’s update is in line, but includes guidance for a very unusual 74% H2 weighting to EBITDA profit. This appears to be based on expectations that the order book, including the recent Omantel deal, will start to unwind in H2. I can see the potential for this, especially if this includes recognition of a licence fee from the Omantel deal. However, management’s lack of disclosure around the value of the order book or the scheduled unwind means investors are left with no visibility and an uncomfortable dependency on H2 performance. I admire the quality and track record of the business, but I think the share price looks up with events and can see some risk that H2 will disappoint. On balance, I’m staying neutral today. | |

Tharisa (LON:THS) (£348m | SR99) | Jacques Breytenback is appointed as CFO Designate with effect from 1 May. He will assume the role from 1 August 2026. He has 25 years experience in mining, including Petra Diamonds and Anglo American Platinum. | ||

Malibu Life Holdings (LON:MLHL) (£323m | SR34) | Book value per share up 4.5% to $33.33. Total comprehensive income of $24m, shareholder equity of $569m. Outlook: remains committed to the medium-term target of generating annual premiums of $5bn and mid-teens return on equity by the end of 2028. | ||

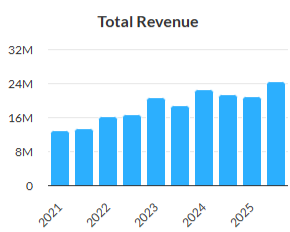

Pinewood Technologies (LON:PINE) (£278m | SR11) | 2025 revenue up 29.8%, adj EBITDA up 17% to £16.4m and pre-tax profit up 3.5% to £8.8m. Total Contract Value of £64.5m at the end of 2025, reflecting incremental future revenue. FY26 EBITDA to be in line with market expectations (consensus: £21.3m). | ||

Ferrexpo (LON:FXPO) (£258m | SR59) | Board believes an equity capital raise is the only viable solution to raise required funding. Intends to launch a fundraise for at least $100m as soon as possible following shareholder approval. Talks are underway with 49% shareholder Fevamontinico in relation to the planned fundraise. | ||

Helical (LON:HLCL) (£240m | SR43) | “Strong progress” during the quarter, with further lettings to tech/AI clients. Notes “strong rental growth being driven by a market with very tight supply”. | ||

Kistos Holdings (LON:KIST) (£220m | SR53) | 21.8 kboepd in Q1. FY26 proforma production guidance remains at 19 - 21 kboepd. Adjusted net debt $78m. | ||

Kenmare Resources (LON:KMR) (£205m | SR23) | “Kenmare is on track to achieve its 2026 guidance on all metrics and drew down 99,900 tonnes of its finished product stockpiles in Q1, in line with its value over volume approach.” | ||

Pulsar Helium (LON:PLSR) (£175m | SR28) | Pulsar Michigan has entered into an exclusive Option to Lease Non-Hydrocarbon Gas Agreement, covering 488,090 gross acres. The agreement “marks a transformative step for Pulsar and for our Falcon Project in Michigan”. | ||

Liontrust Asset Management (LON:LIO) (£166m | SR87) | Net outflows of £0.8 billion. AUMA falls from £21.5bn to £19.6bn. | AMBER/GREEN = (Graham)

Being AMBER/GREEN on this has been a mistake, as I’ve naively thought that it offered value for some time. There are now £124 of AUMA for every £1 spent on Liontrust shares at the current level. That’s actually less cheap than it was in January, when I last looked at the company - so I’m still sitting in the camp which says that the shares might offer some value here, and that they could have hit a bottom. The company is expected to see a solid profit margin this year, with the high forecast dividend yield (7%) easily covered by earnings per share. | |

Quartix Technologies (LON:QTX) (£135m | SR82) | Q1: new subscriptions and the rate of customer acquisition were lower year on year but prospects remain encouraging for the rest of the year. Revenue and profit are in line with achievement of market expectations. | ||

LBG Media (LON:LBG) (£112m | SR80) | Increasing FY26 revenue expectations to c.£110m. However, the revenue mix has lower margins, so Group FY26 EBITDA is to be c.£22m (consensus: £25.4m). | BLACK | |

Ten Lifestyle (LON:TENG) (£71m | SR72) | Trading since the period end has been in line with the Board's expectations for FY 2026. But the Board now expects FY 2027 revenue and adjusted EBITDA to be ahead of current market forecasts, due to contracts won during this financial year. | ||

Fevara (LON:FVA) (£66m | SR56) | “Trading since the half year has been encouraging, with continued strong performance in the UK and further margin improvement. The Board is confident in delivering a full year outcome in line with market expectations”. | ||

hVIVO (LON:HVO) (£63m | SR36) | Signed a contract to conduct a Phase III human challenge trial for ILiAD Biotechnologies, Inc. to test its Bordetella pertussis vaccine candidate. “This multi-year contract will make a strong contribution to near- and mid‑term revenues.” | ||

MTI Wireless Edge (LON:MWE) (£59m | SR96) | Antenna division has received two orders, totaling approximately US$1m, to supply military antennas. | RNS Reach - this announcement should not have any impact on forecasts. | |

Creo Medical (LON:CREO) (£53m | SR61) | Strong trading performance in Q1 FY26. Year-on-year revenue growth of 60%, the upper limit of management’s expectations. On track to deliver 40% to 60% full year revenue growth. | ||

R E A Holdings (LON:RE.) (£51m | SR82) | Revenue +3.7% ($194.9m). PBT $24m including non-routine losses of $3.8m. Current CPO prices comfortably above the 2025 average. Outlook encouraging for increasing returns from the agricultural operations, augmented by contributions from stone and silica sand. | ||

Tpximpact Holdings (LON:TPX) (£35m | SR94) | Expects to comfortably exceed the recently upgraded consensus across all key financial metrics. Revenue +1%. Adjusted EBITDA +54% (£8.6m). Net debt reduced to £4.2m. | ||

Celsius Resources (LON:CLA) (£24m | SR20) | Trading on AIM is unaffected but the company has requested a trading halt on the Australian exchange. Something to do with “developments associated with an alternative conflict resolution process and governance of its Philippine affiliate company, Makilala Mining Company, Inc”. | ||

Shoe Zone (LON:SHOE) (£24m | SR80) | FY October 2026: now expects an adjusted loss before tax of £1.0m - £2.0m, down from previous expectations of a £1.0m adjusted profit before tax. | BLACK | |

Alien Metals (LON:UFO) (£19m | SR27) | Inaugural Mineral Resource Estimate for the Elizabeth Hill Silver Project in Australia. 2.79 million ounces of silver, comprising 0.37 Moz Indicated and 2.42 Moz Inferred. | ||

Prospex Energy (LON:PXEN) (£14m | SR18) | Subsidiary PXEN Tatra has been formally awarded the Dunajec onshore licence area in Poland. | ||

Wishbone Gold (LON:WSBN) (£10m | SR9) | Raised £1.1m gross at 26.35p (last night’s close: 31.5p). 1 warrant issued for every two new shares, strike price 40p. |

Graham's Section

Liontrust Asset Management (LON:LIO)

Up 1% at 272p (£168m) - Trading Statement - Graham - AMBER/GREEN =

There’s zero surprise to read of more outflows here:

Net outflows in the quarter of £0.8bn

AUMA falls from £21.5bn to £19.6bn

On the bright side, £2.6bn of AUMU is set to come in from the acquisition of River Global (LON:RVRG), and there are £500m of institutional mandates that have been awarded but not yet funded.

But with the persistent stream of outflows, these positives are swimming against the tide.

CEO comment:

"Liontrust is benefiting from investor diversification away from US equities and increasing demand from clients for active management, led by strong performance across our European strategies…

This more positive outlook for flows reflects the expansion of Liontrust's international distribution. We are extending our reach in the Middle East and Asia and have continued to make further progress in Europe…

As Liontrust enters the new financial year, we are well positioned to drive organic growth, realise benefits from the proposed acquisition and take advantage of the increased demand for active management."

Performance: they mention eight funds that have performed in the first or second quartile over 1 and 3 years. But I count 56 funds in their fund table. My general impression is that performance has not been very good. Which naturally makes it difficult to attract flows!

Graham’s view

Being AMBER/GREEN on this has been a mistake, as I’ve naively thought that it offered some value for some time:

But the share price has been in long-term decline:

Could it be making a low here?

If we compare the very latest AUMA figure (£20.8bn, 20th April 2026) with the current market cap, there are now £124 of AUMA for every £1 spent on Liontrust shares at the current level.

That’s actually less cheap than it was in January, when I last looked at the company.

AUMA will get a further boost from the acquisition of River Global, which should complete in a few months.

So I’m still sitting in the camp which says that the shares might offer some value here, and that they could have hit a bottom.

My cautious optimism has been wrong so far. But other UK fund managers are now seeing some inflows. Perhaps Liontrust can at least hope to see flows reach a breakeven point at some point this year?

It’s not my top pick in the fund management space, but profits are profits. Liontrust is still expected to see a solid profit margin this year, with the high forecast dividend yield (7%) easily covered by earnings per share. I find it very difficult to be negative on a stock offering this sort of value.

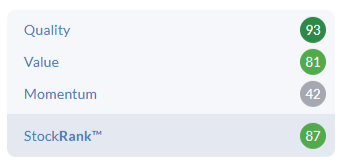

The StockRanks agree, accurately describing it as a Contrarian play.

If fund performance remains poor, and if outflows persist even when most other fund managers have recovered, the outcome should in the end be a takeover from a larger group. There should always a “buyer of last resort” for a business like this.

Roland's Section

Cerillion (LON:CER)

Down 6% at 1,347p (£398m) - H1 Trading Update - Roland - AMBER =

Cerillion plc, the billing, charging and customer relationship management software solutions provider, announces an update on trading for the first six months of its current financial year ending 30 September 2026.

This is an in-line update and there are no changes to broker forecasts this morning for Cerillion. But the market reaction suggests a more sceptical view of today’s guidance, which includes a very heavy H2 profit weighting.

Cerillion leads today’s half-year update with news of its largest contract to date, a five-year deal with Omantel with an expected value of c.£42.5m. This was previously announced in January, but it’s the clear highlight in a half year that is expected to see revenue and profit fall sharply relative to the same period last year:

H1 26 revenue down 14% at c.£18m (H1 25: £20.9m);

H1 26 EBITDA down 37% at c.£6.2m (H1 25: £9.9m).

Outlook: management is guiding for full year results “to be strongly weighted to the second half”. A strong order book (value unspecified) is “anticipated” to unwind during the latter part of the year, supporting a stronger revenue performance.

As far as I can see, the main basis for this guidance is that the Omantel deal will drive significant revenue recognition in H2, including an initial licence fee.

We are also told that new orders during H1 were £39.6m, double the result achieved during the same period last year. This mainly reflects the Omantel win, so may not be a sustainable rate of new business.

The company says that the H2 weighting is “like last year”, but I think this is stretching a point:

Cerillion’s 2025 results carried an H2 weighting of 54% (revenue) and 57% (adj EBITDA);

Today’s guidance implies an H2 weighting of 67% (revenue) and 74% (adj EBITDA).

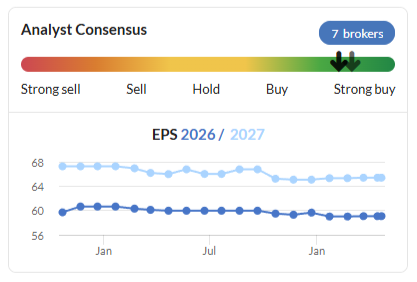

I should emphasise that broker forecasts from both Cavendish and house broker Panmure Liberum are unchanged today, so this is not a stealth profit warning.

However, commentary from both brokers highlights the lumpy nature of progress here, describing it as characteristic but perhaps uncomfortable for investors who are unfamiliar with the business!

A look at past performance certainly suggests this level of H2 weighting is unprecedented in recent years:

Roland’s view

As we always say in these circumstances, it’s possible that Cerillion will deliver H2-weighted results and meet full-year guidance.

However, when we see an unusual weighting of profit to the second half of the year like this, we often find there’s an increased chance of a profit warning later in the year.

In this case, broker forecasts have edged lower over the last 18 months, but have been fairly stable:

While I continue to admire Cerillion’s long-term growth and super quality metrics:

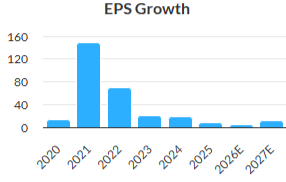

… I am mindful that earnings growth has slowed considerably in recent years:

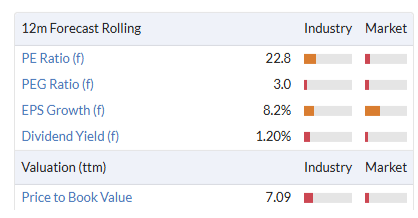

The shares are not obviously cheap, either:

The StockRanks style Cerillion as a Falling Star and suggest caution on value:

I’ve previously noted the complex and lumpy accounting of Cerillion’s multi-year contracts and recognise that this is not necessarily an issue.

Given the strong quality metrics, I could get on board with a forward P/E of 20+ if I was confident about earnings growth.

However, I think the company could provide more visibility for investors than it’s chosen to do today. By specifying the value of its order book and giving some guidance on the value scheduled to unwind in H2, we would have been able to gain some visibility on profit for the second half of the year.

As things stand, we simply have to trust that this situation will deliver an unprecedented level of H2 profit weighting.

I was neutral on Cerillion in November. While I have some concerns, I do also admire the quality and track record of this business. Cerillion has built its reputation and gained market share while often competing against much larger rivals.

I’m going to leave my AMBER view unchanged today, reflecting my mixed view on the shares at current levels.

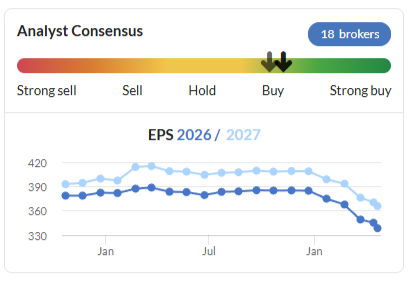

Reckitt Benckiser (LON:RKT)

Down 6% at 4,633p (£30bn) - Q1 Results 2026 - Roland - AMBER/GREEN =

Today’s first-quarter update has seen the consumer goods group’s share price continue its recent descent:

Today’s share price drop may partly be explained by weaker-than-expected sales. Newswire commentary suggests that today’s first-quarter like-for-like revenue growth of 1.3% was below consensus expectations for a figure of 2.9%.

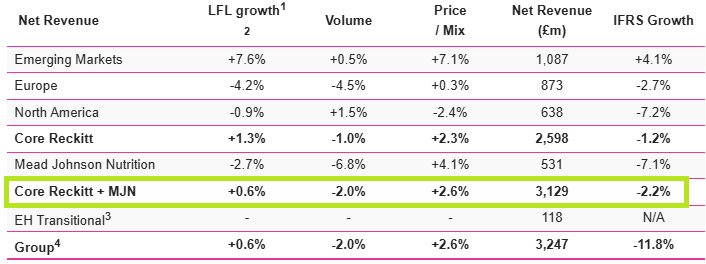

There are lots of moving parts here, but I think the key number to look at for the continuing business are the Core Reckitt + MJN figures (the Essential Home business has now been divested):

The highlighted line flags up weak volumes (-2%) and limited pricing growth, resulting in an overall Q1 revenue decline of 2.2%.

The main reason for the drop in volumes seems to have been a “weak cold and flu season” in Europe and North America. Good news for consumers, not such good news for makers of branded cold and flu remedies.

However, today’s commentary also flags up a number of additional headwinds:

Geopolitical disruption to operations and supply in our Middle East business – current forecasts do not reflect any impact beyond H1.

High single digit LFL net revenue growth in Emerging Markets, but with a c.2% headwind as a result of international sanctions disrupting the group’s Russian operations. Essentially, it seems Reckitt is having to reformulate products sold in Russia so that they no longer benefit from EU-owned Intellectual Property.

In Europe, competition and discounting is making it difficult for Reckitt to expand its share in key categories; “growth rates remained challenged”. The company says it’s seeing encouraging initial results from efforts to gain market share with Finish.

High commodity prices are having an impact: Reckitt estimates that oil at $110 per barrel for the remainder of 2026 would add £130m to £150m to the group’s cost base. This is said to be “manageable”.

Outlook: this is another company that’s guiding for an H2 weighting to profit:

We maintain our expectation for Group adjusted operating profit margin for FY 2026, with the delivery of this weighted to H2. In H1, the impact of stranded costs, lower seasonal incidence on our higher margin seasonal OTC business and higher commodity prices are expected to result in Group adjusted operating profit margin around 200bp below H1 2025 (24.6%).

I don’t have access to broker forecasts today. My working assumption is that consensus estimates are likely to edge lower, given that today’s weak revenue performance appearst to have been unexpected by the market.

This would continue a trend of recent downgrades that have already seen 2026 consensus EPS estimates cut by 10% in three months:

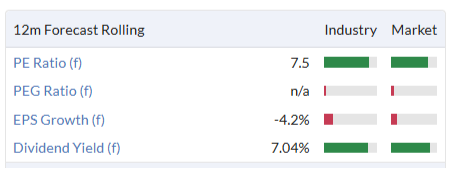

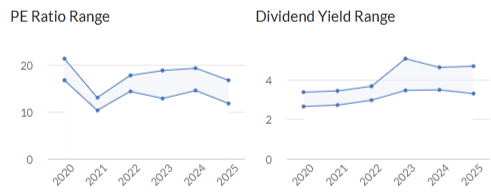

Assuming no major further changes to forecasts, Reckitt shares are now trading on a forward P/E of 13 with a 5% dividend yield. This is at the low end of the group’s valuation range in recent years and looks potentially good value to me:

Roland’s view

Reckitt is still paying the price for its misguided acquisition of infant formula producer Mead Johnson, whose main brand is Enfamil. This business has since been designated as non-core, but can’t easily be sold as it’s mired in lawsuits alleging the company’s products can cause a serious bowel disease in pre-term infants. The company hasn’t provided for specific damages, but it is involved in some of the same cases as Abbott Laboratories, which was recently ordered to pay $70m in damages in one case.

More broadly, Reckitt appears to be facing a number of temporary headwinds, at least some of which should ease over time.

On a short-term perspective, I think a neutral view is appropriate here. However, as an investment I would argue that the fundamental appeal of this business relies on its ability to perform reliably over very long time periods (unlike many other businesses).

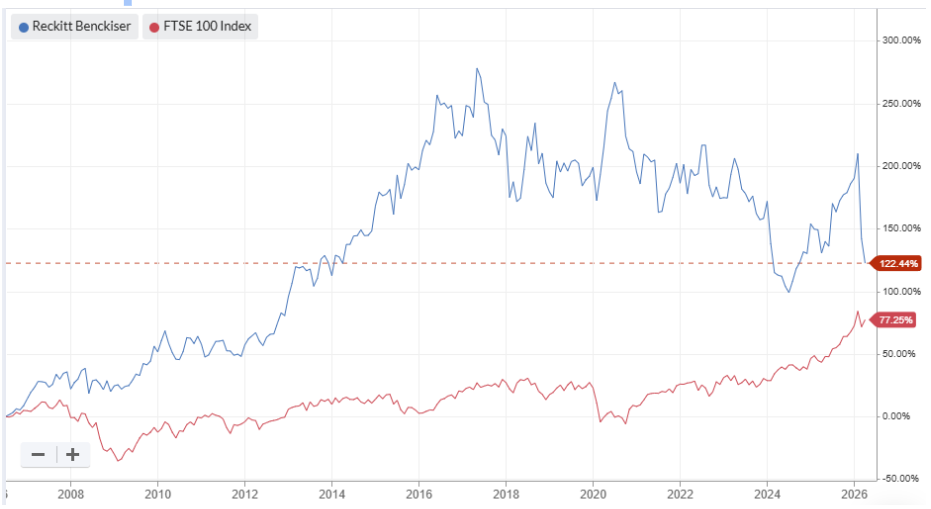

Reckitt has arguably been going through a bad patch for several years, but has still comfortably outperformed the FTSE 100 on a 20-year view. The dividend has also not been cut for at least 20 years, as far as I can see.

It’s often said that consumer brands will be displaced by cheaper own label brands. Today’s commentary makes it clear that this is a source of pressure on trading in Europe at the moment.

At the same time, I think it’s worth remembering how long companies such as Reckitt and Unilever (disc: I hold) have been trading successfully. Reckitt’s history can be traced back to 1840, and Unilever is similar.

These companies’ focus on consumer goods and products that can readily be substituted means they have to adapt to stay in business. The size and age of these businesses proves how good they are at doing this.

The cautious tone of today’s results and the recent downgrades to earnings forecasts mean that I should downgrade my previous AMBER/GREEN view (in January) to AMBER today.

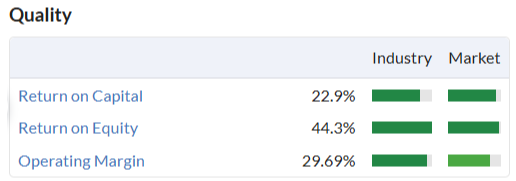

However, I have to admit I’m reluctant to do this. Reckitt’s core brands – names such as Dettol, Strepsils, Durex and Lysol are used by millions of people daily. In today’s update, the company highlighted strong growth in areas of the business that aren’t affected by temporary headwinds:

[...] double-digit growth in China and India and mid-single-digit growth in non-seasonal brands in North America

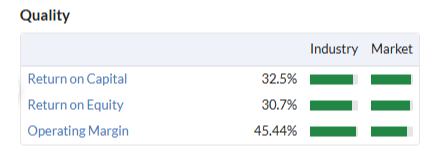

I’ve rarely seen Reckitt shares trading as cheaply as at present. A P/E of 13 and a 5% looks undemanding to me for a business with this heritage and strong quality metrics:

I note that the stock also qualifies for a number of quality/value screens suggesting it could be attractive on a longer-term view:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.