Good morning!

Reminder: Ed and I are doing a webinar together this evening at 5pm, to look at our favourite opportunities arising from results season. Here's the link to sign up.

Overnight markets: the FTSE is set to continue the weakness of recent sessions, opening 50 points lower around 10,420. The US-Iran ceasefire is set to continue indefinitely but it appears to be a fragile peace. There is effectively zero traffic through the Strait of Hormuz.

We're finished for today, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Relx (LON:REL) (£49bn | SR61) | This update is “reaffirming the outlook for the full year”. “We continue to see positive momentum across the group, and we expect another year of strong underlying growth in revenue and adjusted operating profit, as well as strong growth in adjusted earnings per share on a constant currency basis”. | ||

London Stock Exchange (LON:LSEG) (£48.3bn | SR49) | Full-year revenue growth expected to be in the upper half of 6.5-7.5% guidance range. It was “a great start to 2026 across the board”. “We are confident in the outlook and the delivery of all of our financial targets for the year." | ||

J Sainsbury (LON:SBRY) (£8.03bn | SR78) | Outlook: Argos trading reflects “a subdued general merchandise market”. Conflict in the Middle East to impact customers and the business. “The duration and extent of these impacts is very uncertain and this is reflected in our profit guidance, where we currently expect to deliver Total underlying operating profit of between £975 million and £1,075 million.” | BLACK (AMBER ↓) (Graham)

I was positive on this in November last year, and the market cap is only a little lower now than it was then. Given the profit warning, and the lack of visibility, the time is right for us to downgrade our stance. If it was just a profit warning, with a 7% downgrade to expectations, that would be one thing. But if underlying operating comes in at the low end of the range (£975m), that will be an 11% miss against prior expectations. It will also be a 5% reduction in profit against the prior year. | |

Tritax Big Box REIT (LON:BBOX) (£4.19bn | SR46) | New 20 year lease with Currys on recently completed building. 10 year lease extension on existing facility let to Currys (increasing the remaining lease term to 20 years). | ||

Man (LON:EMG) (£3.05bn | SR54) | Net outflows $1.6 billion. AUM increases from $227.6bn (Dec 2025) to $228.7bn (March 2026). Positive investment performance. | ||

Hikma Pharmaceuticals (LON:HIK) (£2.88bn | SR58) | “…On track to deliver revenue and profit growth, in line with our full year guidance and our overarching focus on long-term sustainable profit growth.” | ||

AJ Bell (LON:AJB) (£2.19bn | SR69) | SP -3% “An excellent quarter of growth”. Customers up 50,000. Customers +22% in the year, +7% in the quarter. Assets under administration +20% y/y, +1% q/q (negative market movements in the quarter). Net inflows £2.7 billion. | GREEN = (Graham) [no section below] We've been consistently positive on this for the past year, and there is little reason to change stance today given the terrific growth rates it's achieving. The "Advised" platform is a little sluggish (customers up 7% year-on-year) but the D2C platform continues to roar ahead (customers up 28% year-on-year).TYes, the P/E multiple is close to 20x but for a leader that's growing rapidly in a mature industry - with a cost advantage over Hargreaves Lansdown - it makes sense that it should be highly valued. The QualityRank is 93 and the StockRanks judge it to be a High Flyer. Until there is a change in the big picture, I'll be staying GREEN on this. | |

Resolute Mining (LON:RSG) (£1.69bn | SR71) | Q1 2026: gold production of 59,603 ounces (Q4 2025: 65,918oz) in line with expectations at both Mako (Senegal) and Syama (Mali). All-In Sustaining Costs of $2,210/oz (Q4 2025: $1,877/oz) in line with guidance. High royalty payments due to record gold prices. On track to meet production guidance of 250-275 koz. | ||

WH Smith (LON:SMWH) (£795m | SR37) | Revenue +5%. Headline group profit before tax and non-underlying items £3m (2025: £21m). “In light of the uncertainty arising from the conflict in the Middle East… more cautious outlook reflecting the impact on passenger numbers and weaker consumer confidence.” FY26 Headline Group profit before tax and non-underlying items expected to be £90m - £105m. | RED = (Graham) | |

Dominos Pizza (LON:DOM) (£706m | SR66) | “...An encouraging start to the year, with positive total system sales, like‑for‑like sales and order growth.” LfL system sales +5.8%. “The Board currently expects to achieve our earnings expectations for the full year.” | ||

Young & Cos Brewery (LON:YNGA) (£488m | SR90) | Total managed house revenue up 4.6% for the 52-week period, like-for-like sales up 4.7%. “...trading for the full year is expected to be in line with management's expectations.” | ||

Metals Exploration (LON:MTL) (£441m | SR94) | “A period of mixed success”. Q1 2026 gold revenue of US$52.9 million (Q4 2025: US$63.9 million). Fewer ounces sold this quarter (10,800 vs 16,000). Revised gold production guidance of 40,000 - 48,000 oz, reflecting BIOX circuit disruption from artisanal cyanide contamination in Stages 5 and 6, a geological model downgrade following grade control drilling, and the impact of historical illegal small scale mining activity on recoverable ounces. | BLACK (AMBER/RED ↓) (gold production guidance revised lower) (Mark) We’ve been broadly positive on most UK-listed gold miners given the rise in gold price and the knock on impact on profitability, which has not always been fully priced by the market. However, problems here are becoming the norm, and hence I have little trust that they will deliver as expected.It is not necessarily expensive, and will do well if gold continues to rise. However, it now looks like it is performing badly operationally compared to other UK-listed gold producers and I think our rating should reflect that relative performance. | |

XP Power (LON:XPP) (£417m | SR72) | Q1 Order intake +38% to £79.1m, Revenue -4% to £51.8m (+3% CCY). Net debt £41.8m, similar to year end. Full year expectations are unchanged, including for a second half weighting. | ||

RWS Holdings (LON:RWS) (£313m | SR82) | H1 Revenue £360m +7% organic CCY. Adj. PBT +33% to £24m. Cash generation strong, net debt £33m. “Momentum continues to build, underpinning our expectations for a full year performance in line with guidance." | GREEN = (Mark - I hold) This company is very cheaply rated for such a high-quality and cash-generative business. However, it has been blighted by repeated profit warnings over the last few years. Many will have been expecting further trading weakness today, but with in-line trading confirmed and a return to growth at both the top and the bottom line forecast, I can see why the market likes today’s update. This appears to have finally turned a corner and I see no reason to change our positive view. | |

Anglo Asian Mining (LON:AAZ) (£280m | SR47) | Gedabek flotation plant upgrade is on course to be completed by the end of April. The nine newly-installed, high-efficiency Imhoflot pneumatic flotation cells are designed to deliver rapid mineral recovery from higher grade ores. | ||

Asos (LON:ASC) (£269m | SR37) | SP +9% H1 Revenue -14% to £1.11bn, Adj. EBITDA +51% to $64m, Adj. LBT £52.4m (25H1: £69.5m LBT), Net debt £294.9m (25H1: £275.8m). Current trading is in line with expectations. | ||

Fintel (LON:FNTL) (£193m | SR39) | Disposal of two non-core assets to Kairos Professional Services, owned by former joint CEO for £1m (£0.6m up front). Combined businesses had £11.2m revenue & £0.9m EBITDA. Removes insurance liabilities & client funds custody risk. | ||

Afentra (LON:AET) (£178m | SR98) | 0.517 mmbbls sold in Jan at $65.4/bbl average price: generating $33.8 million revenue, 0.5 mmbbls to be sold in April expected to generate ~$50 million proceeds after hedging. Net debt $12.6m at 31 Mar. Strategic review process announced on 19 March 2026 is ongoing | ||

Mkango Resources (LON:MKA) (£168m | SR9) | HyProMag has produced 9.2 tonnes of recycled NdFeB alloy powder to date following commissioning of the HPMS vessel last year, of which 7.4 tonnes has been shipped to customers. | ||

Phoenix Spree Deutschland (LON:PSDL) (£154m | SR51) | Financial results for the year ended 31 Dec 2025 & Compulsory Redemption | Gross rental income -19% to €22.7m, LBT €13.6m (FY24: €39.5m LBT). | |

Foxtons (LON:FOXT) (£130m | SR55) | Q1 Revenue -10% to £39.6m (Lettings +5%, sales -35%, Financial Services +3%). Cost‑reduction programme targeting at least £3m of annualised savings underway. | ||

EnSilica (LON:ENSI) (£77.8m | SR56) | Entered into two landmark development contracts with a leading European satellite operator to develop two chips for its next-generation satellite network. potentially worth in excess of $50 million from 2030. Initial non-recurring engineering revenue $6.8m from 2026-28. | ||

Journeo (LON:JNEO) (£75.1m | SR51) | Crime and Fire Defence Systems has secured new contracts with a total value of £1.0 million under a five-year framework agreement, with a major UK utility company. Expected to complete in 2026. | ||

Ondine Biomedical (LON:OBI) (£62.3m | SR5) | “University of Ottawa Heart Institute…found notable results in patient safety following the integration of Steriwave nasal decolonisation into its presurgical protocols.” | ||

Oxford Metrics (LON:OMG) (£56.4m | SR70) | H1 Revenue +3% to £20.7m, modestly improved Adjusted LBIT versus prior year period. Management expectations for FY26 remain unchanged. H2 weighting. Heightened macroeconomic uncertainty has affected the timing of certain orders and led some customers to defer project start in IVMS. Net Net Cash £31.7m (FY25: £37.3m). | ||

Atome (LON:ATOM) (£46.6m | SR17) | Funding longstop date extended further to 24 Apr. | ||

Carclo (LON:CAR) (£39.4m | SR80) | Revenue -6% to £114m, Overall Overall trading performance in line with management expectations. Net debt £24m (FY25: £19.3m). | AMBER/RED = (Mark) | |

Lendinvest (LON:LINV) (£37.8m | SR31) | FY26 originations £1,437m, record quarterly originations of £415m in Q4 FY26. Buy-to-Let originations of £917m in FY26. Short Term Mortgages delivered record offers of £113m in Q4. “The Group enters FY27 with its largest pipeline to date, providing strong visibility on forward lending.” | ||

Creightons (LON:CRL) (£16.1m | SR70) | FY26 revenue -1% to £53.8m, PBT -23% to £2.7m, blamed on NIC & NMW increases. Near-term market conditions uncertain. | AMBER = (Mark) This trading update reveals a weak H2 for both sales and trading profits. PBT in H2 will have declined from £1.8m last year to £1.2m in the year just finished. It is nice to finally have some forecasts in the market. However, again the numbers aren’t particularly impressive with FY26 EPS below FY25. Overall, the forecasts highlight that the company is cheap, but perhaps cheap for a reason, given the lack of any material earnings growth, and potential consumer and inflationary headwinds. Until they show investors they can develop a habit of meeting or even exceeding these forecasts, I maintain our previously neutral view. | |

Powerhouse Energy (LON:PHE) (£13.2m | SR2) | 200m shares at 0.2p (33% discount to last night's 0.3p close) raising £400k gross + £250k retail offer at the same price. | ||

Diales (LON:DIAL) (£12.4m | SR96) | H1 Continuing Revenue +9.7% to £23.7m, U/L operating profit +43% to £1.0m. FY26 results at least in-line with market expectations. Cash position £3.9m (FY25: £3.0m). |

Graham's Section

J Sainsbury (LON:SBRY)

Down 5% to 335.2p (£7.6bn) - Preliminary Results - Graham - BLACK (AMBER ↓)

These results look fine - pretty close to market expectations for FY March 2026.

But a downbeat outlook, and a profit downgrade, has put a dampener on the share price this morning.

Let’s quickly review the FY March 2026 figures:

Retail sales +4.3% (excluding fuel and VAT)

Retail underlying operating profit £1,025m (down 1.1%)

Underlying PBT £718m (up 1.3%)

Net debt has improved slightly, year-on-year, to £203m.

ROCE deteriorates only marginally to 8.9%.

So far, so normal.

Underlying operating profit was supposed to be £1,033m, according to consensus, so this is a very small miss.

But the outlook is where things take a turn for the worse, despite a positive start to the year:

We are in a strong competitive position after another year of good progress. We have made a positive start to the new financial year, with grocery volume growth ahead of the market. Argos trading continues to reflect a subdued general merchandise market.

We will continue to make deliberate, balanced choices to sustain this strong competitive position in the year ahead and expect to continue to outperform the grocery market. The conflict in the Middle East will impact both our customers and our business. The duration and extent of these impacts is very uncertain and this is reflected in our profit guidance, where we currently expect to deliver Total underlying operating profit of between £975 million and £1,075 million. We continue to expect to deliver Retail free cash flow of more than £500 million.

I believe that underlying operating profit was supposed to come in higher than this, at around £1.1 billion.

At the midpoint, this is a downgrade of c. 7% against market expectations. And with a pretty wide range around that midpoint, which is almost as bad as the downgrade itself.

While the conflict in the Middle East is blamed, there’s also a voluntary element to this downgrade, with the company emphasising its desire to grow ahead of the wider market.

This is part of the strategic commitments made in 2024:

Two years into this plan, they have “sustained our strong competitive position in an intensely competitive market”. The cost? Underlying operating profit that isn’t going anywhere quickly. “Profit leverage from sales growth” hasn’t been delivered:

The underlying profit leverage from this volume outperformance was offset by investment in our competitive position and by unusually high levels of operating cost inflation, only partially mitigated through the delivery of a further £330 million of structural cost savings.

They have the “biggest Aldi Price Match in the market”, which must be expensive, and 10,000 Nectar offers each week.

Estate growth is limited: only ten new supermarkets opened in the year, and with another ten planned for the year ahead (with convenience stores on top of that number).

Groceries Online: sales up 13%.

Argos: sales were up 0.7% “in a highly competitive market” Profits were “broadly in line with last year”. I’m surprised they are even able to tread water, considering that Argos attempts to compete in so many different categories.

Graham’s view

I was positive on this in November last year, and the market cap is only a little lower now than it was then.

Given the profit warning, and the limited visibility, the time is right for us to downgrade our stance.

If it was just a profit warning, with a 7% downgrade to expectations, that would be one thing.

But if underlying operating comes in at the low end of the range (£975m), that will be an 11% miss against prior expectations. It will also be a 5% reduction in profit against the prior year.

The company was highly rated for a supermarket:

That was fine when modest profit growth was expected.

But as that is no longer the case, my interest evaporates at the current valuation.

I’m neutral now.

The StockRanks already categorised this as "Neutral", so they beat me to it:

WH Smith (LON:SMWH)

Down 11% at 561.45p (£710m) - Interim Results Announcement - Graham - RED =

The 5-year chart here makes for unpleasant viewing:

The bad news continues today with a cautious outlook statement, arising from the Middle East conflict and its impact on passenger numbers and consumer confidence.

Although this is a company I’ve long admired, we’ve been fully negative on it since December (previously AMBER/RED and before that neutral).

So I think we’ve been appropriately cautious, given all the negative news flow around it.

Today’s interims:

H1 revenue +5% at constant currencies, led by North America +10%

“Headline Group profit before tax and non-underlying items” £3m (H1 last year: £21m, restated after accounting errors).

The use of a “Headline profit” figure always makes me nervous, as I assume that it involves more adjustments than the simpler “adjusted profit” would.

The actual PBT result in H1 is a loss of £25m, compared to a loss of £4m in H1 last year (restated for accounting errors).

Trading update: H1 ended in February. Like-for-like revenue growth in the seven weeks since then is 2%.

Things are always obvious in hindsight:

By division, the UK delivered flat LFL revenue growth, largely reflecting a softening in Air following disruption to flight schedules to the Middle East. In North America, LFL revenue growth was 2% with the core Travel Essentials business continuing to perform well with LFL revenue growth of 6%. Rest of the World delivered LFL revenue growth of 5%.

This leads to new planning assumptions for the year:

In light of the uncertainty arising from the conflict in the Middle East, the Group is taking a more cautious outlook reflecting the impact on passenger numbers and weaker consumer confidence. Much will depend on the peak summer trading period and the Group assumes no immediate improvement in consumer confidence and assumes that jet fuel supplies can be maintained. At this stage, the Group expects to deliver FY26 Headline Group profit before tax and non-underlying items of £90m - £105m.

I think that adjusted PBT for the year was supposed to be more like £115m, not £90-£105m. So this is currently heading for a significant miss against expectations.

“Headline net debt” is expected to finish the year around £420m. At the end of H1, it was £496m.

Graham’s view

It’s all gone a bit wrong for a company that was buying back its own shares last year.

It’s pretty clear that our negative stance has to remain in place today: it’s carrying too much debt relative to adjusted profits, and I don’t trust that the bottom line (without adjustments) will be particularly impressive.

It’s a combination of bad luck, along with some self-inflicted injuries - notably accounting errors and an overly aggressive balance sheet.

The StockRanks are still neutral, but I’d be steering clear:

Mark's Section

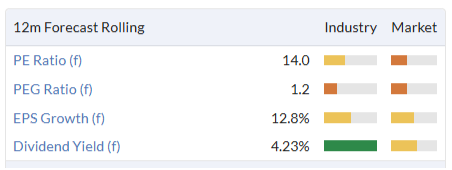

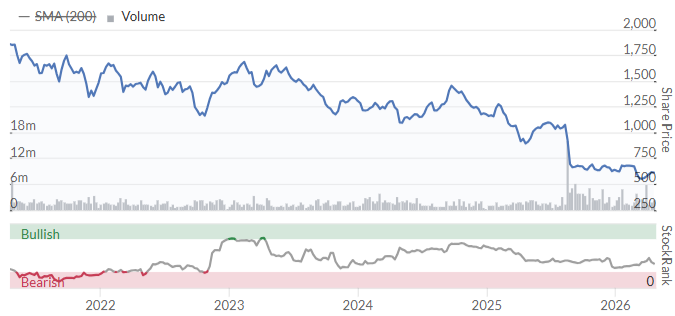

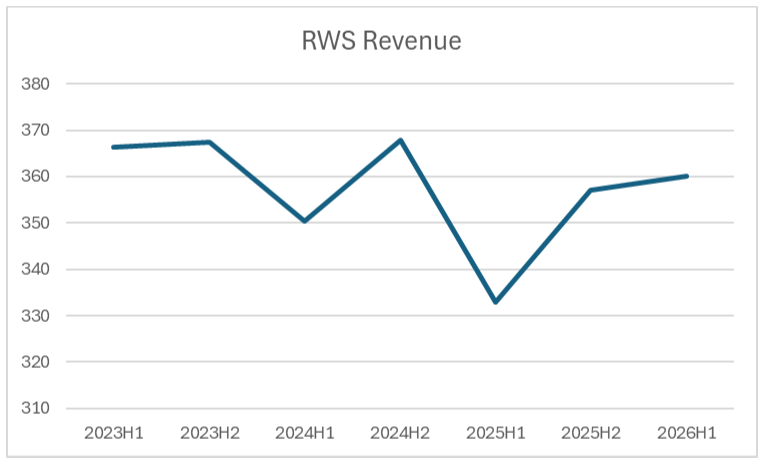

RWS Holdings (LON:RWS)

Up 10% at 92p - Trading Statement - Mark (I hold) - GREEN =

[At the time of writing, I have a long position in this company.]

The overall revenue trend in this announcement doesn’t seem much to write home about:

Reported revenue is expected to be approximately £360m, a c.5% increase on prior year.

However, like much in investing, the direction of travel matters more than the absolute value. In this case, this represents a stabilisation of recent negative trends and a potential recovery underway:

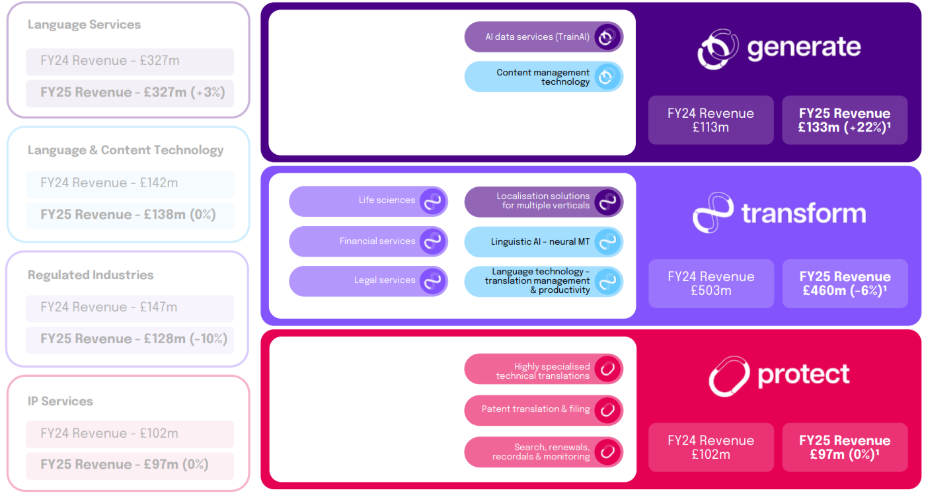

The company changed its segmental reporting with the 2025 full year results, and here is how the previous reporting maps into the new structure:

Generate: This is the content management technology together with the new TrainAI initiative, and this is the stand-out performer in today’s trading update:

Generate delivered strong double-digit OCC¹ revenue growth, with an exceptional performance in the TrainAI business unit driven by additional programmes with existing clients and initial revenues from a new technology client. We expect this segment to sustain strong growth, as anticipated, in the second half.

I have some concerns about this segment. I can understand companies wanting to train their AI systems on RWS’ extensive database of high-quality translations and being willing to pay handsomely to do so. However, I don’t understand how RWS are avoiding training competitors who are going to undercut their core services. Management have never given an adequate explanation of their guardrails to prevent this, as far as I have seen. I think the impact of AI on their business model may be less than the market is currently pricing; in my opinion, corporate clients will still pay for RWS reputation and quality, rather than going with a vibe-coded start-up.

Backing this ups is that so far, their own translation LLM seems to be ahead of competitors, with them saying:

On 25 March RWS launched Language Weaver Pro, the largest dedicated translation model in production. Developed in partnership with Cohere, Language Weaver Pro ranked first in 31 of 32 languages in benchmarking tests, outperforming industry-leading AI translation tools - including DeepL and Gemini - across both sentence- and paragraph-level datasets in factual and more challenging marketing-related content.

However, I’m not sure the TrainAI strategy is the right one, even if it has given a short-term boost to revenue.

Transform: This segment continues to decline, as they expected, but client wins may help a partial recovery in H2.

Protect: This is the new name for IP Services where they say saw good revenue growth.

Profitability:

The combination of cost cutting and a return to revenue growth means that adjusted PBT grows by 33% to £24m for the half year. However, this is off a low base.

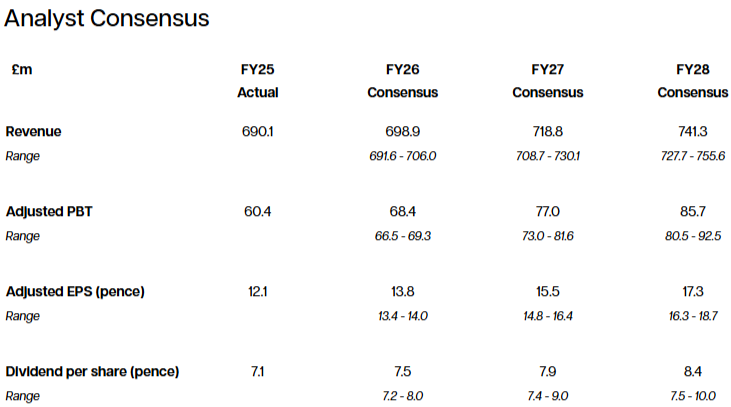

More importantly, the company guides that they will be in line for the full year. We can’t read the research here. However, the company do provide a consensus on their website:

If they deliver this, then the company is certainly showing signs of recovery:

However, it is worth noting that the consensus implies that H2 will be weaker than H1 on revenue and we have been critical of the scale of adjustments they have made in the past.

This could be taken one of two ways: either they look likely to beat on revenue for the Full Year, or miss on Adj. PBT.

Valuation:

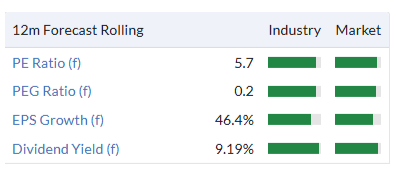

One of the reasons the market liked this trading statement is that the company is priced very cheaply:

This will not look quite as good once today’s share price rise is included in these calculations, but this remains one of the cheapest UK midcap stocks in the market.

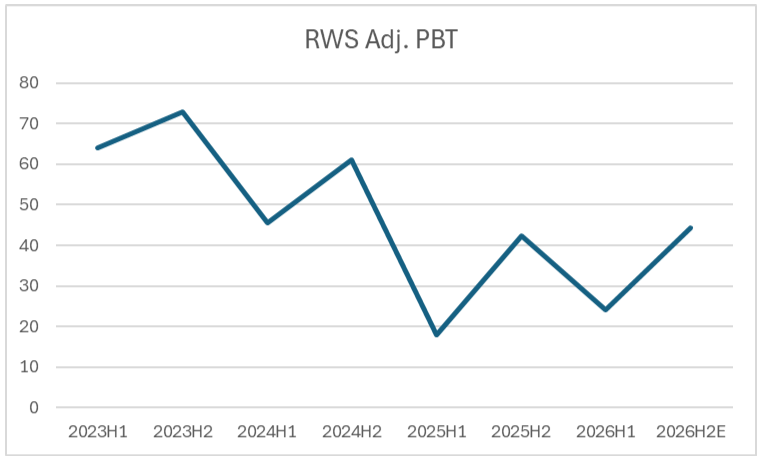

I think it's fair to say that many expected a further profits warning today. Consensus trends had not been encouraging:

They also say that cash flow is expected to be strong. The £33m net debt reported today is up by £7.6m from the £24.4m at the end of FY25. However, this includes £17m of dividend payments. Overall converting around half of Adj. PBT into FCF seems good.

Mark’s view

Roland kept our GREEN positive view when the company confirmed in line trading at their AGM in February. Today’s trading statement confirms that in line view, despite difficult global macro conditions. I still have some concerns over some aspects of the long-term strategy, and how reliant they are on adjustments to hit their figures. However, they are very cheaply rated for such a high-quality and cash-generative business. With a return to growth at both the top and the bottom line forecast, I see no reason to change our positive view.

Carclo (LON:CAR)

Down 12% at 47p - Trading Update - Mark - AMBER/RED =

The market has not liked today’s full-year trading update. Although, looking at the short term chart, this may be a case of buying the rumour and selling the news:

A revenue decline is always concerning. However, they are keen to point out that this is due to exiting lower margin work, and the turnaround strategy remains on-track:

Revenue is expected to be approximately £114m (£121m in FY25), reflecting the continuing rebalancing and careful management of our portfolio, along with completion of customer projects in Design and Engineering. We have exited low-margin, short-run work and concentrated the portfolio on regulated markets - life sciences and aerospace - where what we do genuinely matters.

The US appears to have been a problem for their CTP business, with them saying:

CTP Design and Engineering ("D&E") revenue improved in the second half of the financial year, as anticipated, but was below both management expectations and prior year run-rate due to lower customer activity in the US. EMEA customer project activity was ahead of both management expectations and prior year performance.

They say that they expect strong year-on-year EBIT growth and similar tax rate to previous years. However, they don’t give us any indicative figures.Thankfully, their broker, Panmure Liberum, have updated us saying:

Following the publication of the full year FY26 trading update we have left unchanged both our FY26 and FY27 EBIT estimates of £12.1m and £13.9m. This represents growth of 23% and 15% respectively and margins of 10.6% and 11.5% and is in spite of lower revenues in FY26 due to factory closures and FX translation losses at the revenue level.

While they may keep EBIT forecasts the same, revenue forecasts have been cut from £119m to £114m in FY26 and £125m to £121m in FY27.

Valuation:

Panmure Liberum calculates that the company trades at a modest forward P/E of around 10 for 2026, dropping to around 7 for 2027. However, the broker appears to be basing these figures on a calendar year basis rather than financial year. This is an approach that I find confusing, and it appears to be confusing the algorithms in Stockopedia, too.

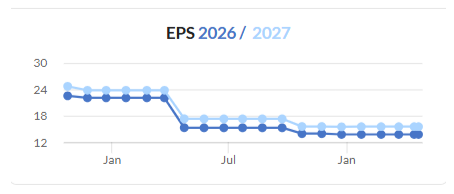

On a FY basis, FY26 has 3.7p EPS and FY27 5.8p, making the P/E figures more like 13x and 8x. Not expensive, but not as cheap as it may first appear, and reliant on them hitting forecasts for the current year, having already seen a revenue forecast cut today.

Net debt is up over the year from £19.3m to £24m, broadly in line with the level at the half year. Looking at the broker’s note it looks like this includes lease liabilities and is forecast to be 1.3x EBITDA. So this shouldn't be worrying from a solvency point of view, but requires adjusting valuation figures or using EV measures.

The factor that is missing from this is the pension deficit, which comes in at a whopping £44.7m at the half year, on an IFRS19 basis.

In some ways, a pension deficit is the best form of debt as it can’t be called. However, this still has to be paid from cash generated by the company, so should be reflected in any valuation. Here is the detail of those payments:

The deficit recovery plan agreed with the Trustees of the UK defined benefit pension scheme as part of the triennial valuation to 31 March 2024 includes an annual schedule of contributions of £3.5m through to 31 March 2029 and thereafter annual contributions of £5.8m indexed at 3.5% through to 31 March 2037. Contributions are funded from cash generated by operations and have been reflected in the cash flow and covenant forecasts reviewed by the Directors.

Using the IFRS19 number, at a 47p share price, I get a £34.3m market cap, but a £98m EV including the pension deficit, excluding lease liabilities. Panmure Liberum forecasts EBIT of £12.1m for FY26, and £13.9m for FY27. The EV/EBIT is around 8 dropping to 7. Again, this is not that expensive, but nowhere near as good as the calendar year figures that the broker gives us excluding the pension deficit of around 5 falling to 4x.

There is no dividend forecast, and that is almost certainly because the pension trustees will not allow this anytime soon.

Mark’s view

The company appears to be doing the right thing with their turnaround strategy. This update shows some weakness in revenue, but profitability forecasts are maintained. However, in the short and medium-term all of the benefits of this strategy are accruing to the former employees in the way of shoring up a large pension deficit. Shareholders will need to wait until the 2030’s or even beyond, before they will start to see the benefits of current management actions. As such, I maintain Graham’s previously cautious view of AMBER/RED.

Creightons (LON:CRL)

Down 8% at 21.55p - Trading update - Mark - AMBER =

Another unimpressive update from a small cap company this morning. In this case, I think there may have been signs that things weren’t going to plan. They had appointed Zeus as NOMAD on their move to AIM over a year ago, but the expected broker coverage hadn’t arrived until today. One may have surmised that with PBT declining 11% in their Half-year Results, they were reluctant to have forecasts in the market until the outlook was brighter.

This trading update shows them struggling with both revenue in H2 and costs. They say:

Revenue for FY26 is expected to be approximately £53.8 million (2025: £54.1 million).

Which means H2 revenue was £26.2m, down from £27m in H2 last year. PBT is said to be “approximately £2.7 million”, which means H2 delivered £1.2m PBT, some 30% below the £1.8m in the prior year H2. The blame is firmly put on a significant increase in employment costs:

The Group delivered a resilient performance during the year despite challenging market conditions and the impact of government legislation, including increases to employer National Insurance Contributions (NIC) and the National Living Wage (NLW), which we previously announced would have an annualised impact of £0.9 million on labour costs, comprising £0.4 million in direct costs and £0.5 million in indirect costs.

Valuation:

The initiation note from Zeus works this out to be 2.8p of EPS for the year just finished. This rises to 3.2p for FY27, which is still below FY25, with FY28 growing to 3.8p EPS.

On top of this they have net cash of £1.7m which is expected to rise to £3.1m in March 2027.

This puts the company at the cheaper end of the market, with Zeus calculating an FY27 P/E of 7.3 and an EV/EBITDA of less than 3. However, a small personal care products manufacturer, which has struggled to grow in recent years should be cheaply rated.

There is potential upside if they can return their higher-margin branded product sales to growth. However, Zeus also highlights increasing raw material costs, which is why their forecast sales growth fails to deliver material EPS growth.

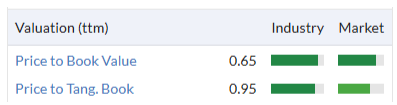

They do trade at a discount to tangible book value, and many investors rate the management team, meaning that if they can make these assets productive again profitability will improve further:

However, I am cautioned by Buffett’s words of wisdom around the relative power of management and business models!

Name change:

From now on the company will be known as Potter & Moore, the original trading name, which they say:

…better reflects the identity by which many of the Group's customers and all of its retail partners and trading stakeholders already recognise the business.

Sometimes a name change can reflect a genuine change in prospects for a business. However, it also may obscure the business for investors, for which Creightons has been relatively well-known amongst individual investors.

Mark’s view

While it is nice to finally have some forecasts in the market, the numbers aren’t particularly impressive. They highlight that the company is cheap, but perhaps cheap for a reason, given the lack of any material earnings growth, and potential consumer and inflationary headwinds. Until they show investors they can develop a habit of meeting or even exceeding these forecasts, I maintain our previously neutral view of AMBER.

Metals Exploration (LON:MTL)

Down 7% at 13.7p - Quarterly Update to 31 March 2026 - Mark - BLACK (AMBER/RED ↓)

I’m surprised this change of outlook has not been taken more badly by the market. In their Q4 results last year the company said:

FY2025 gold production of 65,287 ounces was at the lower end of the revised FY2025 lower guidance forecast at an AISC of US$1,368 /oz, which was above the upper FY2025 guidance forecast range of US$1,275 /oz due to the lower ounces sold.

This suggests that they were already struggling to meet guidance, and the FY26 forecast was already below the FY25 production number:

FY2026 gold production from Runruno forecast: 50,000 - 60,000 ounces. FY2026 AISC forecast for Runruno gold production: US$1,400 - US$1,650 /oz.

QWith Q1 under their belt, they are already making significant revisions to that guidance:

Revised FY2026 gold production guidance of 40,000 - 48,000 oz

That is a 20% cut to guidance, blamed on:

BIOX circuit disruption from artisanal cyanide contamination in Stages 5 and 6, a geological model downgrade following grade control drilling, and the impact of historical illegal small scale mining activity on recoverable ounces

This isn’t just a volume issue, because with gold mining there is an operational gearing impact:

Revised FY2026 AISC forecast for Runruno gold production: US$1,700 - US$2,000 /oz due to lower production levels.

Doing the maths, the midpoint of the previous guidance means that revenue goes from $258m to $207m, whereas costs stay roughly the same. This is a roughly $50m hit to PBT, and reduces it by about 20%.

Part of the lack of reaction may be that they also have the La India development project, and a lot of the value of the business is based on that:

No formal guidance is provided for the La India gold project which remains on track to commence gold production in December 2026. Guidance will be provided for FY2027.

However, the repeated downgrades in existing production means I don’t have a huge amount of faith for that to ramp up production without problems.

Mark’s view

We’ve been broadly positive on most UK-listed gold miners given the rise in gold price and the knock on impact on profitability, which has not always been fully priced by the market. However, problems here are becoming the norm, and hence I have little trust that they will deliver as expected. Since the share price doesn’t appear to have priced in the drop in profitability today, let alone any read through to wider development projects, I think we have to take a slightly negative view of AMBER/RED. It is not necessarily expensive, and will do well if gold continues to rise. However, it now looks like it is performing badly operationally compared to other UK-listed gold producers and I think our rating should reflect that relative performance, at least until there is clear evidence that La India is in production at expected rates.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.