Good morning!

President Trump has delayed fresh strikes on Iran for at least a few days, but “possibly maybe forever”. Gulf states including Saudi Arabia, Qatar and the UAE asked him to let talks continue.

The oil market has reflected the uncertainty: yesterday afternoon Brent Crude reached a low of $104 around 1pm, before jumping to $109.50 yesterday evening.

Interestingly, Trump met with Chinese leader Xi Jinping last week and discussed the possibility of lifting sanctions on companies that buy Iranian oil - this would be welcome news as China previously bought the majority of Iranian oil.

How does any of this apply to our daily company analysis? Honestly I think that for most companies, it’s not too relevant. Iran-related "macro uncertainty" is expressed primarily via oil and gas prices. Oil and gas prices are an important input for many companies, and they do have ripple effects throughout the economy, but frankly I think that most healthy companies are not so energy-intensive that they can't absorb a c. 50p increase in the price of diesel. Plenty of companies are still trading "in line" despite all of the negative headlines.

I think of the rise in energy prices as just another tax on business, and one that could be ended sooner than expected, whenever the conflict ends. In the meantime, consumers still need to consume. Life goes on.

Overnight market movements:

- The FTSE is set to open up 0.4% at 10,330

- S&P 500 is down 0.3% at 7,383

- Brent crude at $110

- Natural gas at 122p per therm

We're finished for today, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Standard Chartered (LON:STAN) (£43bn | SR88) | New medium-term targets: RoTE >15% in 2028, building to ~18% in 2030. High-teens EPS CAGR and 5-7% income CAGR from 2025-2028. | ||

Fresnillo (LON:FRES) (£25bn | SR88) | 2025: silver production was in line with guidance, while gold was ahead of guidance. “The longer-term outlook is positive. We anticipate that at least one of our advanced prospects will join our development portfolio in the coming two to three years.” | ||

Diploma (LON:DPLM) (£8.9bn | SR75) | Organic revenue growth 15%. Adjusted EPS growth 36% to 109.2p. Upgrade to FY26 guidance: organic revenue growth to be 12% (previously 9%) and operating profit growth to be over 30%, which is a 6% upgrade to consensus. | AMBER/GREEN = (Roland) A very strong set of half-year figures with another upgrade to full-year guidance. My impression is that this business is another indirect beneficiary of the AI data centre boom in the US. I also note continued strong contributions from acquisitions and impressive overall profitability. I am a long-term fan of this business and can’t really fault today’s update, but the outlook for next year suggests slower growth. When paired with a demanding valuation, this means that I’m leaving my previous moderately positive view unchanged today. | |

IG group (LON:IGG) (£5.2bn | SR93) | SP +9% Q1 organic total revenue up 19% year-on-year. ”2026 guidance upgraded to organic total revenue growth of 10-15%... ahead of prior guidance of high single-digits… Medium-term outlook upgraded to at least 10% organic total revenue compound growth per annum.” | GREEN = (Graham - I hold) I'm a happy holder and excited about what IG might achieve next. The Strategic Review in particular is very interesting, and could accelerate returns for shareholders - e.g. a US listing could, I think, result in a sharply improved valuation. Why buy IBKR at over 30x earnings when IG Group is available at less than 15x? | |

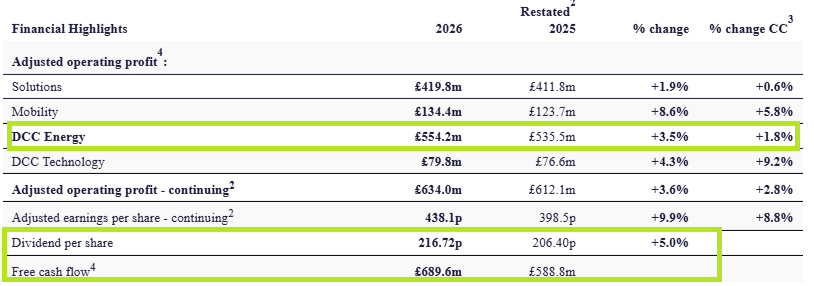

DCC (LON:DCC) (£5.1bn | SR95) | Adjusted continuing operating profit up 3.6% to £634m. Actual profit after tax from continuing operations of £286.9m (2025: £307m). Changing name to DCC Energy Plc. “...our performance keeps us on track to deliver our £830 million operating profit ambition by 2030”. | GREEN = (Roland - I hold) This Irish energy distribution group recently received a half-hearted takeover approach in April, but as Mark discussed, it fell well short of a reasonable price – the shares are now trading comfortably above the price offered. Today’s results highlight the appeal of the core energy business, with adjusted operating profit up 3.5% to £554m. While I recognise some risks around DCC’s efforts to expand its lower-carbon offerings, the shares continue to look too cheap to me at current levels, even without factoring future growth prospects. This is a long-term holding for me and I am biased, but I continue to view this business as fundamentally undervalued by the market, so I’m leaving my positive view unchanged today. | |

Cranswick (LON:CWK) (£2.8bn | SR64) | Revenue +9.5%. Adjusted PBT +11.2% (£220m). Actual PBT +18.8% (£215.8m). "Trading in the early part of the current financial year has been in line with the Board's expectations.” Shore Capital updated estimates: - FY27E adj EPS: 312.5p (+1.8% vs 307.1p previously) - FY28E adj EPS: 327.9p (+1.7% vs 322.4p previously) | AMBER/GREEN = (Roland) [no section below] Not many companies can report 36 years of unbroken dividend growth, as food producer Cranswick does today. In a competitive and somewhat capital-intensive sector, I see this company as an excellent operator. Today’s results flag up continued investment in expanded facilities and reassure on profitability, with a return on capital employed of c.17%. This is consistent with mid-teens results in recent years and shows the company’s ability to expand by deploying capital at attractive rates of return. This is one of the factors that has driven the 140% share price growth over the last decade. Today’s upgrade from house broker Shore Capital is described as conservative and it probably is. But there are a number of potential headwinds out there and my feeling is that Cranswick’s share price is probably about right at the moment. For these reasons, I’m leaving my moderately-positive view unchanged. | |

Currys (LON:CURY) (£1.39bn | SR89) | Performance continues to strengthen (full year trading update) | LfL sales +4% for the 16-week period since “Peak” and for the full year. "Recent trading has been very solid; we've not yet seen an impact from the Middle East conflict, and our energy costs are well hedged for the coming year.” | GREEN = (Roland) A strong finish to FY26 suggests CEO Alex Baldock will leave on a high later this year, when he is due to become CEO of Boots. Shareholders may be sad to see him leave, but my impression is that he will leave behind a business that is genuinely better than the one he inherited and could continue to perform well. A FY27 P/E of 10 seems reasonable and I’m happy to maintain our positive view today following yet another earnings upgrade. |

SSP (LON:SSPG) (£1.19bn | SR30) | Sales +6.2%. Net debt/EBITDA at 2.2x, expected to reduce by full-year. Adjusted operating profit +9.3% at actual FX rates to £50m, +17.8% at constant FX rates. Full year outlook: “The Group as a whole is currently trading solidly… our expectations for FY26 EPS remain within the market consensus range of 13.6p - 14.8p…” | ||

Renew Holdings (LON:RNWH) (£703m | SR91) | £9m acquisition of Electricity Distribution Engineering Services Ltd, which is “a provider of high voltage engineering design services to the energy distribution market for both underground and overhead lines”. | ||

Discoverie (LON:DSCV) (£662m | SR46) | Cash consideration of $67.5m, funded from DSCV’s existing debt facilities. 3Gmetalworx is “a North American-based designer and manufacturer of electromagnetic shielding products for the electronics industry.” DSCV buys a 90% stake, with management at 3G retaining 10%. | ||

Dr Martens (LON:DOCS) (£622m | SR74) | Revenue down 1.4% at constant currencies, but adjusted PBT up 61% to £55m. Without adjustments, actual PBT for the year is £32.7m (2025: £8.8m). “...our business is now well setup to deliver both our FY27 objectives and medium‑term targets." | AMBER ↑ (Graham) | |

Hilton Food (LON:HFG) (£486m | SR77) | On track to achieve 2026 adjusted profit before tax in the range £60m-£65m. | ||

Thor Explorations (LON:THX) (£473m | SR100) | Q1: 15,417 ounces of gold sold (Q1 2025: 22,750) with an average gold price of US$4,820 (Q1 2025: US$2,720). Net cash $178m. Production guidance for FY 2026 of 75,000 - 85,000 oz with an AISC guidance of US$1,000 - $1,200. | ||

C&C (LON:CCR) (£404m | SR82) | Net revenue down 5.7%, adjusted operating profit down 6.6% (€70.5m). “Significant simplification activity was delivered across the business.” Outlook: Trading performance since the period end has been in line with expectations… we currently expect to meet full-year financial objectives.” | ||

Avacta (LON:AVCT) (£387m | SR32) | “Increased momentum and strengthened position as a pure-play oncology biopharmaceutical company by focusing on the Company's unique proprietary pre|CISION® peptide drug conjugate platform, with significant progress in R&D programs.” Operating loss of £30.7m and after interest expense the loss before tax was £36.8m. Cash runway into early Q1 2027. | ||

Luceco (LON:LUCE) (£378m | SR95) | Organic revenue growth 11%. “...the strength of Q1 trading and sustained Energy Transition momentum mean expectations for full-year 2026 Adjusted Operating Profit now exceed £40m, with the potential for further significant outperformance dependent on Demand Flexibility.” | GREEN ↑ (Graham) Maybe Luceco is a higher-quality business than I’ve been giving it credit for? Especially with its foray into EV chargers. I’m upgrading it thanks to the upward trend in EPS forecasts that has been maintained today. This isn’t my typical GREEN: I’m simply noting the very strong momentum in the business. And it's a little expensive for what it is, but perhaps not yet excessively so. I wouldn’t upgrade it, if it was already at 20x earnings (currently at 14x). | |

Mears (LON:MER) (£343m | SR98) | Mears will deliver all repairs, compliance and planned investment works. Contract valued at £24m/yr over five years, with an option to extend for a further five years. | ||

Forterra (LON:FORT) (£315m | SR68) | Trading conditions remain challenging, with LFL revenue -11%. Domestic brick despatches 11% in Q1. Outlook: elevated uncertainty means the range of full-year outcomes is greater than previously anticipated. | ||

Victorian Plumbing (LON:VIC) (£258m | SR88) | Revenue +10.5%, adj pre-tax profit down 20% to £9.4m. Outlook: expects full-year revenue and adj PBT in line with market expectations. | ||

Empire Metals (LON:EEE) (£255m | SR5) | Sold Empire’s 75% interest in the Eclipse ML for A$750,000. | ||

Winvia Entertainment (LON:WVIA) (£250m | SR47) | Net revenue £170.3m (FY24: £38.1m), operating profit £12m (FY24: £5.9m). Net cash increased to £29.9m (2024: net debt £36.6m). Outlook: Q1 trading “strong”, on track to meet full-year expectations. | ||

Capricorn Energy (LON:CNE) (£228m | SR98) | Further to its announcement of 22 April 2026, Capricorn Energy confirms that it does not intend to make an offer for Deltic. | ||

Jadestone Energy (LON:JSE) (£172m | SR70) | Revenue +3% to $408m, with adj EBITDAX +20% to $153m and loss after tax of $110.7m. Production +6% to 19,829 boe/d. Stag field remains shut in. 2026 guidance unchanged (18-21k boe/d). | ||

Crest Nicholson Holdings (LON:CRST) (£170m | SR46) | Remains in discussions with lenders regarding covenant relaxation. This is expected to conclude by mid-July 2026. Results are delayed to allow time for “the covenant reset process” and for audit review. H1 results now expected on 16 July 2026. | ||

Regional REIT (LON:RGL) (£144m | SR46) | Sales proceeds of £12.6m in Q1. All were “close to” Dec 25 valuations. LTV reduced to 39.4% (2025: 40.4%). Completed 26 new lettings/renewals, adding £1.1m to rent roll at 9.8% above ERV. Q1 portfolio occupancy 75.6% vs 78.9% one year earlier. Q1 dividend of 2.0p per share. | ||

EKF Diagnostics Holdings (LON:EKF) (£116m | SR67) | Trading for the year ended 31 Dec 26 was in line with expectations. Currently on track to deliver FY26 revenue and adj EBITDA in line with expectations. | ||

Topps Tiles (LON:TPT) (£67m | SR66) | Pro forma revenue -0.2% with pre-tax profit down 74% to £0.5m. LFL revenue has turned positive during the first seven weeks of the second half. Outlook: expect full-year profit growth in line with market expectations. | ||

Frenkel Topping (LON:FEN) (£62m | SR79) | Deadline for the completion of the takeover scheme has been extended from 29 May 2026 to 29 July 2026, subject to court approval. The reason for this is that change of control approval may not be obtained before 29 May 2026. | PINK | |

Water Intelligence (LON:WATR) (£43m | SR70) | FY26 guidance is unchanged. Revenue +9%, with US B2B insurance and property management +16% and non-US +38%. Adj EBITDA +8% to $4.4m. | ||

Novacyt SA (LON:NCYT) (£32m | SR25) | Yourgene® Insight DPYD is a simple-to-use genotyping test that can identify cancer patients with Dihydropyrimidine Dehydrogenase (DPD) deficiency, which can cause severe and sometimes lethal side effects in patients being treated with chemotherapeutic drug 5-Fluorouracil (5-FU). | ||

Tortilla Mexican Grill (LON:MEX) (£28m | SR80) | FY24/FY25 accounting adjustments: operating expenditure in France totalling up to £2.5m has been identified which was not expensed through the income statement during the relevant period. FY25 adj EBITDA now expected to be c.£1.5m, c.£2.5m lower than previously indicated. | ||

Artisanal Spirits (LON:ART) (£22m | SR11) | “Solid start to the financial year”, trading in line with expectations with FY26 guidance unchanged. Growth in US and Asia is helping to offset a slower start in Europe. | ||

IXICO (LON:IXI) (£15m | SR18) | Revenue +23%, gross margin improved to 53% (H1 25: 50%), EBITDA loss reduced to £0.5m. Order book +38% to £18.1m. Outlook: remain focused on delivering guidance for 15% revenue growth in full year. | ||

EMV Capital (LON:EMVC) (£13m | SR25) | Final Results for the year ended 31 Dec 25 & Phantom Carried Interest Scheme | Fair value of investments +9% to £14.6m, with revenue +17% and group losses reduced to £0.6m (2024: £3.7m). PCI is a new long-term incentive scheme. | |

React (LON:REAT) (£11m | SR39) | Revenue +9%, adj EBITDA +7% to £1.5m. Net H1 net loss of £72k (1H25: £280k loss). Strong contribution from Aquaflow acquisition, stable workload, but decision cycles remain extended. |

Graham's Section

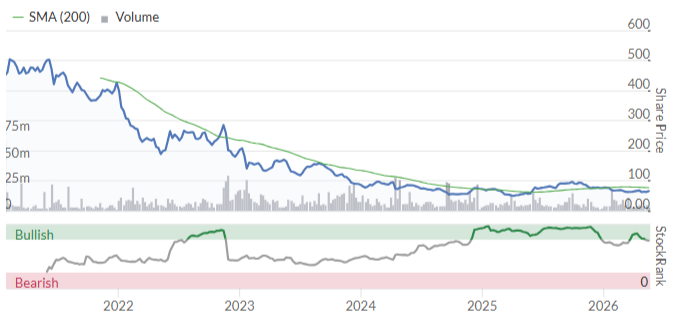

IG group (LON:IGG)

Up 9% at £17.13 (£5.7bn) - AGM Trading Update - Graham - GREEN =

(At the time of writing, Graham has a long position in IGG.)

I should say up front that this is no ordinary holding for me - it’s 19% of my portfolio, a long-term holding, and a multibagger.

3-year chart:

Today’s AGM update keeps the good news flowing:

Q1 organic revenue up 19% year-on-year to £331.2m (total revenue £340m)

Q1 organic first trades up 63% year-on-year, active customers up 12%

“IG is establishing a powerful challenger position in stock trading and crypto” - ever since they created it, I’ve held the view that their share dealing product is excellent (a quality product offering excellent value), although it doesn’t create the rich profits that spread betting and CFDs can do with a smaller customer base.

Guidance:

2026 guidance upgraded to organic total revenue growth of 10-15% on the 2025 base of approximately £1,100 million, ahead of prior guidance of high single-digits, with EBITDA margins sustained in a mid-40s percent range

So let’s provisionally call that an upgrade of c. 5% on revenues.

Medium-term guidance also improved:

Medium-term outlook upgraded to at least 10% organic total revenue compound growth per annum beyond 2026 on the 2025 base, with EBITDA margins sustained in a mid-40s percent range

Looking back on prior updates, the company previously guided for “mid-to-high single-digit percentage annual organic total revenue growth” in the years following May 2026, i.e. 5% to 9% growth.

With new guidance for growth of 10%+, let’s call this a guidance upgrade of 3%+ on revenues for 2027 and beyond.

This is a business that thrives on financial volatility - one of the reasons I like having it in my portfolio. It’s a natural hedge, if you will. Because while the US-Iran conflict has inflicted enormous human costs, it has also triggered a surge in trading: IG notes that Q1 saw “elevated commodity market volatility driving higher activity among existing customers”.

The conflict began in late February/early March, and it’s pretty clear that April and May must have been strong too, considering the raised guidance for the year and for the medium-term. Indeed:

IG has continued to trade well in the first seven weeks of Q2 2026, with underlying commercial momentum continuing to build. First trades remained strong and the organic active customer growth rate has accelerated beyond 12% year-on-year.

Quarterly Divisional performance

Let’s quickly review the major sources of revenue:

The core business “OTC derivatives” saw a 26% year-on-year surge in revenues (£250.6m)

The much smaller “stock trading & investments” business grew 38% organically, or 79% if you include the acquisition of FreeTrade (£19.6m).

Exchange traded revenues were solid, up 7% year-on-year (£40.7m).

Meanwhile, lower interest rates were a drag on interest income (£26.6m).

Graham’s view

Personally, I’m comfortable with this being a very large position in my portfolio. At some point, I may need to trim it, but that time has not arrived yet.

The company’s success has been supported by a positive environment for trading platforms (see the likes of Plus500 (LON:PLUS)), but also by the company’s own strong execution and position.

The most recent wins have been on the marketing front - which caused the surge in “first trades” in Q1, and the upgrade of medium-term guidance:

Marketing efficiency is accelerating active customer growth, multi-product adoption is strengthening, and customer income retention is trending higher.

I have typically used multiple IG products at the same time, so I know all about “multi-product adoption” and how they package multiple account types together. It’s very smooth.

Indeed, they recently came back to Ireland with their share dealing product, having left us for a few years. I’ve witnessed first-hand some of their marketing strategies - including dropping free FTSE-100 shares into new customer accounts! A nice touch.

The ongoing Strategic Review is also very interesting. As I’ve said before, I think Breon Corcoran is going to consider some radical structural changes. He has done this successfully in the past - watch this space.

…the Board is conducting a strategic review which is evaluating routes to maximise shareholder value, including, but not limited to, acquisitions to accelerate growth, IG's domicile and listing venues to unlock capital and enhance strategic flexibility, and potential combinations of parts of the Group with other industry participants. The Group will present the outcome of the review at a Strategy Update in autumn 2026.

A simple change such as a US listing would be one way to boost the valuation - I’m sure that US investors would be very interested. Many of them will already know IG Group personally, e.g. due to its ownership of tastytrade.

Because the valuation is still not excessive, at least to my eyes, despite the company’s success. I can't imagine the stock trading at this multiple in the US:

Interactive Brokers (NSQ:IBKR), for example, trades on a P/E multiple of 32.7x, with forecast EPS growth in a similar ballpark.

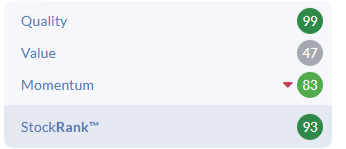

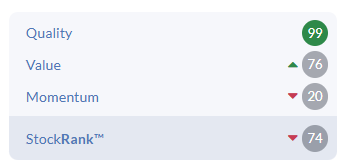

Indeed, with enormous returns and margins, IG enjoys a QualityRank of 99, and is a Super Stock:

So what could go wrong?

Flat, boring markets would slow down trading activity (e.g. VIX below 15)

The company might overpay for a major acquisition, or get involved in a merger that doesn’t work.

Regulators might start to pick on the industry again. It has been 7 years since the last major overhaul.

Personally, I’m a very happy holder here, and excited about what IG might be able to achieve next.

Luceco (LON:LUCE)

Up 1% at 238p (£383m) - Q1 2026 Trading Update - Graham - GREEN ↑

It’s a very nice Q1 trading update from this company, upgrading expectations.

I think of it as a lighting company, but it also provides EV charge points. It refers to itself more broadly as “the leading designer and manufacturer of residential and commercial electrification products and systems”.

Key points:

Q1 revenue +11% organically to £68m

Core products +6%, and EV charging growth of 80%

The Middle East conflict hasn’t been a problem yet:

Luceco is maintaining its disciplined approach to pricing, working with our customers to pass through higher commodity costs. The direct impact of disruption linked to the conflict in the Middle East has been immaterial to date, and the Group remains well placed to manage its operations with appropriate resilience and contingency measures.

Net debt is £66m, with a leverage multiple of 1.4x (perfectly normal). They are open to doing "selective bolt-on acquisitions”.

Outlook: Q1 was ahead of management’s expectations, and they upgrade the full year forecast.

While the Board remains mindful of the broader economic backdrop, including the impact of the conflict in the Middle East, the strength of Q1 trading and sustained Energy Transition momentum mean expectations for full-year 2026 Adjusted Operating Profit now exceed £40m, with the potential for further significant outperformance dependent on Demand Flexibility.

They helpfully provide a consensus figure for adjusted operating profit: £38.3m. So they should beat this by at least 4%.

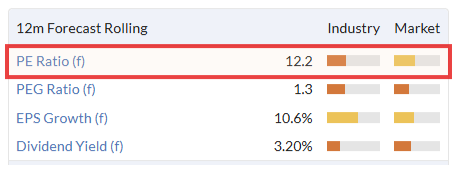

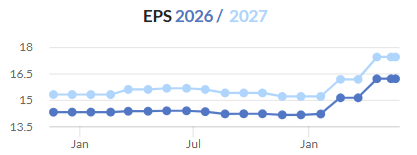

Estimates: the new EPS forecast from Longspur Research is 17.2p, putting the shares on a P/E multiple of just below 14x at the current share price.

Graham’s view

I’m torn on this one. I’ve always been hesitant to get too excited about anything that I consider to be a lighting business, as performance tends to be volatile.

But maybe Luceco is a higher-quality business than I’ve been giving it credit for? Especially with its foray into EV chargers.

More information on Demand Flexibility is available here.

In January, Mark noted the same themes as I have: very strong EV growth, with more modest growth from the other segments.

On balance, I am going to upgrade this to GREEN today, due to the upward trend in EPS forecasts that has been maintained today:

However, I do want to add some disclaimers:

The stock is a little expensive for what it is. In general I would not be positive on a lighting company trading at 14x earnings.

The balance sheet is fine, but not strong enough for any major acquisitions or shareholder distributions.

The EV charging segment is probably still very small within the context of the group as a whole (c. 10% roughly?).

So this isn’t my typical GREEN. I’m simply noting the very strong momentum in the business, and taking our stance on Luceco up by one notch, while it lasts (which might only be 6-12 months). I wouldn’t do this if the stock was already at 20x earnings.

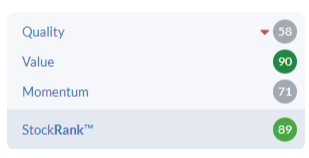

My view is consistent with the StockRanks:

Dr Martens (LON:DOCS)

Up 4% to 66.6p (£645m) - Preliminary Results - Graham - AMBER ↑

This is one of the higher-profile 2021 IPOs:

The shares have been in a 50p - 100p range for the last two years - maybe it’s bottomed out?

FY26 results:

Revenue £765m (-1.4% at constant FX), in line with guidance.

Adjusted PBT £55m (+58.9% at constant FX)

Actual PBT £32.7m (last year: £8.8m).

CEO Ije Nwokorie says “our focus on execution is paying off: we are improving the quality of revenues whilst strengthening margins, cash generation, the Balance Sheet and overall model resilience”.

Ije Nwokorie has an interesting CV. He was Chief Brand Officer for Dr Martens in 2024. He was previously a Senior Director at Apple, and before that spent 11 years at Wolff Olins (a name I remember for eliminating the vowels from Aberdeen - they did that after he left them).

Since taking over in January 2025, he has led the strategy to “stabilise, pivot and scale”. “Pivot” is still happening (to a more customer-centric model), but during the current financial year they will also enter the “scale” phase of the strategy.

Here’s what that means:

This does not mean volume at any cost. It means scaling higher-quality revenues and operational leverage, underpinned by a more resilient model. The desire for our brand is strengthening and we will leverage this momentum, increasing brand investment and delivering our improved retail strategy.

The retail strategy is centred on moving from a transactional one-size-fits-all model to a tiered retail estate which repositions retail as a growth engine, with investment in high potential stores.

The financial results for FY26 are indeed much improved on the prior year, which makes me inclined to think that this is more than just management-speak and might have real strategic substance.

The Outlook is very encouraging, too:

We achieved significant PBT growth in FY26 and plan to deliver further strong PBT growth in FY27, driven by operational leverage. Over the last two years we have put in the hard work to set the business up for growth, and as we look forward there are significant benefits as a result, including the quality of our revenue base through reduced discounting, the strength of our wholesale order books, the benefit from pricing, continued tight management of costs and the improvement in speed of execution from our new market model… our business is materially more resilient than it was previously and this underpins our confidence in our medium-term targets.

Graham’s view

I’m going to upgrade this to neutral, as I think there are signs of a real turnaround, and I don’t want us to be negative on it.

As an aside, I think the balance sheet looks ok: net debt (excluding leases) has reduced year-on-year from £94m to £70m, and guidance is for this to reduce further to £50m. Including lease liabilities, net debt is expected to finish next year at c. £200m (currently £213.5m).

Indeed, the company is comfortable paying an unchanged 2.55p full-year dividend.

One feature of the results that stands out to me is a material increase in margins (up by 120 basis points to 66.2%). This is a very high margin to start with, and the company is clearly intent on protecting it - a good sign of responsible management, in my view.

This could be a really interesting recovery - for now, I think a neutral stance makes sense.

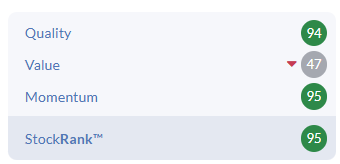

The StockRanks call it "Contrarian", which makes sense:

Roland's Section

Currys (LON:CURY)

Up 11% at 140p (£1.54bn) - Performance continues to strengthen - Roland - GREEN =

While I think Currys’ habit of giving unconventional titles to its RNS announcements is a little annoying, I can’t fault the content of today’s update, which includes an upgrade to full-year profit guidance for the year ended 2 May 2026.

Today’s figures underline a strong finish to the year for the retailer:

Like-for-like sales +4% for both the full year and the 16-week period since the festive peak season. It’s good to see this has been maintained despite the tougher consumer environment.

Full year adjusted pre-tax profit expected to be around £191m, +18% vs £162m in FY25 (previously guided to £180-190m)

£74m of cash returned to shareholders during the year

Year-end net cash of more than £170m (FY25: £184m)

CEO Alex Baldock notes that the company has not yet suffered any adverse effects from geopolitical events:

Recent trading has been very solid; we've not yet seen an impact from the Middle East conflict, and our energy costs are well hedged for the coming year.

Trading across the group’s two geographic regions was positive, although it looks like operating margins came under greater pressure in the UK than the Nordics.

UK & Ireland: “adjusted EBIT expected to grow slightly” versus last year.

UK&I trading is said to have been “robust”, with market share gains and growth in services and business sales.

While Currys did face higher operating costs due to minimum wage growth and other factors, the company says that the impact was offset by sales growth and stable gross margins. In other words, price rises and/or volume growth led to higher gross profits, allowing operating profit to remain flattish.

Currys’ rejuvenated mobile offering, iD Mobile, saw particularly strong growth, with customer numbers up 18% to 2.6m.

Nordics: “adjusted EBIT showing strong growth YoY”. Gross margins were said to be “broadly stable” with costs “tightly controlled”.

The company has been gaining market share and expanding into new categories:

Recent growth driven by market share gains and very strong performance in Kitchens and new categories such as computing components.

Outlook & Estimates

Today’s upgrade continues a long run of increases over the last year:

With thanks to broker Panmure Liberum and Research Tree, we have access to updated forecasts this morning:

FY26E adj EPS: 13.2p (+3.1% vs 12.8p previously)

FY27E adj EPS: 13.8p (unch)

FY28E adj EPS: 14.7p (unch)

Leaving outer year forecasts unchanged at this point is understandable – there’s still considerable uncertainty about the macro outlook.

Recent share price weakness means that Currys is trading on a FY27E P/E of 10x after this morning’s gains:

Roland’s view

I recently heard a well-known investor suggest that one test of a CEO is how the business performs after they leave – have they built a strong, well-functioning organisation? Tesco has performed very well following the departure of Dave Lewis, for example, but there are plenty of examples where the departure of a successful CEO coincides with the start of a period of weaker performance.

Currys CEO Alex Baldock is already working his notice, having announced his decision to leave in March. He’s since been appointed as the next chief executive of Boots, where he will take charge in the autumn.

Baldock has done a sterling turnaround job at Currys and the retailer’s shares fell on the day his departure was announced. Today’s trading update suggests he will be leaving on a high, but shareholders may be anxious lest the group’s improved performance falters following his departure.

I can’t be sure, but my impression is that Baldock has done much of the heavy lifting required to reshape and improve underperforming parts of Currys’ business. In my view, he is likely to leave behind a business that is genuinely better than it was before and should continue to function well.

Areas of notable improvement include a revamped mobile offering and the company’s consumer credit offering, which is now said to be making a useful contribution to group profits:

… we saw UK&I credit adoption climb +180bps YoY to 21.9%, more than double the adoption of four years ago, and we generated £1.1bn of UK&I sales on credit, making us one of the UK's leading brokers of retail credit. As well as additional sales, credit makes a direct profit contribution and as credit scales, we can use some of this profit to invest in the customer offer, driving further sales. We are now in that virtuous circle with credit. [FY25 results]

Mark maintained our positive view on Currys in March, suggesting that the business was still showing good fundamental momentum despite some share price weakness. The StockRank has also remained positive:

Today’s update supports Mark’s conclusions and I see no reason to change our positive view today. The only caveat I’d add is that this will always be a low-margin, cyclically sensitive business – it’s not a stock for which I’d want to pay a high P/E multiple.

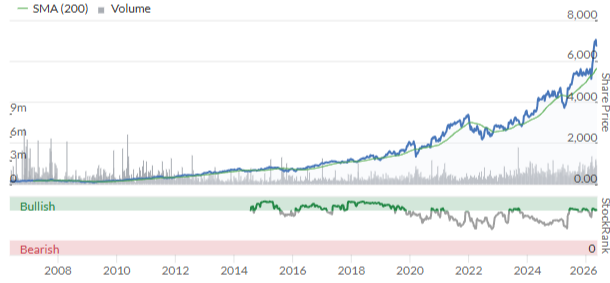

Diploma (LON:DPLM)

Up 4.8% at 6,940p (£9.3bn) - Half Year Results - Roland - AMBER/GREEN =

I have something of a soft spot for well-run distribution businesses. Diploma is a stock I wish I’d bought, well, almost anytime in the last 20 years:

Diploma supplies a huge range of technical products and value-added services to a range of industries. It’s expanded steadily for many years through a mixture of organic growth and bolt-on acquisitions – this is a market that naturally lends itself to consolidation.

Diploma’s share price has risen at a compound average of 21% per year since May 2006! That’s an incredible performance.

Let’s take a look at today’s half-year results

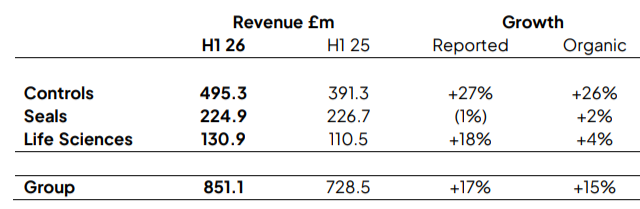

H1 results summary

Today’s figures cover the six months to 31 March. The headline numbers look very impressive to me and include a further upgrade to full-year revenue and profit guidance.

Revenue up 17% to £851.1m

Organic revenue growth: +15% (H1 25: +9%)

Adjusted operating profit up 33% to £208.9m

Statutory operating profit up 18.4% to £165.1m

Adjusted earnings up 36% to 109.2p

Interim dividend up 5% to 19.1p per share

Leverage: 0.8x net debt/EBITDA

Acquisition adjustments: Diploma’s adjusted operating profit for H1 is 26.5% (£43.8m) higher than its reported operating profit for the same period. I feel this is worth understanding.

The company’s policy on adjustments is fairly clear – everything relating to acquisitions is adjusted out. Here’s how this stacked up in H1:

Inventory fair value adjustments: £4m

Employee costs: £1.2m

Amortisation of acquired intangibles: £32.4m

Other operating expenses: £6.2m

I accept that it’s now normal to ignore the amortisation charge on acquired intangibles (even though they were probably paid for in cash), but personally I don’t think it’s appropriate to ignore post-acquisition remuneration/deferred consideration or operating expenses relating to the restructuring and integration of acquired businesses.

After all, acquisitions are a consistent part of Diploma’s business model – the company has done 57 deals since 2019 at a total cost of £1.6bn. In my view, this means that the costs associated with acquisitions should also be seen as a regular operating expense.

Investors can make their own choices on adjustments. My preference is generally to rely on statutory profits as I often find these correlate most closely to free cash flow.

That’s true here – my sums show free cash flow to equity of £100.5m in H1, a perfect match with reported net profit of £100.6m.

The good news is that however you look at Diploma’s profits, they rose ahead of revenue over the same period, resulting in an improvement in margins.

Profitability: even sticking with reported profits, the most conservative measure, my sums give an operating margin of 19.4% for H1, up from 19.1% for the same period last year.

Looking at returns on capital, my sums give me a very respectable trailing 12-month return on capital employed (ROCE) of 19.8%, based on average capital employed over the period.

Diploma reports a more heavily adjusted and favourable “return on adjusted trading capital employed” figure of 22.7% for H1, up from 19.1% in H1 25.

The important thing here, regardless of which measure we choose, is that Diploma is clearly able to deploy capital at attractive and sustainable rates of return, generating value for its shareholders.

Trading commentary

Diploma’s operations are grouped into three segments. Organic revenue growth was positive across all three, but there was one standout winner:

Controls (adj op profit +45% to £165.7m): “[...] excellent execution in favourable market conditions”. Management cite sectors including aerospace, defence and data centres. It looks to me like this business is among the indirect beneficiaries of the AI data centre boom.

Seals (adj op profit unch. at £42.5m): conditions are said to remain challenging in a number of international markets, notably the UK, where construction, oil and gas and agriculture are all highlighted, together with infrastructure project delays.

Life Sciences (adj op profit +18% to £25.9m): organic growth remained positive despite “challenging healthcare markets”. Recent acquisitions added 14% to revenue during the period and have strengthened the group’s footprint in the Nordics, UK and Ireland.

Outlook

Diploma has provided upgraded full-year guidance today, based on improved expectations for both organic growth and the contribution from acquisitions:

Organic revenue growth: 12% (previously 9%);

Acquisitions have added 6% to growth so far (previous guidance 3%);

Guidance for an (adjusted) operating margin of c.25% is unchanged, implying operating profit growth of c.30%;

This implies a 6% upgrade to consensus operating profit, which the newswire tells me was previously £428m.

I estimate a new consensus operating profit of £454m. I estimate this could drop out to give a revised adjusted earnings per share forecast of 235p – about 5% ahead of previous consensus of 224p.

As with Currys earlier, this is the latest in a string of upgrades for Diploma over the last year:

Roland’s view

Diploma’s share price is up by c.5% as I write, so my revised earnings estimate (also up 5%) gives an unchanged forward P/E of around 29x.

The shares are obviously not cheap, but very strong profit growth in recent years means Diploma’s P/E rating has actually moderated since 2020:

Taking a longer-term view, I estimate the current P/E is probably roughly in-line with the stock’s 10-year average.

Should I buy the shares at current levels and tuck them away for another decade? Perhaps I should, but I just can’t bring myself to do that.

Using today’s results, I estimate a trailing 12-month free cash flow yield of under 3%.

Another measure I like to use, the EBIT/EV yield, is just 3.2%.

Continued strong growth may allow Diploma shares to grow into these valuations. But for me, the price is just a little too steep. I also note that ahead of today, earnings growth was expected to slow to just 4% next year.

I think this is an excellent business with strong management. But rightly or wrongly, I’m going to leave my view unchanged at AMBER/GREEN today. I think this is a fair reflection of the quality and valuation of this business.

This view is also reflected in Diploma’s StockRank and High Flyer styling, which flag up the poor value metrics on offer here:

DCC (LON:DCC)

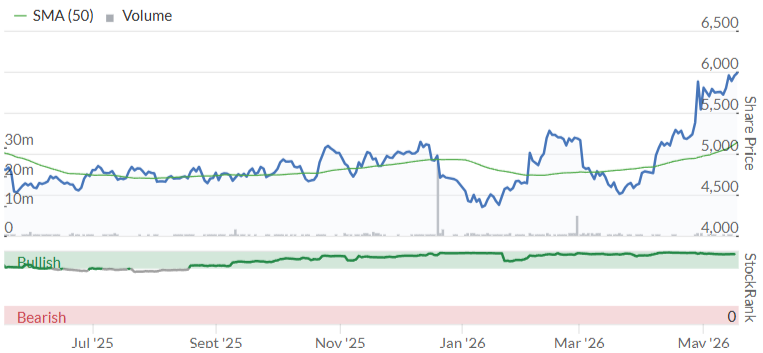

Up 1.9% at 6,060p (£5.2bn) - Results for the year ended 31 March 2026 - Roland - GREEN =

(At the time of writing, Roland has a long position in DCC.)

This Irish energy distribution group recently received a half-hearted takeover approach in April, but as Mark discussed, it fell well short of a reasonable price – the shares are now trading comfortably above the £58 per share offered.

Today’s results highlight the appeal of the core energy business, in my view, with adjusted operating profit up 3.5% to £554m.

Source: DCC FY26 results

Dividend: there’s also a welcome 5% dividend increase while maintaining 2x dividend cover. DCC reminders investors that it has achieved 32 years of unbroken dividend growth at a compound annual rate of 12.7%.

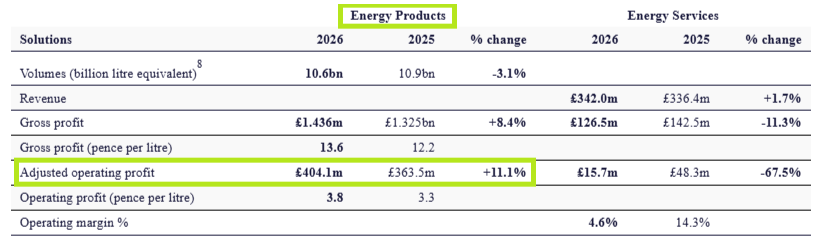

Energy review: the core Energy Products business supplies gas, road fuels and products such as heating oil to customers in a range of markets. Performance was robust last year, with profits up on improved margins, despite slightly lower volumes:

The main area of weakness was the Energy Services unit, where adjusted operating profit fell by 68% to just £16m.

This unit provides sustainable solutions (e.g. solar) and related energy management services for (mostly) business customers. Management notes that in a tough business environment, “discretionary sustainability spend” fell sharply last year, but they expect a recovery over time and are continuing to position for this.

Energy Services consists of a number of businesses that have (largely) been acquired in more recent years as DCC has positioned itself for a lower-carbon future. Last year’s weakness reflects my main concern about this business – that low–carbon solutions will not prove as profitable or predictable as the core gas and fuel oil supply business.

Outlook

Management also confirms that the final part of the DCC Technology business is now up for sale, with a buyer expected to be found by the end of calendar 20256. This will complete the simplification of this business to an energy-only operation, reflected in today’s name change announcement.

There’s no explicit FY27 guidance today, but CEO Donal Murphy does reiterate guidance for a 2030 adjusted operating profit of £830m.

Roland’s view

It’s long been clear that the Energy unit is DCC’s most profitable, capable of delivering double-digit returns on capital and strong cash flows.

Using FY26 profit from the Energy business alone, I estimate DCC trades with an EBIT/EV yield of over 9%. Adding in the discontinued Technology business (now up for sale) makes this even cheaper.

Looking further ahead, if the company can achieve its goal of £830m in operating profit by 2030, then I think it’s fair to suggest DCC shares could trade at a materially higher valuation.

I recognise that I am biased, as this is one of my larger, long-term shareholdings. But I continue to view DCC as fundamentally undervalued by the market, so I’m leaving my positive view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.