Good morning!

I hope you’ve had a chance to enjoy some nice weather, wherever you may be. The UK recorded its hottest ever May day over the weekend.

In the markets, Brent crude is back below $100, gapping lower over the weekend and falling to $98.50, as President Trump says that talks with Iran are “progressing nicely”. Other sources confirmed that a deal is close to being reached, with only certain details yet to be finalised.

At the same time, Iranian boats have been hit by US and Israeli jets in the Strait of Hormuz overnight. The US military said that the Iranian boats were placing mines. But the current ceasefire is still officially in place.

Overnight market movements:

The FTSE is set to open up 20 points at 10,490 (vs. Friday’s close)

S&P 500 is set to open up 50 at 7,520 (vs. Friday’s close)

Brent crude is up 20 cents at $98.20

Gold is down $45 at $4,530

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£216bn | SR76) | AstraZeneca and Daiichi Sankyo's Datroway has been approved in the US for the treatment of adult patients with unresectable or metastatic triple-negative breast cancer who are not candidates for PD-1/PD-L1 inhibitor therapy. | ||

Jardine Matheson Holdings (LON:JARB) (£15.3bn | SR78) | Agrees to acquire “a global leader in diagnostic imaging and teleradiology”, based in Australia, for an enterprise value of AUD $3.4bn (US$2.4bn). | ||

Kingfisher (LON:KGF) (£4.9bn | SR97) | LfL minus 0.7%. On track to deliver full year guidance: expect FY 26/27 adjusted PBT of c.£565m-£625m and free cash flow of c.£450m-£510m. | AMBER/GREEN ↓ (Graham)

This is a Super Stock that performed strongly against expectations for FY Jan 2026 - see Roland’s commentary on their upgrade last November. Roland maintained our positive stance on Kingfisher, but also said “I can see a time in the not-too-distant future when we might need to moderate this view unless revenue growth starts to improve.” Six months later, revenue growth has not improved and indeed is negative on a LfL basis. While this might be a Super Stock, it doesn’t look super to me at this valuation. I’m therefore taking us down one notch. | |

Serco (LON:SRP) (£2.7bn | SR93) | Successfully retains its facilities management contract at Norfolk and Norwich University Hospital (NNUH). Total value >£270 million over the next 10 years. | AMBER = (Graham) [no section below] Average revenue from this contract of £27m p.a. is only about half of one percent of Serco’s total revenues and they would have expected to retain this contract, seeing as they have provided services at NNUH for 25 years. So this RNS does not move the needle. In terms of the bigger picture, the stock appears at least fairly valued to me, considering the forward P/E multiple of 15x and with no step-change in profitability expected between now and FY December 2027. Even against 2027 earnings, it’s trading at 14x. They are buying back their own shares which may continue to support the share price and I acknowledge that EPS forecasts have been on a pleasantly rising trend. But I would still struggle to justify paying this much for a government support services provider. I have form for being overly cautious on Serco - I was too cautious back in Dec 2024, so my neutral stance today might be another very similar mistake. | |

Atalaya Mining Copper SA (LON:ATYM) (£1.21bn | SR93) | Copper production impacted by unfavourable weather. EBITDA of €48.0 million, a “solid performance to begin FY2026”. The Company expects production for FY2026 to remain within the original guidance range of 50,000 to 54,000 tonnes of copper, along with silver contained in copper concentrate of 0.9 to 1.1 million ounces, although production is currently trending towards the low end of the guidance ranges. | ||

CVS (LON:CVSG) (£841m | SR38) | £50m buyback. All shares repurchased will be cancelled. | ||

Anglo Asian Mining (LON:AAZ) (£357m | SR49) | SP +2% 2025: revenues increased to $122.8m (2024: $39.6m). Net cash flow from operations $46.7m. 2026 the first year in which copper is expected to be AAZ’s principal output. Both mines are delivering in accordance with expectations, with Demirli continuing to ramp up to full production. On track to deliver 2026 guidance. | AMBER/GREEN (Graham) [no section below] I'm going AMBER/GREEN on this one purely to be consistent with the StockRank categorisation of it as a High Flyer. AAZ has been a spectacular multi-bagger over the past few years as the gold price has soared, and it's about to become a copper-first producer. The exceptional share price performance reflects its leverage against commodity prices: guidance for its all-in sustaining cost of copper in 2026 is $6,800 to $7,800 per tonne, making it a high-cost copper producer, and it's also a high-cost gold producer (AISC guidance of $1,500 to $1,800 per ounce). Current metal prices do make the economics very attractive and with new mines opening it can continue to do well while the bull market continues. | |

KEFI Gold and Copper (LON:KEFI) (£157m | SR21) | Tulu Kapi Gold Project: all workstreams on or ahead of schedule, targeting commissioning from late 2027 for full production mid-2028. Financing: KEFI has replaced US$15 million of short-term working capital funding with US$15 million of long-term subsidiary level equity ranking capital without any impact on Tulu Kapi Project economics. | ||

Diaceutics (LON:DXRX) (£141m | SR46) | Revenue +24%. Adj. EBITDA +80% (£7.6m). Pre-tax profit £300k. Record order book. Q1 2026 performing in line with the Board's expectations. Confidence that targets for 2026 are on track. | ||

Galantas Gold (LON:GAL) (£130m | SR26) | Quarterly net loss CDN $2.35m (Q1 2026 loss $1.23m). “Until the Indiana mine reaches commercial production, the net proceeds from concentrate sales are being offset against development assets.” Share count has increased by 94m to 553m due to the exercise of warrants. | ||

Calnex Solutions (LON:CLX) (£63m | SR72) | FY March 2026: revenue +19%, PBT +73% (£1.2bn). “Targeted investment in FY27 in key product launches and continued development of market and customer relationships will position the Group for further growth in FY28 as new products are commercialised.” | AMBER = (Ed S - I hold) | |

MTI Wireless Edge (LON:MWE) (£54m | SR97) | Revenue up 6% to $12.8m. Operating profit up 21% to $1.5m. Earnings per share up 18% to 1.40 US cents. Net cash as at 31 March 2026 of $8.5m. Antenna revenues down 20%, Water Control & Management revenue up 19%, Distribution & Professional Consulting Services revenue up 20%. | AMBER/GREEN = (Ed S - I hold) | |

Ariana Resources (LON:AAU) (£49m | SR45) | Ariana has issued Tranche 2 CDIs at the price of A$0.30 per CDI under its agreement with Hongkong Xinhai Mining Services Ltd. | ||

Pathos Communications (LON:NEWS) (£21m | SR N/A) | Secures a US$0.7m 12-month contract with existing client. Contract expected to generate over US$0.5m EBITDA across FY2026 and FY2027. | ||

Genedrive (LON:GDR) (£18m | SR11) | David Nugent, the company's largest shareholder, has joined the Board as a Non-Executive Director. Chairman Dr. Ian Gilham will be stepping down as a Chairman and Director. Non-Executive Director Chris Yates also stepping down. The Board is commencing the search for a new independent Non-Executive Chairman as well as two other independent Non-Executive Directors. | ||

Sancus Lending (LON:LEND) (£13m | SR54) | In the four months to 30 April, revenue increased by 44.1% to £8.5m. The company wrote new loan facilities of £42.9m. Assets under management of £326.8m. Due to geopolitical and macro-economic issues and increased financing and liquidity carry costs, profitability in the first half is below management expectations. Also issued £0.5 million of Sancus Bonds to Somerston Fintech Limited. | ||

Frontier IP (LON:FIPP) (£12m | SR11) | Portfolio news - Dekiln to explore strategic partnership with Johnson Tiles | Dekiln and Johnson Tiles have signed a MoU to form a strategic partnership focused on the scale-up, manufacture and commercialisation of Dekiln's kiln-free, low-energy bio-based materials as ceramic alternatives. Frontier IP holds a 24.8 per cent equity stake in the Company. | |

Kazera Global (LON:KZG) (£11m | SR2) | Subsidiary Whale Head Minerals has entered into a binding Production Sharing Agreement (PSA) with Rare Earth Minerals International in relation to the Walviskop Heavy Mineral Sands project. The PSA is expected to materially enhance operational capability, accelerate production growth and significantly reduce the working capital burden associated with scaling operations at Walviskop. | ||

Earnz (LON:EARN) (£10m | SR9) | Revenue increased to £11.8m vs £2.6m in 2025. EBITDA of £0.1m. Loss before tax of £1.7m. Strong pipeline of opportunities in all the businesses within the Group. The Board remains confident in the outlook for FY26. |

Graham's Section

Kingfisher (LON:KGF)

Up 3% to 300.1p (£5.1bn) - Q1 Trading Update - Graham - AMBER/GREEN ↓

This Super Stock has delivered a reassuring Q1 update, that it’s “on track to deliver full year guidance”.

Key points:

Underlying LfL sales are down 0.7% “vs. strong prior year comparator”.

Trade sales +17% ex-Screwfix

E-commerce sales +14% ex-Screwfix

The overall UK market is said to have declined “low single digits”, with the same being said for France and Poland, too.

In the UK, there’s a big disparity between Screwfix (+4.1% LfL sales) and B&Q (minus 4.1%). B&Q was particularly hit by a 7.5% reduction in LfL sales in the “Seasonal” Category.

France (Castorama and Brico Dépôt) saw LfL sales down 2.1%, and Poland was down 0.2%.

On the other hand, thanks to store openings, Kingfisher’s total sales rose 0.8%. The StockReport suggests that revenues are expected to grow 1.4% in the current financial year (FY Jan 2027), so this should still be possible.

Full year guidance reiterated: adjusted PBT c. £565m - £625m, free cash flow c. £450 - £510m.

The PBT guidance range is wide enough (+5% above or -5% below the midpoint), but we are still quite early in the financial year.

CEO comment:

"We delivered a resilient start to the year, executing well and gaining market share against a soft market backdrop. Sales including marketplace grew +0.8%, with core categories proving resilient - even as a late start to spring impacted footfall and seasonal demand. E-commerce and trade sales both delivered double-digit growth, underlining the momentum in our key growth drivers.

Graham’s view

This is a Super Stock that performed strongly against expectations for FY Jan 2026 - see Roland’s commentary on their upgrade last November.

Roland maintained our positive stance on Kingfisher, but also said “I can see a time in the not-too-distant future when we might need to moderate this view unless revenue growth starts to improve.”

Six months later, revenue growth has not improved and indeed is negative on a LfL basis.

The good news is that this hasn’t had any major impact on profit forecasts, which speaks a lot to the efficiency of the organisation:

And weak revenue must also be put in the context of the wider market - most of their banners seem to have gained market share.

However, for me, some caution is required at this stage. It’s not cheap for a bricks-and-mortar retailer:

Quality metrics don’t impress:

And now it’s ex-growth on a LfL basis (not its own fault, but due to the market in which it operates).

So while this might be a Super Stock, it doesn’t look super to me at this valuation. I’m therefore taking us down one notch.

Ed S's Section

Calnex Solutions (LON:CLX)

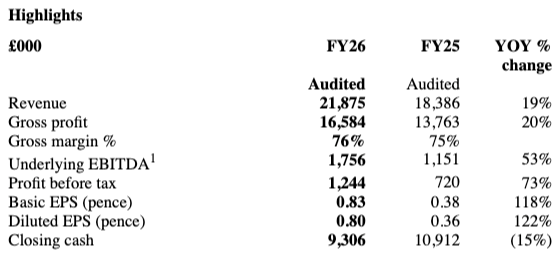

Up 4% at 75p (£65M) - Final Results - Ed S - AMBER =

(At the time of writing, Ed S has a long position in CLX.)

Calnex Solutions, which provides test and measurement solutions for the global telecommunications, digital infrastructure, and government & defence markets, has posted its final results for the year ended 31 March 2026 (FY2026). And they look pretty solid.

Here are some highlights:

Revenue of £21.9m, up 19% year on year

PBT increased to £1.2m versus £0.7m in FY2025

Diluted EPS of 0.80p versus 0.36p in FY2025

Strong balance sheet with cash of £9.3m at year end (£11.2m at 22 May 2026)

Proposed a final dividend of 0.68p per share. Total of 0.99p per share for FY26 (FY25: 0.95p).

Outlook:

Targeted investment in FY27 in key product launches and continued development of market and customer relationships will position the Group for further growth in FY28 as new products are commercialised.

Strongly positioned to benefit from the continued global investment across structural growth markets of digital infrastructure, government and defence, supported by a strong balance sheet, robust product roadmap and diversified market footprint.

We enter FY27 with confidence, supported by a robust product roadmap, strong balance sheet, and a more diversified market footprint. In a period of rapid technological and geopolitical change, the importance of high-performance network testing continues to grow, and as we move into the next decade of Calnex's journey, we are excited by the opportunities ahead.

The Board is increasingly confident in the Group's long‑term prospects. Diversification across products and end markets, strengthened partner channels, and enhanced commercial capability provide a solid platform for sustainable growth.

Ed S’s view:

I’ve been a shareholder in Calnex for around five years now. I originally bought at significantly higher prices before averaging down a little.

The reason I invested here was that I saw a lot of potential in terms of the need for telecoms network testing. My logic was that new technologies (e.g. self-driving cars) would drive demand for network testing.

It’s fair to say my thesis didn’t play out. In recent years, the company’s telecoms revenues have been weak and the stock has tanked.

But I have held on to it. Because I could see the potential for an improvement in performance at some stage and a rebound in the share price.

Now, today’s full-year results certainly show an improvement in performance. Revenue is growing at a decent clip again (+19%) and profits have expanded.

The full-year dividend has been increased to 99p from 95p last year. Meanwhile, the balance sheet looks robust.

What’s working is the company’s diversification into other markets. Recently, Calnex has expanded into the data centre and government & defence markets.

Growth was driven by continued momentum in our newer end markets of government and defence, and digital infrastructure (cloud computing and data centres). This underlines the increasing relevance of Calnex's capabilities across adjacent markets and the early success of our diversification strategy.

Zooming in on the data centre segment, the company says that in H2, it secured a ‘significant repeat order’ for its Sentry product from a leading hyperscaler to monitor network sync.

Digital infrastructure represents a significant growth opportunity, driven by hyperscaler investment, network upgrades and the rapid expansion of AI‑driven workloads.

As for the government/defence segment, it notes in its report that revenues here represented 21% of orders by value last year versus 15% the year before.

The government and defence sector provides an increasingly significant market opportunity for Calnex, driven by modernisation of digital infrastructure and the need for assured performance in mission‑critical environments.

Turning to the telecoms market, this remained ‘steady’. However, the company remains confident in the long-term outlook here.

While this is all quite encouraging, the downside to the stock is that the P/E ratio is very high at present. If we take today’s diluted EPS figure of 0.80p, we get a trailing P/E ratio of about 94.

Now, if Calnex sees strong growth in the years ahead, the company may be able to grow into this valuation. But there’s no guarantee here, so the valuation is a risk.

It’s worth noting that FY2027 is set to be a year of ‘targeted investment to support key product launches’ so this could have implications for near-term profitability. That said, the company believes that this investment will position it for accelerated growth in FY2028.

One other thing to note is that there is a degree of customer concentration here. Last year, its top 10 customers accounted for 55% of orders (FY25: 45%).

Given the high valuation, I’m going to leave the stock on AMBER for now. I do see a lot of potential here in the long run, however, the valuation adds risk in the near term.

MTI Wireless Edge (LON:MWE)

Up 4% at 64p (£55M) - Q1 2026 Financial Results & Investor Presentation - Ed S - AMBER/GREEN =

(At the time of writing, Ed S has a long position in MWE.)

Israel-based technology company MTI Wireless Edge (I hold) has posted its Q1 results today. Here are some highlights:

Revenues of $12.8m, up 6% year on year

Operating profit of $1.5m, up 21%

Earnings per share of 1.40 US cents, up 18%

Net cash at 31 March 2026 of $8.5m (31 December 2025: $9.4m)

Division performance:

Antennas: revenue down 20%

Water Control & Management: revenue up 19%

Distribution & Professional Consulting Services: revenue up 20%

Management commentary and outlook:

Overall, this was a strong Q1 performance, particularly from Mottech which benefitted from an uplift in demand from international customers seeking water management services. Moving into Q2, we received a record level of defence related orders worth just over $9 million, the majority of which is expected to be fulfilled in the current year, adding to a backlog of orders for 2026 that was already high.

While defence orders are likely to continue to be a key driver of revenues in the short to medium term, the diversification of MTI's operations across multiple markets is a core strength of the business and all three divisions continue to contribute positively to the Group's trading performance. Overall, MTI is in a good position with net cash of $8.5m, a strong balance sheet and a growing customer base."

Ed S’s view:

I initiated a very small position here recently (I’m a little in the red right now). I bought mainly as a play on defence (the company has seen strong momentum here in recent months) but I was also attracted to MTI’s financials and its high Stockopedia StockRank (and ‘Super Stock’ rating).

Zooming in on the financials, we have:

Rising revenues (analysts forecast growth of around 6% this year)

A decent mid-teens return on capital employed (ROCE)

Rising dividends (the trailing yield is around 3.9%)

Overall, there’s a fair bit of quality. Note that Stocko gives it a 97 for quality.

One other thing that appeals to me here is that the company is diversified and has multiple revenue drivers. This paid off in Q1, as while antenna revenues were weak (down 20%) due to lower E-band 5G backhaul solution sales in India, the other two divisions saw strong growth.

At the group’s Water Control & Management division (Mottech), which provides wireless control systems to manage irrigation and water distribution for agriculture (helping to generate higher crop yields through more accurate water usage), municipal authorities. and commercial entities, revenues were up 19%. This growth was driven by international markets – particularly North America, Italy, and the Arabian Gulf.

Turning to the Distribution & Professional Consulting Services, where it represents around 40 international suppliers of radio frequency/microwave components and sells products to Israeli customers, revenues were up 20%. Here, the company noted that new business wins have created a lengthy backlog of orders, which it says bodes well for the remainder of 2026.

Going back to the Antenna division, the company has received quite a few defence-related orders since the end of Q1 ($9m of orders in April alone). So, there are reasons to be optimistic here.

In terms of the valuation, I think it’s quite reasonable. Taking last year’s EPS figure of 5.86 US cents, we get a P/E ratio of a little under 15x.

Given the rising revenues, undemanding valuation, attractive dividend yield, and high StockRank, I’m happy to leave MWE on AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.