Short-seller convicted of securities fraud: Andrew Left of Citron Research has been found guilty by a jury of engaging in securities fraud - not just on the short side, but also on the long side.

Left is a well-known commentator who has been around for a long time, with nearly 400,000 followers on X.

According to the US Attorney’s Office, he "often built his positions using inexpensive, short-dated options contracts that expired the same day that he published his commentary". He also "submitted limit orders to close his positions as soon as the company’s shares reached a certain price – often at prices vastly different from the target prices Citron’s commentary touted".

An example given is Nvidia: the US Attorney’s Office says that in 2018, Mr. Left closed a long Nvidia trade at $150-151 just two hours after tweeting about it. The stock was trading at $143.64 when he bullishly tweeted that “We see $165 before we see $120”.

When it comes to debates on the topic of short-selling, I’m nearly always on the side of the short-sellers. But this case isn’t really about short-selling. You can see from the Nvidia example that the prosecutors are highlighting a long trade. And I must say that I would be deeply uncomfortable with trading practices like that.

I don't think I'd want somebody to be punished with long prison time over it, but I also wouldn't want them doing it in the first place!

Overnight market movements:

The FTSE is set to open up 0.4% at 10,360

S&P 500 is down 0.2% at 7,580

Brent crude (August delivery) is down 1% at $94

Gold is up 1% at $4,520

Bitcoin is down 1.4% at $70,400

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

British American Tobacco P.l.c (LON:BATS) (£99bn | SR90) | “Confident in sustainably delivering our mid-term algorithm: 3-5% revenue, 4-6% APFO (adjusted profit from operations) and 5-8% adjusted diluted EPS growth, with 2026 performance still expected at the lower end of these ranges.” New Category revenue growth in FY26 upgraded from low double-digit to mid-teens. | (Graham) | |

British Land (LON:BLND) (£4.1bn | SR68) | Joanne McNamara is currently Executive Vice President, Europe at Oxford Properties, a real estate investor owned by one of Canada’s largest pension funds. | ||

Chemring (LON:CHG) (£1.39bn | SR61) | H1 in-line and FY26 expectations unchanged. At constant FX: order book +5%, revenue +7%, underlying operating profit down 12% to £23.2m. | ||

Paragon Banking (LON:PAG) (£1.39bn | SR44) | Underlying PBT down 2.5% to £145.7m. Underlying RoTE 17.4% (2025 H1: 17.8%). Net loan book up 3.8% year-on-year. Underlying RoTE guidance unchanged. | ||

Serica Energy (LON:SQZ) (£1.01bn | SR91) | All guidance for 2026 remains unchanged. Dividends of 15-30% of post-tax Cash Flow from Operations. This is expected to support a continuation of the current 16p per share annual dividend, with potential for additional shareholder returns. | ||

Elementis (LON:ELM) (£869m | SR46) | Sale of pharmaceutical manufacturing business to ABF has completed. ELM is returning the c.$35m net cash proceeds by way of a share buyback programme. | ||

GB (LON:GBG) (£572m | SR78) | FY26: constant currency revenue +3.2%. Adjusted operating profit +0.7% (£67.5m). Statutory operating loss £68.1m after a large impairment charge. FY27: Adjusted operating margins of 21-22% to reflect a one-off investment; expected to return to 23-24% range in FY28 and exceed 24% in the medium-term. | AMBER = (Roland) Today’s results disappoint somewhat with a big impairment charge for the group’s American business despite a tentative return to growth. Overall performance was pretty flat for the year and while cash generation was strong, it was weaker than in the prior year. I am also discouraged by the somewhat wanton (in my view) use of £45m of borrowed cash to fund buybacks. I want to be positive, especially as a P/E of 11 seems too cheap for this business. But today’s FY27 outlook implies a small cut to profit expectations for the current year and I’d really like to see some stronger evidence of top-line growth. I’m going to remain neutral today – but I suspect this might be a situation that would reward more in-depth sector research. | |

Sabre Insurance (LON:SBRE) (£378m | SR92) | The Board has received regulatory approval to proceed with a share buyback programme for up to £5m. Any shares purchased will be cancelled. | ||

Newriver Reit (LON:NRR) (£332m | SR70) | Underlying funds from operations per share +2% to 8.3p, with net property income +26% to £63.4m. Dividend +3% to 6.7p. LTV redacted to 40% (FY25: 42%). | AMBER/GREEN = (Graham)

We’ve been AMBER/GREEN on this and I’m happy to keep that stance today. NRR is trading at an attractive discount, with a normal LTV, borrowing cheaply, and with acceptable occupancy levels. Overall, I see little to dislike. The only reason I’m not GREEN is that it’s a REIT in an economically exposed sector. So the upside is capped - it’s a property investment, after all - and there is also significant downside exposure in a recession. | |

Gooch & Housego (LON:GHH) (£305m | SR56) | Revenue +15.5%, adj pre-tax profit +13.9% to £5.8m. Adj EPS +9.3% to 16.4p. Strong growth in Aerospace & Defence, FY26 expectations unchanged. | AMBER/GREEN = (Graham) Checking my comments in April, I was happy at the time to bump up our stance on this by one notch to AMBER/GREEN. Unfortunately, the valuation multiples then weren’t cheap, and the stock is even more expensive now. But there are just enough positives to keep me AMBER/GREEN. | |

Secure Trust Bank (LON:STB) (£245m | SR94) | Rachel Lawrence has informed the Board of her intention to retire as Chief Financial Officer and as a Director of STB during the first half of 2027. She has been with STB for six years. | ||

Strategic Minerals (LON:SML) (£140m | SR46) | Cash of $10.8m at 31 May, leaving the company “substantially funded through to completion” of the PFS for the Redmoor project. Infill drilling is progressing, with a second hole due for completion today and a further hole due to start from the same pad. | ||

Helix Exploration (LON:HEX) (£71m | SR15) | Helium-3 to helium-4 ratios (3He/4He) ~33× above typical crustal helium values, with consistency across all three wells. | ||

Likewise (LON:LIKE) (£66m | SR59) | Like-for-like revenue +16.5% for the year to date, with May +19.1%. Order intake is positive and the group reports “exponential gains in market share”. Confident of achieving current market expectations. Zeus FY26 forecasts unchanged for adj EPS of 1.2p. | AMBER ↑ (Roland) Today’s sales growth figures suggest to me that Likewise is successfully pursuing its strategy of picking up market share from Headlam and others who are retrenching. However, profit expectations have been left unchanged despite sales growth running at 2x forecast levels so far in 2026. I suspect there is some pressure on margins. More broadly, I think Likewise’s aggressive expansion strategy carries some risk, but with strong leadership it could succeed. I am not sure I have the insight to gauge which outcome is more likely, but I think it’s fair to recognise the evident momentum here. While I think that the valuation looks up with events, I am going to move our view back to neutral today. | |

Gelion (LON:GELN) (£41m | SR5) | Has agreed a three-year solid state battery project with Nissan and the University of Oxford, commencing in June 2026. The total project cost is £3.4 million, with £2.4 million in combined grant funding from Innovate UK across the partners, including an award of £1.6 million to Gelion's UK subsidiary. | ||

Time Out (LON:TMO) (£38m | SR15) | Spanish publisher RBA has acquired Time Out’s media operations in Spain under a long-term franchise agreement. | ||

Inspiration Healthcare (LON:IHC) (£25m | SR56) | Will transfer the distribution of Micrel infusion products to an entity controlled by Micrel from 31 January 2027. Inspiration has distributed Micrel’s infusion products in the UK since 2011 and they generated c.£9.7m of revenue last year. Expects operating cost savings which will contribute to debt reduction in H2 FY27. | ||

Great Southern Copper (LON:GSCU) (£20m | SR3) | Drilling has commenced at the Victoria porphyry copper target at the Especularita Project and was recently completed at the nearby Artemisa North target, where all five holes successfully intersected biotite-chlorite-magnetite alteration with variable sulphide mineralisation. | ||

Itaconix (LON:ITX) (£16m | SR22) | Following a successful 2025, H1 2026 trading has continued in line with expectations. Management expect H1 to be “another record half” and notes its plant-based products are potentially well positioned to gain share from competitors whose fossil-fuel based products are affected by Middle East supply chain disruption. | ||

Power Metal Resources (LON:POW) (£14m | SR52) | Revenue -62% to £76k, net profit -24% to £3.2m, reflecting fair value gains. Cash of c.£5m. Company notes progress with existing operations and realisations on several investments, against a favourable backdrop. |

Graham's Section

Gooch & Housego (LON:GHH)

Down 14% at 961.6p (£263m) - Interim Results - Graham - AMBER/GREEN =

Gooch & Housego PLC (AIM: GHH), the specialist manufacturer of optical components and systems, today announces its interim results for the six months ended 31 March 2026 ('H1 2026' or the 'Period').

The weak share price reaction here seems to be more to do with recent run-up rather than anything to do with the results themselves.

Here’s the year-to-date chart:

A half-year trading update was released on 9th April. The share price closed that day at £8.70, and there has been no news since then - but the share price ran up to £11.

So I’m going to interpret today’s weakness as profit-taking, or “sell the news”-type behaviour.

Because the key line is this:

FY2026 expectations unchanged; Board remains confident in further profitable growth and progress towards mid-teens returns over the medium-term.

Let’s pick out some other key facts from these results.

Gooch & Housego is an “optical components and systems” business. I simply think of it as making parts for lasers.

H1 revenue +15.5% (to £81.9m). Organic, constant currency growth was 9.1%.

H1 adjusted PBT +13.9% (to £5.8m)

Statutory PBT £3.3m (H1 last year: £2.9m)

Pretty good numbers but we’ll have to investigate the gap between adjusted and statutory PBT, as usual.

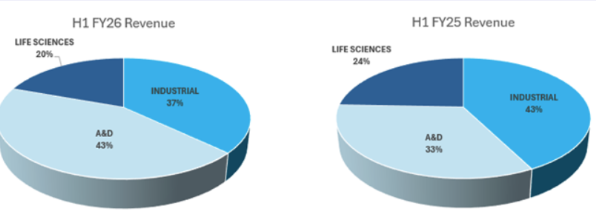

The company has focused on the Aerospace & Defence sector, which appears to be paying off. A&D H1 revenues were up by over 50% year-on-year (up 26% organically) and were over 40% of total revenues:

In contrast, revenues in GHH’s Industrial segment were “broadly flat” and Life Sciences revenues were down 7.7%.

Net debt excluding leases increased year-on-year by over £12m to £36.6m.

There are reasons for the increase in debt:

They have spent cash on acquisitions over the past year, e.g. nearly $8.75m in cash to buy a business called Global Photonics (shares also issued to fund this).

Working capital grew by £5m over the past six months, due to higher outstanding invoices (“which have since largely been converted to cash”).

Order book increased by 16.5% in just six months, “providing near full cover for expected FY2026 revenues”.

CEO comment: happy with the "stronger forward visibility than we have had historically”.

Graham’s view

Let’s start by reconciling adjusted PBT (£5.7m) to statutory PBT (£3.3m):

Amortisation of intangibles £1.5m

Restructuring £0.4m

Acquisition/integration £0.2m

Local employment litigation £0.2m

Interest on defcon £0.1m

For me, restructuring and “local employment litigation” costs sounds like items I would not be willing to look past. There were restructuring costs last year too, and it’s too easy for management teams in general (not specifically at GHH) to lump awkward costs into this category.

So for me, real pre-tax profitability in H1 is probably about £5m.

The balance sheet has a tangible value of about £53m, after writing intangibles down to zero.

Checking my comments in April, I was happy at the time to bump up our stance on this by one notch to AMBER/GREEN.

I still think that was the right call at the time. The share price then was 890p, versus 961p today.

Unfortunately, the valuation multiples then weren’t cheap, and the stock is even more expensive now: the ValueRank is 15 (prior to the impact of today’s share price fall).

Historically, returns are weak:

Today, I’m on the fence about what to do - but my conclusion is to leave our moderately positive stance unchanged.

The positives:

9% organic growth.

Much higher growth after including acquisitions.

Strong A&D and improved order intake in Industrial.

Very strong revenue visibility.

Conclusion: there are just enough positives to keep me AMBER/GREEN, but it’s close.

Newriver Reit (LON:NRR)

Up 1% at 77.56p (£334m) - Preliminary Results - Graham - AMBER/GREEN =

These FY March 2026 results open confidently:

"FY26 was our first full year with Capital & Regional, and it has delivered: integration is complete, synergies have been realised and the enlarged and improved portfolio is generating positive operational momentum and continued valuation progress.

Capital & Regional was bought in late 2024 for £147m, bringing in a range of additional shopping centres to the NRR portfolio and increasing the London retail weighting to 43% of the portfolio.

Some key points about full-year performance:

Underlying funds from operations of £37.2m (up from £30.5m in FY25)

Bought back 10% of its share capital at 75p in August 2025.

Like-for-like portfolio valuation growth +0.7% to £802m

They say “Stable occupancy of 95.0% vs 95.3% at 30 September 2025”. In fact it seems that occupancy has been gently sliding lower: it was 96.1% in March 2025. But 95% is still fine!

Another key data point:

EPRA net tangible assets per share 105p.

The current share price is a 26% discount to that level. There have been no dividends since March 2026 that would require an adjustment to this calculation.

Loan-to-value is 40%, down from 42% a year ago. For REITs generally, this is a level I’m very comfortable with. I only treat them as highly leveraged with an LTV over c. 60%.

As we’ve noted before, NRR has been working for some time to get its LTV below 40%. It made disposals for £110m during the year, and did so at book value.

Graham’s view

We’ve been AMBER/GREEN on this and I’m happy to keep that stance today. NRR is trading at an attractive discount, with a normal LTV, borrowing cheaply, and with acceptable occupancy levels.

Overall, I see little to dislike.

The only reason I’m not GREEN is that it’s a REIT in an economically exposed sector. So the upside is capped - it’s a property investment, after all - and there is also significant downside exposure in a recession.

The most likely scenario is that this simply continues to pay an attractive yield to its investors for the foreseeable future (at least until the next major recession):

There is also the potential for the discount to close vs. NTA, depending on interest rates and sentiment in the market. Disposals at book value over the last year provide solid evidence that the NTA figure is real, rather than an accounting fiction, which increases the likelihood of the discount closing.

Roland's Section

Likewise (LON:LIKE)

Up 6% at 28p (£70m) - Trading Update - Roland - AMBER ↑

On the face of it, today’s update from this flooring distributor suggests impressive sales growth, with like-for-like sales up 16.5% so far in 2026 and sales growth of 19.1% in May.

I am not sure why the company is quoting like-for-like revenue rather than total revenue, but I can’t see any reason why the value of the two figures should be significantly different.

If I’m correct, then revenue growth so far this year is running at more than double the 7% growth rate (2025: 9%) suggested by current forecasts from house broker Zeus, which are unchanged today.

Continued expansion

Today’s update highlights the ongoing efforts to increase Likewise’s capacity so that it can support £250m of annual sales:

2nd distribution hub in Leeds is now operational, expected to improve management of palletised containers

Extension in Newport will begin operations as planned in July, adding storage and cutting capacity

Valley subsidiary has increased cutting capacity in Derby

Total fleet expected to exceed 160 trucks during 2026

Outlook

Notwithstanding the Global uncertainties, the Board is confident of achieving current market expectations for the financial year ending 31 December 2026 and are very focused on improving operating margins to enable further investment and development.

Zeus has left its forecasts unchanged today “on a precautionary basis”, citing concerns around consumer spending and cost pressures.

FY25 actual adj EPS: 1.1p

FY26E adj EPS: 1.2p

There are not yet any forecasts for 2027.

Roland’s view

These strategic investments leave the Group in a strong position and well poised to capitalise on the significant market opportunities before us.

As I understand it, Likewise’s strategy is to gain share by focusing on independent retailers and other areas from which sector leader Headlam is pulling back in order to try and restore its profitability.

Today’s sales growth figures suggest Likewise is having some success at this strategy, given that overall market conditions for UK flooring are said to be fairly subdued at the moment.

Presumably this explains today’s use of the word “exponential” to describe Likewise’s market share gains – it’s hard to imagine this happening unless competitors are withdrawing (or going out of business).

Despite this apparent success, Likewise isn’t immune to the headwinds facing Headlam. This makes me wonder what’s being required to achieve this level of growth. Margins are wafer thin in this business and costs are only heading one way.

I suspect pressure on margins might explain why today’s update is only in line despite sales growth running at twice forecast levels.

I continue to have some concerns about the economics of this business and the strength of Likewise’s finances. Aggressive, debt-assisted expansion in difficult market conditions is not without risk.

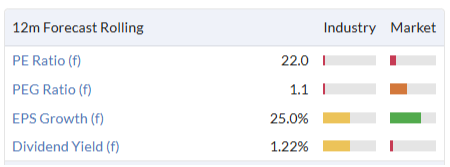

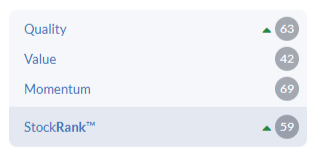

With a forward P/E of 22 and limited visibility, I also think the good news is already priced in here – a view also reflected in the stock’s relatively low ValueRank:

However, I do recognise the strong sales momentum Likewise is generating and the possibility that strategic clarity and strong leadership will allow Likewise to steal a march on underperforming rivals.

To reflect this mix of factors, I’m going to move my view up by one notch to neutral today. AMBER ↑

GB (LON:GBG)

Down 9% at 223p (£515m) - Full-year results for the y/e 31 March 2026 - Roland - AMBER =

GBG, the global identity and location technology business, publishes its audited results for the year ended 31 March 2026.

Shares in this software group have never recovered from the sell-off they suffered from late 2021 through to mid-2023:

In theory, I always feel there should be an opportunity here, but in reality GB seems to keep frustrating investors.

Today’s results are a case in point – the shares are down by c.10% as I type, after the company unveiled a whopping £73m impairment charge and warned that increased spending could hit margins this year. This news has overshadowed some more positive achievements from last year:

GBG Go “our adaptive identity platform” has secured 100+ wins since launch, ahead of expectations.

Americas Identity returned to growth in Q4 with improved execution and “accelerating momentum into FY27”.

New and expanded relationships with global brands including Equifax, FedEx, Uber, Remitly and Temu.

Let’s take a look at today’s results in more detail.

Full-year results - key points

One reason for GB’s weak share price performance in recent years is that its revenue growth has slowed dramatically:

Unfortunately today’s results do not address this shortcoming. Nor is there much improvement on profit:

Revenue up 3.2% to £285m (constant currency)

Adjusted operating profit up 0.7% to £67.5m

Reported (loss) before tax of £(74.5)m

Adjusted earnings per share up 9.3% to 19.0p

Dividend unchanged at 4.4p per share

Net debt up 65% to £80.1m

Revenue: full-year growth is weak but is in line with consensus estimates. Performance improved sequentially through the year, too. CEO Dev Dhiman expects to carry this H2 rate of growth into FY27:

H1: 1.8%

H2: 5.7%

Profit adjustments: like revenue, adjusted operating costs and adjusted operating profit were also broadly flat last year:

Source: GB Group FY26 results

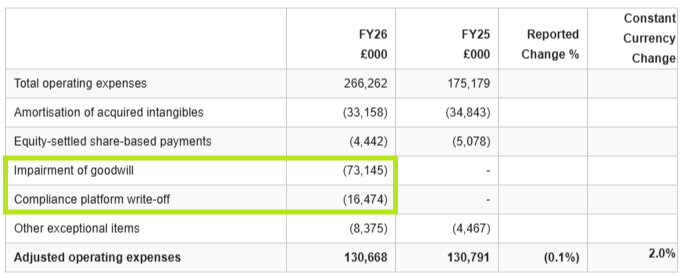

However, the reported figures were marred by some big impairments that plunged GB to a reported net loss of £75m last year:

Compliance platform write-off: this relates to a legacy product that is being retired - this was flagged up in the H1 results so shouldn’t have been a surprise today.

£73m goodwill impairment: this relates to the Americas Identity business unit, where revenue has declined in each of the last three years. The company has revisited its valuation for this unit based on “more cautious assumptions” and “reasonable market multiples” and decided it is appropriate to reduce the level of goodwill being carried to reflect a lower value in use. I don’t know the history of the Americas business, but there’s still £217m of goodwill attached to it, suggesting it was developed through sizeable acquisitions.

The impairment of the Americas business appears to have surprised the market today and does seem disappointing – especially as this unit is said to have returned to growth in Q4 and delivered operational improvements last year:

Good execution improvements: Sales productivity initiatives reduced time-to-revenue by >50%; an increase of 20% more renewals containing minimum commitments, and 3x new business ACV with >35% pre-committed

Cash generation: rather than debating the merits of GB’s recurring profit adjustments, what I usually do in these situations is to see how a company’s free cash flow compares to its various profit metrics.

I would expect a software business like GB to enjoy fairly consistent and strong cash generation.

My sums do indeed suggest good underlying free cash flow conversion (before working capital movements and acquisitions), albeit still lower than in the prior year:

FY26: £40.5m (FY25: £45.3m)

The main point I’d make here is that these figures are reasonably close to GB’s adjusted net profit of £47.0m and £44.3m for FY26 and FY25 respectively. So I am happy to use the adjusted profit measures as an approximate guide to business progress.

Debt-funded buybacks: the increase in net debt last year to £80m reflects the £45m spent on buybacks.

I am not convinced that borrowing money to buy back shares can be described as “capital allocation discipline”, but this decision probably does explain why adjusted earnings per share rose by 9% last year despite adjusted operating profit rising by less than 1%.

Funnily enough, checking last year’s annual report shows that the FY26 long-term incentive plan award criteria for the CEO and CFO are based 50% on earnings per share and 50% on total shareholder return relative to the FTSE 250.

Buying back shares is likely to be beneficial to both of these metrics, although as it happens even £45m of buybacks (from a starting market cap of £739m) was not enough to lift GB’s share price over the last financial year.

The market cap on 1 April was just £470m; it’s £515m today.

This tells me that last year’s share buybacks were probably carried out at share prices significantly above today’s price.

While leverage remains manageable at 1.15x EBITDA, I don’t think that’s the point here.

FY27 Outlook

The early success of GBG Go has prompted management to accelerate investment in this platform:

We will make a one-off operating cost investment of £6 million in FY27 to accelerate Go's innovation roadmap through expanded use of an existing development partner to supplement GBG's technology team.

This will release additional capability earlier such as expanded fraud and identity signals, and agentic readiness to target category leadership aligned with customer demand.

As a result, GB is guiding for an adjusted operating margin of 21% to 22% in FY27, down from 23.7% in FY26.

I guess this may prompt brokers to trim their earnings estimates slightly for this year.

I don’t have access to any updated forecasts today, but based on previous consensus for revenue of £300m this year, this new guidance suggests FY27 adjusted operating profit could fall by 4% c.£64.5m.

Assuming no further buybacks this year, I would guesstimate this could leave GB trading on a FY27E P/E of c.11.

Roland’s view

Before considering whether to invest in GB, I’d want to spend some time learning more about the company’s competitors.

Strong competition is the only obvious reason I can see why the company is struggling to deliver stronger revenue growth. After all, as management points out in today’s slide pack, this is a growing market:

Source: GB Group FY26 presentation

My underlying free cash flow estimate of c.£40m gives GB a trailing free cash flow yield of c.8% at current levels. Management has indicated a similar cash performance is expected this year too.

I think GB shares should offer value at current levels, but I can’t help feeling a little cautious. While I’m prepared to overlook some of last year’s profit adjustments, I’m discouraged by the use of large amounts of debt for share buybacks, the big impairment charge, and the persistently sluggish top line growth.

Guidance is for revenue growth to improve to c.5% for in FY27 and potentially accelerate further in following years. If that can be achieved while maintaining c.20% operating margins, I think this business should be worth more in the future.

However, I can’t ignore the reality that today’s outlook appears to suggest a cut to FY27 profit guidance.

On balance I am going to maintain Graham’s previous neutral view today, but I’d certainly be open to an upgrade if the company can show some evidence of improving momentum this year.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.