S&P SpaceX Decision: overnight, S&P has announced that it will not change its eligibility requirements in order to fast-track mega-IPOs such as SpaceX into its indices.

In addition to free float requirements, the two main rules for inclusion are:

Seasoning: companies must be publicly listed for at least a year.

Profitability: for indices like the S&P 500, companies must have positive net income for the most recent quarter and in total for the four most recent quarters (this is why Tesla spent so many years outside the S&P 500, despite being easily large enough to qualify).

I must say that I’m glad that S&P aren’t changing the rulebook for mega-IPOs. Firstly, it’s important for the character of their indices. Gaining entry to the S&P 500 has always meant something, and it would change the character of the index to dilute that meaning.

Secondly, an important effect of the rules these days is the protection of ETF investors. While seasonality and profitability requirements don’t prevent index investors from having a bad outcome, they do serve to protect them from some of the riskiest situations.

Unprofitable, newly-listed companies are almost by definition riskier than profitable, mature stocks. But other major providers have been adjusting their rules to give newly-listed large-caps faster entry to their indices.

So well done to S&P Dow Jones for this decision. For the millions of passive investors who expect their funds to invest in blue-chip stocks, it's the right call.

Overnight market movements:

The FTSE is set to open unchanged at 10,350

S&P 500 is down 0.5% at 7,550

Brent crude is up 0.2% at $95.40

Gold is down 0.6% at $4,445

Bitcoin is down 1.2% at $63,000

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Raspberry PI Holdings (LON:RPI) (£1.6bn | SR51) | SP +27% H1 profitability materially ahead of H1 2025. The strong profitability delivered in the first half is expected to result in FY 2026 EBITDA being significantly ahead of current market expectations (consensus: $42m adjusted EBITDA). | AMBER ↑ (Graham) We were AMBER/RED on this last time, with the company warning of limited visibility and trading at what seemed to be a very expensive earnings multiple of 30x. The share price has exploded since then, up by nearly 4x. I’m going to have to upgrade our view on the stock, as it has very clearly negated some of the reasons for caution at the beginning of the year. The memory shortage is being overcome and price rises are being passed onto customers. | |

Bodycote (LON:BOY) (£1.41bn | SR85) | SP -10% | AMBER/GREEN = (Graham) | |

Resolute Mining (LON:RSG) (£1.26bn | SR76) | SP -6% Q2 has been impacted by logistical and supply chain disruptions over the past four weeks due to security challenges in Mali in late April and May 2026. Q2 gold production to be c. 30 koz versus original expectation of 40 - 45 koz. Production at Syama is expected to be around the lower end of the guidance range of 195 - 210 koz in 2026. | BLACK | |

Seraphim Space Investment Trust (LON:SSIT) (£444m | SR93) | Monthly newsletter covering £137m capital raise and developments at various portfolio companies. | ||

| Tufton Assets (LON:SHIP) (£233m | SR94) | Market and NAV Update | Intra-quarter update. NAV $413.5m, NAV per share $1.546. “The product tanker and bulker markets remained strong in April and May. Product tankers (which carry diesel, petrol, aviation fuel, chemicals etc.) saw benchmark rates decrease slightly in May from the highest levels of the past decade.” | |

BTG Consulting (LON:BTG) (£202m | SR92) | Buys MVLOnline.co.uk, a specialist solvent liquidations website. | ||

Evoke (LON:EVOK) (£180m | SR60) | SP +13% | TAKEOVER (Graham holds) | |

Somero Enterprises (LON:SOM) (£98m | SR77) | SP +4% “Stabilization in US private non-residential construction, the Company's largest market, continued and the positive trading momentum from the end of 2025 carried over with trading in the five months ended 31 May 2026 tracking well against the full year ending 31 December 2026 guidance.” Also conducting a thorough review of governance arrangements and legal constitution. | AMBER = (Graham) In March, Somero guided that 2026 would see revenue, profitability and cash generation "broadly comparable" to 2025. Unfortunately, those 2025 results were a big disappointment compared to the prior year, with revenues falling 19% and PBT down 36%. I have suspected for some time now that Somero is struggling against homegrown US competitors offering much cheaper screeding tools. After this in-line update, I'll leave our neutral stance unchanged. | |

Iofina (LON:IOF) (£82m | SR87) | Agreement with a new brine water supply partner to provide additional brine water to its IOsorb® plant, IO#11, located in Central Oklahoma. | ||

STV (LON:STVG) (£49m | SR40) | H1 TAR expected to be up c.4%. “Whilst we expect a boost in advertising revenue from the FIFA World Cup, we remain cautious on the outlook for the second half of the year given the underlying softness in the advertising and commissioning markets driven by the continuing uncertain geopolitical situation.” | ||

Revolution Beauty (LON:REVB) (£37m | SR37) | REVB has been notified by the FCA that its investigation into the Company has ceased and no further action will be taken against the Company. "It is fitting to receive this news from the FCA at a time when Tom and Adam are back involved in the business and have reinvigorated it with a clear strategy. The early signs that this strategy is working are very encouraging, and the future is much brighter for the Revolution brand." | RED = (Graham) | |

Kendrick Resources (LON:KEN) (£28m | SR18) | Initial assessment confirms Kieshöhe has the potential to emerge as a major rare earth discovery. “These results mark an important milestone in the development of the Bonya Rare Earth Project and significantly enhance our view of the potential scale of the district.” | ||

Defence Holdings (LON:ALRT) (£26m | SR11) | The Transparency Notice states that the proposed engagement carries a value of approximately £226,000 over a three-month term and covers testing phase of the capability. | ||

Genedrive (LON:GDR) (£20m | SR14) | R&D tax credit refund of approximately £0.76m from HMRC in respect of FY June 2024 and FY June 2025. |

Graham's Section

Evoke (LON:EVOK)

Up 13% at 45p (£180m) - Recommended all-share acquisition of evoke plc - Graham - TAKEOVER

(At the time of writing, Graham has a long position in EVOK.)

This has been a stubborn holding of mine for years, and it seems to be reaching some sort of a conclusion.

The board of Bally's Intralot S.A. ("Intralot") and the board of evoke plc ("evoke") are pleased to announce that they have reached an agreement on the terms and conditions of a recommended all-share acquisition

We’ve known since April that Bally’s were interested in evoke. We were told then that Bally’s were considered an offer of 50p per share.

Bally’s is a Greek lottery company, listed on the Athens stock exchange: here’s the StockReport. It has a market cap of €2.2 billion (£1.9bn), so about 10x the value of evoke.

Today’s proposal is as follows:

0.537 New Intralot shares for each evoke share, representing a value of 52p based on the Intralot share price of €1.12

Cash offer: alternatively, evoke shareholders can elect to receive 52p in cash. If they fail to do that, they will automatically receive Intralot shares by default.

And there’s an important condition: the max amount of cash that Intralot will pay is capped at £117m. If demand for the cash offer exceeds this amount, then shareholders will get scaled back pro rata.

Premium: the proposal represents a premium of 138% vs. the EVOK share price, prior to the announcement of a Strategic Review.

Intralot’s perspective: the combination will create “a global gaming and lottery champion with scaled pan-European B2C, adding significant reach across locally regulated markets”.

evoke’s perspective: the UK government’s tax hikes on the gambling sector were a major cause for the Strategic Review which has ultimately led to this proposal. RGD on online gaming has increased from 21% to 40%, and duty on online betting will increase from 15% to 25% next year:

The evoke Board considered that these changes represent a material shift in the UK operating environment and, given evoke's significant UK exposure, were expected to have a material adverse impact on the evoke Group's profitability and cash generation. On the evoke Group's initial estimates, prior to mitigating actions, these changes would increase duty costs by approximately GBP 125-135 million on an annualised basis once fully implemented representing 36 per cent. of evoke's FY 2025 EBITDA…

evoke expected to mitigate about 50% of the hit, but that still hits profitability by over £60m, results in much smaller long-term growth prospects (as the mitigating actions include less marketing and promotional activities, and shutting stores), and severely challenges the ability of the group to tackle its £1.8 billion debt pile.

We are informed that Intralot has already made five earlier proposals, with the first of these being at 32p per share.

Under the current proposal, Intralot will redeem evoke’s 2028 bonds - which solves a major problem. evoke admit that they “faced near term refinancing risk with the upcoming 2028 maturities”. They currently have a junk rating “B” at Fitch, with a negative outlook.

Irrevocable undertakings/letters of intent: shareholders representing 29% of the company have already pledged to vote in favour of the scheme.

Graham’s view

I expect this to go ahead. Intralot is a credible buyer and as I said before, they must have a very detailed debt management plan in order to go ahead with it. Some of those details are laid out in today’s announcement.

And as I think that evoke could easily be a zero if it doesn’t get taken over, I am strongly in favour of this deal.

No offense to Intralot, but I’d rather have 52p rather than an Intralot share. So that’s what I’ll be asking for. If other evoke shareholders do the same, which seems likely, we will all end up getting scaled back accordingly.

And well done to the evoke board for salvaging something for us and for striking a hard bargain.

Previous awful decisions, by the previous management team - the takeover of William Hill, basically - ruined shareholder value here. The UK tax hikes were then the nail in the coffin. But at least we didn’t walk away with absolutely nothing.

Of course the smart thing for me to have done would have been to sell on the day of that announcement, which was pretty much at the top:

Trading approach: I’ve been asked why I held onto my 888/evoke shares for so long.

As this is sort of a philosophical point, I’d like to explain generally why I think that not selling works so well for me, most of the time, even when it’s painful.

The basic reason is this: I don’t think I’m smart enough to time my entries and exits on a regular basis. If I was moving stocks like Andrew Left does, then maybe I’d be able to do it. Or if I followed a different approach, e.g. regularly rebalancing with the help of an automated system, then it would make sense.

But my approach is simply to find stocks where I like the fundamentals and the price. Sometimes I’m right and sometimes I’m wrong. And after I’ve done my research, I want to gain the full benefit of that work. That means holding the investment for the long-term.

Fresh ideas come along regularly, and I’ll invest in them when I can, but I don’t want to spend my life jumping from one good idea to another. Intellectual honesty means admitting that I can’t predict which of my ideas will perform the best over the long term - so I see little point in constantly juggling them.

When I do sell, it’s for one of three reasons:

Cash flow: if I personally need cash.

Change of opinion: if I no longer believe in the investment thesis.

Concentration: if a stock has done very well and is too large as a percentage of my portfolio.

These are all good reasons to sell. But for me at least, they are rare.

Being a long-term holder who rarely sells has created four multi-baggers in my portfolio (Volvere, Berkshire Hathaway, IG Group and Next). They have all been very boring holdings, most of the time.

If I had sold evoke shares back in 2021 on the day of the William Hill announcement, that would indeed have been smart. But if I had been smart enough to do that, I might also have thought myself smart to sell IG when it announced the expensive acquisition of tastytrade, also in 2021. But the IG share price is up by well over 100% since then, and it has also paid out 250p per share in dividends. So that would have been a dangerous game to play.

Everyone has their own approach, and that’s fine. But as I’ve been questioned about my evoke holding a few times, I wanted to give my answer. The answer is that I like holding investments through to their conclusion, and it seems to work for me.

This does mean I might get a zero some day. evoke could very well have been a zero. But it has already been priced like an option for a while now, so I was fine with holding that option and seeing what happened. The final result is a reasonable one, in the circumstances. We move on!

Raspberry PI Holdings (LON:RPI)

Up 27% at £10.42 (£2.01 billion) - Trading Update - Graham - AMBER ↑

It doesn’t feel like this has been listed very long. The IPO price was 280p in June 2024.

It’s had a remarkable year, especially the last few months:

Today it upgrades expectations.

Key points:

H1 profitability materially ahead of H1 last year.

Over 4 million units, adjusted EBITDA at least $38m.

Profitability may cool down in H2 (emphasis added):

Despite DRAM related price increases, the Company has seen continued robust demand for its products from OEMs and other customers. In the second half, the Company will focus on the strategic opportunity to gain market share and further strengthen customer relationships. Unit economics are expected to moderate in H2 as inventory of memory procured at a lower cost in earlier periods is depleted.

DRAM = dynamic random-access memory, a key input for Raspberry Pi. The market for DRAM is supposed to be experiencing an AI-induced shortage right now, as mega corporations are hoovering up all available supply.

Raspberry Pi again says there are challenges with both the pricing and availability of DRAM and other memory. The company said the same back in January. But it is now “confident that it can secure the inventory necessary to meet its FY 2026 production goals”.

Conclusion:

The strong profitability delivered in the first half is expected to result in FY 2026 EBITDA being significantly ahead of current market expectations.

Market expectations for FY26 adjusted EBITDA are given as $42m. This consensus figure clearly makes little sense now, with 90% of it having already been achieved in H1.

Graham’s view

We were AMBER/RED on this last time, with the company warning of limited visibility and trading at what seemed to be a very expensive earnings multiple of 30x.

The share price has exploded since then, up by nearly 4x.

I’m going to have to upgrade our view on the stock, as it has very clearly negated some of the reasons for caution at the beginning of the year. The memory shortage is being overcome and price rises are being passed onto customers.

Where I would add caution is that today’s statement clearly warns about the sustainability of H1 profitability. Selling old inventory that was cheaply assembled always creates turbo-charged profits after a period of high inflation. My understanding is that DRAM prices have trebled over the past year. But Raspberry Pi will have to pay new DRAM prices when building new inventory, and that cost will be reflected in future profits.

So it seems to me that real, sustainable profitability is still very hard to judge here.

But still, I’m switching us to neutral. This one is in my “too difficult” tray - well done if you’ve been participating in the rally this year.

The StockRanks see enough Quality to give it an average StockRank, despite the lack of obvious value:

Bodycote (LON:BOY)

Down 11% at 735.5p (£1.26bn) - Response to statement by Apollo - Graham - AMBER/GREEN =

This takeover idea has ended very quickly.

On 22nd May, Bodycote confirmed it had received a possible cash offer from private equity giant Apollo at 885p per share. Discussions were ongoing.

Two weeks later Apollo has walked away, as politely as possible:

Apollo confirms that it does not intend to make a firm offer for Bodycote… Apollo continues to hold Bodycote and its management team in high regard, is appreciative of the discussions with them and Bodycote's board of directors, and would like to thank them for their time and consideration of the proposal.

In response, Bodycote says this:

The Board of Bodycote has strong confidence in Bodycote's potential and its strategy to create a high-performing, resilient business with attractive growth prospects. Bodycote continues to execute well on the group's Optimise, Perform and Grow initiatives, with a positive start to 2026 trading as set out in the AGM trading update of 27 May 2026.

Reasons aren’t given, so I don’t see much value in speculating as to what has happened. It could be a simple matter of disagreement over price. What we do know is that Apollo and Bodycote have remained polite to each other in public, which puts a limit on how serious the disagreement might have been. Perhaps Apollo will look at Bodycote again at some point.

Graham’s view

We turned AMBER/GREEN on Bodycote in March so I will leave that stance unchanged today.

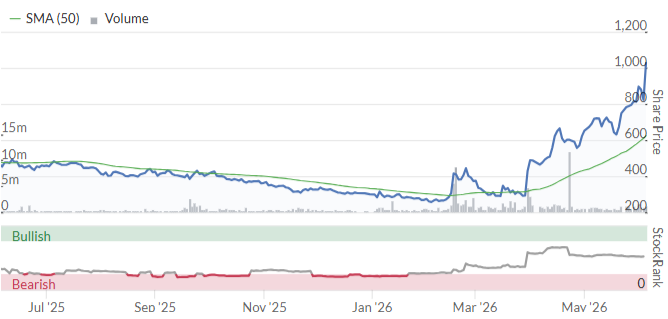

Could it be that we’ve reached the point where the most obvious takeover candidates have left the London market already, and buyers have to be a little more careful now? The Bodycote share price has been firm over the past year:

With Bodycote sticking around, the next one to leave looks like it might be Tate & Lyle (LON:TATE). The PUSU deadline for that one is next Thursday, 11th June.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.