Bitcoin had its worst week since 2022 last week, after Strategy (NSQ:MSTR) was said to have “tested the market” by selling 32 bitcoins in order to fund dividends. It has since attempted to fix the narrative with the purchase of 1,550 bitcoins.

The Strategy share price is down by over 70% since its high last year. The explosive success it previously enjoyed led to a wave of copycat “Bitcoin Treasury” companies in London.

Kospi Index in Korea fell 6% yesterday, and is now down 12% over the past week. I was flabbergasted to learn recently that two tech stocks - Samsung and SK Hynix - are worth about half of the value of this entire index.

Gold is down 11% over the past month (measured in USD), not helped by changing interest rate expectations. Measured in GBP, it’s down 9% over the month.

Overnight market movements:

The FTSE is set to open unchanged at 10,230

S&P 500 is down 0.3% at 7,360

Brent crude is down 0.2% at $90.60

Gold is down 1.3% at $4,200

Bitcoin is down 1.4% at $61,300

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Vodafone (LON:VOD) (£25bn | SR86) | Vodafone Greece and Public Power Corporation have entered into heads of terms for a 50:50 JV comprising their fibre to the home networks and wholesale fibre businesses in Greece. | ||

Tritax Big Box REIT (LON:BBOX) (£3.9bn | SR43) | A decision on planning at the Manor Farm data centre is expected on or before 7th July. The probability of securing planning consent remains unchanged. | ||

Pennon (LON:PNN) (£2.4bn | SR33) | Revenue +23%. Underlying PBT £135.1m (FY25: loss £35.1m). Statutory PBT £114.4m (FY25: loss £72.7m). Return on Regulated Equity 6.7%. “Our financial performance will continue to improve through increased revenues and ongoing focus on cost management…” | ||

Clarkson (LON:CKN) (£1.44bn | SR79) | Directorate change (CFO appointment) | New CFO joins from BP (Senior VP, Finance and Risk). | |

Ceres Power Holdings (LON:CWR) (£1.19bn | SR18) | Gross proceeds of £103m. Placed 17.8m new shares at a price of 570p. 18 new shares in total, including retail offer. 6.5% discount to yesterday’s close. | ||

Molten Ventures (LON:GROW) (£1.09bn | SR86) | Isar Aerospace is “a leading European space launch company creating access to space from Europe”. GROW invested €30m into a €270m Series D financing round. | ||

Workspace (LON:WKP) (£641m | SR43) | Transforming to An Earnings-Focused Business (FY26 results) | Net rental income down 7.1%. Trading profit after interest down 9.4%. Loss before tax £120.5m “primarily reflecting the reduction in the property valuation”. EPRA net tangible assets per share £6.87. “Enquiries and lettings remain resilient, despite the noted economic backdrop.” Expecting a substantial step down in trading profit after interest for FY27. Considering further property disposals. “While we can cover all of our debt maturities until March 2028 using existing undrawn facilities, we are actively reviewing our refinancing options.” | |

WH Smith (LON:SMWH) (£622m | SR22) | TU: revenue +5% at constant FX. LfL revenue +2%. Given the ongoing uncertainty from the Middle East conflict and pressures on gross margins, including the recent deterioration in the North America division, the Group expects to deliver FY26 Headline Group profit before tax and non-underlying items of £75m - £90m. Fundraise: up to 26 million new shares representing c. 20% of its existing share capital. | BLACK (RED= ) (Graham) | |

Intuitive Investments (LON:IIG) (£557m | SR55) | Net assets £498.1m. NAV per share 207.5p. “The first half of the year has seen a step-change in operational progress at Hui10, with rapid expansion of its national infrastructure, strong growth in transaction volumes and the achievement of several strategically important partnerships.” | TAKEOVER (reverse takeover, IIG shareholders to own 99% of the combined group) | |

Enquest (LON:ENQ) (£356m | SR92) | EnQuest Petroleum Production Malaysia has agreed to acquire three separate packages that include interests in four offshore production sharing contracts in Malaysia. Max total consideration $833m, of which $554m to be paid upfront. Will be funded by ENQ’s existing debt facilities and cash resources. | AMBER/GREEN = (Roland) This looks like a sensible deal to me at a reasonable price. Enquest is buying mature assets from Petronas to expand its production in the region and reduce dependency on the North Sea. While the increase in leverage carries some risk, I don’t see it becoming a problem unless oil/gas prices fall sharply. While today’s share price gains and the increase in debt leave Enquest looking a little more expensive than it was, I am happy to leave our moderately positive view unchanged. | |

Fuller Smith & Turner (LON:FSTA) (£348m | SR79) | Revenue +5.7%. LfL sales +4.9%. Adjusted EPS +38% to 47.18p. Outlook: Momentum continues with like for like sales for the 10 weeks to 6 June 2026 rising 4.4%. | AMBER/GREEN = (Roland) [no section below] This looks like an encouraging set of results from this pub group, with revenue up ahead of inflation (maybe?) and an improvement in operating margin to 10.1% (FY25: 7.5%). This improvement in margins has fed through to a substantial increase in underlying free cash flow, which I estimate at £24m excluding disposals. This gives a trailing free cash flow yield of >10%, which could be decent value. However, my sums suggest the group still only generated a return on capital employed of 6.3% last year. This suggests to me that the current valuation of just under 1x book value is probably about right. This is a fairly capital-intensive property business, after all. To reflect the improvement in profitability and consensus expectations for further progress in FY27, I am leaving our previous broadly positive view unchanged today. | |

Caledonia Mining (LON:CMCL) (£275m | SR70) | “The results demonstrate the presence of significant gold mineralisation across multiple zones and highlight the opportunity for Motapa to evolve into a strategic extension of the Bilboes mining complex, potentially enhancing production and extending the life of mine at Bilboes through the development of a combined mining operation.” | ||

Central Asia Metals (LON:CAML) (£233m | SR70) | Production for first five months of 2026 ahead of corresponding periods in 2025 in all three metals. H1 2026 operational update scheduled to be released in early July. Both operations on track to achieve 2026 production guidance. | AMBER/GREEN = (Roland) This update is an addition to the group’s normal reporting schedule and seems intended to shore up sentiment following the poorly-received news of the Cygnus Metals acquisition. For me, the core issue is that the high-margin, cash generative appeal of the Kounrad copper business is being diluted by less profitable mines and exploration/development projects. These efforts could pay off in time, but in the meantime shareholders risk losing the benefit of CAML’s impressive cash generation and must trust that management is creating long-term value rather than simply empire building. Despite these concerns, I think CAML could be cheap at current levels if the copper market remains strong, as expected. | |

Helical (LON:HLCL) (£225m | SR30) | Existing tenant Fin has agreed new leases and taken additional space. A second tenant has regeared its lease across three floors. Both leases extend to 2037, with a break option in 2032. The two transactions combined will generate £4.5m of annual rent and are in line with March 2026 ERVs. Occupancy at The Bower is now 93.7%, with space under offer up to 96.6%. | ||

Tullow Oil (LON:TLW) (£223m | SR66) | Year-to-date working interest production was 43.1 kboepd, at the upper end of 2026 guidance for 34-42 kboepd. 2026 free cash flow guidance unchanged at $70-175m ($70-100/bbl). Hedging portfolio covers 60% of downside while retaining access to 60% of upside in 2026. | ||

VP (LON:VP.). (£192m | SR53) | Revenue -5.7%, adj EPS -18.4% to 54.5p per share. ROACE down 3% to 11.2%. Challenges in water and general construction. Outlook: continues to see “challenging market dynamics” but expects to report an improvement in FY27 trading vs FY26. Current year trading in line with market expectations. | ||

Frontier Developments (LON:FDEV) (£167m | SR92) | CMS Strategy delivers record financial results (FY26 trading update) | Revenue for y/e 31 May +16% to £104.8m, adj operating profit +44% to £19.0m. Net cash of £44m at 31 May. Growth driven by successful release of JWE3 plus contributions from Planet Coaster, Planet Zoo and the wider JWE franchise. | GREEN = (Graham) We've been GREEN on FDEV (e.g. Roland last time) and I’m inclined to stay that way today. The cash balance provides a lot of comfort, the strategy is clear, and risk is tempered by a) the proven strategy; and b) the tail of previous releases that continues to support revenues. In Stockopedia terminology, it’s a Super Stock. I acknowledge that there’s some weakness in the share price today, but I interpret it as profit-taking after shares had a very strong run (up 30% over the past month). The sellers today are “selling the news”, which is often smart, but I don’t think it detracts from the bigger picture. |

H-Power (LON:HPOW) (£145m | SR20) | 5,000kg hydrogen sale agreement signed with Protium, 15x LC30 order received from Speedy Hire (LON:SDY). Loss after tax reduced to £5.8m (FY25: £10.1m). Net cash of c.£17m at the end of April 2026. | ||

Cornish Metals (LON:TIN) (£136m | SR12) | Construction continues with surface civil works at Roskear shaft complete and the winder house under construction. Dewatering is underway through the 195-level pump station. | ||

Beeks Financial Cloud (LON:BKS) (£131m | SR19) | Announces three additional contract wins across Beeks Analytics, Proximity Cloud and Private Cloud offerings, with a combined total contract value ("TCV") of c.£1.7m. These support expectations for the current financial year (y/e 30/6). | AMBER = (Roland) [no section below] I looked at Beeks in more depth on Monday. As I commented then, Beeks appears to be taking it down to the wire to meet revenue forecasts this year. Two out of three of today’s contract wins are expected to generate revenue this month, ahead of the company’s 30 June year end. An update from broker Canaccord Genuity today estimates that these could contribute c.£0.7m to FY26 revenue and suggests that Beeks is now “largely on track to meet our FY26 revenue forecasts”. I don’t see any reason to change my neutral view today. | |

Motorpoint (LON:MOTR) (£105m | SR32) | Revenue +8.1%, pre-tax profit +82.9% to £7.5m. EPS +78.4% to 6.6p, in line with exps. Share used car market (<10 year old) increased to 1.68% (FY25: 1.46%). Outlook: strong momentum has continued into FY27, with retail volume growth of 15% in April/May and stable margins. | ||

Audioboom (LON:BOOM) (£83m | SR24) | Deferred consideration of £0.9m relating to a revenue growth target is payable; 30% of the maximum deferred consideration agreed when Adelicious was acquired. No contingent consideration is payable relating to a specific (unnamed) podcast as it has not exceeded the £2.0m minimum revenue guarantee threshold. | ||

R E A Holdings (LON:RE.). (£52m | SR87) | The group's agricultural operations have continued to perform positively during the first five months of 2026 with production slightly ahead of budget.” Notes that CPO prices have recovered since the Indonesian government announcement in May regarding export regulations. | ||

Power Probe (LON:PWR) (£51m | SR45) | “Trading in 2026 remains encouraging and in line with management's expectations.” A focus on own-branded products and private label brands has supported “a strong recovery in Group gross margin”. In line with previous guidance, 2026 revenues are expected to be H2 weighted to reflect the timing of new product launches. | ||

Time Out (LON:TMO) (£38m | SR15) | Time Out has entered into a franchise agreement with Vinyl (ASX:VNL) for the operation of its Australian media business. The initial term of the agreement is five years. | ||

Petra Diamonds (LON:PDL) (£30m | SR20) | Business Rescue Practitioners have been appointed to the Finsch Diamond Mine and have taken over custodianship of the mine. They have begun suspending production activities and will now formulate a Finsch-specific business plan. | ||

Diales (LON:DIAL) (£15m | SR96) | Revenue +9.4%, underlying operating profit +43% to £1.0m, adj EPS +30% to 1.3p. Net cash +62.5% to £3.9m. Utilisation rate of 70.2% (H1 25: 71.4%) due to the timing of some contracts in the Middle East. Outlook: enters H2 with “strong momentum”. Confident of of delivering FY results “at least in line with market expectations”. | ||

Fulcrum Metals (LON:FMET) (£14m | SR12) | A contract has been signed with Test Design Implement Solutions LLC in Ontario Canada for the operation of a pilot plant that will use Extrakt’s cyanide-free leach technology to process material from Fulcrum’s Teck-Hughes project. |

Graham's Section

WH Smith (LON:SMWH)

Down 19% at 400.8 (£507m) - Trading Update, Proposed Capital Raise & Retail Offer - Graham - RED =

First, some context. We’ve been negative on this one as trading has been weak, earnings forecasts have slumped, and balance sheet leverage has looked excessive.

I turned RED (from AMBER/RED) in December.

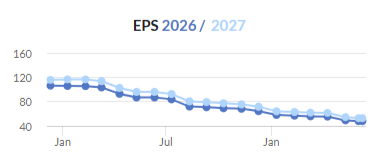

EPS forecasts:

Share price:

I don’t wish to restart the entire buyback debate, but it’s worth mentioning that SMWH carried out a £50m buyback in FY August 2025, which in hindsight was a ridiculous decision. Megan at the time said that the buyback was “bizarre”.

The right time for a buyback is when a) the business has more cash than it needs, and b) the share price offers attractive value. This was not the case for SMWH in 2025.

Trading update

The key points from today’s trading update, for the 14 weeks to 6th June:

UK LfL revenue up 2%

North America LfL revenue down 1% (although Total revenue grew)

Group LfL revenue (including rest of world) up 2%

North America sounds really weak, with LfL revenue in the last 7 weeks down 4%.

The main culprit there is Resorts, with LfL revenue down 11% in the last 7 weeks, “driven by the continued reduction in Las Vegas visitor numbers”. Air saw LfL revenue down 2% “reflecting reduced passenger numbers following recent air fare inflation and a reduction in airline capacity linked to the Middle East conflict”.

Some radical actions are being taken in the Resorts segment:

…14 uneconomic fashion stores now either closed or with agreed closure dates. The remaining 12 fashion stores are likely to be exited in the balance of the year. The Group is also considering strategic options for its Welcome to Las Vegas business.

I associate WH Smith with magazines and meal deals, not Vegas fashion. This Vegas adventure seems to be nearing its end.

Outlook: FY26 headline group profit before tax and non-underlying items of £75-90m.

Management's expectations for the full financial year reflect the observed and anticipated decline in passenger numbers and weakening consumer demand across all divisions and a reduction in brand marketing, increased promotional activity and inflation headwinds across the Group.

I think that the market was expecting headline PBT to come in around £91m, whereas the new guidance has a midpoint of only £82.5m. The company itself had previously guided for £90-105m.

It’s also worth bearing in mind that the last few years have seen very heavy adjustments. As I’ve said before, the use of the word “Headline” in relation to profits always makes me nervous. I associate it with dirty accounts and that’s true in the case of WH Smith, where last year’s “Headline” figure of £108m translated into statutory PBT of a measly £2m.

So even if we get £82.5m of headline profits this year, that will only tell a fraction of the story.

Indeed, today’s guidance includes the warning that there will be “a significant non-underlying non-cash impairment charge of to £150m for the full year relating to goodwill and store impairments”.

My verdict: this is a pretty serious profit warning with a c. 10% reduction in the PBT forecast against market expectations and a warning of very large impairment charges, so there is zero prospect of clean financial results in the near-term.

Proposed capital raise

Prior balance sheet info: Previous guidance from the company was for net debt of around £420m at the year-end date, August 2026. Headline net debt was £496m as of February 2026, giving a leverage multiple of 2.9x (right at the top end of what could be considered reasonable).

This figure does not include the present value of leases. Including leases, WH Smith’s net debt was £1.0 billion as of February 2026.

While 3x is typically the upper limit of what might be considered a reasonable leverage multiple, I actually think a stricter limit should be applied to retailers with heavy lease liabilities. This is not just because the leases themselves are a form of leverage (although that alone is a good reason), but also because experience tells us that most retailers are prone to occasional bouts of severe weakness. So maybe we should accept max leverage of only 1.5x for retailers?

Today’s announced fundraise is for 26 million new shares. The current share count is 125 million, so this is an increase of 20%.

There will be both a placing and a retail offer, and WH Smith’s largest shareholder Causeway Capital says that it will participate pro rata (not increasing its percentage shareholding).

Rationale:

As set out in the Trading Statement, the Company has experienced a downturn in trading conditions as a result of the conflict in the Middle East which has impacted passenger numbers. In addition, the weaker consumer confidence environment has further impacted spend per passenger…

…the Board believes the Capital Raise is in the best interests of shareholders and that raising equity is a prudent and proactive step which will strengthen the balance sheet, enable continued execution of the Group's growth and transformation agenda, provide greater confidence around the Group's leverage position, and reduce the Group's reliance on debt funding as it executes its long-term growth strategy.

Accordingly, the Capital Raise is expected to reduce leverage from the current higher than targeted leverage levels to around 2x by the end of the 2026 financial year.

Graham’s view

We’ve been RED on this, in large part because of the horrific balance sheet, so I am in favour of the company taking steps to address the issue.

Let’s suppose they sell 26 million new shares at about £4 each (around the current share price). In round numbers, that’s about £105m raised before expenses.

That’s going to be a huge help, but is it even enough?

The interim balance sheet had a tangible value of minus £300m. So it will still be deeply in the red.

A leverage multiple of 2x is arguably ok, but it’s still not at a level where I’d be sleeping soundly at night. As stated above, I think that lease-heavy retailers need special treatment and a max leverage multiple of 1.5x might be more reasonable as a general rule. Of course each individual case is different.

And with net debt in February of nearly £500m, the planned fundraise may only reduce this figure by 20-25% (depending on when it is measured).

The big question is whether an additional c. £100m will be enough to get the company back into a position where it’s sustainably cash flow positive.

I’m drawn to this statement by Exec Chair Leo Quinn (the previous CEO quit after the company discovered accounting errors). Quinn says:

…we are now taking action to sell, exit or renegotiate loss-making or low-return situations and, where appropriate, we are replacing directly-run operations with franchises in sub-scale markets. While we make meaningful progress in these areas, we must continue to invest in our core business to drive more productivity. Our underlying processes and systems need upgrading to provide the data for stronger management of risk, working capital and speed of response…

The impact of these actions will both require investment and result in a substantial non cash write off; but the returns to be had are clear.

I accept that the £150m impairment charge will be non-cash, but it sounds to me as if there will also be significant cash costs in order to upgrade the business, even if many of them are categorised as “non-underlying”.

Combine these cash costs to upgrade the business with a less profitable trading environment, and I’m drawn to the conclusion that a large part of this fundraise might end up being lost to near-term troubles rather than to fundamentally addressing the net debt issue.

For these reasons, I’m going to stay RED on WH Smith. It’s a share I’ve always liked but at this stage, the risk levels remain too high for me.

Stockopedia is unimpressed too, calling it a “Sucker Stock”.

Frontier Developments (LON:FDEV)

Down 8% at 433.3p (£154m) - CMS Strategy Delivers Record Financial Results - Graham - GREEN =

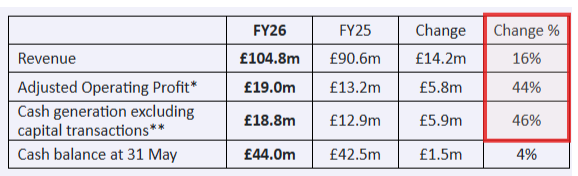

This is an impressive table of results highlights for FY May 2027. We have impressive gains in revenue, adjusted operating profit and cash generation:

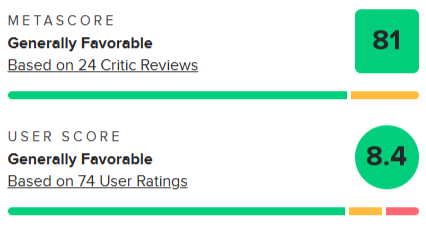

Please bear in mind that the title launch schedule can create a lumpy revenue profile for FDEV. They released an important new title Jurassic World Evolution 3 during the year and this was met with positive reviews, e.g. on Metacritic:

Buybacks: £15.5m of share buybacks will additionally boost earnings per share by 11% from next year. But the cash balance has remained very healthy at £44m.

Jurassic World Evolution 3: the initial revenue boost from this title will be followed up by additional paid downloadable content (PDLC).

On 16 June 2026, a major expansion themed around the Jurassic World Rebirth film will introduce new content and gameplay features. Additional content is planned throughout FY27 to further engage the player base and attract new audiences.

In other news:

Planet Coaster has “a strong roadmap of new content” in place for FY27.

Planet Zoo 2 is scheduled for release on 13th October 2026

Warhammer 40k: Chaos Gate also scheduled for release in FY27.

Further ahead, FDEV is creating “a new own-IP CMS game to create a new Planet franchise in FY28”. No further details but this supports the goal of creating one new CMS (Creative Management Simulation) game per year.

Current trading/outlook:

FY27 is expected to start positively, supported by Jurassic World Evolution 3 joining Microsoft's Game Pass subscription service on 2 June 2026, the upcoming Jurassic World Rebirth expansion on 16 June, and expected portfolio sales ahead of the summer promotional period.

Alongside continued revenue contributions from existing games, FY27 performance will be driven by the release of Planet Zoo 2 and Warhammer 40,000: Chaos Gate - Deathwatch. The Board has been encouraged by the positive reception to the announcements of these games and is confident in delivering FY27 in line with its expectations.

Graham's view

I agree with the strategy of sticking to their knitting. They are good at it and the CMS genre isn’t going out of fashion - I remember loving Theme Park back in the day (that game having been published back in 1994!).

As for the shares, we’ve been GREEN on them (e.g. Roland last time) and I’m inclined to stay that way today.

The cash balance provides a lot of comfort, the strategy is clear, and risk is tempered by a) the proven strategy; and b) the tail of previous releases that continues to support revenues.

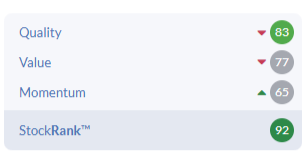

In Stockopedia terminology, it’s a Super Stock:

What could go wrong? Well, they’ve obviously messed up before in terms of game launches that didn’t quite work. I consider visibility here to be lower than average, but they are clearly trying to mitigate those risks.

It’s remarkable to think that these shares were valued at over £30 if you scroll back several years:

They were overvalued then, but I think there’s a case to be made that they are undervalued now, with the cash balance covering nearly 30% of the market cap.

I acknowledge that there’s some weakness in the share price today, but I interpret it as profit-taking after shares had a very strong run (up 30% over the past month). The sellers today are “selling the news”, which is often smart, but I don’t think it detracts from the bigger picture.

Roland's Section

Central Asia Metals (LON:CAML)

Up 1.8% at 134p (£237m) - Trading Update and Outlook - Roland - AMBER/GREEN =

This small cap copper and lead/zinc producer has fallen out of favour with shareholders this year, despite record copper prices:

There seem to be two likely reasons for this.

Disappointing production: as Mark discussed in April, CAML reported (slightly) disappointing Q1 production and revealed a reduction in the life of mine estimate for its lead/zinc mine, Sasa.

A big acquisition: on 2 June, CAML announced the all-share acquisition of pre-production copper-gold miner Cygnus Metals (ASX:CY5) for A$232m (c.£120m). This valuation was based on a CAML share price of 156p per share, but the stock is already trading 14% below this level.

This could suggest that CAML investors are unhappy about the dilution involved and sceptical about management’s ability to create value through this dilutive and large deal, which will see Cygnus shareholders own 30% of the enlarged CAML business post-acquisition.

Without getting into too much detail, Cygnus appears to have a decent-sized copper/gold asset in Canada which needs funding to develop for production. The logic for the deal is that CAML’s strong cash flows can be used to develop this mine.

However, the acquisition announcement doesn’t mention the expected capital expenditure or timescale needed to reach production. This means investors are left needing to do more research and modelling to gain an informed view on the potential returns from this deal.

Trading update: intended to reassure?

Today’s update from CAML covers production for the first five months of 2026. It appears to be an addition to the group’s reporting ahead of its usual half-year update in July.

I can’t help feeling that the main purpose of today’s RNS is to try and shore up support for the share price, rather than imparting any urgent news.

Production: full-year guidance is unchanged today, but output from the group’s operations still seems to be lagging slightly behind the run rate required to hit the mid-point of production guidance:

Kounrad (copper): 5,141 tonnes (FY26 12-13,000 tonnes)

Sasa (zinc-in-concentrate): 7,566 tonnes (FY26: 18-20,000 tonnes)

Sasa (lead-in-concentrate): 11,142 tonnes (FY26: 26-28,000 tonnes)

We are reminded that copper and zinc prices are comfortably ahead of the same period last year:

Record copper prices contributing to an average received price to end-May of $13,076 per tonne ($9,377 per tonne in the first five months of 2025)

Average received zinc price to end-May of $3,299 per tonne1 ($2,765 per tonne)

Average received lead price to end-May of $1,934 per tonne ($1,952 per tonne)

CEO Gavin Ferrar is bullish about the forthcoming H1 results:

H1 2026 is shaping up to be a highly profitable and cash-generative period for the Group, supporting our stated dividend policy.

However, commentary on costs is slightly more vague, in my view:

I am pleased to report that CAML has thus far not experienced any supply-chain issues with respect to raw materials and other inputs to our operations, and input prices remain normal.

Outlook: a fuller H1 operational update is scheduled for July and CAML expects the first drilling results from its exploration projects in Kazakhstan in Q3.

Copper production at Kounrad is typically weighted to H2 due to the impact of the warmer weather, supporting hopes for full-year production in line with guidance.

As far as I can tell, there’s no change to financial guidance today – on that basis, current forecasts put CAML on a forward P/E of less than 5:

Roland’s view

CAML has been listed on AIM for around 15 years. Until 2017, it was a single asset business producing copper from waste dumps at Kounrad, in Kazakhstan. This is an extremely profitable and cash-generative business and CAML has a history of generous dividends.

In 2017, CAML acquired the Sasa lead/zinc producing mine in Macedonia. More recently it’s invested in a number of pre-production and exploration projects.

As I see it, the challenge for shareholders is that this business is evolving from a relatively simple and high-margin cash cow into a more complex and speculative multi-asset business.

To illustrate this, CAML’s operating margin has fallen from 49.5% in 2016 to an underlying figure of 29.7% in 2025, despite the fact that copper prices have tripled over the same period.

In fairness, it’s possible that this business will end up as a much larger and more diversified mining group with a number of attractive assets. On the other hand, it might not.

In my experience, many mining CEOs appear to be genetically programmed to spend money on new projects when they find themselves in charge of cash-rich businesses. CAML falls into this category, with strong free cash flow and a net cash position of c.$80m at the end of May.

The problem for shareholders is that while these spending sprees create larger businesses, they don’t always create more equity value.

One consequence – arguably – of the group’s efforts to diversify and expand was that last year’s final dividend was cut, despite soaring copper prices.

Mark alluded to this situation in April:

… despite a good record of dividend payments, I think there's a risk that management's priorities don't align with shareholders'.

I share this view, but I think it’s also sensible to recognise how cheap CAML shares have become:

While I’d view the 12% forecast yield with caution – my sums suggest 9% might be a safer assumption – I think this is still cheap, assuming copper prices remain stable.

On balance, I share the StockRanks view of this business as a potential Contrarian play:

I’m comfortable leaving our AMBER/GREEN view unchanged today.

Enquest (LON:ENQ)

Up 18% at 22.5p (£422m) - Significant Acquisition in Malaysia - Roland - AMBER/GREEN =

Enquest is known as a North Sea operator, but it also has a long-standing presence in Malaysia. This acquisition will see the group acquire a number of assets from state oil operator Petronas.

At first glance this looks like another example of an independent operator acquiring mature production assets from a major. As we’ve seen in recent years, this can be a cash-generative and profitable model for smaller operators.

Today’s acquisition has received a positive reception from the market and appears to have a number of attractive qualities:

The new Participating Interests together add c.57.4 kboepd of production

This will take group production to > 100 kboepd, with the potential to maintain production at this level through to the end of the decade.

South East Asia contribution increased to 69% (with the UK North Sea contributing 31%)

Enlarged Group 2025 production is weighted 63% liquids and 37% gas (the new Participating Interests 47% liquids and 53% gas)

The transaction will add 138 MMboe of 2P reserves, taking the group total to c.300 MMboe.

Opportunities to unlock a further c.65-100 MMboe (net) through recovery factor enhancement

Enlarged Group unit opex of $16 per boe; a c.35% reduction. Average opex of c.$10 per boe for the new Participating Interests

Higher production at lower costs should help Enquest to maintain strong cash generation even if oil and gas prices ease. A greater weighting to gas production is not a bad idea either, in my view. It reduces exposure to oil market volatility while capitalising on strong demand for gas in Asia (and elsewhere).

What is Enquest paying?

$554m on completion

$189m payable over three years in equal installments

Up to $90m in continent consideration, subject to the decision on whether to proceed with three identified projects in the Balingian PSC.

Total consideration: up to $833m

I estimate this is equivalent to between $5.40 and $6 per boe of reserves being acquired

What’s the financial impact?

This deal is being funded with debt but the expected leverage doesn’t seem excessive to me, barring an oil price crash.

Net debt will rise to c.$1bn

Pro forma EBITDA based on 2025 results would have been c.$900m (FY25 actual: $504m)

These figures give a pro forma leverage multiple of 1.1x, post completion

Enquest has faced debt problems in the past, but I don’t think this level of borrowing is likely to become an issue unless oil and gas prices face an extended period of weakness. That seems unlikely to me, currently.

Valuation: Enquest shares are up by 20% today and I think it’s fair to conclude the company is paying a reasonable price for these assets.

However, investors also need to consider the impact of the increase in net debt on Enquest’s valuation. My sums suggest that on a pro forma basis, Enquest is now a little more expensive than it was 24 hours ago:

Enquest EV/EBITDA ratio (prior to today): 1.4x

Enquest pro forma EV/EBITDA ratio: 1.74x

Harbour Energy EV/EBITDA: 1.5x (for comparison) (disc: I hold HBR)

Roland’s view

I don’t have the time or expertise to analyse this transaction in depth, but my impression is that it’s a sensible deal that is most likely to generate a positive outcome for Enquest shareholders.

While the debt-funded nature of the deal (rather than issuing equity) carries some initial risk, I think it’s manageable. Assuming no major upsets, then over time this structure should lead to an increase in cash generation per share and returns on equity.

I don’t see any reason to alter our previously moderately positive view of this business, whose CEO and founder Amjad Bseisu remains the company’s largest shareholder. AMBER/GREEN =

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.