Iran: there’s been genuine progress, although it remains difficult to quantify as the text of the US-Iran agreement has not been published yet. A key provision is that the Strait of Hormuz will be open for 60 days, allowing negotiations and the fragile ceasefire to continue. The Strait is not currently open for business.

Early last week, Brent crude oil (for August delivery) reached a high of $98. As I type this, it’s below $83. There’s still a gap to fill, to reach pre-war levels of $60-70, but it’s progress.

Japan: I note that the famous “widow-maker” Japan trade, which involves shorting their government bonds (JGBs), continues to perform well.

Here’s the Japanese bond yield. A rising yield means that the value of the underlying bonds is falling:

This is even a trade that I temporarily sat in, about ten years ago. Unfortunately, its reputation as a widow-maker was not without justification: JGBs were remarkably resilient for a remarkably long time.

But that technical fact didn’t stop thousands of traders from betting that JGBs would collapse. Their (or perhaps I should say “our”, as I was one of them) reasoning was impeccable. Japanese rates were close to zero or even negative. Their debt to GBP ratio was over 200%. Their population was shrinking. Logically, it didn’t make sense that rates could stay at that level.

However, the irrationality of markets outlasted our exuberance, and many traders who attempted to short JGBs have been retired by the markets by now. The Bank of Japan has just raised its benchmark rate to 1%, the highest level in over 30 years, and JGB yields are finally at normal levels. A timely reminder that whether we are looking at stocks or bonds, we can never assume that financial prices will return to “normal” within a reasonable timeframe.

Overnight market movements:

The FTSE is set to open up 0.7% at 10,542

S&P 500 is set to open up 1.3% at 7,524

Brent crude is down 4.4% at $83.50/bbl

Gold is up 1.7% at $4,288/oz

Bitcoin is up up 2.1% at $65,698

Today's Agenda is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Zegona Communications (LON:ZEG) (£4.0bn | SR61) | Broadband lines up 29k to 2,591k. Vodafone Spain revenue flat at €3,628m. Returned €1.6bn to shareholders, including €1.4bn special dividend. Year end net debt €3.2bn. | ||

Rathbones (LON:RAT) (£2.1bn | SR59) | Skilled Person Review following engagement with the FCA. Areas for improvement identified in UK wealth management re: the implementation of Consumer Duty and certain aspects of compliance, oversight and assurance. Voluntary pause on certain activities with clients that require Enhanced Due Diligence. | BLACK (AMBER) (Graham) I’m willing to look past the £60m of short-term costs. However, what’s really important is the effect that this review could have on long-term profitability. There could be a general overhaul of fees. Wealth managers such as Rathbones aren’t cheap and while some of their clients are financially sophisticated, many will not be. In the current regulatory environment, this puts the onus on Rathbones to deliver the best possible outcomes to them. I’d suggest that we could be looking at a 10-20% reduction in long-term profitability. The earnings multiple isn’t expensive but economic returns here have been average and I tend to think of it as a people business. I’m therefore inclined to take a neutral stance on it today. | |

International Workplace (LON:IWG) (£1.75bn | SR30) | Founder and current CEO becomes Exec Chair. Chief Transformation Officer becomes CEO. Non-Exec Chair becomes Deputy Chair. | ||

Hilton Food (LON:HFG) (£471m | SR69) | New independent non-Exec Chair. The current Exec Chair to become CEO. | ||

Tatton Asset Management (LON:TAM) (£369m | SR46) | Revenue +20.1%.Adjusted operating profit +24.1% to £28.5m. Adjusted EPS +22.3% to 35.05p. All of these figures are ahead of expectations. Outlook: maintaining growth target of £30bn assets under management and influence by the end of the financial year 2029. | ||

Boohoo (LON:DEBS) (£349m | SR38) | GMV down 21.6%. Adjusted EBITDA +35% to £53.3m. Pre-tax loss £109m. FY26 net debt £93m. Leverage multiple 1.75x, targeting <1x for FY27. Outlook: expecting GMV to return to growth. FY27 adj. EBITDA to grow at double digits. Operating costs to reduce further. | ||

Optima Health (LON:OPT) (£211m | SR61) | Revenue +15%. FY26 adj. EBITDA to be c. 10% ahead of previous expectations, as previously announced. Net debt £94m. | ||

Gulf Marine Services (LON:GMS) (£208m | SR71) | All vessels temporarily evacuated from one of the countries in the Gulf due to the prevailing geopolitical situation have now successfully returned to hire on the same contracts. Maintaining adj. EBITDA guidance for 2026 in the range of $105-115m but continues to assess the final financial impact of this disruption through ongoing discussions with clients. | AMBER = (Roland) [no section below] It looks like GMS hopes to secure at least partial payments from clients for the period when four of its vessels were out of action, although I don’t know how likely they are to succeed. As things stand, full-year guidance is unchanged. Broker Zeus also confirms its EBITDA forecasts are unchanged, while noting that Zeus’s $105m EBITDA estimate is at the bottom end of guidance. Looking ahead, the recent expansion of the fleet could support a stronger year of earnings in 2027, assuming normal market conditions. However, there’s no guarantee of the latter and the risk remains that management will overpay for fleet expansion to the detriment of shareholder returns. The current share puts GMS on a FY26E P/E of 10, which seems about right to me. I’m going to leave my previous neutral view unchanged today – a position also reflected by the StockRanks. | |

SThree (LON:STEM) (£206m | SR91) | Net fees down 7%. Rate of decline moderated through the half. Strong growth in USA. Performance for FY26 expected to be in line with the previously announced c.£10 million PBT guidance. | ||

Accsys Technologies (LON:AXS) (£187m | SR44) | LfL revenue +20%. Adjusted EBITDA +96% (€21.2m). Statutory loss before tax €0.6m. "This strong set of results reflects disciplined execution of our FOCUS strategy in a challenging macroeconomic environment.” Trading in line with the Board's expectations for FY27. | ||

Warpaint London (LON:W7L) (£174m | SR73) | Trading conditions continue to be difficult, but Q2 has been more encouraging than Q1 so far. FY expectations remain unchanged. | AMBER ↑ (Roland) An H2 weighting is expected this year, as improved margins and growth initiatives contribute later in the year. It’s too soon to be certain that the run of profit warnings seen over the last year has ended, but I think there’s enough here to justify upgrading to a neutral view. In my view, this business has a number of attractive qualities. If the company can deliver on forecasts this year, the P/E of 11 and 6% yield suggest to me the shares could offer value at current levels. The steady rise in Warpaint’s StockRank over the last three months is also encouraging, in my view. | |

Galantas Gold (LON:GAL) (£135m | SR28) | Voted to approve the acquisition of Sol de Oro Mining and in favour of the Company’s omnibus equity incentive plan”. A new non-board CFO has also been appointed. | ||

Smarter Web (LON:SWC) (£131m | SR20) | Oliver Hewett has been promoted to CFO. He was previously Group Financial Controller. He will not be appointed to the Board. | ||

IG Design (LON:IGR) (£87m | SR71) | Revenue -3% reflecting tariffs, pricing and softer UK demand. Adj operating profit -40% to £9.6m, adj EPS -28% to 7.2p. Outlook: guidance remains unchanged, expect 0-5% adj op margin of 4-5% and c.£5m free cash generation. | ||

Tpximpact Holdings (LON:TPX) (£59m | SR87) | Revenue +1%, with H2 revenue +16% vs H1. Adj EBITDA +54% to £8.6m with op profit of £0.8m and adj EPS of 5.4p (FY25: 3.0p). Completed three-year turnaround and halved net debt to £4.2m. FY27 outlook: expect double-digit revenue growth with adj EBITDA of not less than £12m. | ||

Alternative Income REIT (LON:AIRE) (£56m | SR50) | Responding to Friday’s offer of 70p per share: “There are many reasons why the Independent Board is not currently in a position to recommend the Glenstone Offer to shareholders, with the principal one being that Glenstone's Offer represents a 17 per cent. discount to AIRE's latest published net asset value of 84.4 pence per share as at 31 March 2026”. | TAKEOVER | |

Poolbeg Pharma (LON:POLB) (£53m | SR27) | Received notice of decision to grant for its POLB 001 cancer immunotherapy-induced Cytokine Release Syndrome ("CRS") patent. “... this grant increases the commercial value of POLB 001 to potential partners”. Trial data is expected over the summer. | ||

Gelion (LON:GELN) (£42m | SR5) | A subsidiary has signed an exclusive commercial licence agreement with the Max-Planck-Innovation GmbH for intellectual property covering nano-encapsulated sulfur cathode technology and novel nano-confined anode materials. This concludes an agreement announced in March 2025. Payment terms not disclosed. | ||

Christie (LON:CTG) (£36m | SR94) | “Robust levels of demand” so far this year with agency pipelines +19% in deal volumes. H2 weighting expected due to “slightly extended deal times”. Outlook: expect full year performance in line with expectations. | ||

Everyman Media (LON:EMAN) (£32m | SR50) | 3 board members controlling 45.6% would like to delist the company. They believe they have the support of shareholders representing a further 11% of the stock. Stakeholder discussions are underway. At this stage, the board believes it is likely that Everyman will be delisted. Trading: admissions +23.1% YTD (to 28 May 26), with revenue +26.5% and adj EBITDA +45.2% to £9.4m. FY26 Outlook: uncertain due to economic environment and dependence on Q4 trading. | ||

Gana Media (LON:GANA) (£30m | SR2) | Raising £750,000 through the issue of 375m new shares at 0.2p per share. Directors participated. Company reports new registrations and wagering volumes at Estadio Gana in Mexico are “up significantly” in Q2. | ||

Inspiration Healthcare (LON:IHC) (£23m | SR57) | Revenue +24% to £47.5m, gross profit +27% to £20.8m and adj operating profit of £0.8m (FY25 £(1.9)m. Net debt reduced to £5.1m. FY27 Outlook: currently trading in line and confident of meeting full-year expectations. | ||

Great Southern Copper (LON:GSCU) (£21m | SR3) | Scout reverse circulation ("RC") drilling commences at Artemisa South prospect, targeting old mine workings where structurally-controlled vein and disseminated type Cu-Au mineralisation occurs in granodiorite south of the La Colorada lithocap. | ||

Cizzle Biotechnology Holdings (LON:CIZ) (£13m | SR14) | CIZ1B biomarker (early stage lung cancer) test successfully accredited for clinical use in the U.S. under CLIA. Enables licensed U.S. healthcare providers to order the test signifying commercial launch. | ||

Galileo Resources (LON:GLR) (£12m | SR15) | Has entered into an agreement with a subsidiary of Sandfire Resources for the sale of Botswana prospecting licences PL039/2018 and PL040/2018. There will be an upfront consideration of $3m on completion, with a possible one-off success payment of $20-80m, subject to levels of contained copper. |

Graham's Section

Rathbones (LON:RAT)

Down 16.5% at £16.29 (£1.49bn) - Regulatory Update - Graham - AMBER

This is a grim update:

Rathbones Group Plc… announces that it has undertaken a Skilled Person Review following engagement with the Financial Conduct Authority… The review has identified areas for improvement within the Group's UK Wealth Management business regarding the implementation and embedding of Consumer Duty, as well as certain aspects of its compliance, oversight and assurance arrangements.

The words “Skilled Person Review” sends shivers down my spine.

This is when the FCA mandates a review of a company’s processes. We’ve seen it before with the likes of Jarvis Investment Management and S&U. They tend to be long and very expensive episodes and the outcomes can sometimes be very serious for the organisation.

Rathbones announces that it’s taking the following actions:

A programme of work addressing the recommendations from the review, which is expected to be conducted over a two-year period.

A two-year period - see what I mean about these reviews taking a long time? These reviews tend to hang over a company and its valuation for years.

Continuing:

A targeted review of a portion of our clients to assess whether they have received good outcomes.

The FCA’s Consumer Duty requires firms to act to deliver good outcomes for retail customers. That might sound somewhat subjective - because it is. If a review is happening, that says that the FCA wants some questions answered.

For a period of up to twelve months, a voluntary pause to the onboarding of new clients that require Enhanced Due Diligence ('EDD clients') whilst the Group focuses on implementing changes to its procedures and controls. In the last twelve months, relevant gross inflows from EDD clients totalled approximately £370 million.

A voluntary pause to the acceptance of inflows into general investment accounts from some existing EDD clients…

Let’s try to put the flow figure into context. In 2025, total gross inflows were £11.2 billion, while total gross outflows were £13.3 billion.

So £370m would not have been a huge percentage of total inflows, but it would have been significant in terms of its impact on net flows, if it had been paused last year (net outflows were £2.1 billion).

Due diligence has been a hot topic at financial firms for many years as governments have attempted to crack down on money laundering and tax evasion. So it’s a significant misstep if Rathbones’ procedures have not been up to scratch - the type of thing that can lead to serious but avoidable fines.

Costs: these actions are expected to cost £60m over the next two years. Rathbones will nevertheless continue with its £20m buyback as planned.

Fees on cash balances: underlying PBT will take a £9m hit in 2026 from ceasing to charge fees on cash balances in discretionary portfolios. This will be implemented from 1st July, so that’s a c. £18m hit if it’s annualised and if it becomes a permanent change. This is part of the company “reviewing certain aspects of its pricing as part of its ongoing commitment to delivering fair value for clients.”

Graham’s view

We don’t usually cover this stock but it looks like this story will be worth following.

I’m willing to look past the £60m of short-term costs. However, what’s really important is the effect that this review could have on long-term profitability.

According to market forecasts, Rathbones’ PBT was supposed to progress from c. £260m to c. £300m over the next few years.

It sounds like the FCA might take a dim view when it comes to charging investment management fees on customers’ cash balances in portfolios that are being managed by Rathbones. I’ve annualised the cost to £18m and while Rathbones might be able to mitigate that figure, I think it’s reasonable to assume that this change will be made permanent and most of it will not be mitigated.

After that, there might be a more general overhaul of fees. Wealth managers such as Rathbones aren’t cheap and while some of their clients are financially sophisticated, many will not be. In the current regulatory environment, this puts the onus on Rathbones to deliver the best possible outcomes to them.

So I would consider Rathbones’ earnings forecasts to be highly fragile now, even after we cut them by £20m to reflect the change to fees on cash balances. I’d suggest that we could be looking at a 10-20% reduction in long-term profitability, plus the short-term impact from one-off costs. The initial £60m estimate in that regard should be taken with a pinch of salt.

In conclusion: the 16% fall in the share price this morning seems approximately right to me, although I personally might have marked it down by 20%+.

The earnings multiple isn’t expensive: perhaps still in the region of 10x, depending on what happens to EPS forecasts after this announcement. But economic returns here have been average and I tend to think of it as a people business. I’m therefore inclined to take a neutral stance on it today.

The QualityRank is 47:

Roland's Section

Warpaint London (LON:W7L)

Up 1% at 220p (£178m) - AGM Statement - Roland - AMBER ↑

Today’s AGM Statement takes a fairly measured tone on trading, but leaves full-year expectations unchanged. If management can deliver on this, it could mark an end to the run of profit warnings we’ve seen over the last 10 months:

Key points:

The [challenging] trading conditions seen in 2025 continued into Q1.

Trading remains difficult, but Q2 sales from 1 April - 31 May are ahead of the same period last year.

Overall group sales are at “an improved margin” compared to 2025.

The group has “significant planned expansion opportunities” for later in 2026 and expects further margin improvement.

Expectations for the full year remain unchanged.

Inevitably this commentary means that an H2-weighting is expected this year:

… sales in 2026 are expected to be more second half weighted than prior years due to the timing of certain larger orders and planned customer rollouts.

Warpaint’s management flag up growth opportunities in Germany and the US:

Germany: launched a capsule range of W7 products into 2,200 Dirk Rossmann stores in May, “early sales are encouraging”.

US: “significantly improved Christmas order received from Walmart”. Warpaint will also be launching an online Christmas gift range with Ulta Beauty, “the largest specialty beauty retailer in the US”. This could lead to further opportunities in 2027.

Balance sheet: the company confirms that the balance sheet remains debt free, with cash of £20.6m at 31 May 2026 (May 2025: £15.0m).

Ward & Hagon: the company is in talks to renew a management consulting contract with Ward & Hagon for a further 24 months. The renewal is expected to include “additional sales responsibilities and increased time commitments” to reflect the expansion of the Warpaint business since the previous renewal on 1 February 2024.

The partnership with Ward & Hagon is a longstanding arrangement (since 2020) which has previously seen Ward & Hagon representative Paul Hagon serve as an executive director of Warpaint. As part of this renewal, Hagon will step down from the board.

Terms haven’t yet been finalised for the renewal, but the previous contract was priced at £225k per year. Further details of the renewal will be provided in due course.

Broker estimates

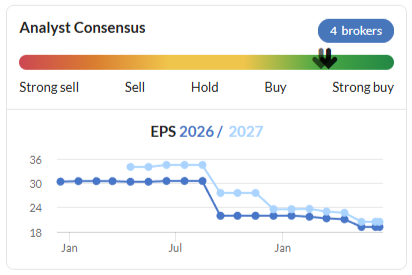

Forecasts from both Cavendish and Shore Capital are unchanged today and largely reflect the consensus estimates in the StockReport:

Roland’s view

I took a cautious view on Warpaint in April when the company issued a profit warning with its full year results. But I also noted at the time that “some value may be emerging” and suggested it could be worth watching for signs that the outlook had stabilised.

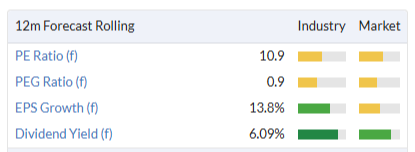

It’s too soon to be certain given the expected H2 weighting, but my feeling is that we may now have reached that point. The current valuation looks undemanding to me, with a P/E of 11 and PEG ratio of 0.9x, below the traditional value threshold of 1.0x:

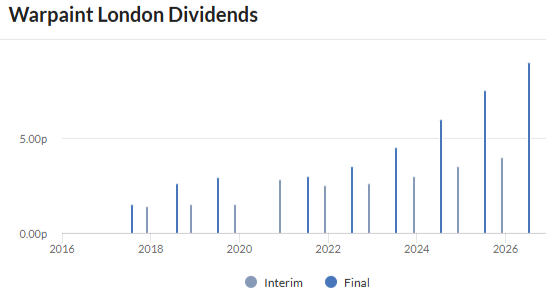

The 6% dividend yield – covered by earnings and net cash – is an additional attraction in my view. Except for a pause during the pandemic, Warpaint’s payout has not been cut since the company’s IPO in 2016 – a typical characteristic of companies with owner management:

Taking a quantitative view, Warpaint shares have consolidated at the current level for more than six months and the StockRank has been rising steadily:

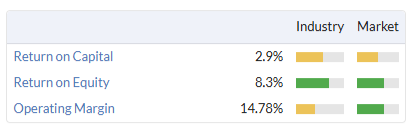

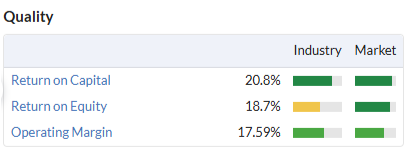

Finally, quality metrics for this capital-light business remain excellent, highlighting Warpaint’s ability to self-fund its growth while still generating attractive shareholder returns:

I am going to move our view to neutral today, with a view to turning more positive if guidance remains unchanged later this year. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.