Iran: The price of a barrel of oil has fallen by another c. $4 since yesterday, with a peace memorandum due to be signed in two days. The memo has been seen by Bloomberg News and includes the following points:

An immediate and permanent end to the war on all fronts, including Lebanon.

Undertakings to negotiate and reach a final agreement within 60 days.

The US to lift the naval blockade and Iran to allow merchant ships to pass through.

$300bn of financing for Iran, for rehabilitation and economic development.

The ending of all types of sanctions against Iran.

Iran will never produce nuclear weapons.

In summary: the conflict appears to be at an end.

SpaceX: the market cap of Space Exploration Technologies (NSQ:SPCX) was approaching $3 trillion at one point yesterday, overtaking Amazon and Microsoft and becoming the fourth-biggest US stock. It closed the day at $201.80, up an impressive 49% from its IPO price.

Yesterday was also important for the stock as it was the first day that options went live for it. 1.8 million contracts were traded, easily creating a new record for the volume of contracts traded on the first day of a new stock. Tesla has had an extremely active options market for years, and SpaceX has the potential to be even bigger in that regard.

Overnight market movements:

The FTSE is set to open down 0.1% at 10,480

S&P 500 is up 0.3% at 7,530

Brent crude is down 0.4% at $78.60/bbl

Gold is unchanged at $4,330/oz

Bitcoin is unchanged at $65,800

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Games Workshop (LON:GAW) (£6.7bn | SR79) | A dividend of 90p per share has been declared, the first dividend for FY27 (FY26: 85p). | GREEN = (Graham) | |

Tritax Big Box REIT (LON:BBOX) (£4.2bn | SR42) | Tritax has entered into an agreement to deliver a 125MW data centre in Essex, the second in its pipeline. The project will target a yield on cost of 10-11%. | ||

Kosmos Energy (LON:KOS) (£1.1bn | SR40) | Sale of interests in Ceiba Field and Okume Complex to Panoro Energy for c.$127m. Future contingent payments of up to c.$40m are possible. Proceeds will be used to repay debt. Updated full-year guidance will be provided in August. | ||

Hays (LON:HAS) (£568m | SR34) | Hays has sold operations in six European countries to Meraki Capital for net cash proceeds of c.£4m. The company is also exploring options in another 13 countries that are collectively expected to deliver a breakeven result in FY26. Hays now plans to focus on 16 core countries. | ||

AO World (LON:AO.). (£548m | SR72) | Revenue +11.4%, adj pre-tax profit +16.1% to £50.5m. Free cash flow up 152% to £66.4m, net cash of £16.4m. Will pay a £10m special dividend and carry out a £10m share buyback. FY27 outlook: external environment remains uncertain, but expect FY27 result in line with expectations. | AMBER/GREEN = (Roland) I can’t find much to dislike about these results. Profit margins doubled last year and the business appears to be generating attractive returns from its capital-light model. Cash generation is also good and shareholders should benefit through a special dividend and buyback. Forecast for FY27 are unchanged today and suggest slower growth ahead of a stronger result in FY28. The valuation looks reasonable to me, if not obviously cheap, so I’m happy to maintain our broadly-positive view on this founder-led business. | |

Guardian Metal Resources (LON:GMET) (£458m | SR28) | Purchase includes 841 acres of real property zoned for mixed use, as well as 2,540 acre-feet of annual water rights. The property is less than 10 miles from the Company's Tempiute Tungsten Project. | ||

PZ Cussons (LON:PZC) (£392m | SR83) | Upgrade to FY26 profit guidance: expect FY26 LFL revenue growth of c.6%, with reported revenue of c.£540m. Reflecting strong trading, expects FY26 adj operating profit to be at or slightly above previous guidance of £53-57m. The company has already taken actions to offset expected FY27 cost inflation related to the Middle East. | AMBER/GREEN = (Roland) Operating profit guidance for the year is nudged higher and is now c.13% above the company’s original guidance one year ago. This improvement hasn’t fallen through to EPS forecasts though, as I explain below. While I think PZC still faces some potential issues, I’m broadly positive about the outlook here. With the stock trading on c.13x FY27 forecast earnings, I’m happy to maintain our existing view today. | |

Social Housing REIT (LON:SOHO) (£284m | SR63) | Will acquire senior living assets comprising 1,907 rental flats and 256 housing manager flats from Residential Secure Income (LON:RESI) for £108.3m, with £45m in cash and c.£62.3m in new shares at 94.23p per share. The acquisition has a reported valuation yield of 6.63% and will increase SOHO’s EPRA NTA to £471.4m. | ||

Hargreaves Services (LON:HSP) (£249m | SR98) | Expects to report FY26 revenue ahead of expectations and pre-tax profit in line with expectations, reflecting the mix of contribution from the group’s three businesses. (Company-compiled consensus: revenue £288.2m, adj PBT £33.4m, EPS 64.1p). Cavendish updated EPS forecasts: - FY26E adj EPS: 75.7p (unch.) - FY27E adj EPS: 48.8p (unch.) - FY28E adj EPS: 50.7p (prev. 48.1p) | AMBER/GREEN = (Roland) [no section below] I’m a long-term fan of this business (and its management) and today’s update doesn’t alter that view. However, FY26 profits will be boosted by a £7m one-off item and earnings are currently expected to fall in FY27 – a view confirmed by broker Cavendish today. Hargreaves’ shares currently trade at c.1.3x book value and on 16x FY27E earnings. For a capital-intensive business with a trailing ROE of 11%, this valuation seems about right to me. I’m going to leave our previous broadly-positive view unchanged today. | |

Tristel (LON:TSTL) (£185m | SR79) | Appointed Christopher Lee as CEO from 1 August 2026. He was recently CEO of UK medical device business Summit Medical Ltd from 2020-2025. | ||

Rockwood Strategic (LON:RKW) (£185m | SR59) | NAV total return of 7.1% to 266.44p/share. NAV rose by 54.7% to £149.4m. Issued 17.3m new shares to meet demand, increasing share count by 44.5%. NAV Total Return from period end to 12 June was 17%, to 311.64p. | ||

Savannah Resources (LON:SAV) (£161m | SR37) | Has signed additional MoUs with various community groups in areas close to the proposed mine site. Plans for a bypass road around Boticas are being progressed. | ||

Smiths News (LON:SNWS) (£157m | SR94) | Secured long-term contract with News UK & Ireland (publisher of The Sun and The Times). The contract expands the areas in which Smiths is the exclusive distributor for News UK, “effectively securing national distribution of News UK’s leading titles” from July 2027 through July 2037. Expected to deliver a c.£125m uplift in annual revenue from July 2027. Certain implementation costs will be incurred ahead of this time. Dividend guidance unchanged. | GREEN = (Graham) | |

GreenX Metals (LON:GRX) (£144m | SR11) | Tannenberg mineralisation consistent with producing Polish Kupferschiefer copper-silver mines. Review by independent metallurgist confirms potential suitability for a conventional flotation-based processing route, as used at KGHM's long-running operations and planned for Lumina Metals' Nowa Sól project. | ||

Castings (LON:CGS) (£142m | SR84) | Revenue -2.1%, with operating profit +108% to £10m. Dividend maintained at 18.4p. Despite subdued demand, foundry is now operating more efficiently. Forward order schedule suggests an increase in volumes of 5% to 10%. A recent power restriction to William Lee has now been lifted. | AMBER = (Roland - I hold) [no section below] These results are in line with expectation and highlight a significant improvement in profitability after a cyclically-challenging period for the business. Looking ahead, there seems some scope for top line growth as well as improved margins. However, I think the real test will be whether the company can succeed in building a more diversified customer base that’s less closely tied to cyclical demand from truckmakers. Early signs seem positive, with increased orders from wind farms and new capacity for larger castings. But I think it’s too soon to be sure. Castings’ robust balance sheet and good cash generation provide some protection but last year’s improved results still only showed a return on capital of 7% – not really enough to justify a premium to book value. I’m naturally biased and inclined to be positive, but in reality I think the valuation is probably up with events on a near-term view, following recent gains. | |

Brave Bison (LON:BBSN) (£108m | SR42) | SP +5% H1 net revenue increased by “at least 92%” to not less than £23m, while adj EBITDA is in line with management expectations. Trading remains weighted towards H2. | AMBER/GREEN = (Graham) [no section below] Valuation makes me a little nervous here, given that this can be viewed as a marketing consultancy (P/E 12.5x as of last night). And today's AGM statement doesn't provide an overall organic growth rate, which undermines the values of the headline growth rate given. We are told that the acquired business MiniMBA has organically grown by 18%. We've been moderately positive on BBSN and on balance that continues to look like a reasonable stance, given the momentum it's enjoying. Do watch out for an H2-weighting, with 53% of full-year revenues anticipated to arrive in the second half. Cavendish are forecasting full-year EPS of 8p. | |

Roadside Real Estate (LON:ROAD) (£105m | SR15) | Acquisition of Ross Road Petrol Filling Station & Completion of Acquisition | Agrees to buy a standalone filling station in Gloucester for £2.9m. Has now completed the £28.6m acquisition of the Hoch Group portfolio of 12 petrol station forecourts and a standalone convenience store in Cumbria. | |

Speedy Hire (LON:SDY) (£92m | SR40) | Revenue down 0.1%. Adjusted EBITDA down 12%. Adjusted loss before tax £9.8m. Statutory loss before tax £32.3m. “New financial year has started well, with revenue to the end of May 2026 c.2% ahead of the prior year.” Reconfirms market guidance for FY2027. | ||

Arrow Exploration (LON:AXL) (£76m | SR72) | The Icaco 2 exploration well was spud May 18, 2026, and reached target depth on May 26, 2026. It was drilled, on time and under budget and encountered multiple hydrocarbon-bearing intervals. Total gross corporate production is approximately 5,000 boe/d. | ||

Likewise (LON:LIKE) (£68m | SR63) | Year to date revenue +17% like-for-like. Given the widespread Global tension and uncertainty, H2 26 is very difficult to predict, but the Board remains confident in achieving market expectations for FY26. | AMBER = (Graham) [no section below] Impressive growth continues here and Likewise has continued to build momentum in recent weeks (20.8% like-for-like growth in June so far). But I think we are right to be neutral on this share, e.g. see Roland's recent coverage which outlined various positives and negatives. Being very careful when it comes to the floor coverings sector is generally the right approach for investors, and pre-tax margins at this distributor are expected to be only c. 2.2% this year. The £80m market cap suggests to me that the market is already pricing in margin expansion in 2027 and beyond - years for which there are no broker forecasts. The market's optimism might be justified but I think we are right to stay cautious. | |

Frenkel Topping (LON:FEN) (£64m | SR77) | Revenue +11%. PBT +24% (£5.2m). Funds under management £1,803m (2024: £1,560m). Current year: Trading remains in line with board expectations for the current year to date. | ||

Aura Energy (LON:AURA) (£57m | SR8) | The Swedish Parliament voted to amend the country's Nuclear Activities Act so that uranium mining will no longer be regulated as a nuclear facility. Consequently, uranium extraction no longer requires explicit municipal consent, creating a more predictable permitting framework which will facilitate future uranium mine development. | ||

Oxford Metrics (LON:OMG) (£52m | SR61) | Revenue +3%. Adjusted EBIT loss £0.2m. Management's expectations for FY26 remain unchanged, with revenue for the 15-month period expected to be approximately £56m, noting the delayed timing of an IVMS customer project… [GN note: some revenue has been delayed but it is still expected to fall within the 15-month financial year to Dec 2026.] | ||

CML Microsystems (LON:CML) (£49m | SR65) | Revenue £20.45m (FY25: £22.90m). Loss from operations, excluding exceptional items, of £1.93m. Cash £12.8m. Net assets £51.45m. “FY26 delivered significant strategic and operational progress despite continued market headwinds.” | ||

80 Mile (LON:80M) (£43m | SR43) | Written guidance from the Greenlandic regulator confirms that no third-party licence can be granted over the Company's hydrocarbon concessions covering the Jameson Land Basin, East Greenland. The Company continues to maintain guidance for drilling to start during H2 2026, subject to receipt of final approvals. | ||

Cadence Minerals (LON:KDNC) (£29m | SR54) | Mobilisation of the Azteca restart programme at the Amapá Iron Ore Project in Brazil has been completed and refurbishment works are underway across the principal processing, infrastructure and electrical workstreams. Cadence's total investment in Amapá is c. $16.1m, representing a 36.2% equity stake. | ||

Wynnstay Properties (LON:WSP) (£23m | SR68) | Rental income +7%. NAV per share +3.8% to 1,212p. Portfolio valuation up 2.9% on a like-for-like basis. “We have delivered very satisfactory performance from our property investments and operations over the past year…” | ||

Frontier IP (LON:FIPP) (£13m | SR19) | Placing closed at 12p, raising gross proceeds of £3.9m plus another £0.1m from Subscription. Retail Offer being conducted to raise up to £0.4m. |

Graham's Section

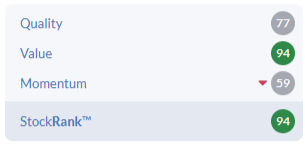

Smiths News (LON:SNWS)

Up 6.5% at 67.5p (£167m) - Contract Win - National Distribution - Graham - GREEN =

Some positive news: Smiths News has agreed “a transformational long-term contract with News UK & Ireland Limited”. News UK publishes The Sun, The Times and The Sunday Times.

The contract provides “(i) an expansion of the distribution territories in which the Company is appointed as News UK's exclusive wholesale distributor, thereby effectively securing national distribution of News UK's leading titles across all of Great Britain, to take effect from July 2027 and (ii) an extension in the contract term of our appointment through to July 2037.”

The revenue uplift is c. £125m per annum from July 2027, although it will require expansion of their distribution network with one-off implementation costs and transition costs. These will be funded from existing cash resources.

CEO comment:

"We are delighted to announce the extension and expansion of our partnership with News UK through to 2037.

This deepens a relationship spanning more than 50 years, securing a reliable and sustainable national route to market for retailers and consumers - and enabling us to freeze delivery service charges for our retail customers for the life of the Contract.

Estimates: Canaccord Genuity have left their forecasts unchanged today, pending further guidance. Smiths News say that they will provide further guidance on the financial effects of this contract “in due course”. Preliminary results for FY August 2026 are due in November, and those results will include the new guidance.

Graham’s view

I’ve been GREEN on this due to its excellent cash generation and clean results which have seen the company move into a net cash position and continue the payment of generous dividends relative to the market cap (the expected yield was over 10% last night).

What’s fascinating is that this contract might change the narrative around the company’s declining distribution business. Instead of shrinking, the company’s network is going to expand - presumably at the expense of smaller distributors.

It’s counterintuitive, but in a world where print newspaper circulation is declining, it seems that News UK prefers to have one national distributor, rather than multiple distributors. Declining circulation has therefore created a growth opportunity, through increased market share.

In the long-term, of course, print circulation should continue its overall decline.

But for now at least, and perhaps for the foreseeable future, Smiths News’ long-expected demise has been postponed further into the future. An incremental £125m should boost revenue forecasts by over 12%.

I’m obviously going to stay GREEN on this today. This cigar butt appears to have plenty of puffs left in it. It was trading at 6x earnings as of last night’s close, and is categorised as a Super Stock by the algorithms.

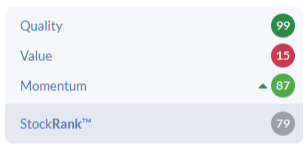

Games Workshop (LON:GAW)

Up 1% at £205.60 (£6.8bn) - Dividend Declaration - Graham - GREEN =

This is a tiny RNS:

The Board has declared a dividend of 90 pence per share, being the first declared dividend for 2026/27 (2025/26: 85 pence). This is in line with the Company's dividend policy as set out in its Annual Report and Accounts.

Graham’s view

Roland covered the full-year trading update here last month. That brief update didn’t mention any cash figure; the half-year report said that the company had cash of £171m, with a “cash buffer” of £85m.

For context, the dividend announced today will cost £30m. So there is no issue when it comes to affording it. Games Workshop has a long track record of successfully distributing the cash that is “truly surplus” to their requirements.

I also note this little line from the interim report:

We are not planning any share buybacks or acquisitions.

Refraining from buybacks is also what I would do at this valuation:

That said, I can’t find any record of Games Workshop buying back its own shares in recent decades, so I doubt that they would do so even at a lower valuation.

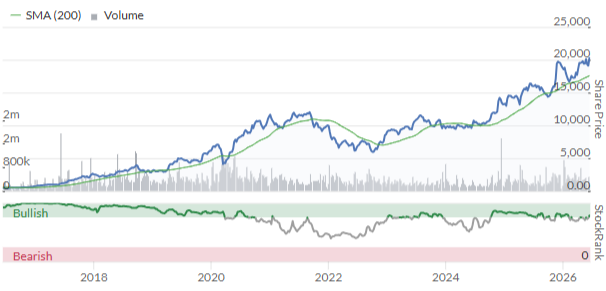

The absence of buybacks hasn’t held back the stock price:

I’m going to leave our GREEN stance unchanged today. It’s a High Flyer, for good reasons (i.e. exceptional business quality).

Roland's Section

PZ Cussons (LON:PZC)

Up 7.6% at 98p (£421m) - Trading Update - Roland - AMBER/GREEN =

PZ Cussons shares have risen by 35% so far this year as signs have emerged that a difficult turnaround may now be delivering results for this venerable consumer goods group.

I covered this business in a recent Stock Pitch, so I’m pleased to see that today’s full-year update (y/e 31 May) confirms a return to revenue growth and nudges profit guidance higher.

Key points:

FY26 like-for-like revenue growth is expected to be c.6% (FY25: 8.0%)

Reported revenue (not LFL) is to be c.£540m (FY25: £514m)

FY26 adjusted operating profit to be “at, or slightly above” the upper end of the £53-57m guidance range.

Net debt is expected to be under £30m, a reduction from £112m at the end of May 2025. This largely reflects the proceeds from the sale of the group’s 50% stake in PZ Wilmar.

Is this a big upgrade? Not really.

In March’s Q3 update, the company indicated that profit would be “towards the upper end” of the guidance range. Today’s comment only indicates a modest increase to this expectation.

However, it’s worth remembering that PZ Cussons’ original guidance for FY26 was for an adjusted operating profit of £48-53m. Based on today’s guidance, I estimate that FY26 adjusted operating profit is now likely to be around 13% higher than originally expected.

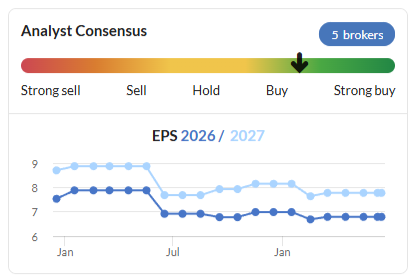

EPS forecasts are flat: unfortunately, it looks like this improved operating profit isn’t expected to drop through to earnings per share. Consensus EPS forecasts have remained largely unchanged over the last 12 months:

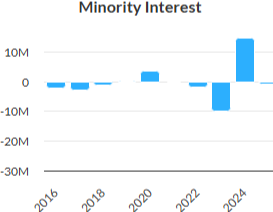

As I understand it, the reason for this is that a greater share of profits will be due to PZC’s non-controlling interests than last year. So-called minority interests are included in operating profit but are deducted from post-tax profit before calculating earnings per share.

Reflecting its complex and somewhat historic structure, PZC still has two subsidiaries where minority interests have a material shareholding. Both are listed in last year’s annual report as manufacturing businesses in Nigeria:

HPZ Limited (25.01% minority interest);

PZ Cussons Nigeria PLC (26.73% minority interest).

It looks like the improved profitability of the group’s Nigerian operations last year has translated into higher profits for these two manufacturing operations.

Even without researching this in detail, the StockReport shows us that profits due to minority interests can vary widely from year to year for PZ Cussons:

Last year saw minority interests take an unusually small proportion of profits. Recent forecasts from broker Singer Capital suggest their share of the group’s profits returned to a more normal level of c.£5m in FY26.

Outlook: there’s no new guidance for FY27 today, but the company has taken measures to manage expected cost pressures:

Looking ahead to FY27, the Group is mindful of the potential impact of the conflict in the Middle East and has already taken actions which are expected to offset a large majority of any cost inflation.

The minority interest issue makes it harder to model the impact of today’s revised operating profit guidance on earnings without some extra research. Unfortunately, I don’t have any access to updated broker notes today to short-cut this process.

What we do know is that consensus forecasts prior to today suggested adjusted earnings would fall slightly in FY26 (for the reasons discussed above) before returning to growth from FY27:

FY25 actual adj EPS: 7.34p

FY26E adj EPS: 6.8p

FY27E adj EPS: 7.8p

I would guess that full-year adjusted earnings may now be slightly above current consensus, but I don’t think the final result is likely to alter the broad shape of the earnings progression suggested above.

As Graham commented in March, recent share price gains for PZC appear to be out of proportion to the actual upgrades to guidance from the company.

Roland’s view

Of course, one possible reason for the strong share price performance is that investors are buying into a re-rating of the stock to reflect the recovery in sales and improved profitability.

PZ Cussons has been through a difficult period in Nigeria and elsewhere, but the balance sheet has now been repaired and the group’s performance does seem to have a new stability.

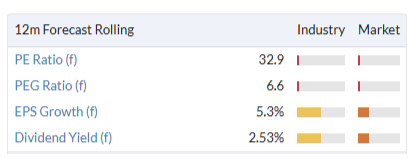

At 98p (at pixel time), I estimate the shares are trading on a FY27E P/E of 12.5x, with a possible 3.8% dividend yield. That’s still a fairly attractive valuation, in my view, especially as profit adjustments are expected to fall to minimal levels over the next couple of years.

However, given the level of change over the last year, I would like to see the FY26 accounts and updated FY27 guidance before getting too excited. As I discussed in my Stock Pitch, I believe this business still carries some risks relating to its geographic spread, (lack of) scale and product portfolio.

On balance I think it’s fair to maintain our previous moderately positive view today. AMBER/GREEN.

AO World (LON:AO.)

Down 2.7% at 93p (£532m) - Final Results for y/e 31 March 2026 - Roland - AMBER/GREEN =

Ed Sheldon covered AO’s full-year trading update in April, so we already knew that today’s results would be pretty strong.

Checking back through the archives, I’m relieved to see that I upgraded online electrical retailer AO World to AMBER/GREEN in November last year.

Although the shares haven’t actually performed especially well since then…

… the company’s performance has certainly improved, driving multiple broker upgrades ahead of today’s in line guidance:

When earnings expectations are rising but the share price is falling, there are generally two likely explanations:

the shares were too expensive to start with;

market mood swings have provided an opportunity to buy at a more attractive price.

I think that both factors may apply here, justifying a closer look at today’s figures.

FY26 results highlights

Revenue up 11.4% to £1,266.6m

Core B2C Retail revenue up 9.5% to £911.0m

Adjusted pre-tax profit up 16.1% to £50.5m

Reported pre-tax profit up 145% to £50.5m – no adjustments!

Adjusted earnings per share up 11.6% to 6.36p per share

Free cash flow up 152% to £66.4m

Net cash of £16.4m (FY25: net debt of £35.9m)

Shareholder returns: to reflect the group’s improved cash position, AO is planning to return £20m to shareholders:

Special dividend: £10m

Share buyback: £10m

With a market cap of c.£540m, this gives a dividend yield of 1.9%.

The share buyback also looks reasonably valued. Using the methodology followed by Next, I estimate this purchase could provide a 9.3% pre-tax return. That’s comfortably above the 8% threshold used by Next to decide on buybacks.

Profitability: when profits rise faster than sales we know that profitability has improved. That’s certainly the case here – margins doubled last year:

Operating margin: 3.9% (FY25: 1.9%)

Return on capital employed: 21.1% (FY25: 10.6%)

For a business in this sector, I think the FY26 figures are pretty respectable.

AO has a medium-term target for an adjusted pre-tax profit margin of 5%, so founder-CEO John Roberts presumably still believes there’s scope for further improvement.

Balance sheet & cash flow: AO moved to a net cash position last year, but this appears to have been driven by a build-up of cash on the balance sheet rather than any repayment of debt:

Cash & equivalents: £81.3m (FY25: £27.4m)

Gross borrowings: £1.7m (FY25: £1.9m)

There’s a good reason for the lack of debt, though – AO effectively carries debt in other forms:

Lease liabilities: £63.1m (FY25: £61.4m)

Payables (mainly supplier credit on stock): £238.2m (FY25: £212.9m)

Cash, inventories and receivables broadly offset AO’s trade payables, resulting in a very capital-light business model:

This type of business model can support strong cash generation and this is evident in today’s results.

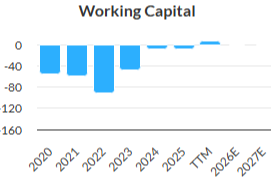

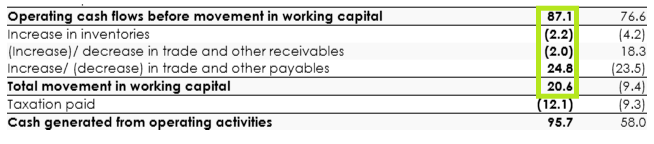

Last year’s free cash flow of c.£66m was significantly higher than the group’s net profit of £36m. The largest single factor responsible for this working capital inflow of £20.6m, reflecting an increased payable balance. This is effectively increased credit from suppliers:

I’d be concerned if there was any sign that AO was stretching out its payment terms, but that doesn’t seem to be the case – in fact the reverse seems to be true. My sums suggest AO took an average of 87 days to pay its suppliers last year, down from 93 days in FY25.

The increase in trade payables last year simply reflects increased sales volumes. Even so, it’s a nice example of how the company can generate cash from fast-moving stock before it has to pay its suppliers.

Trading commentary

AO became the first retail globally to exceed 1 million Trustpilot reviews last year, with an average rating of 4.9 out of 5. I’m not sure how significant this is, but if nothing else it’s a useful reminder that the UK is Trustpilot’s largest single market, accounting for around 40% of its revenue.

Getting back to AO, operational progress last year included a new phone offering, cost savings and improved performance from its musicMagpie used business:

Attracted over 720,000 new customers.

The performance of AO’s membership offering is said to have improved, but no figures are provided.

Switch24 launched: this is a service that provides a new phone every two years for AO members; a flagship offer from last year was a new iPhone 17 from £17 a month.

Finance partnership with NewDay continues to perform well; 13% of sales were made on finance last year.

Completed offshoring problem, moving inbound sales to South Africa.

Post-pay mobile business is now profitable, reflecting improved network terms.

Soft launch of AO Mobile; planning full launch in the first quarter of the current year. Management believes that combining this offer with the Switch24 product could attract strong customer demand.

AO’s core major domestic appliance (MDA) business gained 1% market share to 17.1%; the company is now experimenting with own-branded offerings.

musicMagpie has moved from being a c.£6m loss-making business to being profitable on a run-rate basis.

Outlook

CEO John Roberts warns that the external environment “remains uncertain” but remains confident the company can deliver FY27 pre-tax profit in line with current market expectations.

Thanks to an updated note from commissioned research house Equity Development, I can see that adjusted pre-tax profit is expected to rise by 5.9% to £53.5m in FY27.

EPS forecasts are also unchanged for each of the next two years, with slower growth expected this year and a more significant step up in FY28:

FY27E adj EPS: 6.5p (+3% vs FY26)

FY28E adj EPS: 7.6p (+13.8% vs FY27E)

These estimates put AO on a FY27E P/E of 14, falling to a P/E of 12x in FY28.

Roland’s view

AO shares have been rangebound for three years. I think it’s probably prudent for investors to remember the core attributes of this business; it’s a low-margin box shifter that operates in an intensely competitive market.

Having said that, this business is performing well and appears to be following a similar strategy to UK sector leader Currys. I would guess AO will reach a point where competitive pressures cap further (profitable) growth, but I don’t think the company is there yet.

Although I wouldn’t want to pay a high earnings multiple for this business, I’m inclined to think the current valuation is fair given the positive earnings momentum. I think the leadership of founder-CEO John Roberts – who has a 14.6% shareholding – is also a positive factor for outside investors.

On balance I’m going to leave our moderately-positive view unchanged today. AMBER/GREEN

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.