Bank of England: no change is expected to UK rates today, with the decision due at midday. Rates are expected to stay at 3.75% but it would be really surprising if everyone on the MPC agreed with this decision. Watch out for dissent on the 9-member committee.

For context, UK inflation numbers published yesterday gave an annual inflation rate at 2.8%, matching the prior month’s reading. While this is still higher than the 2% target, the figure was below market expectations (3%) and is the lowest level for over a year.

Federal Reserve: the US central bank published a decision yesterday, keeping rates unchanged as expected.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

It’s a similar story to the UK: inflation is too high, but there isn’t much appetite for rate hikes to address this. Indeed, US inflation is currently running at 4.2%, double their price target. But if temporary supply shocks are to blame, then the Fed can argue that rate hikes wouldn’t fix that underlying issue.

Overnight market movements:

The FTSE is set to open down 0.3% at 10,465

S&P 500 is up 0.8% at 7,475

Brent crude is down 2.2% at $77.50/bbl

Gold is up 1.2% at $4,305/oz

Bitcoin is down 0.8% at $63,950

Mark Simpson joins me today.

The Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Tesco (LON:TSCO) (£28.8bn | SR76) | LfL sales +1% (UK+1.8%). Outlook: Having made a good start to the year, we continue to expect Group adjusted operating profit of between £3.0bn and £3.3bn for FY 26/27 and free cash flow within our medium-term guidance range of £1.5bn to £2.0bn. | ||

Informa (LON:INF) (£10.6bn | SR60) | Underlying revenue growth of 6.4% in the five months to 31 May. Earnings guidance reaffirmed. “We remain committed to full year Group earnings guidance (double-digit underlying growth in adjusted EPS).” | ||

Whitbread (LON:WTB) (£4.02bn | SR29) | Total sales +2%. LfL accommodation +2%, LfL Food & Beverage down 1%. “In the UK, our forward booked position remains ahead of last year, supported by peak leisure bookings. Whilst visibility remains limited… we are confident that we can continue to outperform the wider M&E [midscale and economy] market.” | ||

Drax (LON:DRX) (£2.53bn | SR83) | The FCA has closed its investigation into the Company, which was announced on 28 August 2025, and no action will be taken. The FCA has confirmed that it has no concerns warranting further investigation. | ||

Firstgroup (LON:FGP) (£982m | SR71) | Adjusted revenue +25%. Adjusted operating profit £219.4m, marginally lower. Outlook: the Group expects to maintain Adjusted EPS in FY 2027, from a higher quality earnings base. | ||

Workspace (LON:WKP) (£670m | SR38) | Acknowledges the letter and presentation to shareholders issued by Saba. “The Board firmly believes in the strength of the Company's strategy… is carefully reviewing the Letter and Presentation.” | ||

XPS Pensions (LON:XPS) (£661m | SR43) | Revenue +13%. Revenue excluding McCloud +185. Adjusted EPS +7% (23.5p), Statutory EPS 13p. Outlook: “...confident of further growth in FY 2027 and beyond in line with the Board's expectations.” | ||

Costain (LON:COST) (£560m | SR94) | Costain selected by Norfolk County Council to design and build the new road infrastructure for the West Winch Housing scheme. | ||

Seeing Machines (LON:SEE) (£209m | SR23) | Significant expansion to an existing Automotive production program with a major European OEM. Estimated value of US$31m. | ||

Kistos Holdings (LON:KIST) (£195m | SR44) | Vår, in partnership with Kistos, has taken a final investment decision (FID) on the Balder Next project, which will deliver seven new production wells from the Jotun FPSO. 7 additional wells will deliver significant additional volumes at a b/e cost of approximately $30/boe. Will have increased gross production by an additional 11 mmboe to 86 mmboe. | ||

Eco (Atlantic) Oil & Gas (LON:ECO) (£164m | SR30) | “…multiple further value accretive workstreams remain underway across our portfolio of four diversified Atlantic Margin basins” | ||

Duke Capital (LON:DUKE) (£136m | SR72) | FY Cash revenue +7% to £28.6m. FCF +13% to £14.2m, Adj earnings -10% to £13.9m. Dividend held at 2.8p. £7.0m recurring cash revenue expected in Q1 FY27. “Looking ahead, the macroeconomic environment is likely to remain uncertain…The team's focus is on maintaining and creating value in our portfolio companies while navigating the macro headwinds.” | AMBER = (Graham) | |

Anpario (LON:ANP) (£104m | SR82) | “…has made a good start to the year with revenue and profit performance ahead of prior year and in line with full year analyst consensus expectations, despite well-reported geopolitical and related economic conditions.” Cash £10.9m (31 Dec: £12.4m) after £1.1m buyback. | ||

Ondine Biomedical (LON:OBI) (£81.4m | SR17) | Nasal Photodisinfection Reduces Surgical Infections in Complex Brain Surgery by 78.5% Compared to Nasal Antibiotics at Leeds Teaching Hospitals | ||

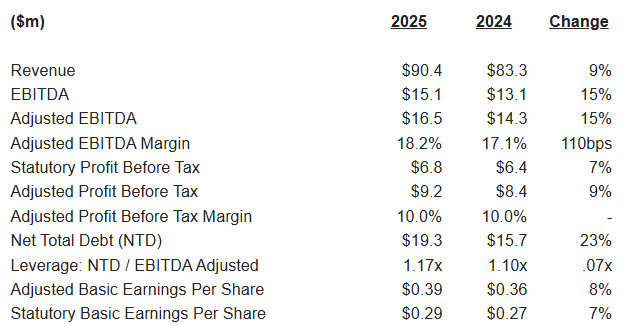

Water Intelligence (LON:WATR) (£41.6m | SR76) | Revenue +9% to $90.4m, Adj. EBITDA +15% to $16.5m, Adj. PBT +9% to $9.2m, Net Debt $19.3m (FY24:$15.7m). Q1 Revenue +9% to $23.2m. | AMBER/GREEN = (Mark) There is so much going on here that I struggle to come up with a cohesive view. These results look slightly ahead of brokers’ forecasts, but they don’t put to bed any of the concerns with the company; namely, a lack of operational gearing and the tendency for all the cash flow to go back out in re-acquiring their own franchises. If some commentators are right about the industry being fundamentally overtaken by technology, then this growth strategy will ultimately destroy shareholder value. However, big changes in industries tend to take much longer than we expect, and the valuation multiples are getting to the stage where the upside may well exceed the downside. As such, I keep our broadly positive view, at least until things come to a head, one way or another. | |

Time Out (LON:TMO) (£37.9m | SR17) | Signs franchise agreement to bring Time Out Market to South America. Will generate revenue through contractual franchise fees and ongoing payments, while not contributing capital towards the development of the Market. No figures given. | ||

tinyBuild (LON:TBLD) (£36.7m | SR41) | Sales are ahead of expectations for the first five months of the year. Strong pipeline, based on Steam wishlists. Net cash mid-single digit millions, reaching trough in summer 2026. “…remains on track to deliver results for 2026 at least in line with expectations.“ | ||

Synectics (LON:SNX) (£35.6m | SR90) | New orders from Stagecoach with an aggregate value of £1.5m, including £1.1m call-offs under Ocular's recently extended five-year framework agreement., for the supply and installation of Ocular's CCTV systems on 190 new electric buses. Majority of work expected to be completed between Q4 2026 and Q1 2027. | ||

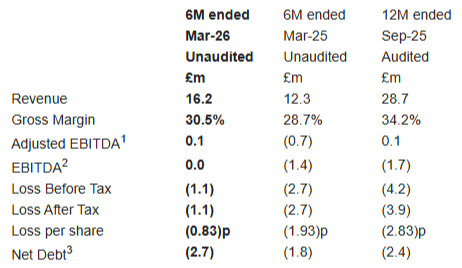

Tekmar (LON:TGP) (£23.5m | SR69) | H1 Revenue +31% to £16.2m, Adj. EBITDA £0.1m (25H1: LBITDA £0.7m). LBT £1.1m (25H1: £2.7m LBT). Order intake £29.5m (25H1: £10m). Net Debt £2.7m (25H1: £1.8m). | AMBER/RED ↓ (Mark) | |

Genedrive (LON:GDR) (£19.7m | SR15) | Genedrive MT-RNR1 ID kit for the prevention of Antibiotic Induced Hearing Loss in neonates is now a usual routine clinical service at Manchester University NHS Foundation Trust hospitals. | ||

Medpal AI (LON:MPAL) (£17.5m | SR0) | Launch of "Juno", its next-generation agentic AI health companion, alongside a full upgrade of the technology that powers it. | ||

Panther Metals (LON:PALM) (£12.3m | SR21) | £2.5m raised at 135p at a 3.5% discount, 21% dilution. |

Graham's Section

Duke Capital (LON:DUKE)

Up 2% at 27.2p (£139m) - Annual Financial Report - Graham - AMBER =

“Duke Capital Limited (AIM: DUKE), a leading provider of hybrid capital solutions for SME business owners in Europe and North America, is pleased to announce its audited results for the 12 months ended 31 March 2026…”

Duke provides a revenue-based “royalty” product for businesses. Investees make regular payments back to Duke - and these payments adjust higher or lower depending on revenue growth at the investee.

And although some of Duke’s investments can look risky at times, they haven’t yet suffered a major default.

These full-year results are solid:

Revenue +7% (£28.6m)

Recurring revenue +5% (£27.1m)

Profit after tax £11m (2025: £2m), “reflecting the reduction of non-cash fair value decreases across the investment portfolio”.

Q1 recurring revenue is expected at £7m, so the annualised figure continues to grow.

Chairman’s comments

These results demonstrate the income certainty and resilience created by Duke's disciplined approach to deploying capital into well-established, cash-generative businesses. Our focus over the period has been on backing existing investments, where we have strong relationships with the management teams, and we were pleased to make £21 million of follow-on investments into our portfolio of capital partners.

As Mark pointed out last year, there was a follow-on investment which seemed to be necessitated by the investee’s financial obligations - in other words, it was a bailout of a company that Duke had previously invested in. So we should treat follow-on investments carefully - and check in each case whether they are assisting real business growth, or merely papering over financial issues that the investee might be experiencing.

The Chairman also says that “access to flexible, long-term capital for SMEs has remained constrained as traditional lenders have maintained cautious credit appetites in the lower mid-market… businesses are actively seeking patient capital solutions that align with their long-term growth plans rather than traditional leverage-driven structures.”

I would also treat this statement carefully. Duke’s main product is a corporate mortgage in all but name. And it’s a mortgage that comes at a high cost with large, contractually-defined cash payments. I’m not sure that I would call it “patient capital” (compared to a straight-up equity investment) or inherently more attractive for a business than “traditional leverage-driven structures”.

For owners who want growth capital, who can’t access cheaper credit, and who also don’t want to give up too much equity, I can see the attraction.

Indeed, the fact that Duke is so happy to pick up equity stakes in its investees is ssomething that I still find surprising. A bank wouldn’t do that. This was one of the reasons I ended up selling my DUKE shares several years ago: they seemed to be moving further up the risk spectrum than I had anticipated, and further than I was comfortable with.

That said, the bulk of the portfolio is still in royalties. The investment portfolio today is described as containing £249m of “hybrid credit investments” (i.e. royalty investments) and only £14m of equity investments. Their borrowings to fund all of this are close to £100m. Net assets are officially £175m.

Outlook by the CEO: some important paragraphs here.

…we are pragmatic about the year ahead. Although we saw three rate cuts during FY26, the outlook no longer favours further easing, and persistent inflation and geopolitical headwinds are likely to keep rates higher for longer. These same pressures make growth in the portfolio a lower-probability outcome in the near term, and we are planning accordingly rather than assuming a more favourable environment.

The outlook for the portfolio in the coming financial year has both encouraging and challenging aspects. On the one hand, we have current visibility over two capital partners who are currently going through a formal M&A process with Tier 1 investment banks to sell their business and thereby exit Duke, both of which could occur in the current financial year.

On the other hand, two partner companies most affected by the economic challenges are going through restructuring in parts of their group, which tests the strength of our portfolio and its ability to weather adversity. We will of course keep shareholders informed on a real time basis on all these processes, as they develop.

Graham’s view

Although Duke is trading at a 20% discount to its official balance sheet value, there are a few good reasons for this.

Duke itself is leveraged up, increasing the risk profile for a portfolio of high-yield investments.

Interest rates staying higher for longer keeps a lid on the value of the portfolio.

The specific news that two of the 14 partners are going through restructuring is a warning - could losses from that part of the portfolio exceed profits from the disposals being worked on in other parts of the portfolio? It remains to be seen.

Long-term, I believe that Duke itself would like to raise more equity capital, which is something to consider if the Duke share price recovers to NAV or higher.

For these reasons, I think an AMBER stance from us remains reasonable. For investors who only want yield and who don’t care about capital appreciation, it could be worth looking into. The yield now is c. 10%.

Mark's Section

Tekmar (LON:TGP)

Down 10% at 15.2p (£23.5m) - Unaudited Interim Results - Mark - AMBER/RED ↓

Tekmar has had a rather chequered past:

I’ve followed this company for a long time as the story appeared compelling. Amongst other things, they provided cable protection systems for offshore wind farms. This was a business where Tekmar had considerable market share and was forecast to grow 15% CAGR for a decade from 2019. It would seem in such a scenario it would be hard for Tekmar not to be a success. Yet they managed it.

The downfall:

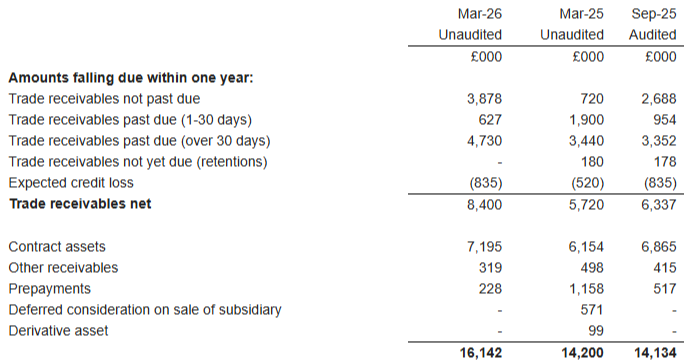

Project delays in 2020 began impacting margins which led to the founder-CEO stepping down. One of the signs that there may be deeper problems was a huge jump in receivables, mainly contract assets:

These are usually unbilled revenue, showing that the company was booking revenue that had not yet been invoiced. There is nothing wrong with this practice per se, but these are inherently lower quality and it was one of the warning signs that meant I steered clear of the company.

Receivables continued to rise even as revenue declined, and eventually the company had to take write-downs within their Chinese subsidiary. They also had a warranty issue with a major customer, and while Tekmar denied that their product was to blame, the risk weighed heavily on sentiment.

The rescue:

By mid-2022, compounding losses forced the board to launch a Formal Sale Process to find an external strategic partner to rescue the balance sheet, admitting that the company required emergency capital to support growth.

A £7.3m subscription by SCF Partners plus up to £18m of Convertible Loan Notes, a £2m placing and £1m retail offer rebuilt the balance sheet, but at the cost of significant dilution. The company now has roughly 140m shares in issue up from around 50m.

Today’s results confirm that the loan note was never drawn and has expired since they managed to secure a £4 million UK Export Finance-backed Barclays facility, a £2 million British Business Bank Growth Guarantee Scheme loan, and raising cash through the £2.84 million disposal of its Innovation House premises.

The present:

Tekmar’s survival is good news as it seems the UK taxpayer would have been on the hook for some of the losses. The company finally managed to access sufficient other facilities to repay its CBILS loan in October 2025, more than 5 years after it took this out as a short term loan to get it through the COVID period. However, today’s results show that they are not completely out of the woods:

Net debt is rising, and the company continues to be loss-making. Given that SCF Partners still own 31%, I would expect them to still be supportive if further equity capital was required. After all, they were happy to offer loan notes.

The concern:

Given the background above, I hope readers will forgive me, that the next place I naturally turn to in these results is the note to the accounts that details the receivables:

So again we have a not insignificant amount of contract assets, and trade receivables more than 30-days past due are both significant and rising. It is hard not to get the feeling of deja vu.

The future:

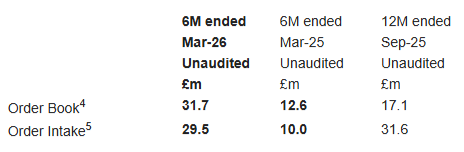

The good news, and the reason that the share price has almost trebled since December last year, is a series of contract wins that have been announced since then and have led to a jump in order book:

Revenue for these will be recognised across FY26 and FY27. However, with their broker Cavendish forecasting £22.4m of revenue for 26H2 and a big jump to £52.6m of revenue for FY27, the much-improved order book only just covers H2 and the first two months of FY27.

Cavendish suggests they will deliver 1.5p of Adj. EPS in FY27 and 2.7p in FY28, which would make them look pretty cheap. However, with a gross margin that remains around 30% (and therefore suggests that they are delivering mostly a commodity product) they absolutely have to deliver the big jump in revenue figures to be able to hit those forecasts.

Mark’s view

Perhaps I am jaded by the company’s long-term history, and this really is turning a corner under a new management. Recent contract wins and the jump in order book means that the future looks better than the recent past. However, there is still a huge amount of work left to do to meet broker forecasts for FY26 let alone FY27 and beyond. The low gross margin suggests that their product does not have a huge technical advantage over competitors and issues such as pricing and availability may have a bigger impact on sales than technical prowess.

I still have doubts that they will meet these challenging revenue forecasts, and even if they do, questions remain as to whether they will be paid on time, or at all, for the revenue they book.

I expect their major backer to be supportive if further equity is required, and the banks will be sanguine as the debt appears to be largely underwritten by the UK taxpayer. However, there is no escaping that this was a loss-making half where net debt rose.

In December, following the second contract win I maintained our neutral view. However, with the share price now materially higher, the Stock Ranks starting to decline, and the benefit of seeing these half-year results I think we should take a slightly more negative stance. AMBER/RED

Water Intelligence (LON:WATR)

Up 2% at 252p (£41.6m) - Audited Results for Year - Mark - AMBER/GREEN =

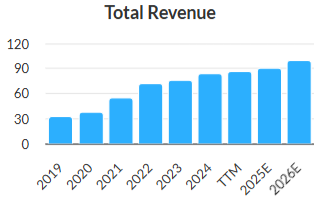

I continue to be fascinated by Water Intelligence. On the surface, this is one of the cheapest growth companies on the market, with revenue having growth 20% CAGR for the last five years:

There is a lack of operational gearing, but still, if 2026 forecasts are to be believed, EPS will have almost grown 4x since 2019. Few companies can boast this sort of performance.

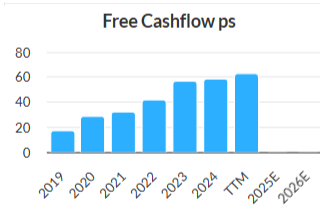

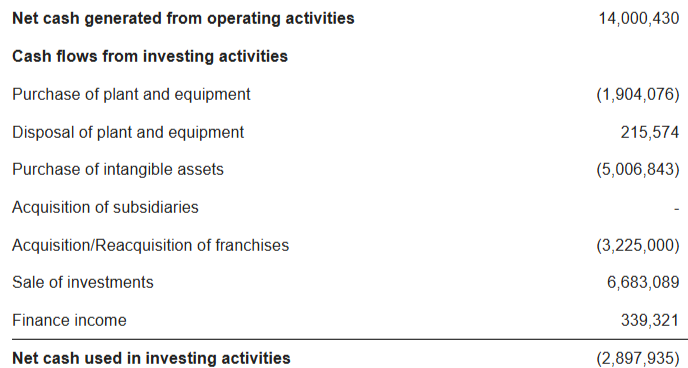

Cash flow:

However, I remain sceptical. Despite strongly growing Free Cash Flow,

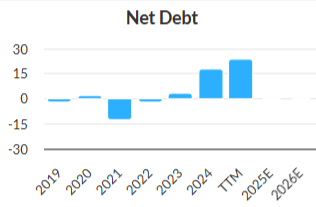

Net debt is rising:

Today’s 2025 FY results show a similar pattern:

Revenue grows, statutory and adjusted profitability measures are up, but without any operational gearing. Adj. EPS at 39c looks like a small beat on the 36c in the StockReport, and Canaccord Genuity calculate this as 38c on a diluted basis confirming this was slightly ahead of forecast. However, net debt is also up.

It is also worth noting that it is getting quite late to be reporting results for the year to 31st December, and we are approaching the 6 months cut-off at which point AIM companies would be suspended. They clearly got them over the line in time, but the time taken shows the complexity of the business.

This is no doubt not helped because the company has a habit of both selling and buying back franchises:

Forecasts:

Canaccord don’t upgrade future forecasts, but they do introduce a FY27 number showing further progression, saying:

We make no changes to FY26 estimates and introduce FY27. These assume doubledigit adj. PBT/EPS growth in both years, supported by commercial progress, modest margin expansion and no further M&A. This suggests potential upside if the preventative maintenance model can quickly scale and/or ALD franchises are reacquired. Leverage falls to 0.7x by year-end FY27E, providing headroom to capitalise on growth opportunities.

However, that growth opportunity appears to largely be the acquisition of more of their own franchises, with CG saying:

M&A optionality: Three acquisitions in FY25 for $4.6m added $3m revenue and $0.9m profit in-year. The franchise reacquisition pipeline remains deep with $92m of gross sales still in third-party hands after a $0.2m deal was completed in March.

Strategy:

The company points out that this strategy gives them the best of both worlds. Getting start-up growth for little cost and then bringing the successful ones back under the fold. However, we only have the company’s word that these transactions make financial sense.

Given the time to report FY results they also mention Q1 trading. But the update here is less detailed than the actual Q1 trading update released last month. Although Q1 is ahead of the growth rate of the previous year, it is slightly behind the 10% full year growth in revenue forecast by their broker. Adjusted EBITDA was up by a similar amount to revenue, showing the same lack of operational gearing and net debt is up a bit more.

These trends are that far off trend that the FY results don’t look achievable, which would mean that company trades on a P/E of 7.8, falling to 7.0x for FY27. This would appear to be too cheap.

However, I can’t help feeling that shareholders would like a good chunk of that cash that ends up going to re-acquire franchises being returned as a dividend instead. The market is clearly sceptical about the strategy, and until it results in clear shareholder returns, I don’t see that changing.

Existential threat?

Overall, I’m not sure these results quell the debate that rages in my mind over whether Water Intelligence is a great opportunity, or a company pursuing growth at any cost to the detriment of overall shareholder value.

Adding to the confusion is a brilliant substack article written last year that argues that the company is at a fundamental crossroads. The article is well worth reading in full, but the final paragraphs say:

For investors, the question isn't whether they're right about water infrastructure needs (they are) or whether they execute well (they do). It's whether being right and executing well matters when the game itself is changing.

They've spent fifty years perfecting the science of detection. But no amount of acoustic equipment can hear the sound of your industry evaporating.

If the author is right about where the industry is going, repurchasing franchises, even if done selectively and at a good price, will destroy shareholder value.

Mark’s view

There is so much going on here, both within the company and industry, that I struggle to come up with a cohesive view that captures it all. The temptation is to cop out and go for a neutral view. However, the valuation appears to be getting to the level where the upside perhaps out-weighs the downside. With a StockRank of 76, I think it makes sense to be broadly positive, but I can see why many will simply avoid this kind of complex situation. AMBER/GREEN

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.