Gold price: Gold is back below $4,000, erasing the gains made since c. November 2025. It’s still up by nearly 20% over the past 12 months. But maybe the blow-off top is behind us now? Especially with the potential for the Fed and other central banks to raise rates, rather than lower them.

Bitcoin: in a similar vein, digital gold is below $60,000 and has now fallen by more than 50% from its peak.

Anki: seeing as the overnight news isn’t too exciting, I thought I’d ask if anyone here has used Anki before? I just downloaded it last night, and started working on Ultimate Geography. The “spaced repetition” learning technique has worked really well for me in the past, and I’m tired of not knowing the answers to simple geography questions - wish me luck!

Overnight market movements:

The FTSE is up 0.2% at 10,520

S&P 500 is up 0.2% at 7,450

Brent crude (September) is down 0.9% at $73.25/bbl

Gold is down 0.8% at $3,985/oz

Bitcoin is down 1.1% at $59,600

Wrapping it up there, thanks everyone! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

J Sainsbury (LON:SBRY) (£7.1bn | SR35) | Like-for-like sales exc. fuel +2.1% in Q1. “...we continue to expect to deliver Total underlying operating profit of between £975 million and £1,075 million and Retail free cash flow of more than £500 million.” | AMBER = (Roland) [no section below] Today’s update is in line with revised guidance from April, when Sainsbury’s warned on profits. I don’t think today’s Q1 update highlights any new problems, but LFL sales (ex-fuel) of 2.1% highlight how difficult it is to keep sales growth ahead of inflation at the moment. With the stock on a forward P/E of 13 and a yield of 4.6%, I think the share price is up with events. After all, this remains a low-growth, low-margin business that generates single digit returns on equity. The recent sharp decline in Sainsbury’s StockRank shows the algorithms taking a similarly neutral view. | |

International Workplace (LON:IWG) (£1.76bn | SR34) | Increase to the share buyback of $50m, taking the programme up to $150m. | ||

Grafton (LON:GFTU) (£1.70bn | SR94) | Further share buyback programme for up to £25.0m. | ||

Saga (LON:SAGA) (£879m | SR53) | SP +7% Traded in line with expectations for the first four months of the year and remains on track to deliver its full year guidance. Net debt falls to £465m as of May 2026. | AMBER = (Graham) Meeting full year guidance should result in adjusted EPS of about 36.3p this year (FY January 2027). The note from Singers issued in April suggested that EPS would rise to 42.2p next year (FY Jan 2028) and then 55.8p the year after that. I've quickly reviewed the January 2026 balance sheet (nearly £1.3 billion of total assets) and while it does have a negative tangible net worth, the liabilities are now overwhelmingly in the form of Ocean Cruise loans (£600m+) provided by the largest shareholder, Chairman, and son of the founder, Sir Roger de Haan. There has been a fabulous turnaround in the perception of this stock and rightly so, as it has addressed its debt problem and achieved a leverage ratio of only 3.2x. But I think a neutral stance from us continues to make sense for us, given that the earnings multiple out to FY 2029 is over 10x. | |

Intuitive Investments (LON:IIG) (£725m | SR71) | Recommended offer from Acceler8 Ventures (LON:AC8). IIG shareholders will receive 2.6797 new AC8 shares for each IIG share. Based on yesterday’s AC8 closing price of 80p, this values IIG at £600m. | TAKEOVER (AMBER) (Graham) | |

Rockhopper Exploration (LON:RKH) (£602m | SR27) | Rockhopper and the buyer (Zodiac Energy) now both have the option to withdraw, as the long stop date has been reached. Both sides continue to try to satisfy the demands of the Italian regulator. | ||

Guardian Metal Resources (LON:GMET) (£429m | SR27) | Results indicate that the Project is planned to produce 15,916 tonnes of WO3 over an 8-year mine life, generating after-tax free cash flow of US$1.058 billion, with a capital payback period of 1 year from first commercial production. This translates to a net present value of US$660.3m. | ||

Chrysalis Investments (LON:CHRY) (£367m | SR64) | NAV per share falls 22% in six months to 133.94p. “The decline in NAV per share over the period largely reflects the de-rating of comparable peer groups amid significant equity market volatility, rather than the operational progress of our portfolio companies.” | ||

Mears (LON:MER) (£341m | SR97) | Has continued to trade well. New orders with local government of £1.5bn. Expects to report results for the full year in line with market expectations. | ||

Kore Potash (LON:KP2) (£175m | SR19) | On 8 June 2026, the Company was approached by a new party wishing to participate in the FSP. Two parties are currently engaged in the FSP. | ||

KEFI Gold and Copper (LON:KEFI) (£145m | SR15) | Tulu Kapi development is on schedule, now entering month four of its 27-month development programme, with first gold production targeted for mid-2028. AGM seeks shareholder approval to increase borrowing capacity, a condition precedent for Tulu Kapi debt drawdown and helping minimise future equity dilution. | ||

Mercia Asset Management (LON:MERC) (£121m | SR52) | Revenue falls 3% to £34.1m. Operating loss £8.9m after £12.8m unrealised fair value loss in direct investments. EBITDA £8.1m (FY25: £7.6m). “We have entered FY27 with pragmatic confidence in our path forward and the environment we are navigating.” | GREEN = (Graham - I hold) It’s a little contrarian of me, and I am talking my own book, but I’m staying GREEN on Mercia. I don’t think the investment thesis has been disproven yet. They are still seeking to sell their direct portfolio soon (albeit on a slightly extended timeline), and they should still get a very large cash inflow relative to their market cap, even after the writedowns we’ve just seen in FY26. Meanwhile, the fund management business continues to grow at a nice pace. The StockRank is only 52 and the share price has refused to agree with me so far, but I see a lot of value here, so I’m staying positive! | |

Smarter Web (LON:SWC) (£96m | SR18) (I think this market cap is correct, based on the latest share count) | Interim Results & Interim Results Commentary and Quarterly Update | Revenue £400k. Operating loss £2.7m. Other gains and losses: loss of £69m. Held £220m of crypto at the beginning of H1. By the end of H1, its value had fallen to £157m despite the company adding £8m to it. “Bitcoin is a volatile asset… periods of challenging price action are a feature of its history rather than an exception to it.” | AMBER/RED = (Graham) I stopped being fully negative on this in February. It was no longer ludicrously overvalued, and (a very much related point) it had stopped issuing shares so rapidly. The share count is now 372 million, not too far above the 350 million figure I had in February. So share issuance does appear to have slowed down. Today's balance sheet (for April 2026) shows crypto holdings of £157m. The bitcoin price in sterling has however fallen by 20% since then, so let's write down their balance sheet by £31m. That gives an adjusted balance sheet value of just over £100m (down from £135m). At a market cap of £96m, I can therefore stay AMBER/RED on this: it's not ludicrously overvalued, and might not be a terrible way to invest in bitcoin. I'm still a little negative on it, as I do suspect there are better ways to get pure crypto exposure, with fewer costs, than with these "Bitcoin Treasury" companies. |

Macfarlane (LON:MACF) (£106m | SR66) | The 1974 scheme is de-risked by the purchase of a £53m bulk annuity from Royal London. All financial and demographic risks relating to the Scheme's liabilities will be fully insured. The scheme is in surplus with no cash contributions required. | ||

Cake Box Holdings (LON:CBOX) (£84m | SR46) | Revenue +39.5%. Like-for-like sales growth 4.8%. 37 new stores (25 Cake Box, 12 Ambala). Trading in 2027 has started positively and ahead of 2026. | AMBER/GREEN = (Roland) Today’s results are largely in line and the forecasts for FY27 have also been left unchanged by the company’s broker today, suggesting another year of double-digit growth may lie ahead. While the business faces evident cost pressures and the risk of over-expansion, Cake Box’s franchise model is generating attractive returns on capital and strong cash flows. The balance sheet looks fine and the forecast dividend yield of 6% seems supportable. This stock is on my watch list and I think it’s fair to maintain a broadly positive view today. | |

Ondine Biomedical (LON:OBI) (£83m | SR17) | Published Leeds study shows Steriwave® reduced surgical site infections by 78% versus standard of care using Mupirocin in High Risk Endoscopic Endonasal Skull-Base Surgery. | ||

Venture Life (LON:VLG) (£81m | SR64) | Revenue +16% on a pro forma basis with Power Brands +21% to £13.4m. “Revenue and Adjusted EBITDA in line with management expectations.” | ||

Zoyo (LON:ZOYO) (£71m | SR43) | H1 after-tax loss of £444k, cash of £2.4m at 31 March 2026. | ||

Zephyr Energy (LON:ZPHR) (£69m | SR33) | Revenue -43% to $13.9m, gross profit -65% to $2.6m. Net loss of $10.8m. Continuing to develop a non-operated portfolio in the Rockies while developing the Paradox project in Utah. | ||

Gemfields (LON:GEM) (£67m | SR31) | Sean Gilbertson will step down as CEO by mutual agreement with the Board on 15 July. He is thanked. CFO David Lovett has been appointed interim CEO alongside his existing role. | ||

Helix Exploration (LON:HEX) (£57m | SR10) | H1 net loss of £774k, cash of £1.8m at 31 March 26. Commenced helium production at Rudyard in February and secured spot supply arrangement in May 2026 with an industrial gases group, establishing a route to sales. | ||

Made Tech (LON:MTEC) (£57m | SR69) | Revenue +27%, adj EBITDA +69% to £5.9m. Net cash of £14.5m at 31 May 26. “FY26 expected to be ahead of recently upgraded market expectations.” | GREEN = (Roland) Today’s upgrade to FY26 guidance also highlights the positive operating leverage in this business – margins appear to be rising as revenue grows. With current FY27 forecasts suggesting c.30% EPS growth over the coming year, the current valuation looks reasonable to me. I don’t see any reason to change our positive view based on today’s news. | |

Chariot (LON:CHAR) (£45m | SR20) | Net profit of $475k following disposal gain. Year-end cash of $413k. Post-period end, raised $24.3m through a placing in March. Continues to pursue interests in various renewable and oil projects. | Publishing results right on the six-month deadline. | |

Gelion (LON:GELN) (£39m | SR3) | Directorate change & US market entry and Investor Presentation | John Wood retires as CEO with immediate effect and is replaced by Matthew Wood, who was previously at Cabot (NYQ:CBT). Gelion also announces a new collaboration agreement with the US DOE National Laboratory of the Rockies. | |

Zenith Energy (LON:ZEN) (£32m | SR23) | Construction of the first solar project in Puglia has started. The remaining two plants in the 7MWp under construction portfolio are expected to enter construction in July and August 2026. | ||

Palace Capital (LON:PCA) (£32m | SR34) | Launching share buyback of up to 3,633,880 shares, in line with its remaining authority from the 2025 AGM. Buyback is expected to increase the shareholding of the concert party from 29.88% to 36.71%. | ||

Kendrick Resources (LON:KEN) (£26m | SR15) | Previously unanalysed core from TKDD001 returned excellent individual pXRF values, as did TKDD002. TKDD003 confirmed “excellent continuity of mineralisation”. | ||

Neo Energy Metals (LON:NEO) (£24m | SR23) | £2.5m raised in January 2026, board restructured, mining rights transfer at New Beisa “on track”, timeline extended to Dec 2026. | ||

Wynnstay Properties (LON:WSP) (£23m | SR56) | Company shares statement from 11.9% shareholder Gareth J. Gibson and notes its disagreement with a number of Gibson’s proposed AGM resolutions. | ||

Metals One (LON:MET1) (£18m | SR8) | Lions Bay Capital to acquire 100% of Lions Bay Resources, including Metals One's 30% shareholding and option to acquire a further 19.99%, in an all-stock transaction. MET1 will receive between 30m and 72m Lions Bay shares, depending on option uptake. All consideration shares are expected to be issued at C$0.35 per Lions Bay share. | ||

Zinc Media (LON:ZIN) (£18m | SR30) | Raw Cut has achieved its FY25 earn-out target. Payment of £0.35m is due to vendors, to be paid through the issue of 661,625 new shares (52.9p per share). | ||

Team (LON:TEAM) (£18m | SR10) | Revenue +19%, pre-tax loss of £1.84m. Loss per share of 2.9p. Cash increased to £3.8m following acquisition of WH Ireland Group for £12.7m. Pro forma AUMA of £2.3bn following recent acquisition of investment mandates from EPIC Markets. | ||

Energypathways (LON:EPP) (£18m | SR11) | Net loss of £1.7m (2024: £1.2m). Cash of £1.1m at year end. Post period end received Gas Storage Licence GS009 and signed a £15m financing agreement. Submitted proposed MESH gas storage development to DESNZ. | Publishing results right on the six-month deadline. | |

Mycelx Technologies (LON:MYX) (£16m | SR51) | Chair steps down from 31st July 2026. | ||

Reabold Resources (LON:RBD) (£12m | SR56) | Net loss of £7.8m, with overheads up from £2m to £2.7m and a £4m impairment relating to the investment in Danube. Cash of £2.1m at 31 Dec, £4.2m raised post-period in April 2026. | ||

Rua Life Sciences (LON:RUA) (£11m | SR41) | Revenue up 6% to £2,747k, with gross margin of 74.9% and adj EBITDA of £76k. After-tax loss of £183k (H1 25: £641k). |

Graham's Section

Mercia Asset Management (LON:MERC)

Down 5% at 27.3p (£115m) - Preliminary Results - Graham - GREEN =

(At the time of writing, Graham has a long position in MERC.)

Mercia Asset Management PLC (AIM: MERC), the proactive, regionally focused private capital asset manager with c.£2.2billion of assets under management ("AuM") today, is pleased to announce its preliminary results for the year ended 31 March 2026.

I’m invested here because of a) the strength of the balance sheet, including Mercia’s own investment portfolio; and b) the growing fund management business which I believe has a defensible niche in regional investing.

But I must acknowledge that these full-year results aren’t so great, in terms of the headline numbers:

Revenue falls from £35.2m to £34.1m

Operating loss £8.9m

Cash falls from £40m to £26m

Net assets fall from £188m to £174m (rounded numbers).

So far, so bad.

The “alternative performance measures” are as follows:

Total AUM is virtually unchanged at £1,997m (includes Mercia’s portfolio and third-party funds under management)..

EBITDA improves from £7.6m to £8.1m.

EBITDA is measuring the profitability of the fund management business, so at least that moved in the right direction.

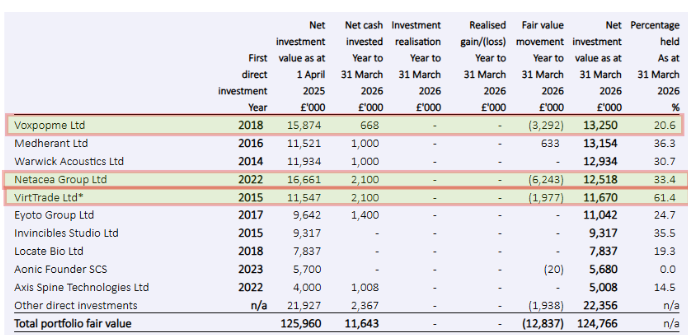

Direct investment portfolio

What has really dragged down the results is a nearly £13m loss in the fair value of Mercia’s own direct investments. This is included in the operating loss.

This direct investment portfolio, along with its movements during the year, are laid out very clearly in this table. I’ve highlighted the biggest losers:

- Voxpopme (£3.3m fair value loss): this is a consumer intelligence platform or “AI research agent that helps you understand customer truth”.

- Netacea (£6.2m fair value loss): bot management software for enterprises, preventing attacks on businesses.

- VirtTrade (£2m fair value loss): digital trading card company.

If I was to put a positive spin on these losses, I could note that none of the fair value losses imply that the investments are now worthless: it’s just a question of the current value.

A more negative spin on it would point out that Mercia found itself pouring more money into each of these three underperforming investments - would they have depreciated even faster without those cash infusions?

Mercia themselves say that the fair value loss “largely reflects market sentiment arising from geopolitical instability and the rapid development of AI, which in turn have reduced market confidence and risk appetite, impacting market valuation comparables.”

It’s true that 31st March - the year-end date - was not the best time to measure the value of this portfolio. The NASDAQ composite index is up by 20% since then. Even if I personally think that the NASDAQ is overvalued, it’s fair to say that comparables might have already improved since that valuation date.

And I should emphasise a crucial point: this portfolio is up for sale. Mercia are not rushing to sell these investments, but they are not intending to hold them forever. This paragraph is worth quoting extensively:

…whilst the underlying technical and commercial progress of the direct investment portfolio has been largely unaffected by external events, comparable market valuations and acquiror behaviour have both been influenced, with the result that expected exit timelines have lengthened. We remain committed to a full portfolio exit within the stated three-to-five-year window but now expect the majority of realisations to fall between FY28 and FY29. This is a frustrating but realistic re-calibration to reflect current market conditions. The Board is however also considering other alternative options for the divestiture of the direct investment portfolio.

Whenever these investments are sold, this will create a (hopefully) very significant cash inflow for Mercia, relative to its market cap. The portfolio is now valued at £125m which is actually higher than Mercia’s own market cap.

Of course, there is a good chance that it won’t be possible to sell all of these positions by FY29, nor to sell them at their official valuations. My hope is merely that they will be able to sell most of them at close to their official valuations. If they do that, then they should receive something close to their market cap in cash.

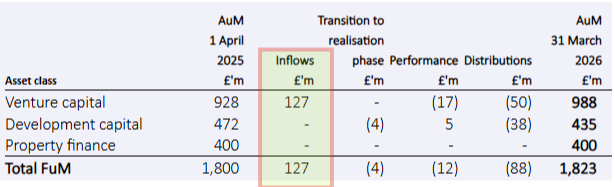

Fund management: besides the direct portfolio, there is also the fund management business which continues to enjoy nice inflows and zero outflows (largely due to the structure of VCTs and other fund types they manage).

While the “AUM” figure quoted above includes both Mercia’s direct portfolio and third-party funds under management, it’s the third-party funds under management which interest me the most. These increased by 1.3% in FY26, to £1,823m.

Inflows were offset by some distributions:

This might not seem like very impressive growth but we are also told that third-party FUM has grown to £2.05 billion since year-end, as additional funds were raised just after year-end. So overall, I think this is decent progress.

The combination of gradually increasing FUM and controlled expenses is what created the modest increase in EBITDA for the year.

Dividends and buybacks: the total dividend for the year is 1p which, if it continues, creates a useful yield at this share price (over 3.5%). There was also a £3m buyback which helps to keep the share count under control - the shares purchased were cancelled.

Graham’s view

It’s a little contrarian of me, and I am talking my own book, but I’m staying GREEN on Mercia.

I don’t think the investment thesis has been disproven yet. They are still seeking to sell their direct portfolio soon (albeit on a slightly extended timeline), and they should still get a very large cash inflow relative to their market cap, even after the writedowns we’ve just seen in FY26.

Meanwhile, the fund management business continues to grow at a nice pace.

The StockRank is only 52 and the share price has refused to agree with me so far, but I see a lot of value here, so I’m staying positive!

Intuitive Investments (LON:IIG)

Up 6% at 320p (£768m) - Recommended Offer for Intuitive Investments Group - Graham - AMBER

I think I can see what’s happening here, and it’s not what the headline sounds like.

Firstly, it’s an all-share offer. So Intuitive Investments (LON:IIG) and Acceler8 Ventures (LON:AC8) will become one company.

AC8 has zero revenues and a market cap of £2m, i.e. it’s just a shell. Under listing rules, it has to complete an acquisition by July 2027, or else shut down.

IIG, meanwhile, has been looking to get off the Specialist Fund Segment and onto the Official List of trading companies.

IIG was in theory a fund, but its principal investment (Hui10) “represents substantially all of the Company’s investment portfolio”. It makes more sense to think of IIG as the holding company for Hui10, not as a fund. And so it makes sense that IIG would want to get off the Fund Segment of the LSE, and onto the Official List.

This creates a natural solution: AC8 “buys” IIG, bringing Hui10 onto the official list. But as it’s a reverse takeover, existing IIG shareholders get to continue owning the vast majority of Hui10.

Share counts / valuation

AC8 has 7.5 million shares when fully diluted.

IIG, on the other hand, has 239 million shares outstanding, or 280 million fully diluted.

Under the terms of the Acquisition, the Scheme Shareholders shall be entitled to receive:

2.6797 New AC8 Shares for each IIG Share held (the "Exchange Ratio)

This means that IIG shareholders will end up with 750 million AC8 shares.

With only 7.5 million AC8 shares (fully diluted) currently in existence, this means IIG will end up owning 99% of the combined entity.

What might surprise IIG investors is that the exchange ratio only values IIG at £600m. This might seem to be a lowball valuation, given that IIG is worth over £750m.

However, I don’t believe that this valuation is particularly relevant. The only practical effect it has is on the percentage ownership that existing IIG shareholders will get to enjoy after the merger. And that percentage ownership is 99%.

IIG shareholders are being asked to give away 1% of their company, in order to get off the Specialist Funds Segment and onto the Official List.

That doesn’t sound like an exorbitant price to pay, as being on the SFS is a little restrictive in terms of accounting and in terms of the types of funds that can buy into you.

The £600m number, meanwhile, has little or no practical relevance. It does mean that AC8 are getting a very nice deal: they will get ownership of 1% of Hui10, which could be worth a lot more than their current £2m market cap. But I'm not going to muck about with shares in a £2m market cap company - I presume there is zero liquidity.

Graham’s view

I think this is a win-win for both sides.

From IIG’s perspective, it’s a small benefit to get onto the Official List but it doesn’t ultimately change much: everything depends on the performance ofHui10. For some background:

Hui10 is a technology company involved in the digital transformation of the Chinese lottery. Its paperless lottery play platform unlocks the market expansion of the Chinese lottery aiming to increase the number of people playing the lottery from the current 10% participation level to a target of more than 30%. Lucky World is Hui10’s omnichannel commerce platform which provides China's existing 200,000 lottery only shops access to a wider fastmoving consumer goods product offering through its growing number of commercial partnerships with leading Chinese suppliers.

It does sound pretty exciting, but at the same time I don’t think we’ve been given much information on Hui10’s key financial numbers. We are told how many lottery shops they’re connected to, their registered users, and transaction value, but not revenues and profits.

Checking a note from Progressive Research that was issued last year, I see a profit forecast for 2026 of minus RMB 248 million, improving to RMB 1,555m next year and RMB 6,179 million in 2028. You get about 11p for one RMB currently.

I have no way of telling if these forecasts are realistic. They do sound intriguing. At this stage, I’m just going to be neutral on IIG.

Well done to anyone who has held it while it has multi-bagged:

Roland's Section

Made Tech (LON:MTEC)

Up 5% at 41p (£61m) - FY26 Full Year Trading Update - Roland - GREEN =

We’ve been positive on this digital services provider to the UK public sector in recent months thanks to a reasonable valuation and a succession of upgrades:

Our faith has been rewarded today with a further upgrade to FY26 guidance:

FY26 revenue up 27% to £58.9m (+2.4% vs consensus of £57.5m)

Adjusted EBITDA up 69% to £5.9m (+5.4% vs consensus of £5.6m)

Year-end net cash (31 May) of £14.5m (+7.4% vs consensus of £13.5m)

Management commentary on trading is also positive:

Sales Bookings momentum: includes a recent £19m contract with the UK Government Digital Service and “a healthy Contracted Backlog”, giving good revenue coverage for FY27 and beyond.

Remains well positioned to benefit from UK Government Spending Review,

AI “is creating new product & growth opportunities”.

CEO Rory MacDonald is Made Tech’s largest shareholder, at 28%. He sounds confident:

The UK public sector is entering a multi-decade AI transformation, creating a substantial long-term opportunity for trusted delivery partners like Made Tech. Recent contract awards reinforce our position at the centre of a number of critical programmes across government.

Outlook & broker estimates

Made Tech will release its FY26 results in September and will provide an update on current trading at that time [… ] we look forward to FY27 with confidence.

House broker Canaccord Genuity has left both its FY26 and FY27 forecasts unchanged today, despite the upgrade to the company’s FY26 guidance.

Crunching the numbers myself, my feeling is that any increase to FY26 EPS forecast of 2.2p from today’s upgrade is only likely to be quite modest.

FY27 - Canaccord has also left FY27 estimates unchanged ahead of September’s updated guidance:

Revenue: £60.6m

Adj EBITDA: £6.0m )

FY27E adj EPS: 2.9p (+32% vs FY26E)

Net cash of £17m

Roland’s view

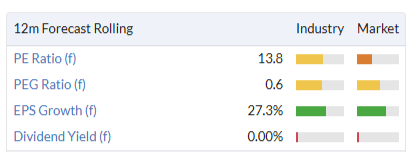

Made Tech’s share price hasn’t done much over the last year, but the company has clearly made operational progress. In the context of current forecasts, I think the shares probably remain quite reasonably valued – note the sub-1x PEG ratio:

Made Tech’s profits are rising more quickly than its revenue, suggesting that the business is benefiting from positive operating leverage as it expands. This is logical for a business of this type – variable costs are likely to be fairly limited, except for remuneration.

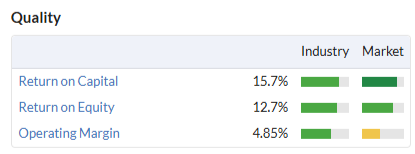

Improved margins could lead to an improvement in the company’s (already good) quality metrics when the FY26 results are published:

The caveat to this is that this is a people business that’s dependent on UK public sector contracts. Any change to purchasing policy or pricing – or the loss of a major contract – could hit a company like Made Tech quite hard.

There doesn’t seem to be any immediate risk of this happening though. Given the combination of continued momentum, a strong balance sheet and owner management, I’m going to leave our positive view unchanged today.

Cake Box Holdings (LON:CBOX)

Up 3.4% at 197p (£86m) - Final Results - Roland - AMBER/GREEN =

Shares in this confectionary franchise business have now risen by 80% from their 2022 lows – a growth rate of 17% annualised:

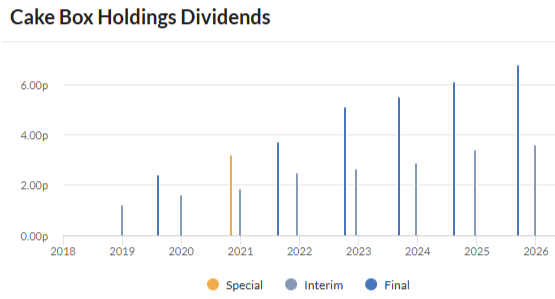

This performance has been paired with an unbroken dividend record since listing:

For investors who backed the company following news of its financial reporting issues in 2022, Cake Box has been a pretty satisfactory investment.

Today’s results suggest to me that this momentum could continue for a little longer yet. Let’s take a look.

FY26 results highlights

This year’s sales include the first full-year contribution from Asian sweet retailer Ambala. This has resulted in a big jump in revenue that’s worth splitting out:

Group Revenue up 39.5% to £59.7m

Total Systems Sales up 27.7% to £111.3m (the value of finished products sold to customers)

Cake Box revenue +9.3% to £45.9m (+4.8% like-for-like)

Ambala revenue: £14.1m

The group added 37 news stores last year, taking the total to 310. This included 25 new Cake Box stores and 12 new Ambala stores.

Management reports solid trading during the year, reflected in solid LFL sales growth of 4.8%. For contrast, Greggs’ LFL sales growth was less than 3% over a similar period.

Online is also playing a growing role – website sales rose by 16% and contributed nearly £22.9m (39%) of revenue – a 20% increase on the prior year. I suspect much of this reflects the inclusion of Ambala, whose products are perhaps more likely to be advanced purchases for gifting, etc.

However, while profit growth was strong, earnings didn’t quite keep pace with sales growth:

Gross profit +52.6% to £34.3m

Underlying pre-tax profit up 22.6% to £8.7m

Reported pre-tax profit up 16.5% to £6.9m

Underlying earnings per share up 21.1% to 15.97p

Full-year dividend up 5.9% to 10.8p

Drilling down into the P&L shows that the group’s gross margin improved last year, but operating margins fell on both an adjusted and statutory basis:

Gross margin up to 57.4% (FY25: 52.5%)

Adjusted operating margin 17.0% (FY25: 17.2%)

Reported operating margin: 14.0% (FY25: 14.4%)

I think there are a few points worth highlighting to understand the movements in margins:

Gross margin: Ambala’s gross margin of c.70% is much higher due to its predominantly owned store estate. This is the reason why the group’s gross margin rose so much last year - core Cake Box gross margin was fairly stable.

Operating margins: administrative expenses rose by 59% to £25.9m last year, putting pressure on operating margins. Average headcount rose from 185 to 377 due the acquisition of Ambala and broader expansion. Labour and energy cost inflation presumably also contributed to this increase.

Profit adjustments: Cake Box embarked on a project to replace its ERP system in 2022, but has decided that this is no longer fit for purpose following the acquisition of Ambala. This has resulted in a £1.7m impairment charge, which accounts for the bulk of this year’s profit adjustments.

Balance sheet & cash flow: finance costs rose last year due to the acquisition of Ambala, but year-end net debt of £10.8m (FY25: £9.0m) only represents 0.9x EBITDA and does not look a concern to me.

Free cash flow was constrained last year as capital expenditure is running higher than usual to fund a new Bradford warehouse, which is due for completion in 2027.

However, I think the underlying picture remains positive. After adjusting for the extra capex, my sums suggest Cake Box converted 100% of net profit into underlying free cash flow last year.

I don’t have an issue with companies investing in their operations to support growth when it’s done sustainably and in a balanced way, which I think is the case here.

Profitability: one of the beauties of a franchise model is the ability to expand rapidly without a corresponding increase in capital employed. This can lead to very high returns on capital for the franchisor.

Cake Box’s capital employed was essentially unchanged last year:

Capital employed: £47.3m (FY25: £48.4m)

Net assets: £28.0m (FY25: £26.7m)

But the increase in profits supported a healthy improvement in profitability:

Return on capital employed: 17.6% (FY25: 12.7%)

Return on equity: 19.1% (FY25: 15.5%)

Such double-digit returns can support attractive cash generation, allowing companies to self-fund expansion and maintain attractive shareholder returns. I think these results provide a fair demonstration of this.

Outlook

Trading in 2027 has started positively and ahead of 2026, supported by continued momentum in system sales performance

This sounds like an in-line outlook statement to me and house broker Shore Capital has indeed left its FY27 forecasts unchanged today. Hitting these wouldn’t be a bad result though, in my view. Current estimates suggest another year of double-digit sales and pre-tax growth:

FY27E revenue: £67.8m (+13% vs FY26)

FY27E adj pre-tax profit: £10.0m (+14.9% vs FY26)

FY27E adj diluted EPS: 16.7p (+8.4% vs FY26)

As far as I can see the lower earnings growth forecasts for this year reflects a return to a normal c.25% tax rate in FY27, after benefiting from a dip to 23.9% in FY26 relating to prior year adjustments.

Roland’s view

Many UK investors still appear to be wary about cake shops following the failure of Patisserie Valerie. Cake Box has also had its own accounting issues in the past, albeit relatively minor.

This business is certainly not free of risks. While management has chosen not to mention it much in today’s results, I think we have to assume that cost inflation is an ongoing challenge, as it is elsewhere in the consumer sector. Over-expansion is also a potential risk – the group plans to open a further 35 stores this year and is targeting 500 over time (versus c.370 today).

However, like Made Tech, Cake Box is an owner-led business – CEO Sukh Chamdal controls 23% of the shares. My guess is that Mr Chamdal will be keen to preserve and enhance the value he’s created for equity holders.

While it’s disappointing to see the company write off nearly £2m of IT spending following the acquisition of Ambala, more broadly this acquisition seems to have been a successful and logical addition to the business.

The company’s growth record in recent years has been fairly strong. Operating profit has risen at an annualised growth rate of 14% since 2021 and the balance sheet remains sensible. Cash generation has been consistently good and the stock continues to look reasonably valued to me, with a forecast P/E of 12 and 6% dividend yield.

We’ve been AMBER/GREEN on Cake Box for a while now and the shares are on my personal watch list.

I’m tempted to turn fully positive, but while I do have a positive impression of the business, I think the in-line nature of today’s results and guidance and evident cost pressures mean it’s fair to leave my previous view unchanged today.

The StockRanks also have a somewhat cautious view, although I suspect this may improve when today’s numbers are digested by the algorithms:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.