Good morning, it's Paul here. I'll be writing all 5 reports this week.

Estimated time of completion - about 1pm.

Update at 12:28 - I'm running a bit late, as I spent so much time on Sosandar this morning. So with my apologies, am extending today's estimated completion time to 3pm.

Update at 14:33 - today's report is now finished.

Please see the header for the updates I've covered today.

.

.

Sosandar (LON:SOS)

Share price: 19.5p (up 23% today, at 08:19)

No. shares: 162.9m

Market cap: £31.8m

(at the time of writing, I have a long position in this share)

Sosandar PLC (AIM: SOS), the online women's fashion brand, is pleased to announce the following trading update covering the six month period ended 30 September 2019.

Today's update reads well, and is better than I expected.

The last update we had from Sosandar was on 23 Sept 2019, which I reported on here. I remember that day well, as I dashed around the London underground, mid-afternoon, trying to spot a Sosandar escalator panel digital advert, to no avail! Turns out that they only appear at peak commuter times. That update indicated that sales growth was strengthening, as promised, with sales in Sept roughly doubling on prior year. As I pointed out at the time, a good initial reaction to the autumn/winter range is usually a good omen for this peak season overall.

Sales growth - the LFL sales growth trend looks very positive;

Q1 (Apr-Jun) +23% - this was a big concern, and the share price sold off heavily when announced (understandably)

Q2 (Jul-Sep) +84% (including +112% for Sep)

H1 total +53% (£2.82m)

Oct >100% growth, over £1m (net of returns) revenues, for the first time.

Clearly we can see a very strong, improving sales trend.

Marketing spend - The strong sales growth trend has been driven by increased marketing spend, which is what the company said it would do, so no surprises there. That's why it raised £7m in a placing at 15p (heavily over-subscribed, which I know is true because my own allocation was scaled back considerably).

TV ads seem to be doing well;

These new marketing initiatives are significantly increasing brand recognition and awareness. September, the first month TV went live, saw a record number of email subscriber sign-ups with a 224% increase on August and the equivalent to approximately six months' performance in the prior year.

Incidentally, I was watching ITV last night, "Return of Alright on the Night", and nearly fell off my settee when a glitzy Sosandar advert appeared at the 9:30pm commercial break. It looked great, and is certainly very eye-catching, playing to Sosandar's strength in high quality imagery, from the joint CEOs background in fashion publishing.

Here is their TV ad. What amazes me is that they managed to find so many parts of Paris with hardly any people around, on a sunny day. From the angle of the sunlight, maybe it was filmed first thing in the morning? (Edit: yes it was, confirmed in my telecon). Anyway top marks here for some lovely shots;

Marketing spend is being further cranked up. This means extra costs & a higher loss this year & next.

Given the strong current trading and the very positive results achieved so far, the Board has taken the strategic decision to accelerate the growth of the business by investing further in TV advertising. Accordingly, marketing expenditure for the current financial year is expected to be higher than previously planned. This increased expenditure is expected to significantly enhance future growth through accelerated customer database growth and increasing frequency of purchase from a loyal and highly engaged following.

Repeat orders - the reason why it makes sense to spend heavily on marketing, is because the customer repeat order rate is high. In other words, once a customer has discovered Sosandar through its marketing, then many of them develop brand loyalty. This means that subsequent contact with that customer is either free (email), or low cost (brochures by post). This point is absolutely key to understanding the investment case for this share.

The numbers haven't been calculated yet, but the lifetime value of each customer could be very large, since Sosandar is turning out to have a very wide customer demographic. The core customer is aged 35-55 female, but the actual customer base is much wider than that. Therefore a new customer aged, say 25+ might still be buying Sosandar clothes 40 years later. That's not something that the fast fashion, youth brands can say, where the customer lifetime might be only 5-10 years.

Gross margin - no figures are given, but the company does say;

Entering Q3, the Company expects to continue with strong full price sales performance and expects some increase in AOV as the cold weather drives sales of higher price point items such as leather and outerwear.

That implies decent margins are being generated, from full price sales. I did wonder about this, as recently I received a 20% off everything email offer from Sosandar. I (wrongly) guessed that this must mean sales might be struggling. Querying it with the company this morning, they tell me that customers are segmented. I hadn't ordered anything for a year (when I bought a lovely velvet dress for my friend Gina, for her birthday - I still haven't got round to giving it to her, it's in a cupboard somewhere!). For that reason, I would have come up on a list of dormant previous customers, who were specifically targeted in a re-engagement email offer.

For this reason, it can be dangerous to draw general assumptions from Sosandar emails, which will be specifically targeted to different types of customer.

Returns rate - has improved from 52% last year, to 49% this year in H1. As the company has repeatedly said, this level of returns is just a cost of doing business. The strategy to grow the product mix into categories that have a lower returns rate (e.g. denim & accessories) appears to be working somewhat.

Active customer base - is only 75k, up 70% - clearly Sosandar is only scratching the surface of the potential market, which is massive, and international too of course. This is why I like this share. If it works, and reaches breakeven next year as planned, then the sky's the limit from then onward.

Of course, bears like to imagine that the company won't achieve that result, miserable sods! Mind you, I've not heard any bearish comments from sector experts.

Forecasts - note that whilst it's looking increasingly likely that Sosandar should meet the challenging growth forecast for this year at the top line & gross profit level, the operating loss for FY 03/2020 is now forecast to be £3.8m - a good bit worse than the previous forecast of £2.3m. Therefore bulls need to be clear that this is still a highly speculative share, and that it's burning cash in order to achieve the growth.

The reason why this is fine, in my view, is that marketing spend is a genuine investment - it's buying repeat, loyal customers, not one-off purchases. After the £7m fund raise there should be plenty of fuel in the tank to reach breakeven next year. No current cash figure is given, but the latest forecast assumes £4.7m net cash remaining at 03/2020, and £2.9m at 03/2021.

My opinion - this update considerably strengthens management credibility. The Q1 bombshell of only 23% growth did dent investor confidence. However, everything management said at the time, about growth accelerating in the key peak trading period of autumn, has turned out to be correct.

That's come at a cost though, in greatly increased marketing spend. That's why they raised more money in the £7m placing earlier this year, so shouldn't come as a surprise to anyone.

Overall, I'm a lot happier today, than I was yesterday.

This share is all about backing high quality management, who really know what they're doing. That's becoming increasingly evident, as the business achieves very ambitious growth targets. Once it's into profit, and self-funding further growth, then we could be onto something very exciting indeed.

Bear in mind also that Sosandar is planning to engage with online platforms, so there's more growth to come from that (effectively wholesaling) route.

Not for widows & orphans, this remains a speculative, loss-making company. But with exciting potential that seems to be working out reasonably well, albeit at higher cost than originally planned.

Call with management - this was a bit of a rush, but hopefully I got answers to some points people asked about;

Q1. Gross margin - no figures given. Narrative talked about high level of full price sales, so am I correct in assuming that gross margin is in line with expectations?

A1. Yes.

Q2. Why is cash figure not mentioned?

A2. I don't think we usually give the cash figure in trading updates. But you'll see all the numbers when the interim figures are published.

Q3. Repeat order statistic of 1.66 - please can you explain how you work this out?

A3. This is order frequency (per customer). It's worked out in the same way as Asos & BooHoo. Calculated as total orders, divided by active customer base. Because we're growing so fast, a lot of orders are from first time customers, which suppresses this metric. If we strip out new customers, the rate rises to about 2.0 times. i.e. an established customer orders from Sosandar about twice per year. This is rising, and customer churn is low.

Q4. TV ads look great, but must be very expensive?

A4. We've worked out a cost effective way of producing the video content. That can then be used in multiple ways, e.g. TV, social media, London underground digital panels by escalators, etc. We closely monitor the uplift in website visits & email sign-ups for every slot where the TV ad is played. So we calculate ROI for every play of the ad, enabling us to fine-tune which slots (times, and specific TV programmes) work best. Not as expensive as you might think. There's a longer tail with TV ads - i.e. immediate sales yes, but also subsequent sales once customers have signed up for email list prompted by a TV ad.

Q5. Are you feeling downward pricing pressure from competitors?

A5. No. Our price points are chosen very carefully, and things tend to sell at full price if we get the price right first time.

Q6. New factories working out?

A6. Yes, we've broadened the supplier base considerably and it's going well.

Management sound upbeat (they always do!), and said they're happy with the way things are progressing.

.

.

Water Intelligence (LON:WATR)

Share price: 287p (up 8% today, at 10:19)

No. shares: 16.9m

Market cap: £48.5m

Water Intelligence plc (AIM: WATR.L) ("Water Intelligence" or "Company"), a leading multinational provider of precision, minimally-invasive leak detection and remediation solutions for both potable and non-potable water is pleased to provide a trading update for year-to-date through the end of the third quarter.

I'm getting a sense of deja vu reading this announcement, and the reason is that it used the same wording with its interim results about a month ago, which I reported on here.

Today: Results for 2019 through Q3 are ahead of market expectations for revenue and comfortably in-line with expectations for profits before taxes (statutory and adjusted).

30 Sept 2019: Results are ahead of market expectations for annual revenue and comfortably in-line with expectations for profit before tax.

Outlook comments sound upbeat today;

"Moreover, we believe strongly that our technology investments will enable us to sustain our growth trajectory in 2020 and beyond. Given our installed base of service operations, especially across the US, and the strength of market demand for both potable and non-potable water infrastructure solutions, we have a considerable opportunity for realizing significant value for our shareholders...

My opinion - it looks quite good.

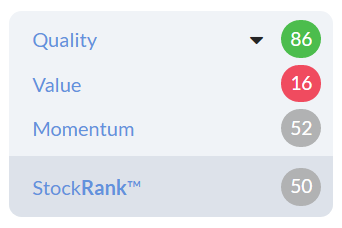

The rating looks full, for a fairly small company, on about 23 times 2019 forecast earnings.

Stockopedia reflects that - good quality, but expensive;

.

.

Cloudcall (LON:CALL)

Share price: 99p (up 2% today, at 11:29)

No. shares: 38.7m

Market cap: £38.3m

(at the time of writing, I hold a long position in this share)

I don't usually comment on "holding in company" announcements, unless there's something of wider interest. The reason for mentioning this one today, is that CloudCall appears to be attracting interest in the USA. Why does that matter? Because US investors value tech/growth companies very differently (i.e. much higher) than we do in the UK. They take a longer term view, generally value this type of company at multiples of the UK, and are much more relaxed about cash burn. They want growth above all else. This approach, combined with vast available funding, is why the USA leads the world in tech companies.

Today, Long Path Partners LP has popped up with a 7.75% (3m shares) stake in CloudCall. Its website describes Long Path like this;

Long Path Partners is a privately-owned investment firm that manages two concentrated equity Partnerships. The Firm employs an ‘ownership’ approach to public equity investing. We seek to compound capital by investing in high quality, predictable businesses that we intend to own for the long term.

It's based near New York, in Stamford. All of which makes me wonder how on earth they came across this tiny AIM-listed company? Looking at the major shareholders list, Long Path already had 2m shares (5.16%), so I'm wondering if perhaps they bought another 1m in the recent placing?

There's another American fund, called Kinderhook 2 LP, which has 11.2% of the company.

My opinion - this is getting interesting. CloudCall operates in both the UK, and USA. The USA is about 40% of its business, and there are obviously much greater growth opportunities there than in the UK, as its economy is something like 6-7 times the size of the UK's. I find it very interesting when a UK company succeeds in breaking into an American market, as its very difficult to do so.

CloudCall's recent big placing, means it has plenty of cash to deploy for faster expansion, which is the plan. Expansion into Australia is happening now, and it is bidding for some much bigger global accounts.

All of which makes me feel that, rather later than originally planned, CouldCall looks as if it could take off. The Yanks think it's cheap by the looks of it, so I wonder if the end game might be a takeover bid from across the pond? It's starting to look more interesting.

.

.

Cerillion (LON:CER)

Share price: 188.5p (unchanged today, at 12:39)

No. shares: 29.5m

Market cap: £55.6m

Cerillion, the billing, charging and customer relationship management ("CRM") software solutions provider, is pleased to provide a trading update for its financial year ended 30 September 2019.

I've been impressed with this company lately. It had some problems earlier this year, with large lumpy orders causing it to deliver a weakish H1. The outlook commentary at the time promised an improved H2. That old chestnut of an H2 weighting! However, kudos to the company, as it has delivered the stronger H2, and today indicates that its results for FY 09/2019 will be in line with expectations. Note that expectations have not been lowered either, so this is a bona fide in line outcome for the year just ended a month ago.

The y-axis hasn't worked properly there. The light blue blobs for 2020 forecast EPS are 11.8p.

.

Big contract wins - this is reiterating what previous announcements have said;

As anticipated in the Company's Interim Results in May, trading has been significantly second half weighted this year due to the timing of contract closures. The second half of the year saw Cerillion sign three major contracts, with these new wins continuing the trend towards larger deal sizes. Over the year, major new contracts were secured from all the Company's key international geographies, Europe, the Americas and Asia-Pacific.

My opinion - I like this share. Management has a lot of credibility, as it has steered investors accurately through a year with lumpy contract wins.

The forward PER of 16.0 looks about right to me for now. Although with some large contracts under its belt, that looks a good reason to expect further growth in FY 09/2020 maybe.

Worthy of a closer look, I'd say. I imagine contracts in this sector would be quite sticky. Therefore there could be nice, operationally geared upside, if it continues winning big contracts. Shareholders also get a 2.8% dividend yield.

.

.

Photo-me International (LON:PHTM)

Share price: 86p (down c.4% today, at 13:32)

No. shares: 378.0m

Market cap: £325.1m

Photo-Me (PHTM.L), the instant-service equipment group, announces the following trading update covering the period from 1 May 2019 to 30 September 2019.

I'm not sure why it's providing a 5-month update, instead of waiting until H1 was finished?

In the period to 30 September 2019, overall Group trading has been in line with expectations, underpinned by continued growth in Continental Europe and Asia, led by the Laundry business, despite trading in the Identification division in the UK remaining challenging. This has been due to continued uncertainty around the UK's European Union exit negotiations, leading to lower consumer activity, and the UK Government's decision to allow for photos taken on a smart device or camera at home to be used for passport photo identification.

That last bit is the major concern about this business. Its photo booths, mostly used for passport & other ID photos, look very much like a legacy business that maybe won't exist at all in a few years' time, if smartphone photos become generally accepted in its other geographies. Alternatively, it might end up being the case that booths become more necessary, in order to securely capture & send to Government agencies not only a photo, but also biometric data connected with that person.

PHTM also operates in other markets, such as laundry machines, other kiosks, and there was talk of introducing self-service banking kiosks too. With various geographies having different dynamics, it all looks far too complicated for me to be able to work out what's going on, let alone predict what might happen in the future. I think researching this share would need a lot of work, to understand what Government policies are likely to be in its various markets.

My opinion - people have been predicting the demise of this business for about the last 20 years. Yet it's still churning out big profits & cashflow, and paying a whacking great 9% dividend. That very high yield is the market clearly signalling that it doesn't see the dividend yield as sustainable. If the market's wrong, then the share price would recover well from here.

I would have to spend days solely focused on this one share, to understand all the different markets, and products, that this company offers. Even then there would be a lot of guesswork involved, to form a view on the future prospects of each. That means I have to file it in the too difficult tray. But good luck to holders. This company does have a long track record of multi-bagging from near-death experiences. Just look at the long-term chart below;

.

.

A couple of snippets to finish off with;

Ilika (LON:IKA) ( I hold a long position in this share) - invites investors to apply to attend a company visit, in Romsey, near Southampton, on 5 Dec 2019. I attended a similar event in Jan 2014. The company's laboratories are like something from a 007 Bond film - everyone wearing white coats, machines whirring away with robotic things inside them, doing stuff.

The narrative was tremendously exciting, and a number of us on the visit texted our brokers to buy shares in this tremendously exciting company, developing new materials, and solid state batteries. We thought we were geniuses, when the share price shot up from c.25p to c.100p. It then took nearly 4 years to come all the way back down again!

What's happened since 2014 then? The share count has doubled, and it's generated losses of £3-4m each year, with nothing of any commercial value having been achieved, seemingly. Revenue is mainly Govt grants. It all looks pretty dismal.

That said, I've kept a tiny residual holding, just in case something commercially viable does eventually come out of Ilika. It's working in a very interesting area, of battery technology.

If the share price 4-bags again after this next investor visit in Dec 2019, then I'll happily release my shares into the market for someone else to treasure!

.

OK, that's me done for today. Hopefully this has been useful/interesting for readers, and thanks for your comments.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.