Good morning! It's Paul here with the SCVR for Tuesday.

Please see the header above for companies reporting today that I will be reviewing.

As usual, it's initially a blank article, which I put up about 7am, so that readers can add any comments you have about the 7am RNS releases. I then write up the main report throughout the morning, section by section. Assuming I can manage to avoid accidentally deleting any of them!

Estimated timings - I have to write today's report early today, due to needing to travel back to Bournemouth this afternoon, from London. It will be interesting to see how the city centre looks these days. It was like a ghost town last time I walked through the City, towards Waterloo. It's difficult to predict what is likely to happen to all those fancy offices, if companies decide to have staff permanently based from home. Or will companies & staff gradually return, once treatment/vaccines have resolved covid-19 (whenever that might be)? My feeling is that humans don't have terribly long memories, and it often surprises how quickly things do return to normal. after e.g. natural disasters, terrorist attacks, wars, etc..

Today's report is now finished.

AA.

Share price: 25p (pre-market open)

No. shares: 620.8m

Market cap: £155.2m

Possible Offer & Update on Refinancing Progress

Possible Offer for AA

The Board of Directors of AA plc (the "Company" or the "Group") notes the recent press speculation regarding a potential refinancing of the Group's indebtedness and the possibility of an offer being made for the Company in connection with such a refinancing.

The Company confirms that it is currently in discussions with a number of parties in relation to a wide range of potential refinancing options.

This is particularly interesting, because the AA's balance sheet was wrecked by financial engineers, who came up with the ridiculous idea to load it up with massive debt that would never be repaid. It was therefore only a matter of time before the company ran into a financial crisis. The scale of the problem is mind-boggling, given it's only now a £155m market cap company;

As stated in its preliminary results announcement on 7 May 2020, while the Group continues to remain well within its financial covenants, at the end of the last financial year the Group had approximately £2.65 billion of total net debt, of which £913 million is scheduled to fall due for repayment within the next two years.

Debt reduction is therefore a key priority and the Group continues to proactively manage its capital structure and to seek to reduce its indebtedness well ahead of the upcoming maturity dates on its outstanding indebtedness.

Today's announcement goes on to say that 3 (named) private equity organisations are sniffing around, saying;

The Potential Offerors have each indicated that any possible offer would involve a significant amount of new equity capital being injected into the Group, in order to reduce indebtedness following completion.

That makes complete sense, but it does raise the question as to why an offer would be generous to existing shareholders? The financial incentive would be for an acquirer to make a lowball offer for the equity, on the basis that the company could otherwise become insolvent if it were not able to refinance its huge debt pile.

Management is also considering an equity raise separately. Note the use of the word "stakeholders" below, which is often code for existing equity being worth little to nothing;

Separately and in parallel with the discussions relating to a potential offer for the Company, the Board intends to continue assessing a range of other potential refinancing options including the possibility of raising new equity. In considering the different potential refinancing options available, the Board wishes to ensure that the Group has a stable, long-term capital structure and that the proposed refinancing enhances the long-term viability of the business and is in the best interests of the Company and its wider stakeholders.

My opinion - I think this could go either way. There's so much private equity money sloshing about, that maybe someone might be prepared to pay top whack? Or, there's a possibility that a bid could be below the current share price, maybe a lot below, and debt holders could be asked to take a haircut in return for the injection of fresh equity? At this stage we don't know, but I'm wary that this might not necessarily be a good deal for existing shareholders. In massively over-indebted company refinancings, the existing equity can be all-but wiped out. Hence I'm not tempted to buy on the opening bell, as it's too risky without knowing what the approach of the potential bidders is going to be.

.

Reach4entertainment Enterprises (LON:R4E)

0.13p (down 48% today) - mkt cap £1.65m

Delisting

The company says 2019 was strong, but it's seen a severe impact from covid. It does marketing for West End shows, etc, so it's understandable that business must have dried up. Not the company's fault, it's just unlucky to be operating in the wrong space.

After careful consideration, it is the Board's belief that in a time where prospects for the future are uncertain and where cash management is paramount, the costs of maintaining a London listing outweigh the benefits afforded by operating as a public company...

Even for the smallest companies, an AIM listing can cost £100k+ p.a., so what's the point, if there's little market liquidity, and no appetite to provide more funding? I've heard from other sources too, that there's so much money sloshing around, that private investment (e.g. from family offices) is more readily available than from AIM investors. Hardly surprising really, considering that we've had so much junk floated on AIM over the years, that investors are more wary these days.

I do think it's a good idea to review our portfolios for rubbish that's likely to de-list. Even if it's only worth a couple of hundred quid, I'd rather salvage something, than throw it away. After all, if there was £200 cash lying on the floor, you wouldn't disregard it as immaterial to your portfolio! So why do the same with failed investments?

By the time a market cap goes below about £5m, companies are at high risk of de-listing. Then you have usually an instant 50% loss on the de-listing news, and a scramble to sell at any price. Although occasionally, something interesting can happen, so it's not always clear-cut. Sometimes a more interesting speculative business gets reversed into an existing AIM listing.

.

Beeks Financial Cloud (LON:BKS)

Share price: 96.5p (down 2% today, at 08:55)

No. shares: 51.2m

Market cap: £49.4m

Beeks Financial Cloud Group Plc (AIM: BKS), a cloud computing and connectivity provider for financial markets, is pleased to provide an update on trading for the year ended 30 June 2020.

The Group has continued to make good progress against its strategic objectives and expects to announce trading results within the range of market expectations.

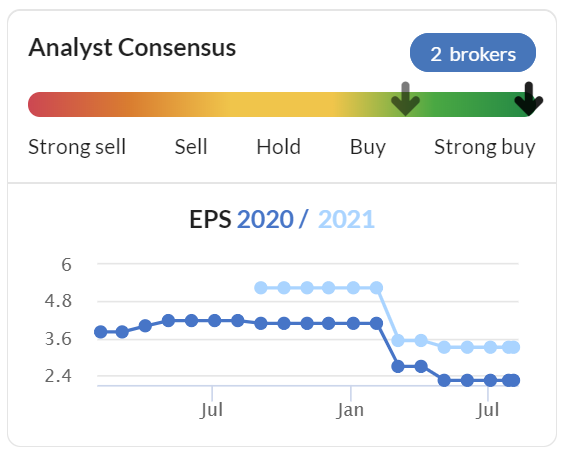

What a pity the company & its advisers didn't include a footnote, to disclose what market expectations are. I can't find any broker research, and the trouble with consensus figures is that we don't know if they're still current forecasts, or have been withdrawn?

The Stockopedia broker consensus graph is usually a good guide - if forecasts dropped sharply in Feb-Apr 2020, then that's a good indication covid impact was being baked into the figures, so they're probably OK to rely on. Here we have;

.

.

I therefore surmise that the 2.22p forecast EPS for FY 06/2020 must be relevant. That's a PER of 43.5.

Note how much forecasts were reduced this spring - from 4.08p to 2.22p, a reduction of 46% in forecast earnings for FY 06/2020. That's a big reduction in earnings, and makes me feel less positive about the company than before.

Today's update strikes a positive tone, and says covid had little impact, pipeline strong, etc. But that's not reflected in the big reduction in forecasts.

My opinion - I hadn't realised that forecasts had come down so much. If the company had been on track to achieve 4-5p EPS, then the current share price would look justifiable. However, given the much lower forecasts, I think the valuation is looking a bit toppy. It's still an interesting niche company though, so I'll keep it on my watch list.

.

Brickability (LON:BRCK)

Share price: 96.5p (up 3% today, at 09:26)

No. shares: 230.5m

Market cap: £222.4m

Brickability Group plc ("Brickability" or "the Company" or "the Group"), the leading construction materials distributor, is pleased to provide the following update on trading for the three months ended 30 June 2020.

I can't remember much about this company, and have only covered it here once before, so to refresh our memories, here are my notes from Nov 2019.

The update today reflects the brief shutdown of the building sector in April & May. It's a hopefully one-off impact, as being outdoors, the building sector is probably one of the lower risk areas of facing a renewed lockdown if we get a second wave of covid. It sounds like the impact wasn't too bad, helped by the furlough scheme;

Revenues for the 3 months ended 30th June 2020 were £23.8m and encouragingly, June revenues returned to 83% of June 2019 and this trend has continued throughout July. While April's reduced trading levels resulted in a loss in that month the Group returned to profit in May and produced a pleasing EBITDA* of £1.6m in June.

Note that BRCK seems to drop-ship a lot of product, so there shouldn't be a problem with inventories.

Liquidity - sounds fine;

The Group's liquidity continues to be strong with a net debt of £1m as at 30th June 2020. Cash balance as at 30th June 2020 was £24m with £25m revolving credit facility drawn. In addition, the Group has an unutilised overdraft of £5m and an accordion of a further £5m available.

Outlook - nothing to worry about here;

While it is still too early to predict the level and sustainability of market recovery the Group remains confident in the underlying demand for UK housing. Recent government initiatives along with the SDLT "holiday" have further reinforced that confidence.

The Group can also confirm that its acquisition strategy remains on track and that it is currently evaluating a number of value-creating opportunities.

A time of crisis can be a good time to pounce on financially distressed competitors.

My opinion - the consensus forecasts look like they might pre-date covid, so I'm not going to rely on them. I cannot find any recent broker notes, so am in the dark when it comes to forecasts. Without that information, I can't take this any further unfortunately.

The share price chart below looks very similar in shape to the housebuilders, so it looks like BRCK shares are just tracking the sector. There could be upside here, as I think housebuilding (and hence their suppliers) could see a sustained recovery. There's plenty of demand for new houses.

.

.

Nwf (LON:NWF)

Share price: 213p (up 4% today, at 10:07)

No. shares: 48.75m

Market cap: £103.8m

There was a strong update which I reported on here on 29 April 2020. Although the uncertain outlook comments worried me at the time.

Moving forwards to today;

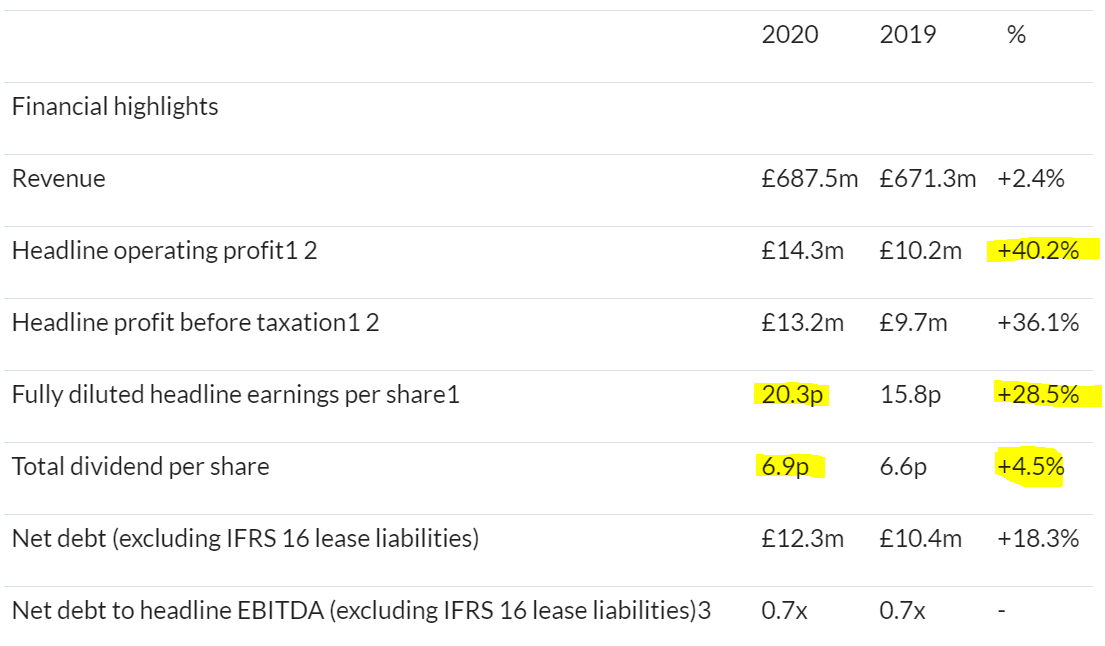

NWF Group plc ('NWF' or 'the Group'), the specialist distributor of fuel, food and feed across the UK, today announces its audited final results for the year ended 31 May 2020.

The headlines look excellent;

.

Not many companies are increasing divis this year, so a good positive move there.

20.3p EPS looks like a beat against forecast of 18.6p shown on the StockReport.

Based on a share price of 213p, and 20.3p EPS, the PER is 10.5. Historically that would have looked about the right price for this type of low margin business, but in this new era of apparently permanently low interest rates, maybe PERs should be higher?

The fuels division makes most of the group profit, and there is a one-off benefit here. Therefore, I think caution is needed re chasing up the share price;

A dramatic fall in the oil price and an increase in demand for heating oil from domestic customers during lockdown delivered substantial one-off gains.

Outlook - this looks fine, the key part says;

Performance to date in the current financial year has been in line with the Board's expectations. Overall, the Board continues to remain confident about the Group's future prospects.

Balance sheet - looks adequate. NAV: £51.1m, less intangibles of £31.4 = NTAV £19.7m

Note the pension deficit has risen to £21.0m.

My opinion - it's performed well, and seems resilient re covid.

Overall, the valuation looks about right to me.

.

I have to leave it there for today. See you tomorrow!

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.