Good morning, it's Paul here with the SCVR for Tuesday. Many thanks to Jack for covering yesterday.

Timing - I should have the whole day free to concentrate on this. Update at 12:31 - I've spent most of the morning on Redde (I hold) because I think it looks excellent on a risk:reward basis. So that's the best use of my time. This afternoon I'll be focused on shorter sections for lots more companies. Likely finish time is about 6pm. Update at 20:06 - I'm still plugging away, should be done when it's done. Update at 21:57 - I got there in the end! Today's report is now finished.

.

Agenda

Redde Northgate (LON:REDD) (I hold) - Interim results & my notes from the analyst call (done)

Joules (LON:JOUL) - Trading update (done)

Begbies Traynor (LON:BEG) - Half year results (done)

Gaming Realms (LON:GMR) - Trading update (done)

Zytronic (LON:ZYT) - Final results (done)

Porvair (LON:PRV) - Trading update (done)

Ideagen (LON:IDEA) - placing at 215p (done)

Anything else that there’s time for, and looks interesting.

.

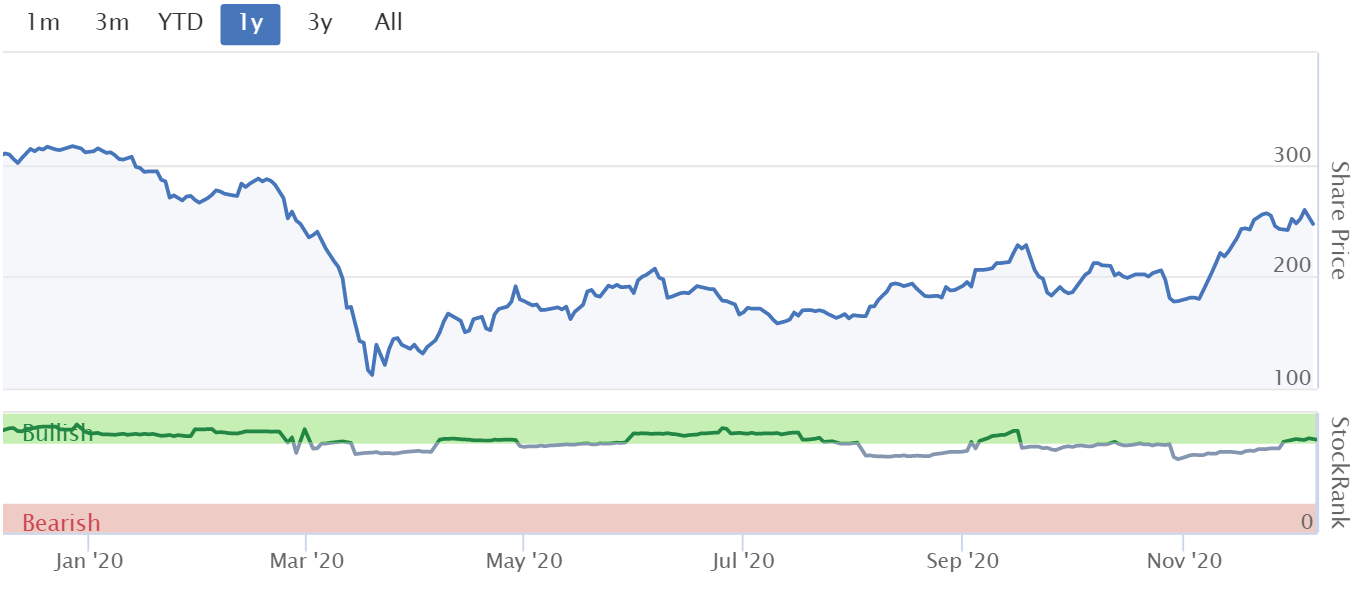

Redde Northgate (LON:REDD)

Share price: 252p (up 2% today, at 08:17)

No. shares: 246.1m

Market cap: £620.2m

(I hold)

Redde's market cap is now above my usual upper limit of c.£400m, but I like the share (and hold personally), so I would be analysing the figures anyway for myself. So might as well share my work here too. Also an arbitrary upper limit on market caps is crazy really - because it means that we stop covering the winners, and carry on reporting on the also-rans!

Several readers nagged me to look at this group - a combination (all-share merger Feb 2020) of accident management (courtesy cars, etc) group Redde, and Northgate - a white van hire company. Here are my notes from 29 Oct 2020, which are worth re-reading, to set the scene. I felt the share represented an excellent investment proposition at 178p per share (on a PER of only 6.5!), and added some to my own portfolio afterwards, when funds permitted (I tend to be fully invested most of the time). The share price is up nearly 40% since then, although so have lots of other cyclical companies, triggered by the positive news on covid vaccines, so we mustn't run away with the idea that we're genius stock-pickers, when we could have picked anything cyclical and seen a similar rise in the same timeframe.

Today’s interim figures are for the 6 months ended 31 Oct 2020 - the first thing to note is that prior year comparatives are not comparable, as they pre-date the merger in Feb 2020. Also of course this is a period heavily affected by covid.

“Encouraging momentum” - Northgate performed ahead of expectations, recovering to slightly above pre-covid levels. Strong residual values & disposal profits

Redde seeing a slower recovery - impacted by lockdowns - as previously advised, so no surprise here

Cost savings from merger achieved of £15.9m p.a. - ahead of plan

Outlook - remains confident in meeting market expectations for FY 04/2021 - excellent, that’s the main thing I want to know when any company reports on trading, despite possible disruption from further lockdowns

Interim dividend declared of 3.4p. Stockopedia shows full year divis forecast at 13.9p, a yield of a very healthy 5.6% - in a low interest rates environment, that makes this share very attractive I think, and could drive continued share price increases perhaps?

Underlying EPS of 13.4p (down 24.1%) looks in line with full year broker consensus of 27.3p

Note that FY 04/2021 is a heavily disrupted year, so we should realistically expect increased earnings next year. Broker consensus is 36.1p for next year, which would drop the PER to only 6.8 - which looks far too cheap, to me. That's the type of rating I'd expect to see in a structurally declining business, which is not the case here. So it's the wrong rating in my view - irrationally low.

Borrowing facilities - plenty of headroom, and look how cheap these borrowings are!

.

Balance Sheet - looks fine to me. NAV: £882.1m, less intangibles of £296.2m = NTAV £585.9m - a similar figure to the mkt cap of £608m. There's a lot of debt, but the value of the vehicle fleet is very much larger than the debt, so not a problem. That's evidenced by how cheap the borrowings are - i.e. lenders don't see this as risky lending, hence it's cheap.

My opinion - I haven’t read through all the detailed commentary yet, but have the key facts & figures I need - i.e. in line with FY 04/2021 expectations, which means the PER is only about 9 - why so low, that doesn’t make sense to me.

This share seems fundamentally under-priced, especially versus next year’s forecasts, which the market will soon be focusing on for valuation purposes. I really cannot see any valid reason why this share is below 400-500p per share, which seems a reasonable (not even expensive) valuation range of about 11-14 times next years earnings. That seems a sensible price target to me.

Therefore, at the current price of about 245p, this share just looks the wrong price to me. It looks a bargain, despite the recent c.40% share price rise. Plus we’re paid generous divis whilst we wait for it to continue re-rating.

This share looks one of the best value shares I’ve seen in a while. Thanks again to readers who persuaded me to look into it. The white van hire business should continue doing well, because so much retail is now moving online, requiring an army of vans & drivers to deliver everything. The accident management business should recover next year once covid lockdowns are finished. Therefore common sense tells me that it's realistic to expect earnings to recover next year.

Note the consistently high StockRank too, which reassures me.

.

.

EDIT: Analysts call - I’ve been listening in to this. It mostly reiterates what’s in the results statement. Here are my notes of key points from the call;

- Residual values of vehicles - sold excess stock of vehicles into rising demand/prices. Under-supply supporting residual values. Reckoned to be 20% under-supply of new vehicles this year, and forecast 8% next year (not sure if this is cars or vans, or both?). Remember that right-hand drive vehicles for the UK are bespoke production for European manufacturers.

- Good recovery potential from Nationwide Accident Repair, recent acquisition

- Cost synergies excellent at £19.2m from merger

- Early take-up is good from offering Redde services to Northgate customers

- Better margins, due to cost cuts

- Example of cost control - all done digitally now, everything over £1k (apart from usual consumables) is subject to Board approval. Fantastic way to avoid over-spend

- Lockdowns impact - significant potential once things return to near-normal

- Net Promoter Scores routinely over 70. Good TrustPilot scores. Happy staff & customers creates a good business

- Large new orders being tendered for, sound optimistic about these

- Structural & permanent favourable changes in van market - many fleets that historically bought vehicles, are now switching to leasing

- New lending lines for leasing vehicles, at comparable cost to buying. Coy about size, just said “tens of millions”

- Market expectations - as in RNS, confident of meeting them. That’s based on current run rate. So could be upside, if lockdown restrictions eased this FY. So it sounds to me like likely to meet or beat FY 04/2021 forecasts, rather than just meet

- Vans - now offering a package of services, not just rental of the van itself. Proving popular, strong demand, not seeing margin pressure from competitors

Presentation slides from today's analyst call are available here on Redde's website, worth a look for a nice clear explanation of the main points.

Overall, I think the tone of the call was positive, and management sound down-to-earth, hands-on managers, which is what I like.

I asked the PR company to consider doing a webinar for everyone on future results days, not just for analysts. They said they’ll consider that next time, so let’s hope they go ahead, as there are a lot of private investors interested in this company, so it would be a positive step for the company to engage more with its small army of PIs!

End of edit.

.

Joules (LON:JOUL)

Share price: 162p (down 3%, at 10:23)

No. shares: 108.4m

Market cap: £175.6m

Joules, the premium British lifestyle brand, is pleased to provide a Pre-Close Trading Update in respect of the 26-week period ended 29 November 2020 (the first half of the Group's financial year ending 31 May 2021 or the "Period").

Continued strong e-commerce growth reflecting the strength of the Joules brand and its growing customer base

As I’ve mentioned here many times before, the attraction of Joules over other retailers are twofold;

- Very distinctive brand, customer loyalty, with differentiated (hence high margin) products, and

- High level of internet sales, at c.50% of total retail sales before covid, and even higher now

It’s very clear now, that the brands which are failing, are nearly always the ones that were too slow to embrace eCommerce, and/or failed to crack digital marketing. Probably the only exception I can think of is Primark, which doesn’t sell online, but still attracts large footfall into town centres. Other shops should probably pay Primark a fee, as a thank you for attracting so much footfall into their areas!

Brands that are prospering, or at least not under any threat of insolvency seem to be ones which have a high proportion of internet sales. Next (LON:NXT) springs to mind there. Even stodgy old Marks And Spencer (LON:MKS) (I hold) is making strenuous efforts to increase its online offering, aiming for c.40% in a couple of years’ time.

Back to Joules, and today’s update looks good -

The positive trading trends reported in the Group's update on 5 November 2020 have persisted through the important Black Friday trading period and into the Christmas trading period so far, with sales for the Period remaining ahead of the Board's initial expectations.

E-commerce sales are very good, although bear in mind the period in question would have caught lockdown in November, and lower footfall at other times prior to that. Therefore eCommerce sales would naturally rise as a % of the total from these factors.

- H1 revenues down 15.3% Y-on-Y, is really good in the circumstances, I think.

- Total store trading hours (a useful stat) down 40% of typical trading time

- Like-for-like stores sales down 17% on LY, again very good I think, and ahead of expectations

- Retail gross margin down 300bps in H1 - that’s fine, because retailers must have had nightmares managing intake & inventories, so more discounting is bound to happen. Dropping just 300bps again is impressive in the circumstances I feel

- Wholesale revenue down 44% - I think this reinforces how well Joules has done with its own store sales (and online), very much better than wholesale customers have done. I worry about the bad debt risk from wholesales, it would be good to know what credit control procedures Joules adopts (e.g. insuring its receivables book?). If any of you speak to management, that is a good question to ask for any business doing fashion wholesale.

Liquidity - ample -

The Group's balance sheet remains strong with net cash of £15.6 million and liquidity headroom of £64 million.

Guidance - very impressive that the company has remained profitable, albeit with temporary relief from business rates, and possibly some benefit from furlough. I feel the company should have disclosed the extent of these benefits, to give us the full picture -

As a result of the Group's encouraging trading, the Board anticipates reporting PBT (IFRS16 basis, pre-exceptional items) for the Period of between £3.5 million to £4.0 million. Notwithstanding the significant uncertainties that are anticipated to persist over the remainder of the peak trading period and into the next calendar year, the Board remains confident that the Group will achieve its Full Year expectations.

Outlook sounds confident -

Nick Jones, CEO of Joules, commented:

"The strength of our digital proposition, the increased number of Joules customers and the growing appeal of the brand has meant that Joules has continued to trade well during the Period, despite the impact of enforced store closures.

"We delivered a good Black Friday trading period through our online channel and our Friends of Joules digital marketplace continues to perform ahead of our expectations. We have strong momentum - particularly through our online channel - and a good stock position that underpins our confidence for the peak Christmas trading period. We have been pleased with the performance of our stores in England for the first few days since their re-opening in early December.

"As anticipated, our wholesale sales have been subdued in the first half, however an improved performance over recent weeks and the positive response to our spring/summer 21 ranges, that were sold-in via our digital B2B sales platform, gives us confidence for the recovery of the wholesale channel over the coming seasons.

"The retail sector continues to face a number of near and medium-term challenges, including the ongoing impact of Covid-19 on our communities and economy as well as Brexit-related uncertainties. I have no doubt that Joules, underpinned by the strength of our brand and our flexible and scalable platform that now includes our Friends of Joules digital marketplace, is well positioned to be one of the long-term winners against this challenging backdrop.

My opinion - I’ve been really impressed with how Joules has coped with this chaotic covid/lockdown year. This has been reflected in a very strong share price recovery.

How to value it, that’s the really difficult question? Here are 3 options, take your pick!

- Value JOUL on a multiple of (greatly reduced, and probably too pessimistic) earnings forecasts. So 162p share price, divided by 3.6p FY 05/2021, and 6.7p FY 05/2022 forecasts (I’m using the latest forecasts from Liberum, in its update note today, rather than consensus numbers). That gives a valuation of a PER of 45, and 24.2 - expensive, but I would expect the PER to be high, when based on abnormally bad years.

- Assume a full recovery back to pre-covid actual/forecast earnings, which suggests EPS of maybe 20p is achievable, giving a PER of just 8.1 - attractive value.

- The most bullish scenario - treat Joules as a growing online business, with a few shops (called “showrooming”, I am told!), although with its own lifestyle portal called Friends of Joules, with exponential growth potential, therefore value the shares at a multiple of future sales (i.e. ignore earnings).

Personally, I can’t make up my mind. The recent surge in share price looks justified, but someone else has benefitted from that, and I can’t bring myself to pay top whack for it so soon after this surge - illogical maybe, but there we go -

.

.

As Liberum points out, the share price is now still well below its former highs, despite the business having made great strides in developing its eCommerce side of the business.

I think this share is a good one to consider buying on any market panic which might occur if no-deal Brexit spooks people, if it happens, who knows?

.

Begbies Traynor (LON:BEG)

Share price: 89p (down 3% at 14:35)

No. shares: 127.9m

Market cap: £113.8m

Begbies Traynor Group plc (the 'company' or the 'group'), the business recovery, financial advisory and property services consultancy, today announces its half year results for the six months ended 31 October 2020.

The share price hasn’t moved much today, which suggests there’s probably little changed since Begbies issued a recent H1 trading update, which I covered here on 18 Nov 2020.

H1 revenue up nearly 11% to £37.5m

- Adj PBT up 25% (as guided previously) to £5.0m

- Adj EPS up 19% to 3.1p

- Interim divi of 1.0p (up 11%)

- Net cash £0.7m (as guided previously)

Adjustments relate to acquisitions, £1.5m amortisation of goodwill, which is fine to ignore. Although the £3.1m of transaction costs for acquisitions also adjusted out, seems rather a lot.

Current trading & outlook - this looks very similar to the last trading update, so no surprises -

· Business recovery and financial advisory strongly positioned:

o increased order book of committed future insolvency revenue

o increase in market insolvency levels expected once short-term support measures for the economy are removed

· Property advisory and transactional services continue to recover:

o anticipate will maintain current levels of performance in spite of the challenging environment

· Results for the full year expected to be at least in line with current market consensus*, which would represent a further year of growth

· A Q3 trading update will be issued in March 2021

* Market consensus for adjusted PBT of £9.8m (as compiled by the group)

Balance sheet - is unusual because of the nature of this sector - running up a lot of costs, which are eventually paid longer term when an insolvency case is closed. Although stage payments are often negotiated along the way. BEG seems to be effectively balancing up receivables and payables, such that overall the balance sheet seems reasonable.

NAV: £62.0m, less intangibles of £58.3m, leaves NTAV of only £3.7m. Although of late, I’m deducing deferred taxation creditor too, because this usually seems to relate to intangible assets. That improves the NTAV to £9.4m - adequate, but that is very little asset backing for a £114m mkt cap company - so you’re buying earnings here, not assets.

See note 8, taxes & social security creditor has gone up from £2.6m a year ago, to £6.0m this time, implying creditor stretch - using time to pay schemes from HMRC I imagine. That means cash is likely to be temporarily flattered. Something to bear in mind, but not a major problem given that BEG has plenty of headroom on its bank facilities.

I’d like more clarity on the “Deemed remuneration” receivables, which I think might be connected with partner incomes, or acquisitions? Or both. I’m not saying there’s anything wrong, just that I’d like to understand it better.

Valuation - I can’t find any broker notes unfortunately. The broker consensus figures we have on Stockopedia show net profit (after tax) of £7.84m for FY 04/2021. That looks consistent with the company saying profit before tax of £9.8m, i.e. a tax rate of 20% - near enough to the actual rate. So that means we should be able to rely on the 5.95 EPS forecast shown on Stocopedia (it’s always good to sense check figures for small caps, because just one old forecast could skew the consensus badly).

At 89p per share, divided by 5.95p forecast, then we have a PER of 15.0 times, dropping to 11.3 times if BEG meets FY 04/2022 forecasts.

My opinion - the valuation looks about right to me. Interim results are in line with guidance, and the outlook comments seem positive.

As mentioned before here, I think this share is a nice hedge, if you think the UK economy is going to tank next year. Even if you’re wrong, the downside looks quite limited. It pays divis along the way, whilst you wait.

Quite good overall then, in my opinion.

.

Gaming Realms (LON:GMR)

Share price: 19.65p (down c.5% today, at market close)

No. shares: 286.0m

Market cap: £56.2m

Gaming Realms plc, the technology led developer and licensor of mobile focused gaming content, today issues a trading statement ahead of its 31 December 2020 year end ("the Period").

Today it says -

Since updating the market on 8 September 2020 when publishing its interim results [Paul: see my notes here], the Company is pleased to report that business performance and sales momentum has continued the trend demonstrated throughout the first 8 months of this year.

Revenues for the Period are expected to be £10.7m, 55% ahead of 2019. As a result of this increase in revenue, the Company expects adjusted EBITDA of not less than £2.75m for the year ended 31 December 2020.

Stockopedia is showing broker consensus of £10.8m revenues for FY 12/2020, so that looks almost in line.

Adj EBITDA of £2.75m compares with £1.24m in H1, so that implies an increase to c.£1.51m in H2 - good, but not stellar.

Capitalised development spending was £1.1m in H1, double for the full year to £2.2m, and that’s using up most of the £2.75m adj EBITDA. So in the real world, this business is only just above cashflow breakeven.

Therefore a £56m market cap is factoring in a lot of further growth.

On the upside, it does have some big name clients, and is expanding nicely in the USA. The market cap largely rests on this upside potential, as it wouldn’t be worth anywhere near £56m based on the numbers published today.

This strong performance is due to the expansion of our partners internationally, the release of new "Slingo" games, and improvements to the Group's technology. In the second half of the Period, we have gone live with 5 new partners, including PaddyPower Betfair in Europe, and launched 4 new "Slingo" games including Slingo Fluffy Favourites.

The Company has applied for licenses in Pennsylvania and Michigan in the US and hopes to launch in these states during the first half of 2021.

The Company is confident of achieving further progress during 2021 and will provide further updates on its progress in due course.

My opinion - I’m intrigued by this company. There does seem to be something interesting here, in terms of products, contract wins, international expansion, big end markets, etc. Therefore, I think it could be worth readers investigating it in more detail, perhaps?

A key question to find out about, is how recurring or repeatable are the revenues? It mostly comes from licensing - are those one-offs, or SaaS type recurring revenues? The word recurring doesn’t appear in today’s update, so my hunch is that revenues might be one-off licence wins, because if they were recurring, the company probably would have emphasised that in this update.

Overall, I would need more precise details about the business model to get me interested further. At the moment it looks too expensive for me.

Also as mentioned in my last quick review of the company, its balance sheet looks stretched, and it needs to raise some fresh equity in my view.

A wild card is that it might become a takeover target, for one of its USA customers, possibly?

.

Zytronic (LON:ZYT)

Share price: 135p (down c.7% today, at market close)

No. shares: 16.0m

Market cap: £21.6m

I see from today’s reader comments (always a joy), that I practically had a mutiny on my hands earlier, because I gave priority to more important, more liquid stocks. So just to keep everyone happy, here’s a comment on nanocap bespoke touch screen manufacturer, Zytronic.

Zytronic plc, a leading specialist manufacturer of touch sensors, announces its audited full year results for the period ended 30 September 2020.

Zytronic gave us flash numbers for FY 09/2020 in a trading update, which I reported on here on 21 Oct 2020.

Revenue of £12.7m is as guided (down 37% on LY)

Gross margin also well down, at 20.1% (LY: 33.7%)

Despite this, it only generated a modest loss of £0.4m (LY: £3.1m) - clearly a poor result, but a modest loss in a one-off (hopefully) disrupted year, isn’t the end of the world. Note that a furlough claim helped boost profits by £0.5m (see note 5 - exceptional items)

No divi - strange given the balance sheet is groaning with cash

Net cash of £14.0m, or 65% of the market cap - so you’re really buying a pile of cash, with a business thrown in for half as much as the cash pile - which has to raise questions about what needs to be done. It sounds as if institutions might have been putting pressure on the company behind the scenes, as this is a shift in attitude (I've been telling them this for literally years) -

The Board considers that a large proportion of these cash balances are surplus to current requirements, and it may be appropriate to distribute this surplus cash by a share buy back, and will seek shareholder approval for the requisite authorities at the next general meeting.

It sounds like they've decided on that course of action, if shareholder approval is being sought.

Current trading - not bad, considering that the business is valued at not much above its cash pile -

Sales are still running at similar levels to the last quarter of last year, but even at these low levels, the actions we took to reduce staff levels have enabled us to improve gross margins to close to historic levels, and with reduced overheads produce a positive EBITDA.

On the order front we have experienced some increase in enquiries and activity levels which is encouraging, although we would not expect any material change until the pandemic is under control.

Outlook - I’m not sure about this. It seems to be putting more emphasis on covid than other companies. Which makes me wonder if there might be a deeper problem with demand, beyond covid? I don’t know, only company insiders really know that level of detail.

Whilst we are only two months into the financial year, we have adjusted our operations to the lower levels of demand as it is likely to take several months for the Coronavirus vaccines to allow a return to more normal living and then further time for our customers to operate fully and sales to return.

My main concern with Zytronic, is that it has previously said that some big projects were end of life. Therefore, reliable repeat orders which proved lucrative in the past, could be gone for good maybe?

Balance sheet - the current ratio is almost off the scale good, at 11.6 - bear in mind that I normally see anything over 1.5 as strong!

I’d say there is at least £10m in surplus cash on the balance sheet, which could safely be distributed to shareholders in one form or another. Although bear in mind that as (hopefully) revenues rise again, then that sucks in working capital. So Zytronic will need to keep back some of the cash pile to fund future working capital growth.

My opinion - if it was down to me, I’d say to institutions that are stranded by lack of liquidity, that if they want to sell up, then the company would buy them out at a 20% discount. What other options have they got?

The only problem with a share buyback to get rid of the surplus cash, is that we’re then left with an even smaller, nano market cap company, with no reason to be listed on the stock market at all. Therefore, I’m flagging de-listing risk.

If the market cap drops to say £10m, after distributing the cash via a buyback, then the upside is more nicely leveraged for people who hold on, if (and only if) the company manages to improve future trading.

Either way, I think this share looks quite a nice each way bet - underpinned by the cash pile, and something might happen in future, if trading improves.

I’ve been in contact with Zytronic management several times, over quite a few years, and always found them completely straightforward, and trustworthy. That comes across in the RNSs too - telling it how it is. Hence I have a high level of comfort that they'll do what's best for everyone involved. If you look at Director remuneration, the CEO and CFO are paid appropriately in my view. Whereas so many small companies grotesquely overpay executives. Although £81k for the Non-Exec Chairman seems steep.

For me personally, I don’t want to get involved in yet another tiny, illiquid share, unless I see it as a potential multibagger. Based on current information, it’s difficult to see ZYT multi-bagging. That said, it must be one of the safest nano caps out there, being backed two thirds by net cash, and being close to breakeven despite having just had a horrible year.

.

Porvair (LON:PRV)

Share price: 518p (down 4% today, at market close)

No. shares: 46.1m

Market cap: £238.8m

Porvair plc ("Porvair", "the Group" or "the Company"), the specialist filtration, laboratory and environmental technologies group, announces the following trading update ahead of its close period for the year ended 30 November 2020.

Let me turn the first paragraph of the RNS into bullet points, it’s just easier to read like this -

- Revenues for the year ended 30 November 2020 are expected to be 7% lower than 2019.

- Net cash at 30 November 2020 was £4.9 million (2019: £4.0 million) after capital investment of approximately £5.0 million and dividends of £2.3 million in the year.

- Adjusted operating profits are in line with management's expectations.

Generally, I’m not keen on operating profit these days, as it can be skewed by IFRS 16 effects.

Current trading - this all looks self-explanatory, if almost completely lacking in specific detail! -

As previously announced the Group's aerospace, molten metal and most industrial order books had reduced sharply through the middle of the year. Costs were adjusted and the Group will charge exceptional restructuring costs of around £2.0 million in the second half.

Since July order books have been building steadily from a lower base. The Group was consistently profitable and cash generative in the second half, and showed sequential growth between the third and fourth quarters. The economic outlook for aerospace and some industrial segments remains uncertain but orders for the first quarter of 2021 in the Laboratory division are strong. Investment in productivity, skills and new products have continued at pre-Covid levels throughout 2020.

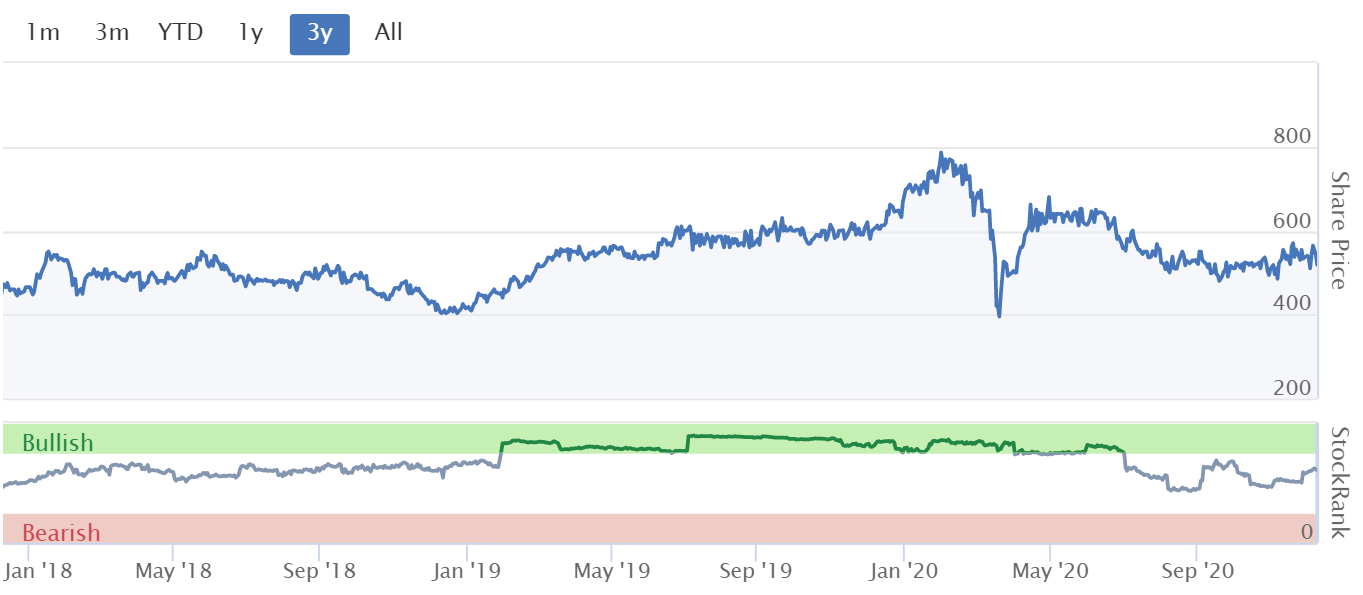

My opinion - this share has looked over-priced to me for years. The bull case is that it makes niche products with high margins, and being consumables, revenues repeat. Aerospace looks a really grotty sector to be operating in, but maybe things might look better there post-covid?

Why would I want to pay 23.5 times forward earnings for PRV, when I can buy Redde Northgate (LON:REDD) (I hold) which has a similar 10% profit margin, at about 7 times next year’s forecast earnings? Both have earnings recovery potential. Or a 1% dividend yield from PRV, compared with a 5-7% yield from REDD?

Sideways 3-year chart - sometimes this can cause a revolving door shareholder register, with stale bulls keen to exit as fast as new people come in. I think it might need some fresh news to revitalise things. We didn't get that today.

.

.

Ideagen (LON:IDEA)

Share price: 233p

No, shares: 229.5m

Market cap: 534.7m

I'm pleased to see Ideagen is raising some fresh equity - quite a lot, £48.7m in total, at 215p per share. A nice fee for Finncap too, which recently reported good results.

It says this is possibly for acquisitions, or if none complete then to reduce debt. Either way, this is clearly a good move - companies should take advantage of a buoyant share price to strengthen a weak balance sheet, with relatively modest dilution, as in this case.

Current trading - sounds reassuring -

Current trading and prospects

The Board provided an update on the Company's trading for the six months to 31 October 2020 on 12 November 2020. The Group's trading has continued to be pleasing and there has been no material change in the Company's financial performance, position or outlook since that date.

My opinion - bulls like the recurring & sticky revenues. It's good to see the balance sheet repaired with nice expensive equity, hence little dilution - ideal, and well played!

.

That's it from me today. See you in the morning.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.