Good morning! Paul & Graham are here with you today, for our usual trawl through the RNS, looking for opportunities in the small caps space.

Agenda -

Paul's Section:

Gear4music Holdings (LON:G4M) - my initial review of the final results for FY 3/2022 leads me to believe this share could be very cheap, taking a longer term view. In the short term there are obvious macro headwinds. Big changes in the balance sheet are worth noting, and not all investors will be comfortable with the large increase in inventories & bank debt. Slide deck is here.

Also, I had a quick Q&A with G4M management, with brief notes added here below.

K3 Capital (LON:K3C) - readers have asked me to review a strong trading update today. This looks an interesting, and highly profitable professional services business. If profits are sustainable at this level, then it looks cheap.

Graham's Section:

Record (LON:REC) - this currency manager is trying a new strategy of moving into fund management, after many difficult years of price compression in currency services. The strategy is already bearing fruit with large increases in revenues, margins and profits. I’m excited about the potential for the company to grow over time and become a larger, much more profitable business. It has built up an excellent reputation over many years, so I rate its chances of success highly.

Quick comments from Graham -

Assetco (LON:ASTO) [No section below] - As recently as February 2020, the purpose of this company was to provide “management and resources to the fire and emergency services in the Middle East”. That business suffered a revenue collapse, but was cash-rich, and so the company changed strategy. It is now involved in “acquiring, managing, and operating asset and wealth management activities and interests”.

It is led by three former top executives at Standard Life Aberdeen, including the co-founder of Aberdeen Asset Management. Today it announces the debt-funded, conditional acquisition of SVM Asset Management for £9 million. SVM is a well-known and long-established but, in an industry context, small-scale fund manager based in Edinburgh. This appears to be a sensible acquisition, both strategically and in terms of the purchase price.

HSS Hire (LON:HSS) [No section below] - this equipment hire business reports Q2 revenue up 10% versus 2021. Adjusted earnings are still set to be in line with expectations. As noted in previous SCVR, this company’s balance sheet has improved and strategy has evolved, meaning it is less of a basket case than it was when private equity dumped it on the market. Risk/reward has improved with net debt of just £45m as of the most recent year-end.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Gear4music Holdings (LON:G4M)

175p (before market open)

Market cap £37m

FYI, I’m not currently holding this share (as mentioned in April here), but want to buy back in at some point (subject to newsflow, and funds being available - which is a bit of an issue right now!)

Gear4music (Holdings) plc, ("Gear4music" or "the Group") (LSE: G4M), the largest UK based online retailer of musical instruments and music equipment, today announces its financial results for the year ended 31 March 2022.

PR headline -

"Good progress following an exceptional prior year"

These are audited accounts, and are in line with broker consensus -

Revenues £147.6m (as indicated in the April trading update)

Profit before tax £5.0m (no adjustments)

EPS (diluted for share options) 17.3p

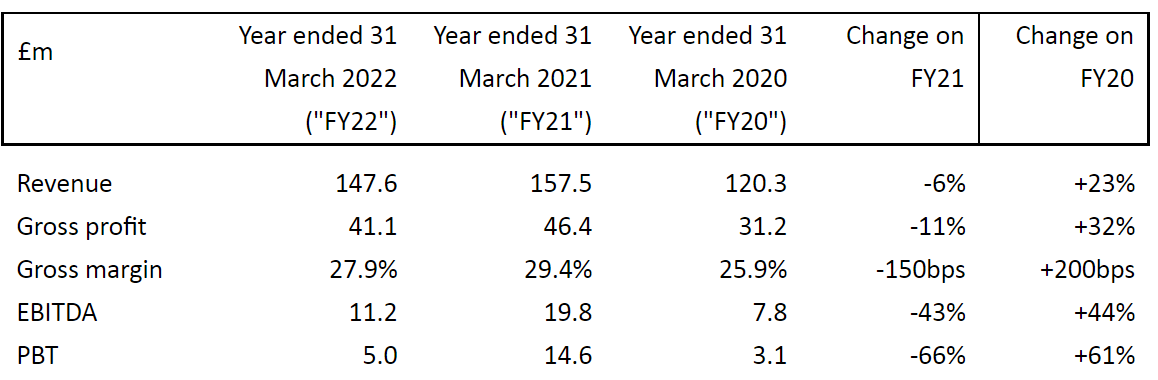

This table shows the huge boost last year got from the pandemic. Although note revenue, gross margin, and profit are all ahead of the pre-pandemic comparison year of FY 3/2020 -

.

Recovery in eCommerce shares - this is a key investing theme for 2022/3, for me.

I reckon a lot of eCommerce shares might have sold off too much, because the market has currently de-rated them as ex-growth. That’s happened because more normal trading now looks weak against last year, when the figures were hugely boosted by the pandemic lockdowns.

Yet many eCommerce businesses are still showing good 2-year growth rates. If growth resumes from now (when the last pandemic-boosted prior year comparatives disappear) to a more structural, long-term growth rate, of maybe 10-20% p.a., then I reckon many shares in this eCommerce sector could be tremendous bargains, and re-rate upwards, once people realise some of them actually still are growth companies.

There’s also potential help from freight & carriage (in & out) costs, and supply chains gradually normalising over time, although maybe that’s more likely to be 2023, rather than 2022? (judging from what other companies have been saying).

The key point being that there’s a continuing shift to online, in many areas of life, not just retailing. But the pandemic pulled forward a lot of that growth into year 1, making year 2 look soft in comparison, as physical competition re-opened. Now year 3 should compare more favourably against year 2. That’s the opportunity for good quality online businesses to see their shares re-rate to growth companies again. Maybe! It’s only a theory at this stage.

On the downside, we all know about inflationary pressures, and more cautious consumer demand, so that’s already in the price I would suggest, given calamitous share price falls across the whole sector.

It’s time to look for bargains, I reckon, if you’re brave. Or sit on the sidelines, and pay more once there’s more economic certainty. It’s a tough call. Or do a mixture of the two, with small initial purchases maybe? That’s my preferred method when unsure - dip my toe in, to get me focused on a share, then either build as confidence grows, or ditch them if it was a mistake.

Key points from FY 3/2022 results -

I’ll go through the figures & commentary again, in more detail, later. Also I have a call with management at 10 am, so have jotted down some questions.

On my first skim, these points jumped out at me -

Pretty solid results in the circumstances - the company remains profitable at £5.0m PBT, and doesn’t massage the numbers with adjustments.

Gross margin - of 27.9% looks low, and is down on (exceptional) last year, but up on pre-pandemic. The commentary makes an important point - that G4M’s prudent accounting policy means it absorbs outbound carriage costs into the gross margin. Adjusting this out boosts the gross margin to a more decent 34.9%. Also, when demand is soft, due to macro factors, having a lowish gross margin, and mostly variable costs (labour & marketing), is a good thing!

As I’ve mentioned before, yes the gross margin is quite low, but the average order value is decent at £125. Therefore the cash margin per order is £35 - which is not bad. Factor in lower returns than fashion businesses, and it’s a viable business model.

Outlook - sounds sensibly cautious, given macro factors -

As a result of Brexit, Covid, and now the war in Ukraine, the general outlook for many retailers during 2022 remains challenging and difficult to predict, with increasing product and overhead costs forcing up product retail prices and potentially impacting profits.

To help combat these challenges, we have a strong pipeline of growth orientated projects launching in FY23, and we will retain a sharp focus on productivity, efficiency and overhead cost control.

Inflationary pressures and weaker consumer confidence are likely to constrain growth in profitability in the short term. However, with the strategies and actions we are taking, along with our strong balance sheet and significant working capital headroom, we believe we remain well positioned to take market share and are confident in our medium and longer-term profitable growth strategy.

Growth projects sound interesting, and include -

AV.com being launched in Europe, after “successful UK launch” (this was a recent acquisition) - entered home audio/visual market

New range of own-brand premium products, with worldwide distribution planned.

Secondhand platform for musical instruments to be traded in.

Additional European warehouses now open, so should be scope for a resumption of growth in the EU, now delivery coverage is improved. A key advantage, is stock is now imported directly into the EU, rather than coming via the UK.

Current trading - sounds OK -

Trading in line with consensus market expectations for FY23

Balance sheet - some big changes here.

NTAV looks sound, at £28.7m - so the market cap of £37m is now strongly asset backed. This includes £8.8m of freehold property, which is a big plus for investors, as it reduces risk (banks are usually happy to lend against freeholds, and they appreciate in value long-term, especially when inflation takes hold).

The big moves are increased inventories, now up to a very high £45.5m. The company explains this as being a deliberate strategy, to get round supply chain problems. That makes sense to me.

The commentary points out that being heavily stocked up now, is presenting margin opportunities (i.e. higher inflation means raised prices, hence higher margins on existing stock bought cheaper).

Working capital is very healthy, with £53.3m in current assets (mainly inventories), and £17.4m in current liabilities, a very healthy surplus of £35.9m. This is a current ratio of 3.06, very healthy indeed.

However, remember that the bank debt is further down the balance sheet, with £28.0m borrowings in non-current liabilities. So make no mistake, the business is now dependent on bank financing. Not all investors will be comfortable with that. I am, because about a third of the bank debt is covered by freehold property, and the large inventories could be run down somewhat to generate cash and reduce (or even eliminate) bank debt at any time it might be required. There’s a lot of flexibility here, which I like.

Bank debt - a new facility of £35m was set up quite recently, which has been used to finance the higher inventories, and some acquisitions. Maybe the timing wasn’t great, given the economic slowdown now.

Going concern note - there’s some key information (positives) in here, which reassures me. Going concern notes are vitally important, and all investors should home in on them & read carefully, given current macro problems -

In FY22 the Group secured a £35m three-year committed Revolving Credit Facility with its bankers, HSBC, to make acquisitions and invest in stock for precautionary reasons during a period of potential supply chain disruption, and early in a period of inflationary cost price increases, putting the Group in a strong competitive position heading in to FY23.

The Directors have considered the Group's position and prospects in the period to 31 March 2023 based on its offering in the UK and improved proposition in Europe and concluded that potential growth rates remain strong.

There is a diverse supply chain with no key dependencies.

The Group's policy is to ensure that it has sufficient facilities to cover its future funding requirements. At 31 March 2022 the Group had net debt of £24.2m (31 March 2021: net cash of £2.7m), with £3.9m cash (31 March 2021: £6.2m cash), with a good and appropriate level of headroom that has been factored into the Directors going concern assessment.

The Group has conducted various budget flexes principally on a reduction in revenue, and performed a reverse stress test. There is no plausible scenario where the Group breaches its covenants, re-affirming the assessment of the Group as a going concern.

To reiterate a point I made above, as a lowish margin business, with variable costs, G4M should not be under threat of insolvency, even if demand drops a lot. It could de-stock, and slash marketing spend to survive, for example, if things really fell off a cliff. Modest fixed costs are a big advantage of eCommerce businesses, which is another reason I now really like this sector, which I see as irrationally cheap right now.

Cashflow statement - reflects the big balance sheet changes, so bank debt has shot up, which has been used to finance acquisitions, and a large increase in inventories. You’re either comfortable with that, or you’re not - I can see both points of view. Risk averse investors might not be happy, but for the reasons explained above, I’m fine with it.

Competition -

The competitive retail landscape in musical instruments and equipment is seeing a continued channel shift to online, albeit understandably at lower online penetration levels than during lockdowns. We expect the current challenging economic environment will add further pressure to less agile competitors already struggling post-Covid, thereby allowing us to take further market share. This, in turn, may present future growth opportunities for the Group.

My opinion - I need to re-read the results more thoroughly, and I’ve also got a call with management at 10 am, so am frantically trying to finish this section and think up some clever questions, so I don’t sound a muppet when speaking to them!

My initial impression now, is that this share looks really cheap, if you take a long-term investing perspective. It’s still a growth company, with plenty of good stuff in the pipeline.

I like the low operational gearing, and soft prior year comps it’s now up against, which makes a disastrous profit warning very unlikely, even if demand does fall a fair bit, which is possible of course.

Would I buy it at £100m market cap? No. But the market cap is only £37m. That’s ridiculous I think, taking a 2-3 year view, I reckon this could be 2-3 times the current price,with patience, and the fortitude to continue riding out this current bear market. There’s a ton of cash on the sidelines remember, so if we wait for happier days, then the price might have already taken off.

I’ll definitely be buying back in here, but need to find some cash first!

EDIT:

Q&A with management

This is the rough gist (from memory) of some questions I was able to ask mgt this morning -

Raising prices - yes prices are going up, a lot of it is automated. Have high inventories, so well positioned. Inflation is actually helping raise the average order value, which helps dilute carriage & marketing costs. So some advantages to higher inflation.

Supply chain - is improving now.

Wage inflation - is it difficult to attract & retain staff? Didn't say much in reply, but said yes we're having to pay people more, and given the exceptional year during the pandemic, that is the right thing to do. Pandemic boost gave the funding to considerably expand the team.

Distribution - I was surprised carriage costs fell, from 7.3% LY to 7.0% TY. How come? Product goes direct to 4 distribution centres (DCs) in EU & 1 in UK. Local fulfilment in Europe is important - speed, and keeps carriage costs down if it's within the same country. More expensive if dispatched from another country, even within the EU. Works well with smaller, country-specific DCs, different model to competitors (e.g. Thomann distributes from one large DC in Germany). Also gives competitive advantage with faster delivery, better customer service.

Customer returns rate - is only 5.5%. And lower still for own brand. Customer pretty much know what they've ordered. No issues with fashion, not perishable.

Online marketing costs - google & others seem to be price gouging online businesses - a problem for G4M? Very careful on marketing spend, to target & measure against results. Expert digital marketing team. Profitable from first order: cost of acquisition is £14, profit on first order is £33.

Brexit - G4M has its own distribution within the EU, so see opportunities for growth there. Is it easier to compete in the UK due to Brexit border friction for EU competitors selling into the UK? Some initial difficulties with Brexit, but companies are using a scheme called One Stop Shop, which is smoothing things over somewhat.

Growth initiatives - we're excited about AV.com (recent acquisition). New brand "G4M" for more premium, own brand products, will be higher margin, and looking at global distribution, including wholesale. It's next step in company's growth. We're not interested in sitting still, it's all about growing, and we want to be one of the world's largest musical companies. That's why we put in place the bank facility, so we could stock up to ease supply chain issues, and make some good acquisitions. Net debt is reducing now, as are inventories, as planned

Pandemic impact - presumably you're now coming up against softer comparatives, as the prior year pandemic boost washes through. Yes, from round about now the comps get easier. Still some pandemic boost in H1 LY, but H2 this year is up against softer comps.

Product categories - live gigs are back now, are you seeing boost from that? Yes, product categories selling best have switched around, with the big boost from playing at home in pandemic, to now seeing products for live playing (e.g. amplifiers) now taking up the slack. Very much as we expected.

Secondhand platform - how will this work? A lot of work has gone into this behind the scenes, will be launched later this year. Allows customers to sell secondhand musical equipment back to us. Has to be in perfect working order. Utilising the existing returns infrastructure, it's picked up from the customer in the same way, checked, then offered for sale. Good margins, and we'll only buy known bestsellers.

How are investors & analysts reacting to the results/outlook? Brokers seem pretty positive about the future.

My opinion - I learn a bit more about businesses each time they report, and it's great to have the opportunity to talk to management as well. Our time constraints & breadth of coverage mean that I only talk to mgt at the companies I think are the most interesting, and where I understand the sector.

The CEO & CFO at G4M are not at all flashy, they're quiet and measured in style, so I always get the feeling that everything the company does is well thought-through, not impulsive - clearly a good thing. There's no denying the ambition of the business, they want to grow this into a big business, and are focused on the next 5-10 years.

It's heavily IT-driven too, with an amazing 90 in-house software developers, plus a big marketing team.

As mentioned above, for patient investors who can cope with macro uncertainty & volatile markets, I do think sub-200p could be a very good long-term entry point for G4M. Nobody knows though, so as always, DYOR.

There have been 2 great bull runs for G4M shares in the past. I reckon we could get a third, it's the timing that is unknown. Meanwhile, on value metrics it stacks up - with the current PER only about 10. Hence nothing in there for planned growth. I think that's attractive.

It's astonishing to see the share price right back down to where it started, on listing 7 years ago. Yet the business is multiples the size, profitable, and international now. Yet the same share price! There's no even been much dilution: from 18m to 21m shares in issue over that 7 years. Mgt has sold a lot, but the CEO still owns almost 23%, so plenty of skin in the game.

.

.

K3 Capital (LON:K3C)

258p (up 10% at 11:03)

Market cap £190m

K3 (AIM: K3C), a multi-disciplinary and complementary group providing specialist advisory services to SMEs, incorporating Business and Company Sales, Restructuring and Insolvency and Tax Advisory services, announces an update on trading for its financial year ended 31st May 2022.

PR headline -

Revenue and EBITDA expected to be comfortably ahead of market expectations

Jack used to cover this company, so I’m re-acquainting myself with it today.

Headline numbers are certainly eye-catchingly good -

*Market expectation based upon Numis research note of May 22 (£63.5m revenue and £18.2m EBITDA)

It doesn’t provide the split of EBITDA by division in this update, but the last interims do, and show that EBITDA margins are highest (both around 50% of revenues!) at the M&A, and Tax divisions.

Restructuring has a still good, but lower 18% EBITDA margin.

The M&A division looks the profits powerhouse, making £5.0m EBITDA in H1, 48% of the group total. So you could argue that profits might be vulnerable to a slowdown in M&A.

There again, restructuring is counter-cyclical, so could offset that maybe? I don’t know the business well enough to say, but it’s clearly doing very lucrative work, which makes me wonder how it manages the split of the loot between staff & shareholders, which is often an issue with professional services businesses.

Readers who know the company better than me might be able to answer some of these queries. I’m just doing a quick review of the figures.

Balance sheet - the company calls it “robust” with £12.0m in net cash. Although on checking the last published balance sheet (interims, as at 30 Nov 2021), it only had NTAV of £7.9m, which is adequate for a people business (negligible fixed assets), but not what I would call strong.

Outlook - I was worried that M&A could be a problem area in an economic slowdown, but the pipeline sounds good -

"We are continuing to demonstrate over-delivery against market expectations, highlighting the resilience of our diverse business model. Against a backdrop of wider macro-economic challenges, our growing base of SMEs turn to us for essential services throughout their business journeys. Whilst we are seeing a growing demand for Restructuring services as SMEs navigate economic headwinds and unwinding of covid Government support, the opportunity across Business Sales and Tax is buoyant as we grow our footprint and apply our specialist skills. My thanks must go to all our employees for their dedication and hard work in delivering these results.

"We anticipate another year of growth across all divisions, supplemented with an attractive pipeline of M&A opportunities."

Valuation - last night’s numbers show a value share here - low PER, and great dividend yield (although negligible asset backing -

The big question is whether bumper profits can be maintained?

I don’t have a view on that, and can’t access any research (Numis - enough said!).

My opinion - I can see why several readers like the look of this - the figures seem highly impressive.

Also, management seem to have made skilled acquisitions, without constant dilution. The share count was flat at 42m for 5 years, then jumped to 70m in 2021, so it looks like there has only been one fundraising since listing in 2017, yet it has achieved massive growth in profits and EPS recently. If mgt can repeat that trick with further acquisitions, then this could get a lot more interesting.

With some counter-cyclical work (e.g. restructuring division), and a good pipeline in the more cyclical M&A side, then profits might prove resilient, or they might not, who knows?

The valuation has dropped by about a third this year, presumably as the market discounts a slowdown in M&A if we go into a recession? That’s flattering the market by assuming it’s rational of course, which it isn’t necessarily, especially at the moment, where selling is often led by momentum and fear.

Given the disconnect between this sparkling update today, and the drop in share price this year, then I imagine this share would be a comfortable hold, or even one to top-up maybe? That’s providing you don’t expect profits to nosedive in future.

Looking at the long-term chart, something seems to have gone wrong from 2018-19, so it would be worth seeing what caused that, and if it could happen again?

.

.

Graham’s Section:

Record (LON:REC)

This is a currency manager that remains under the stewardship of its founder Neil Record, who first started it back in 1983, and who still owns 7% of the company.

I heard him give a lecture about returns in the currency markets quite a long time ago, and didn’t forget the name.

I even ended up buying a few shares in REC back in early 2018, but didn’t have the conviction to stay with it for the long-term. So I missed out on the share price rally which did eventually occur, but not until 2021!

In recent months, the share price has been softening again:

Today’s results are for FY March 2022, and show that 2021 was indeed a very successful year:

· Revenue +38% to £35m

· PBT +76% to £10.9m

The operating margin improves to 31% (from 24%), and dividends are massively boosted.

Why so successful?

For most of the time that I’ve been studying this company, it has been struggling to raise AUM and struggling to charge its clients properly, as currency services become cheaper and commoditised.

After all, if you’re a large corporation who needs hedging services, there is no shortage of banks and smaller firms who will line up to assist you. The forex market is incredibly efficient, and always changing to become even more efficient. It’s no easy task for a small company in this market to remain fresh, innovative and competitive!

Record allowed its basic fees to erode, but hoped to make up the loss with performance bonuses. This didn’t work too well.

More recently, it has branched out into new products and is, according to the new CEO, moving “from a pure currency management specialist to having a broader offering in the alternative asset management space”.

In her own words:

Whilst our core skills in currency and derivatives will continue to provide an important and robust source of hedging revenue, our focus on innovating and collaborating on higher revenue-margin products will continue to increase our profitability, as evidenced this year by the increase in our operating margin.

In my words: Record is now looking to become a fund manager with currency expertise.

While that’s easier said than done, I am inclined to believe that this is the right move for the company: it has the credibility to move in this direction, it will already have many of the right skills, and from an economic point of view, it makes far more sense than continuing to suffer the margin erosion in currency services.

You can find some details about Record’s EM Sustainable Finance Fund here. According to the FT, the fund currently has a size of £909 million, with an ongoing charge of 0.82% (so you can start to guess at the prospective revenue from this product!). The objective is straightforward enough: “to achieve capital gains over a medium to long term time horizon.”

Note that Record’s AUME (assets under management equivalent) only increased by 4% this year, but management fees increased by a staggering 37%. The margins on fund management are vastly greater than the margins on currency management. So I’m not sure if the comparison of AUME to prior years is even worthwhile at this point, since we are comparing apples to oranges.

Neil Record says this is “the start of a new chapter in Record’s history”. I’ve added the bolding below:

We plan to diversify into areas where specialist skills are well rewarded; where investor appetite is high, and where our existing expertise can be put to use… I am pleased to report that we plan to launch further funds with a variety of different investor appetites and asset classes.

Financial performance

For as long as I’ve been watching it, this has always been a cash-rich, cash-generative company which paid out generously to shareholders. That remains the case today. Cash inflows from operating activities for FY 2022 were £11.4 million.

Net assets finished the year at £26 million, or about £20 million even if you deduct the value of all non-current assets.

The dividend policy is aimed at 70%-90% of annual earnings for the ordinary dividend, and a special dividend if the company can afford it! Very few companies are able and willing to do this - either because their earnings are non-cash, or because they need to reinvest whatever cash they generate!

Outlook

Neil Record is positive on the outlook for the company he founded, but very worried about the wider economic outlook.

As I have already mentioned, we are witnessing a fundamental change in the business, which I believe has the potential to transform for the better Record's scale and resilience within the next few years. This leaves me feeling very optimistic for the firm.

CEO Leslie Hill writes:

I believe we can combine the flexibility and agility of a small business - as is shown by our Tech transformation, with the scale and credibility of a much larger business, as is demonstrated by our asset base, our growing global reach and the scalability of our product and service offering.

My view

I’ve allowed myself to get excited about this change in Record’s strategy. Now I’m going to have to go and reflect on all the reasons why it might not work!

But a successful fund management company does great things for its shareholders (assuming that it does a decent job for its customers, of course!).

The shares are up 12% this morning, leaving the company with a market cap of £147 million. Given the potential of the new strategy, and the growth already achieved in FY 2022, this looks to me like an unflattering valuation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.