Good morning! It's Paul & Graham again today - the new normal, now Jack has moved on to a job in the city. Hopefully he'll let us know how he's getting on!

Grim market conditions continue for now, but we're finding bargains almost on a daily basis, for your watch lists, or brave purchases that could be the multi-baggers of the future. It's the work done now, which I think will lay the foundations for the next period of out-performance. The only thing we don't know, is the timing.

Mello show tomorrow - this one's free, and the content looks interesting, from 12:30. I tend to put on my bluetooth headphones, and then wander around doing other things whilst listening to webinars, which is a good use of time.

Agenda -

Paul's Section:

Vertu Motors (LON:VTU) (£189m) (I hold) - strong trading continues, although the company is coy about raising guidance again, due to consumer uncertainty. It says supply of new cars is expected to gradually improve in the coming months. Exceptionally cheap value share, strongly asset backed too. CEO previously said sector consolidation is inevitable, so prospect of a takeover bid looks high.

Micro Focus International (LON:MCRO) - amongst the top fallers today, it's rapidly approaching small cap territory from the wrong direction. The ultra-low PER indicates that something is badly wrong, which it is - a $3.65bn debt mountain. This looks precarious, as a result. The business itself looks decent, but equity seems at risk of being engulfed by the higher-ranking debt holders. A special situation, only for experts who know what they're doing, I would say.

Graham's Section:

Churchill China (LON:CHH) (£154m) - This year’s AGM statement guides for year-on-year improvement in 2022, with the company experiencing record demand. The trends in hospitality remain positive and this bodes well for Churchill. Against that, I have some concerns that inflation may affect the company’s margins and profitability in the medium-term. Real profitability may not reach pre-pandemic levels until this situation has normalised.

System1 (LON:SYS1) (£36m) - this advertising consultancy announces that future distributions will be made in the form of share buybacks or tender offers. While this won’t be to everybody’s taste, I think that it signals intelligent leadership. When combined with the announcement of a one-off tender offer, I think this company is showing excellent shareholder orientation. If it can continue to raise the quality of its earnings - which is uncertain - then shareholders should do very well with this one.

UP Global Sourcing Holdings (LON:UPGS) (£98m) [No section below] - This company owns some consumer brands including Beldray, Dreamtime and Salter. Today’s minor announcement lets us know that the company has bought the Salter.com domain, and will be giving beldray.com an overhaul. UPGS has traditionally been a supplier to the retail sector, but has aspirations to build a strong direct-to-consumer business, including sales on Amazon and eBay. The questionable pricing power of the company’s brands is potentially priced in at this market cap.

Iqe (LON:IQE) (£283m) [No section below] - this company loves to make announcements via RNS. Last week, it entered the news feed with the declaration that it was committed to “Net Zero” and carbon neutrality. This week, it lets us know that it has signed a multi-year agreement with a customer to provide its semiconductor wafers for a variety of applications.

This is not a new customer for IQE, and there is no indication as to the impact that the deal will have on IQE’s revenues or profits. One thing I am certain about: if somebody drops a hat at IQE headquarters next week, we are likely to hear about it via RNS.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Vertu Motors (LON:VTU) (I hold)

53p (yesterday’s closing price)

Market cap £187m

I reported quite thoroughly on the FY 2/2022 results & last trading update here on 11 May 2022, for background. This showed that bonanza profitability from last year had continued in March & April 2022 (due to a shortage of new cars, causing sale of used cars to be highly profitable).

On to today’s news.

Continuing constrained supply of new vehicles (this is good news for car dealers, as it keeps prices & margins high!)

Margins have remained strong as a result (for new vehicles)

Used cars also supply constrained.

Decline in used car volumes sold, as expected, due to strong comparative (pent-up demand in 2021 when lockdown ended).

Gross margin is strong on used cars, higher per unit profit than prior year May comparative.

Used car prices have stabilised (after a large increase last year).

Aftersales (e.g. servicing, warranty work) - doing well (high margins).

Parts & accident repair departments - the group “continues to make progress”.

Outlook - unclear. New car supply expected to “improve gradually in the months ahead”

Profit guidance - “strong start” to FY 2/2023, but “premature” to change full year expectations.

Strategy -

Management remains focused on the delivery of operational excellence around cost, conversion and customer experience. In addition, the Group continues to evaluate and execute acquisition opportunities as it seeks to deliver its core strategic objective of growth.

My opinion - the context here is that pre-pandemic, Vertu achieved c.5p adj EPS. In the first pandemic year, FY 2/2021, EPS rose slightly to 5.27p, thanks to Govt support measures, but hindered by lockdowns. Then in FY 2/2022 it had an absolute bonanza, as used car prices shot up, achieving a one-off 17.92p EPS.

Therefore, we all know profits will come back down again, and that’s allowed for in the share price of only 53p (historic PER of 3!)

Consensus forecasts are for EPS to more than halve from last year’s peak, to c.7.5p this year, and slightly less next year.

Reading between the lines today, it seems that the current year is probably tracking ahead of that, but they’re holding back on raising forecasts due to uncertainty, that’s how I read it anyway, Hence risk, as they say, to current guidance looks to be on the upside, which is very pleasing - I’d say the opposite is true for so many current forecasts. That should make it safer to buy & hold Vertu shares, since we probably won’t see a profit warning, given that there looks to already be some slack in the forecasts.

(EDIT: Liberum has just updated, saying its forecast of 7.6p for FY 2/2023 is "cautiously set", which I find reassuring. End of edit).

That means we have a PER of only 7.1, at 53p per share, if we assume 7.5p EPS is probably fairly safe for this year & next year.

Asset backing is another key attraction of VTU shares - last time I calculated NTAV as about 63p (the company works it out differently, and said NTAV was 67p), so the current share price of 53p applies an unjustified discount to the assets, which are generating good profits, so why would they be discounted? It doesn't make sense to me.

NTAV will have gone up further too, since Mar & Apr 2022 generated £19.1m profit (as reported on 11 May 2022), take off say 25% tax, and that’s earnings of c.£14m, which would boost NTAV further by about another 4p per share. So I reckon NTAV is now more like 67-71p. Remember that’s mainly freehold property, which is probably worth at least book value, maybe more?

Note that VTU is reducing the share count on a daily basis, with buybacks, which will enhance EPS and NTAV per share further.

Overall then, we’ve got -

- a still highly profitable business,

- NTAV now about 30% higher than the share price,

- reasonably priced, even allowing for profits more than halving, and

- a takeover bid could come any time as the sector is ripe for consolidation.

That’s a fantastic set of factors, and makes this a highly attractive value share, in my view, even allowing for a consumer slowdown.

Note the StockRank looks jammed on maximum too (below the share price chart here, for anyone not aware) -

.

Micro Focus International (LON:MCRO)

290p (down 19% at 10:01)

Market cap £964m

This is a large software group, which I spotted on the top fallers list today, down 19%, and looking like it’s going to be knocking on the door of the SCVR for inclusion, if the share price drops much further.

I recalled that MCRO had a weak balance sheet, so wanted to check that, in case it does start to attract interest around here.

Interim results are out today, for the 6 months to 30 April 2022.

H1 revenue is down 6.8% on a like-for-like basis, to $1.3bn

Adj EBITDA is down 12% to $449m

Operating profit was only £35m, the main reason for this being so far below EBITDA is due to the $413m amortisation charge of intangibles (non-cash), and the huge $129m interest charge for just 6 months - so clearly debt is the big issue.

H1 adj EPS is 57p, with consensus FY 10/2022 forecast at 120p - the company says FY expectations are unchanged.

PER - at 290p per share, with c.120p EPS for this year expected, the PER is just 2.4 - a big warning sign, that there’s something badly wrong with either/both future earnings, and balance sheet weakness.

Exceptional items - are positive this time, at $42m, due to a profit on disposal, whereas H1 LY saw exceptional costs of $143m.

Free cashflow looks good in H1 at $190m.

Net debt - the big issue here. It’s gigantic, at $3.65bn. This has come down from $4.2bn a year earlier, but most of the reduction seems to have come from a $364m disposal. This is nearly all interest-bearing borrowings, with only a small amount being lease liabilities. The ratio is high, at 3.7x adj EBITDA.

Balance sheet - is dominated by $3.63bn goodwill, and $3.89m other intangible assets.

NAV is $2.65bn. Writing off the intangible assets, takes NTAV to a staggering negative $(4.87)bn! Now we could be charitable, and also write off the $522m deferred tax liabilities, which are often related to intangible assets, which takes NTAV to negative $(4.35)bn.

Another argument is that intangible assets at software companies could have some real world value.

However you look at it though, MCRO has a massive net debt pile of $3.65bn, which would take many years to repay from cashflows.

My opinion - going into an economic slowdown, and with interest rates rising, MCRO looks to be in a potentially precarious position, due to its wildly excessive debt pile, and one of the worst balance sheets I’ve ever seen. This is precisely the type of situation we need to be steering clear of, at the current stage of the economic cycle.

A key research issue would be to look in detail at the terms of the debt, in particular when it falls due for repayment, and the covenants which could trigger immediate repayment if breached. Also the interest rate is important - fixed or floating?

I’m worried that readers might look at the PER of 2.4, think it’s a bargain, and buy a share that is very high risk, due to its excessive borrowings, and extremely weak balance sheet.

What many relatively new investors don’t understand is that debt can easily become toxic in a downturn. Lenders can force companies to raise fresh equity, causing (sometimes heavy) dilution. If existing shareholders don’t want to stand their corner in an equity fundraise, then any fundraising (if one happens at all) can be at a huge discount, thus diluting existing shareholders to almost nothing sometimes. You’re then forced to either accept you’ve lost your money, or go back into the market to buy loads more shares in a company that’s already been a disaster - a horrible choice.

If things get even worse than this, then insolvency looms. As we saw with McColls recently, once equity is worth very little, then it’s the debt holders who call the shots. That’s because shares rank behind debt in company law. Therefore, in such situations, equity is often wiped out, along with unsecured creditors too usually (the trade creditors), leaving the remaining assets to be sold (often the business as a going concern, without the debt), with the spoils being taken first by the administrators & preferential creditors, then the bank getting what’s left. In insolvencies, there’s rarely anything for unsecured creditors, although MCLS was unusual in that they did get a partial payment I believe. There’s hardly ever anything remaining for shareholders, who are last in the queue.

Could MCRO end up in that situation? I don’t know, but the huge debt position means that investors need to be really careful before committing funds here. This is really a special situation now, where debt reduction is the no.1 priority. That could involve selling off the best parts of the business.

Thinking about a bullish case, for balance. Software companies can have considerable hidden value to an acquirer, since customers are often very long-term, and captive, since the software is often business-critical. Therefore the software company gets a reliable, recurring, and high margin stream of maintenance & support revenues. Plus there are cross-selling opportunities often perceived by companies which launch takeover bids at apparently very high prices - e.g. the recent bid for EMIS (LON:EMIS) looked a full price. Other apparent basket case software companies have attracted bids recently - e.g. Proactis (PHD), and Tungsten (TUNG) - both serial disappointers, which looked doomed to eventual failure. Yet they were sold in takeovers.

MCRO is now c.£1bn equity, and c.$3.65bn debt. So if the situation improves, and debt reduces, then the benefit could flow through to equity, giving a geared favourable outcome for shareholders. Equally, if the situation deteriorates, then equity could be reduced, or even wiped out. Hence a volatile share price looks set to continue.

Overall then, MCRO looks too high risk for me. In a deteriorating economy, it could attract the attention of short sellers too. It’s very high risk, and suitable only for experienced special situations investors, in my view.

Forget the high dividend yield, as divis are clearly not sustainable.

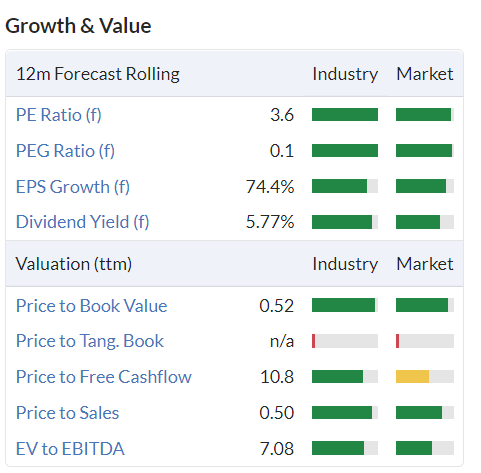

Indeed this is a situation where the apparently great value scores are rendered null & void by the debt mountain -

.

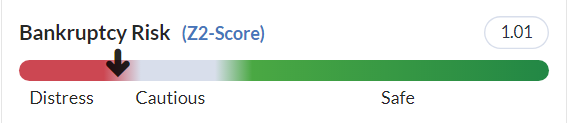

At times like this, checking the Z-Score (statistically proven measure of bankruptcy risk) is absolutely vital. Although my manual assessment of the balance sheet suggests a far worse position of financial distress than the Z-score indicates -

.

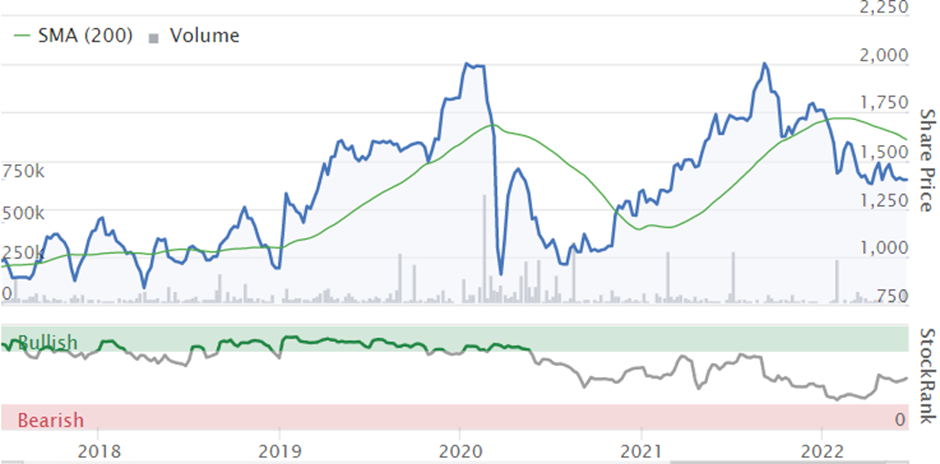

Clearly big problems emerged, well before the pandemic -

.

Therefore, as you might have guessed, it's a thumbs down from me for MCRO.

Graham’s Section:

Churchill China (LON:CHH)

Market cap: £154 million

I’ve always liked writing about this ceramics company: it’s a family business with an impressive history stretching back a few decades. It hasn’t made a loss since the last millennium, has barely issued any stock in all that time, and normally grinds out an acceptable return on capital for shareholders.

As previously reported in the SCVR, Churchill has already reported that trading has returned to pre-pandemic levels. The hospitality industry is Churchill’s end-market, and so the level of demand is always going to be a little unpredictable.

Fortunately, sales in the most recent H2 period were ahead of the comparable period in 2019 – before adjusting for inflation. If you adjust for inflation then it becomes debatable! But the point is that trading has mostly, if not fully, recovered. This is reflected in the share price performance:

The AGM statement today is the first update since April. The Chairman says:

"In our Preliminary Results, announced on 21 April 2022, we advised that we were experiencing record demand across our geographic markets. I am pleased to report that this demand has continued and our order book remains healthy. We remain confident in our ability to deliver an improved year on year performance in 2022.

My view

It’s all systems go at Churchill, and hopefully the trends in hospitality will remain positive, giving the company a sustained tailwind.

However, like many companies, this one won’t be immune to the effects of inflation. As a manufacturer we can expect some margin pressures and some volatility in results. The most recent results statement noted the following (I have added the bold):

The sharp increase in production output required to satisfy demand, together with elevated levels of input price inflation, have in the short term constrained the improvement in overall business performance…

the inflationary pressures more generally evident within the global economy have […] impacted both our material and energy costs. While we have ultimately raised our prices to reflect these rises we have absorbed some of the increases in the short term.

As I’m very worried about inflation in the medium-term, I would have concerns that the real profitability at Churchill might lag the results of 2019 for some time, even if nominal sales have improved and even exceeded those levels.

City forecasts share this caution, at least for this year and next:

This company is rarely “on sale”, and building a stake in it has nearly always involved paying high multiples. That remains the case today.

System1 (LON:SYS1)

Market cap: £36m (+4%)

I loved this advertising consultancy when it was known as “Brainjuicer”. It had a quirky website that was more like watching a cartoon than visiting the homepage of a listed company!

Unfortunately, the share price overheated, when a temporary rush of sales and profits in 2017 was wrongly interpreted by the market. The shares are still down over 70% from the high that was achieved back then.

More recently, it has changed tack and focused on more automated marketing solutions, with less focus on the lumpy, unpredictable, labour-intensive revenues that have traditionally made up the bulk of its revenues.

It also made it onto Ed’s 2022 New Year NAPS. The StockRank is terrific:

Today we get an update on the company’s distribution policy:

…the Board has decided to pay annual distributions to shareholders by way of on market share buyback or tender offer, rather than by way of a dividend. The Board has concluded that the distribution policy will be progressive, taking into account underlying business performance. It is expected that the absolute level of distribution for the year end 31 March 2023 will be between 30 - 40% of through-the-cycle profit after tax.

This is music to my ears – I love buybacks! For all of the following reasons:

- There’s no tax liability for me, if I hold on to all of my shares while one of my companies carries out a buyback (of course for shares in an ISA or other tax-free wrapper, then dividends generally don’t have a tax liability, either).

- I get a bigger percentage ownership of my companies, without needing to put any more money in! This is preferable to dividends since my primary goal is to build my portfolio, not live off my dividend yield. Of course other people will have different preferences!

- The overall value of the company’s equity increases, so long as the shares have been bought back below fair value and without creating a risk of financial distress.

The last bit is what trips up many investors, and many companies. On the one hand, many companies do carry out buybacks when their shares are overpriced, and this destroys value for the remaining shareholders while also increasing the company’s financial risk.

On the other hand, the fact that many buybacks are overpriced leads many investors to be suspicious of them – perhaps overly suspicious.

I’ve just double-checked my personal portfolio. Out of the nine companies I own shares in, seven of them are engaged in buying back their own shares. I don’t believe that they are recklessly endangering shareholder interests – quite the opposite. I think they are well-managed and responsibly run companies, arguably to the point of being boring! And I’m delighted that my long-term percentage ownership in these companies is increasing while I sit back and do nothing except continue to hold my existing shares.

Let’s get back to System1. The only criticism I have of the policy just announced is that it doesn’t allow for any discretion, based on the company’s share price. Most good management teams have some idea about whether or not their company is overvalued (better than we do, at least) – and when they think their company is overvalued, it would be better if they didn’t carry out buybacks at that time. So I would prefer to see a condition that buybacks will be subject to market conditions.

Anyway, there is yet more pleasant news to be found in today’s announcement: the Board at System1 believe that “the Company has cash at levels above its through-the-cycle and near-term requirements and will therefore seek to return up to £1.5m of excess cash by way of a tender offer”.

My view – I like the strategic direction at System1, and today’s announcement gives me additional confidence in the company’s shareholder orientation. Whether or not it will achieve the quality of earnings that it seeks is uncertain, but it still has some very attractive features for potential shareholders.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.