Good morning! It's been such a busy week, that I think today is likely to be taken at a leisurely pace.

This week's small caps podcast is here.

Agenda -

Graham's Section:

Zoo Digital (LON:ZOO) (£99m) - Excellent results from this media services company that provides services such as subtitles and localisation streaming platforms. The outlook looks positive, too, and it’s hard to imagine that it won’t hit its $100m revenue target before long. The growth in sales has finally enabled it to earn a meaningful operating profit, despite heaving spending on growth such as the leasing of a new office and international acquisitions. In a bull market for growth companies, I can imagine that the valuation here would be vastly higher than its current level.

DX (Group) (LON:DX.)(£172m) - This suspended company is still publishing trading updates and its broker continues to publish earnings forecasts. Trading is said to be ahead of expectations, and EPS forecasts are raised accordingly for FY 2022 and FY 2023. The corporate governance problem, whatever it is, has taken up the attention of Board members for a very long time now (an internal investigation started some time before July 2021). But if the costs related to it remain low, and it doesn’t derail the business of the company, then shareholders can still emerge unscathed.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Graham's Section

Zoo Digital (LON:ZOO)

- Share price: 110.5p

- Market cap: £99m

I’ve been checking the archives for this one, as it’s been a while since I covered it.

Way back in July 2018, at 94p, I guessed that the share price would have to wait a while for the company to grow into its valuation.

Here we are four years later, and the share price has risen by just under 20% over that time.

The company’s revenues have continued to grow strongly over that time, but sustained profitability has been difficult to come by.

The company highlights “adjusted EBITDA” every year. Unfortunately the EBITDA has not turned into cash, and it has had to raise money from investors several more times.

In April last year, Zoo raised a further $10.1m from shareholders.

It also had a $3.6m convertible note which was converted to 5.3 million new shares. Zoo highlights the removal of borrowings from the balance sheet, and the elimination of interest payments, but doesn’t talk about the dilution suffered by shareholders!

This Stockopedia chart shows the share count reaching 78 million in 2021, but the share count is now 88 million (up from 33 million in 2017):

And what has the company achieved, after issuing all of these shares?

Well, it has achieved huge increases in revenues, and the organic growth in FY March 2022 was 78%, bringing the figure up to $70.4m.

This is not just a Covid-related rebound, either. Revenues also grew well in the previous year (FY March 2021).

There was terrific revenue growth in particular from dubbing (170%) and media localisation (108%).

When I read that, I began to suspect Zoo’s momentum might have something to do with Squid Game, the Netflix-backed Korean TV series – and the most successful Netflix show ever.

A quick Google does indeed lead to search results talking about the momentum created by Squid Game for the likes of Zoo – see here. Zoo is expanding in places like South Korea, Turkey and India.

Squid Game 2 was announced by Netflix last month. According to what I read online, this series is subtitled in 31 languages, and dubbed in 13. This means plenty of work for companies like Zoo.

Personally, I don’t think that Zoo shareholders should be too concerned about the success or failure of the Squid Game franchise, or even of Netflix itself. What matters is the overall direction towards more globalised media consumption, and more streaming. As long as that trend continues, there will in the long-run be lots of work for Zoo to do.

Zoo talks about this in a section called “Broader market highlights”, where it gives a range of statistics to show increased media spending and increased demand for localisation services, as major media companies strive to reach international audiences. I think all of this is true.

So I don’t think any of this is a concern for Zoo and its shareholders.

The bigger concern, in my opinion, is the low profit margin historically achieved by Zoo.

Financial Review

There are a few things to discuss here, but I’ll try to be brief by using bullet points.

- Customer concentration: Zoo’s largest client (let’s call it FletNix) is responsible for 78% of its revenues. Customer concentration at this level is typically seen a risk factor, because the value of the company is wrapped up in the value of a single corporate relationship. It also affects pricing power: in negotiations, Zoo can hardly threaten to walk away from this customer!

- The overall gross margin falls to 31% from 35% as the fast-growing services such as dubbing are low-margin activities.

- Operating expenses increased by 50%.

Zoo’s financial performance over the years has been marked by its growing revenues nearly always being lost to its low margins and higher operating expenses.

For FY March 2022, there was an improvement in the sense that operating expenses, despite growing at 50%, didn’t grow quite as fast as top-line sales.

This leads to an improvement in the “Opex as a % of revenue” metric, which falls from 33% to 27%. This means that we finally get a meaningful operating profit from the company of $3.15m.

Furthermore, the company will argue that it has spent widely. For example, the proceeds from last year’s placing were spent “growing the R&D and service delivery teams, establishing regional hubs, expanding international business development, and strengthening our infrastructure”.

The company leased a new office in Sheffield, increased headcount, invested in computer equipment, and made several small international acquisitions.

Balance sheet – there are net assets of $26m, a huge improvement on last year, after the fundraisings and the operating profit. If you exclude intangibles, this falls to c. $15m. The company argues that it can fund itself from now on:

Going forward the business remains confident that it has sufficient headroom to trade for the foreseeable future, as the recent completion of a $5 million invoice discounting facility from HSBC gives us the working capital headroom for the next phase of our expansion.

Outlook sounds good:

Trading in the first quarter of FY23 has been very strong with sequential growth over FY22Q4 and significantly ahead of the equivalent period in the prior year…

Visibility through until the end of H1 indicates further significant progress towards the goal that we set in 2020 of delivering sales of $100 million. We expect H1 sales to exceed the second half of the prior year which was in turn 60% ahead of FY22H1.

My view

While I was very sceptical of the valuation back in 2018, I think that Zoo has achieved enough growth now to potentially warrant a valuation of c. £100m. This would be an expensive valuation if the company suddenly stopped growing, but it’s difficult to imagine that further growth will not be forthcoming.

FY 2023 revenues are expected to reach c. $80m, and I wouldn’t bet against Zoo hitting its $100m revenue target before long.

Additionally, we’ve just seen the company enjoy the financial benefits of operating leverage for the first time. As it grows, maybe its “cloud-based software systems” will enable more of this, and we’ll finally get some juicy profit margins.

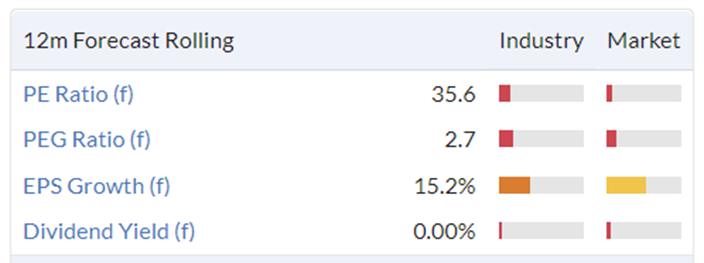

No doubt thanks to the sell-off in small-caps, the valuation here is no longer ludicrous, given its growth rate:

.

DX (Group) (LON:DX.)

- Share price: 30p (SUSPENDED)

- Market cap: £172m

A highly unusual situation at this logistics company. Its shares have been suspended for more than six months, but trading continues and is “significantly ahead of management expectations”!

That statement relates to FY July 2022, and “a further improved financial performance” is also expected for FY July 2023.

Key points:

- FY 2022 revenue +11% to £425m

- Growth in Freight (large items) at 15%, growth in Express (next-day delivery of small items) at 7%.

- Net cash of £27m.

The easing of supply chain issues is mentioned, and makes perfect sense – without functional supply chains, nothing can be delivered!

Expansion – three new depots were opened in H2, and another twelve are planned over the next two years.

Capital allocations policy – dividends and share buybacks are being considered. Again, this is very unusual for a share that is suspended for six months!

Corporate governance problem – the nature of the problem at DX has been kept secret, while it is being investigated and analysed. Whatever it is, it must be serious, given the company’s reaction.

As a reminder, the company’s auditor, Grant Thornton, resigned in February.

This seems important (from an RNS on February 4th):

Grant Thornton's stated Reasons relate to its view of the Company's governance and to executive conduct, specifically arising in connection with Grant Thornton's concerns over: (i) actual or potential breaches of law and/or regulations by the Company and/or by an entity in the DX (Group) Plc group and/or by employees; (ii) the performance of the investigation and subsequent corporate governance inquiry referred to by the Company in its announcement on 25 November 2021, and action in response to the evidence generated by that investigation and inquiry; (iii) the provision of inaccurate information, which in Grant Thornton's view did not give a full picture of the scale and seriousness of the facts referred to in (i) and (ii) above; and concerns over insufficient access to relevant information and documents, in relation to the matters being investigated by the Company.

Unfortunately, views like this from an auditor tend to make shares untouchable for most investors.

My view

Personally, I would never want to have a large position in a company with a problem like this.

The special circumstances in the case of DX are that it continues to trade, and according to the management, is trading very well and has a large net cash position!

The corporate governance investigation has only cost £1.4m so far, which is small relative to the size of the company.

The company’s broker continues to issue research notes, and has upgraded its EPS forecasts materially to 2.6 (FY 2022) and 3.4p (FY 2023). This puts the shares on a forward PE multiple of 9x, at the suspended share price (but who knows what the shares will trade at when they are unsuspended).

The late 2021 Annual Report is due to be published by the end of September, and clarity should finally be achieved by then. Whatever the problem is, it does look like shareholders still have good chances of emerging from this unscathed.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.