Good morning from Paul & Graham!

Episode 6 of my weekly SCVR summary podcast went up on Saturday lunchtime. I rambled way past time, longer than ever (hitting the 32Mb upload limit!), but it's all relevant I think. As well as reviewing the key announcements of the week, I also talk about how I'm coping with heavy losses in this brutal bear market for small caps. It's important that people talk about this, rather than bottling up the anguish.

Renold CEO interview - In case you missed it, I interviewed (over the phone) Robert Purcell, CEO of Renold (LON:RNO) on Friday, an interesting small cap I think (no position personally at the moment).

Agenda -

Paul's Section:

Facilities by ADF (LON:ADF) (I hold) (£47m) - I had a look at its last trading update over the weekend. Looks a good business, although I'm wondering if the boom in UK TV/film production might have have peaked?

Joules (LON:JOUL) (I hold) (£37m) (no section below) - confirms the weekend reports re discussions with Next (LON:NXT) . Given the market cap is currently £37m (at 33p per share), then a £15m fresh raise from Next would imply Next ending up with c.29% of the company. Sky News reckons Next is aiming for 25%, which would equate to a price of c.40p per new share to raise £15m. This would certainly be preferable to raising money at a discount from the stock market, and would address worries about Joules' solvency. Then we need a new CEO & a proper turnaround strategy. So it's early days for a recovery, and it's still risky. Very disappointing to date.

Joules, the premium British lifestyle group, provides a statement in response to recent media speculation.

Joules confirms that it is in discussions with Next Plc ("Next") about adopting its Total Platform services to support the Group's long term growth plans.

Additionally, in conjunction, Joules confirms it is in discussions with Next about a potential equity investment raising proceeds for Joules of c.GBP15 million at no less than Joules' current market price, which would result in Next becoming a strategic minority shareholder in the Group. The equity investment would be subject to approval by Joules' shareholders.

There can be no certainty these discussions will lead to any agreement. A further announcement will be made if and when appropriate.

Works co uk (LON:WRKS) (£21m) - results for FY 4/2022 are better than expected, due to reduced stock provisions. But there's a profit warning (not quantified, and no broker notes available) for FY 4/2023. Hence I'm in an information vacuum, and can't value the shares. I don't think this is a good business, so remain uninterested in this share, especially now guidance is coming down. Business rates relief was a huge boost, so with that gone, higher costs and softer consumer demand seem likely to slash the wafer thin profit margin. It's not for me. Tiny market cap though, so there could be upside if it performs better than expected in the key Xmas trading period (how likely is that though when its customers will be worrying about the utility bills?)

Graham's Section:

Mincon (LON:MCON) (£188m) - Solid results from this drilling equipment manufacturer and supplier. Revenues are up by 27%, as export values are boosted by a strong dollar and the company uses unusual shipping methods to reduce its order backlog. The decision to reduce the backlog as quickly as possible has hurt margins in the short-term but is likely to have kept customers happy and should be good for the long-term value of the businesses. Inflation is also a factor when it comes to margins being compressed; Mincon is passing on price increases to customers and this should improve margins for H2. I’m a fan of this business and its excellent track record over many years, and I’m looking forward to seeing the outcome of its “Greenhammer” project.

ECO Animal Health (LON:EAH) (£69m) (-20%) [no section below] - investors at this company are patiently waiting for results for FY March 2022. Today brings a trading update with news that revenues for that year were £82m and EBITDA around £6.5m. This is below expectations, despite an exchange rate gain of £1m. There is a problem with sales tax in a foreign country: £2.5m has been provisioned but the final cost, if any, is unclear. In addition, £0.3m of development costs have failed an accounting test and must be expensed rather than capitalised. This doesn’t change the underlying business performance, but it does raise a question about whether the so-called development costs are really just an ongoing business expense? In combination with the sales tax confusion and the lateness of this update, it paints a picture of a disorganised company.

On top of that, Q1 FY 2023 sales to the Chinese market are “significantly below” the prior year, as the prior year’s high demand is described as being exceptional in nature. Despite revenues from the rest of the world growing strongly, EAH’s broker has warned that it is likely to reduce its estimates for FY 2023. Shareholders might end up with a no-growth year: hardly a disaster, but it’s not easy to justify last night’s £80m+ market cap when the company isn’t growing, looks disorganised, and is only earning c. £3m - £4m in net income.

Bidstack (LON:BIDS) (£31m) (-1%) [no section below] - this company claims to have technology that improves in-game advertising. Revenues have been minimal so far, but do show improvement. H1 sales this year are £2m (H1 last year: less than £1m). Unfortunately, any gross profits continue to be dwarfed by Bidstack’s operating expenses. The operating cash burn is £3.4m over the six-month period, leaving just £3.7m in the bank. An R&D tax credit was received so that the cash balance may have recovered to £5m, temporarily. How long will this last? Even optimistic broker forecasts are expecting continued losses for the rest of this year and for next year, despite an anticipated surge in revenues. This is likely to be an entertaining punt but until the cash burn stops threatening the company’s solvency (see the going concern note), it’s a low-grade investment.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Facilities by ADF (LON:ADF) (I hold)

62p

Market cap £47m

Facilities by ADF, the leading provider of premium serviced production facilities to the UK film and high-end television industry, today provides an update on trading for the half year ended 30 June 2022 ("H1-FY22"), ahead of announcing its half year results in mid-September.

“Continued to trade strongly throughout H1”

High levels of fleet utilisation.

H1 revenues “marginally ahead” of “exceptional” prior year H1 comparatives.

Shorter hire periods this year has meant more costs moving equipment around.

“Strong order visibility for the remainder” of FY 12/2022 - order book almost full for 2022.

Overall trading - looks fine -

“continues to trade in line with market expectations for the FY22 year*

*FY22 market expectations as at the date of this announcement of £31.8 million revenue and adjusted EBITDA** of £7.8 million.”

Outlook -

Additionally, market dynamics remain strong, with continued robust demand for film and high-end television the UK and the Group's 2023 order book continues to grow. Therefore, the Group remains confident of further success.

The Group raised £15m of gross proceeds on admission to trading on AIM and a portion of these funds have been deployed in increasing the size of the Group's fleet to meet demand. Management also continues to actively review initial acquisition opportunities in line with the Group's strategy detailed at Admission.

My opinion - I’ve covered ADF a few times before. In particular, the SCVR for 5 Jan 2022 looked at ADF on its listing at 50p, and I formed a favourable view - which we hardly ever do here for new issues. ADF was one of very few decent small cap recent floats. In particular, the valuation was sensible, and the funds raised were for expanding its hire fleet of TV production vehicles, not previous owners cashing out at an inflated valuation.

Since listing, performance has been good. ADF is benefiting from strong demand for its equipment, given a recovery in TV/film production post pandemic. Also the growth in streaming services is boosting the sector - also noticeable at Zoo Digital (LON:ZOO) . Whether this lasts, is the big question, because streaming services seem vulnerable to customers cancelling subscriptions. Could that have a knock-on impact on ADF in due course, if its customers begin to rein in production of new shows? No idea, you’d have to ask a sector expert.

For now though, ADF looks a decent niche business, and priced reasonably, on a forward PER of 12.4.

My main question is over European expansion. ADF already has a big UK market share, so expansion was planned, by acquisition, into Europe. Has management got the experience & bandwidth to execute on that strategy? Sometimes it’s better to focus on what you do best, and dominate a niche, rather than over-reach.

ADF is still above its 50p float price (Jan 2022), testament to the fact that Cenkos priced this deal sensibly.

Note that the Stockopedia algorithms have taken a shine to it more recently too.

.

.

Works co uk (LON:WRKS)

35.5p (down 24% at 08:46)

Market cap £22m

TheWorks.co.uk plc, the multi-channel value retailer of arts, crafts, toys, books and stationery, announces an update on FY22 results and current trading for the 13 weeks ended 31 July 2022 (the "Period" or "Q1").(1)

TheWorks has an unusual 4/2022 year end. So its Q1 period covers May, June & July 2022.

I last looked at it here on 20 May 2022, being a bit sceptical because performance appeared to be getting a major boost from business rates relief, and other reasons.

Today we’re told -

FY 4/2022 underlying EBITDA now guided up, to £16.5m (WRKS guided £15.0m in its y/end update on 20 May).

Profit boosted by lower than expected provisioning against inventories.

Dividend of 2.4p reiterated for the year - the first one since the pandemic hit.

FY 4/2023 - Q1 trading - store sales were up 1.4% on a like-for-like basis (the best measure of underlying performance, as it strips out site openings/closures).

Improving trend within Q1, May was bad (no figures. Tough comps due to prior year re-opening - fair enough), by July LFL sales had improved to 7.6% for the month - pretty good.

The smaller online division (only 10% of total sales) dropped a striking -28.6% in Q1 revenues (still up 40% on pre-covid). This seems to be the fallout from a previously disclosed “cyber security incident”, which sounds as if it was more serious than I previously imagined. It makes negative noises about online, but maybe it’s just not very good at selling online? Or these types of products are more appealing in-store, for browsing & impulse buys? e.g. children demanding particular products from their parents in-store?!

Outlook - market outlook has deteriorated, heightened degree of uncertainty, especially re forthcoming Christmas (peak trading period).

Still expecting sales growth this year though, not sure at what level.

Cost headwinds mentioned, wages, and freight “showing little sign of abating in the short term” - this is surprising, because shipping costs are falling now, so maybe WRKS has contracted at higher prices? Worth querying this, if anyone speaks to the company.

Profit warning - here’s the hammer blow - “materially” usually means at least 10% -

…the Board has materially lowered its expectations in relation to FY23's result.

Bank facility - good news here. The interim results indicated a facility (RCF) with HSBC of £22.5m, stepping down to £20.0m in Jan 2022. Expiry Sept 2022. Today we’re told that a larger, £30.0m facility has been agreed until Nov 2025. That’s really good news actually, as it shows the bank must be comfortable, at a time when we might expect them to be nervous due to macro factors.

Scrutinising the bank covenants, and the going concern note, will be important when the results come out on 23 September 2022 (a very slow reporting schedule, which I dislike).

My opinion - I remain unconvinced with this share. As mentioned here back in May, SHOE looks a tons better business than WRKS.

There’s no broker research available, so I have no idea how much the company is guiding down FY 4/2023 expectations by. Therefore, with this lack of information from the company and brokers, it’s currently not possible to accurately value this share.

It seems obvious that FY 4/2022 profits are not sustainable, with rising costs, and withdrawal of business rates relief, and little prospect of imminent revenue growth due to consumer retrenchment. Also, remember that actual profit is nowhere near the distorted, misleading EBITDA figures quoted.

If consumers rein in spending, as one imagines they might, then it wouldn’t surprise me if WRKS warns on profits again, and struggles to make any genuine profit at all this year. That’s the trouble with a largely fixed cost business, operating on a wafer thin net profit margin. It was struggling pre-pandemic, remember.

Although the market cap is peanuts now, so if things go better than expected, it could be a good punt. It’s not for me though, too much uncertainty.

The balance sheet is OK, if you strip out the IFRS 16 entries, which have a considerable deficit - indicating there are some problem sites with onerous leases.

I need to see the full figures, in late September, we don’t have enough information currently.

.

.

Mincon (LON:MCON)

- Share price: 95p

- Market cap: £188m (€224m)

This is an AIM-listed Irish engineering company. It is listed in pounds and pence, but reports sales, profits and dividends in terms of euros.

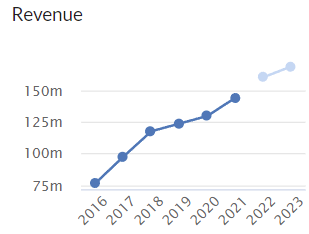

It has a fine track record of profitability stretching back over many years. It has also grown the top line considerably:

That’s a six-year chart but the view over fifteen years is excellent, too.

The company calls itself “The Driller’s Choice” and specialises in a wide range of drilling equipment that it sells internationally.

Let’s see what is reported in today’s interim results:

- Revenue +27% to €85.1 million, boosted by a strong dollar.

Most products sold by Mincon are manufactured by Mincon itself; sales of its own products are up 24%.

There was a small acquisition during the year (€1 million price tag).

Here’s an outline of the industries served by Mincon, and their share of revenues in each period:

These are cyclical industries, but that doesn’t seem to have hurt Mincon’s performance much over the years. Remember how impressive the results from Somero Enterprises (LON:SOM) usually are, even though it also serves the construction industry.

Continuing with today’s results:

- Gross profit +18% to €27.1 million.

- Operating profit +18% to €8.8 million.

Results from Mincon tend to be clean, without the usual adjustments and excuses that you get from the average company that tries to make itself look bigger and more successful than it really is.

Revenues grew at a faster rate than profitability, i.e. margins have declined.

The CEO’s comments confirm this. There have been “cost increases across many fronts, but particularly in raw materials and energy, as well as freight, partly arising from the use of air freight to reduce our order backlog”.

Note the last part of this: margins hurt by a decision to swiftly meet high customer demand.

This is something I love to watch out for. I call it “a good profit warning” (though today’s results don’t constitute a profit warning).

It happens when a company is experiencing so much customer demand, that it is actually unable to meet that demand through normal operations.Companies in this situation sometimes make decisions that hurt their profitability, because they don’t want to let down their customers.

In the case of Mincon, they could have allowed their order backlog to fester, but they decided to use an expensive shipping method instead, even at the cost of lower margins and lower profits on these contracts.

But the decision will likely have positive long-term consequences: their customers will be satisfied and Mincon will maintain its reputation for the speedy fulfilment of orders. It has also increased its inventory of finished goods, to help facilitate this.

The difficulties in freight are part of the ongoing business backdrop, that includes high inflation and even shortages in some categories. Mincon’s CEO says:

We have implemented price increases, and these are starting to take effect, but constant vigilance is required to keep up with the pace of the cost inflationary pressures that we are seeing.

Paul and I agree on the importance of pricing power in this environment, and on the importance of businesses being able to pass on cost increases to customers without too much of a delay - any significant lag between cost increases and sale price increases could sink a struggling business. Mincon has started the process of sale price increases, but is clearly (and rightly, in my view) concerned that this could be an ongoing process for some time.

Product development - Mincon has a mysterious (to me) project called “Greenhammer”. This is a new, proprietary mining system that has been in the works for a long time. It sounds like it could be big, but who knows?

CEO comment:

…we are in discussions with a major mining contractor in Western Australia on commercialising the system and we hope to have a further update on this shortly. This is the culmination of many years of development work, and we are confident that it can have a significant impact on both Mincon and hard rock surface mining more generally. This Greenhammer development has not gone unnoticed by the mining industry in Western Australia, who are keen to monitor the performance of this new system.

I can’t put a value on this but it suggests some optionality with Mincon’s shares. Future results might be turbo-charged by Greenhammer, if it successfully takes off.

Outlook - nothing too specific here. Margins should improve in H2, with the help of price increases I’ve already mentioned, and the order backlog is reducing.

My view

Mincon’s shares haven’t travelled far over the years:

Why is this?

Five years ago, in August 2017, the company was generating €97 million of revenues and generating €10 million of net income.

This year, it is forecast to do over €160 million of revenues, and over €15 million of net income. And this is with margins temporarily suppressed, and with the Greenhammer project soon to complete.

Yet the share price now is the same as it was five years ago, despite the progress made since then. The P/E multiple is 15x - it could be argued this is fair for an engineering group, but maybe it’s too cheap, given the quality performance?

There’s a small dividend to keep investors happy, as they wait to see what happens with Greenhammer. I think Mincon shares look promising here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.