Good morning from Paul & Graham! Today's report is now finished.

Agenda -

Paul's Section:

See the reader comments section below, where I put up brief comments first thing, covering (as I hold these shares, I see their news first, from email alerts) -

Boohoo (LON:BOO) (I hold) - acquires 7.1% strategic stake in Revolution Beauty (LON:REVB) a few days ago.

Cambridge Cognition Holdings (LON:COG) (I hold) - announces involvement in a drugs trial with Oxford University, in which it says take up of a new voice-based testing service has been good.

Purplebricks (LON:PURP) (I hold) - another big Director buy from the Chairman, might be significant, who knows?

Moonpig (LON:MOON) - I got an email telling customers to order early, due to Royal Mail strikes. Could this damage its business, if strikes remain unresolved?

Mysale (LON:MYSL) - breaking news! Mike Ashley's Frasers (LON:FRAS) has announced a 2.0p cash bid for the company (an Australian flash sale eCommerce business). This is a 25% discount to yesterday's closing price. Although as FRAS points out, the price spiked up from 1.25p when FRAS popped up with a new 28.5% stake in MYSL on 1 July 2022, which I covered here. MYSL is a serial disappointer, so I'll be really glad to see the back of it, and not to have to waste time covering its future updates. As an entry into Australian markets, it makes much more sense for MYSL to be consumed within FRAS's vast empire, than try to operate on a standalone basis, which has tried, but failed.

Bigger sections:

Cineworld (LON:CINE) - finally concedes that it needs to restructure its technically insolvent balance sheet. The only surprise is it's taken so long. Looks like a debt for equity swap is being considered, which "will likely result in very significant dilution of existing equity interests in Cineworld". We've been warning here for a long time about this high risk share, which is a good example of why highly indebted companies are best avoided. Especially in an economic downturn.

Gattaca (LON:GATC) - an in line trading update, but forecasts had previously been slashed to only breakeven. Clearly something is wrong with this business, as it operates in the staffing space for STEM skills, which is a lucrative area for competitors. New CEO & CFO were appointed in April 2022, so I look forward to hearing their turnaround plans. Finances are secure, and there hasn't been any dilution, so this could be a promising platform to start a turnaround. I'll monitor it more closely in future, as I can see speculative potential here.

Colefax (LON:CFX) - stellar results for FY 4/2022, but the outlook comments make clear this was a one-off bumper year, with a variety of factors meaning profits are likely to fall this new year. Although it could surprise on the upside, who knows? Lovely balance sheet, and it seems to collect in cash on delivery, rather than offering credit to customers - so trade receivables are small, and result in CFX sitting on a big cash pile, that it's been using to buy back a lot of its own shares. Very nice company, but share price probably now up with events, in my view, after a great run up.

Graham's Section:

Gooch & Housego (LON:GHH) (£165m) - a profit warning for G&H after the promised H2 recovery fails to materialise. If management’s narrative is to be believed, the order backlog provides for excellent prospects next year and beyond. I’m inclined to believe that the problems being encountered are indeed of a temporary nature. Indeed, given the size of the backlog, my instincts are to treat G&H’s current problems as growing pains: if they can rise to meet these challenges (especially their challenges in recruitment and retention), they will have a larger and more successful business. The market cap is now only around 11x the broker estimate for next year’s adjusted PBT. So if you can give the company the benefit of the doubt for next year, these shares are starting to look a lot more interesting from a value perspective.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Cineworld (LON:CINE)

13.2p (down 37% at 08:18)

Market cap £180m

Update regarding current trading, liquidity position and capital structure

Key points are -

“Gradual recovery of demand” since re-opening in April 2021.

Recent admissions have been below expectations, due to limited new film releases (expected to continue until Nov 2022)

Trading & liquidity impacted “in the near term”

Taking “proactive steps” to cut costs & save cash.

“Evaluating various strategic options” to obtain more liquidity, and restructure balance sheet debt “through a comprehensive deleveraging transaction” - i.e. a debt to equity swap - “likely result in very significant dilution of existing equity…”

Day-to-day operations should not be affected.

My opinion - none of this should come as a surprise, because CINE has been operating with a ridiculous, over-leveraged (that’s putting it mildly) balance sheet for some time. We’ve been ringing the alarm bells about it here for a long time.

For example, as at 31 Dec 2021, NAV was $345m, but that included $5.3bn of arguably worthless goodwill and other intangible assets. Write those off, and NTAV was negative at $(5.0)bn! How is that even possible?!

Net debt at Dec 2021 was $4.8bn - when a company owes its creditors this amount, then it’s the creditors who are in charge effectively, not equity holders. When control slips away from equity to debt, it usually ends in a near, or complete wipe out for equity, unless they’re prepared to stump up fresh cash in a meaningful way.

Hence being long of this share was just idiotic. Or based on pure hope that lenders would continue rolling over the debt, and the company could trade its way out of trouble. Although that was never likely, given the huge scale of finance charges, as lenders tend to increase the cost of debt as it becomes riskier.

All that remains to be seen now, is how brutal the debt holders are in the negotiations to swap debt for equity. I would argue the equity is likely to be worthless as things stand now, so the only reason debt holders would be kind, is if existing shareholders stump up a significant amount in a refinancing. For existing holders, it probably makes more sense to just ditch whatever is left, and move on, and maybe take a refresher course in understanding balance sheets, because there was nothing subtle about the risk here, it was obvious.

To be fair, the pandemic didn’t exactly help, but CINE was set up for failure before that, due to a reckless acquisition strategy that involved taking on ruinous debt.

Well done to shorters here, that was a logical trade, and required patience too. I don’t do shorting any more, because it’s so difficult, and share prices of distressed companies can behave in a completely irrational way - I remember both Thomas Cook, and McColls roughly doubling in price, shortly before they went bust. Hence shorters can be stretchered off just due to the irrational volatility. And what if you’re wrong? Then you could face being on the wrong side of a multibagger.

Another reason to avoid shorting, is that you can’t guarantee that the position would stay open. Shorts are often closed out, because the lender of the stock calls it in, at a time & price of their choosing. It’s very specialised, and high risk, so for most people I think shorting is definitely best avoided. Leave it to the experts, and even they get burned badly every now and then.

.

.

Gattaca (LON:GATC)

75p (up 3% at 10:11)

Market cap £24m

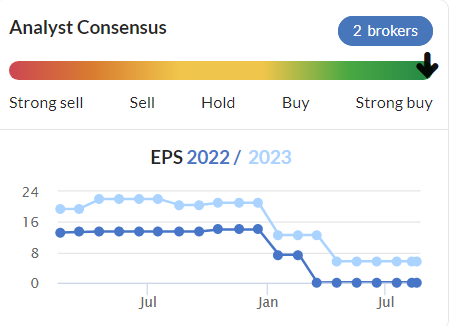

A dire long-term share price performance from this serial disappointer staffing group.

Forecasts have crashed this year, as you can see from the brokers consensus graph -

This is despite the staffing sector generally performing well, and other (better) companies performing ahead of expectations, so GATC’s problems are obviously internal, and have been for several years - profitability crashed before the pandemic.

On the upside, the share count has remained static at 32m over the last 6 years, so that means in theory, were the business performance to turn around, then the share price could recover well, back to previous highs since there's been no dilution.

Another positive is its strong balance sheet. Price to tangible book is actually below 1, not something you see very often in this sector.

.

.

Gattaca plc ("Gattaca" or the "Group"), the specialist Engineering and Technology staffing solutions business, today provides the following trading update for the 12 months ended 31 July 2022.

Company’s summary -

Trading in line

We expect our continuing underlying PBT for the full year to be in line with market consensus of break even

More detail is provided, but it seems irrelevant to me. The only question, is why this group is not making any profit, given tight labour markets, when competitors are doing well?

Looking back to its H1 results,the “continuing underlying” PBT was a £(0.3)m loss. So achieving breakeven for FY 7/2022 implies that H2 was a slight improvement, to a £0.3m u/l profit. Not madly exciting, but at least the trend is moving a little in the right direction.

Net cash position - looking good, at £12m at end July 2022. That’s down £2m on a year earlier, but includes payment of VAT arrears of £5.6m. That means net cash is half the market cap. The low finance charge on the P&L (last interim accounts) suggests that the net cash position is probably maintained most of the time throughout the year.

I see from note 9 (interim results) there’s a huge £75m invoice financing facility with HSBC. So plenty of headroom there to cope with intra-month working capital movements.

Balance sheet - Writing off £4m intangible assets take NAV of £31.4m down to £27.4m NTAV, a healthy position. The structure of the balance sheet is good - with a decent working capital surplus (current ratio was 1.47 - comfortable), and no long-term debt.

Outlook - sounds quite encouraging - although I wonder why management is pleased with performance that is only breakeven? They shouldn’t be! -

Matthew Wragg, Chief Executive Officer said:

"We are pleased with the performance of the Group through the second half of the year and importantly the speed in which the business is embracing our four strategic pillars; increased external focus, improved culture, operational performance, and cost rebalancing. We have established a solid foundation from which we can grow, leaving us well placed as we enter our new financial year, which has started well.

"We are mindful of the current macro-economic conditions as we continue to see robust demand in our key markets. There remains a shortage of candidates which plays to our key strength of deep knowledge and understanding of our sectors and niche STEM skills. We remain confident that the long-term fundamentals in our core STEM markets provide an exciting future for the business as it returns to growth."

My opinion - management sound a bit complacent to me. Being pleased with breakeven, doesn’t impress. GATC focuses on STEM skills (science, technology, engineering and mathematics) which is a booming area. Much larger competitor SThree (LON:STEM) makes a decent enough profit margin in this sector, where GATC makes nothing.

If GATC managed to increase its profit margin to a similar level as STEM, then this share would be a multibagger.

It’s adequately financed, so waiting for a turnaround doesn’t carry dilution risk.

I see that Matthew Wragg became CEO in April 2022, being an internal candidate. The CFO was also replaced at the same time with another internal candidate.

It’s too early to judge whether the new management are any good. Let’s hope they get some webinars going for us, so we can hear their plans, and ask Q&A.

Overall, I think GATC shares look quite appealingly cheap, for a potential turnaround. Although there’s not yet any evidence that a turnaround is actually happening, as it’s early days for the new CEO/CFO. Let’s see what they can do.

.

Colefax (LON:CFX)

808p (up 3% at 12:12)

Market cap £64m

(for the year ended 30 April 2022)

Colefax is an international designer and distributor of furnishing fabrics & wallpapers and owns a leading interior decorating business. The Group trades under five brand names, serving different segments of the soft furnishings marketplace; these are Colefax and Fowler, Cowtan & Tout, Jane Churchill, Manuel Canovas and Larsen.

My notes here in April on the “ahead of expectations” trading update are a useful quick refresher.

I guessed that EPS for FY 4/2022 might come out at 75-90p, when market consensus was 68.6p. The actual out-turn revealed today has blown the doors off, at 102.5p (up 127% on LY). That’s a cracking result.

Revenues up 31% to £102m

Pre-tax profit up 100% to £10.8m (helped by operational gearing, and a one-off big contract)

Share count - very unusual, in that Colefax has significantly reduced its share count with buybacks & tender offers (11m in 2016, now down to 8m shares in issue). That’s worked out tremendously well, and really shows the value when a decent business that’s on a low rating, uses that cash to buy back shares, thus enhancing EPS in future.

Modest divis though, only 5.2p for the full year (0.6% yield)

CEO owns 19% of the company, lots of skin in the game, which we very much like here at the SCVR.

Outlook comments - I like the measured tone here, clearly guiding us towards not expecting a repeat of the stellar FY 4/2022 results -

"Over the past year we have benefitted from the very strong housing market conditions which emerged after the first lockdowns in 2020 and this is the main reason for the Group's record results for the year ended April 30 2022.

"Rising interest rates and high levels of inflation have already started to slow housing market activity and we are therefore cautious about prospects for the coming year especially as we tend to lag changes in the housing market.

We are also experiencing high levels of cost inflation especially from our fabric suppliers whose manufacturing operations are being impacted by large increases in energy and raw materials costs.

Against this backdrop we believe it is unrealistic to expect continued sales growth in the current year especially against such strong prior year comparatives.

The fact that the Group operates at the premium end of the market should provide some protection from high levels of inflation.

In addition we are benefitting from the recent strengthening of the US Dollar as over 60% of our Fabric Division revenues are in the US.

The Group has a very strong balance sheet including cash in excess of £21 million and is well placed to deal with more challenging trading conditions"

Balance sheet - looks strong. NAV is £33.1m, with no intangible assets, to NTAV looks excellent also at £33.1m.

Stripping out the IFRS 16 lease entries gets rid of the £25.6m RoU asset, and £4.2 + £23.8m = £28.0m liabilities, so a £2.4m deficit. That adjusts NTAV up to £35.5m, which is very comfortable for the size of business, and means that the £64m market cap is about 55% asset-backed, giving great downside protection, and clearly more scope for continued share buybacks, given the £21.8m net cash pile.

One query I have, is why receivables are so low? Only £7.0m in April 2022, and £8.6m a year earlier. That’s extremely low for a £100m revenues business. This suggests that most customers must be paying pro forma - i.e. cash on delivery. If paying on more usual 60-day terms, then I would have expected receivables to be £20m+

I just raised a query through an adviser, and the answer is yes, the fabrics business sells cash on delivery to customers, no credit. The furnishings business operates differently, but has stage payments from customers during its work to revamp high end residential property. What a fantastic business model! That shows considerable strength, and means that CFX gets to keep the cash in its bank account, rather than offering free credit to most of its customers. That’s not something I see very often, but I like it a lot!

My opinion - lovely numbers, but the commentary is making it very clear that this was a one-off bumper year. Therefore, for valuation purposes, I wouldn’t use the 102.5p EPS achieved in FY 4/2022. Indeed, broker consensus is a halving to 50.7p EPS for FY 4/2023, which makes more sense as the figure to use for valuing the shares. At 808p that means a PER of 16.0x which looks if anything a bit too high.

Although if we adjust for the fact that about a quarter of the market cap is surplus cash, then that would adjust the PER down to about 12x.

Taking everything into account, the share price looks about right to me.

EDIT: a new broker note out this morning pencils in 57.4p for this year FY 4/2023, so that reinforces the point that we need to treat FY 4/2022 at 102.5p EPS as a one-off. End of edit.

This share has had an amazing run, but I don’t think it makes sense to chase it any higher right now.

Very nice business though.

.

.

Graham's Section:

Gooch & Housego (LON:GHH)

Share price: 662p (-20%)

Market cap: £165m

This is a photonics group with a long history of profitable operations. However, bottom-line growth has been somewhat limited in recent years and this explains the lacklustre five-year chart:

Today brings a trading update with a profit warning, let’s dig in:

Strong order book - the order book reaches a new record high thanks to strength “across all principal areas of the business, namely industrial lasers, telecoms, A&D and life sciences”.

Lasers are used in a wide variety of sectors and one of the most important is in semiconductor manufacturing. But there are also applications for undersea cables, satellites, and defence and medical purposes.

The order book has increased to £140.6m, up 32.6% over a 12-month period at constant FX (but actually up by 43.9%, if you don’t make any FX adjustments!)

Current trading - the ability to meet the order backlog is hampered - or “gated” in the words of the company - by supply chain shortages, Covid-related absences, competitive labour markets, and higher workforce attrition. I wonder are all of these factors external to the company, or do they need to try harder to engage employees to stay for longer?

On Glassdoor (the employee review website), the company gets a rating of 3.4 out 5.

54% of those who left a review would recommend the company to a friend, and there are some who left scathing reviews of management. Many companies do worse than this on Glassdoor, but still it suggests to me that there is a lot of room for improvement.

Profit warning - if you can trust what management are saying here, I’m not sure that this is such bad news:

Second half trading levels are expected to be better than the first half of the financial year due to the actions taken to improve recruitment and ameliorate supply chain shortages with higher inventory, but the longer ramp up and the higher level of investment to meet the increased order book mean that adjusted profit before tax is now forecast to be around £3.5 million lower than management's previous expectations.

The bad points are:

- We are promised both an H2 weighting and an improvement next year, which often fails to materialise. G&H already promised that H2 would be better than this.

- The company has recruitment issues and this may hint at deeper problems such as management who are out of touch with the job market and with the expectations of employees and candidates.

- Supply chain shortages continue to fester. These are outside the company’s control and there’s no clarity on when they’ll be resolved.

- Customers may be disappointed if their orders are fulfilled much slower than they expected (but again, this may be an industry-wide issue and not specific to G&H).

Against all of that, there might be positive elements to this profit warning. After all, the company is being forced to invest in staff, in order to meet high customer demand. It is being forced to outsource manufacturing that it would have preferred to do itself.

This sort of thing occasionally happens to a growing company and it doesn’t mean that the company is failing: it’s better thought of as growing pains. In future years, the investments and the decisions made now should benefit both the company and its customers.

Impairments? Management will “review intangible asset carrying values” - I wouldn’t worry about this. These will be non-cash adjustments to carrying values which are usually wrong, anyway!

FY 2023 Outlook - G&H expects “double-digit volume growth” in the financial year that begins at the end of next month (FY Sep 2023). Price increases are being passed onto customers, and revenue growth will be positive for the EBIT margin.

The FY 2023 outlook sounds ok, which helps to bolster my suspicions that the problems in FY 2022 should not be of huge concern to long-term investors. G&H itself tries to prove this with a progresive dividend declaration: the full-year dividend for the current year will be higher than last year’s.

New CEO - the long-standing CEO is stepping down after eight years in the role, and his successor has been selected. I don’t see any major red flag here - eight years is a reasonable tenure. There will be a handover period, and hopefully an orderly transition.

Estimates - the new FY Sep 2022 estimates from finncap are for adjusted PBT of £7.5m (previously £11m).

The adjusted PBT estimate for FY 2023 is now £12.1m (previously £15.1m).

It’s unfortunate to see that the FY 2023 estimate is cut by almost as much as the FY 2022 estimate: the profit figures are highly dependent on small changes to revenues and margins, and the FY 2023 revenue estimate has been reduced slightly. But you can see that there’s still a big improvement expected in FY 2023.

My view - I’ve hopefully made my view clear during the course of this report. G&H does have issues, of that there is no doubt. But many of these issues are industry-wide and found in other companies. But on the basis of this update, some of the issues simply stem from high customer demand and the challenges posed by trying to meet it. There’s an interesting contrarian thesis which says that these shares should have a nice recovery over the next 1-2 years, as the backlog is fulfilled.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.