Good morning from Paul & Graham!

Podcasts - good news, I've managed to publish my weekly summary podcasts on the main podcasting services now. Just search for "Paul Scott small caps" and it should come up (e.g. on Apple, Google, Spotify, Amazon Music), and hopefully it'll filter through to others too. I've used a free publishing service called Acast, and had to figure out what an RSS feed was, and how to use it, which took some time! I'll still be publishing them on my own website, with the latest episode here (warning includes a rant about energy prices, and bitcoin, and I don't expect everyone to agree with me, it's just one person's opinions, as usual!)

Agenda -

Paul's Section:

Diurnal (LON:DNL) - a takeover bid at an amazing 144% premium from a larger US bioscience group.

Revolution Beauty (LON:REVB) - confirms (as expected) that it won't meet the deadline for publishing FY 2/2022 results. So its shares will be suspended from close of play tomorrow. It's currently impossible to value this share without knowing the extent of the accounting problems.

Joules (LON:JOUL) - Sky reckons that talks with Next for a "rescue" refinancing have stumbled. Joules says that discussions continue.

Braemar Shipping Services (LON:BMS) - I have a good rummage through the (late) results for FY 2/2022, raising quite a few issues over balance sheet items. Current trading (in a separate RNS today) looks highly impressive, albeit the big upgrade is mostly due to favourable forex. Overall, Braemar looks to be making hay, in a buoyant sector. Shares look cheap, if current strong performance can be maintained longer term.

Graham's Section:

R&Q Insurance Holdings (LON:RQIH) (£386m) - Boardroom drama is heating up as a special general meeting approaches. Major shareholders want the Executive Chairman removed and replaced by one of the founders who gave the company its name. In this section, I discuss the background to the story which includes a collapsed takeover bid and an emergency fundraising. It looks to me as if bridges have been burned and there is no going back: I don’t think these relationships are going to be mended. As for the shares, they are an interesting speculation and offer cheapness versus the rate of profitability which the Chairman aspires to. Whether or not he will be around to implement his strategic plans is another matter.

Uniphar (LON:UPR) (£761m) (-4%) [no section below] - We’ve never looked at this “diversified healthcare services business” before. It joined the AIM market in 2019 and share price performance has been positive. Its three divisions are involved in 1) the sale, marketing and distribution of specialty medical products, 2) supplying early-stage, high-tech or otherwise difficult to source medicines, and 3) supply chain and retail (i.e. pharmacies).

Today’s interim results show single-digit growth in revenues and in various profit measures. Adjusted PBT increases by 9.9% to €26.1m, and net bank debt climbs to €73.8m. Post period end, the company increased its bank syndicate to include seven banks and they more than doubled the RCF to €400m, plus an extra €150m. Trading in H2 is in line with expectations despite “unprecedented inflation in all markets”, including “continued cost inflationary challenges which the management team are focused on mitigating”. There is no profit warning but the outlook statement comes with a disclaimer that maintaining margins will be a focus for the rest of this year and for 2023. Overall, there’s not much to dislike here but it’s far from cheap, the RCF-driven acquisition strategy is ambitious, and for followers of the IPO avoidance rule, it remains out of bounds.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Diurnal (LON:DNL)

11.25p (pre market open)

Market cap £19m

It’s another takeover bid, at a huge % premium - Diurnal has agreed to sell itself to Neurocrine Biosciences Inc, for 27.5p cash per share, an amazing 144% premium.

Neurocrine is listed on the US market under the ticker NBIX. Looking at its StockReport here, this has been a stellar share, rising 40-fold since the low of 2010. Its current market cap is £8.5bn, so buying Diurnal is a tiny morsel.

It has to be said that Diurnal’s track record since listing in late 2015 has been dire, as you can see from the share price -

.

The last trading update shows that Diurnal was well funded, with £16.5m cash in the bank at end June 2022. Therefore the takeover market cap of £48m is about a third self-funded.

Sales were starting to take off, with revenues up 104% to £4.7m for FY 6/2022, although Diurnal remains heavily loss-making.

So it looks like UK investors have funded the heavy losses over the last 7 years, and now the upside is being taken away with a takeover bid. Arguably not very satisfactory, although a 144% gain today is a nice way to start the week.

I wonder if the mainly institutional shareholder base will support this bid? The largest shareholder is listed IP (LON:IPO) which owns 29.3%, so it’s just made a profit of £8.1m this morning, but that’s only just over 1% of its market cap, so not madly exciting.

Personally I never touch biosciences shares, because they're impossible to value, unless you have expertise in the relevant science. And this is a good example of how the upside gets whipped away, if they do develop something interesting. Meanwhile the usual pattern is a plummeting share price, and repeated fundraisings. I see the share count at Diurnal has risen c. 4x since it listed. Still, at least it's not been a complete write-off, with the bid being 27.5p, being 81% below the 144p IPO price in Dec 2015.

.

Revolution Beauty (LON:REVB)

17.5p (pre market open)

Market cap £54m

Update on Publication of Final Results

The saga here continues. It has previously announced accounting problems, and that the deadline for filing accounts of 31 August for FY 2/2022 was not expected to be met (announced on 19 August 2022).

Today’s update just confirms this, and accordingly (again, as previously indicated) the shares would have to be suspended temporarily, under AIM rule 19 -

19. An AIM company must publish annual audited accounts which must be sent to its shareholders without delay and in any event not later than six months after the end of the financial year to which they relate.

REVB shares will be suspended before the market opens on 1 Sept, so if shareholders want to sell (or buy) then you’ve only got today & tomorrow.

After that, who knows what happens?

Timing - nice and vague -

The Company aims to complete its audit and publish its annual report within a matter of weeks of this announcement, post which trading in the Company's ordinary shares is expected to recommence.

My opinion - it’s just a gambling share at the moment. Since we don’t know the extent of the accounting problems, then the company is impossible to value accurately. Although of course investors could guess, and calculate a range of scenarios, then decide what seems most probable outcome, and go from there.

Although it is interesting that Boohoo (LON:BOO) (I hold) has bought up 12.85% of REVB in the open market, so clearly sees value here. There’s an obvious fit with BOO’s mostly young, female core customer base. REVB targets the same customers, with affordable make up.

So it’ll be interesting to see how this pans out. Expect more share price volatility today & tomorrow, before a nerve-wracking wait for more news, with the shares suspended.

Joules (LON:JOUL) (I no longer hold)

23.5p (down 8% at 08:09)

Market cap £27m

Sky News seems to be the go to place if you want to leak any company news for whatever reason! It reported on Sunday (28 Aug) that “rescue talks with Next stumble…” .

“The two companies are not close to agreeing the terms of an investment from Next…”, Sky tells us.

City sources said this weekend that Next had not received sufficient financial information to enable it to make a formal proposal to the Joules board.

There were also doubts that the clothing retail giant would be prepared to proceed with a deal at 33p-a-share or more - Joules' valuation when the talks were revealed by Sky News earlier this month.

Response to media reporting - Joules has issued a bland update this morning, just saying that “positive discussions” are continuing with Next, and the usual statement that there can be no certainty that agreement will be reached.

My opinion - obviously this share has been a disaster, with a series of (is it 4 now?) profit warnings. As mentioned last time I reported on it, the risk is now too high for me, given that it’s generating losses, and the clock is ticking re bank facilities, where the bank have been helpful in giving leeway, but only for about 3 months from now.

The risk is obviously that a discounted placing might be needed, diluting existing holders. Or worst case scenario, it might even end up in administration. Against that backdrop, it’s difficult to see why Next would be in a rush to do a deal, when it can let them sweat. Although there’s also the possibility Joules might do a deal with someone else.

I should have sat on the sidelines, and waited for a turnaround to become established, and the financial situation resolved, rather than jumping the gun and hoping everything would be alright. That’s my current stance, very belatedly - I’ll sit this one out, and only look to go back in once the funding situation is resolved, and a credible turnaround strategy in place. It should be salvageable, but I think they’ve done a lot of damage to the brand by being in constant sale, and I even saw a lamentable hour of TV shopping dedicated to clearing half price Joules stock - and it was grim, the product I mean. Hideous stuff, being sold on a tacky TV shopping channel. How on earth will they get back to selling at full price? So unfortunately, I think the brand’s pricing power has gone, and that’s a key thing right now.

My apologies that this one went so badly wrong, the sceptics were right as it turns out.

Braemar Shipping Services (LON:BMS)

332p (up 16% at 08:38)

Market cap £107m

These are very late numbers, for FY 2/2022.

Company’s headline -

Strong trading performance, balance sheet built for growth, and achievement of key strategic objectives.

Braemar Shipping Services Plc (LSE: BMS), a leading international shipbroker and provider of expert advice in shipping investment, chartering, and risk management, today announces its preliminary results for the year ended 28 February 2022.

The board is delighted with the performance of the business for the financial year and looks to the future with confidence.

Some key numbers -

Revenue up 21% to £101.3m

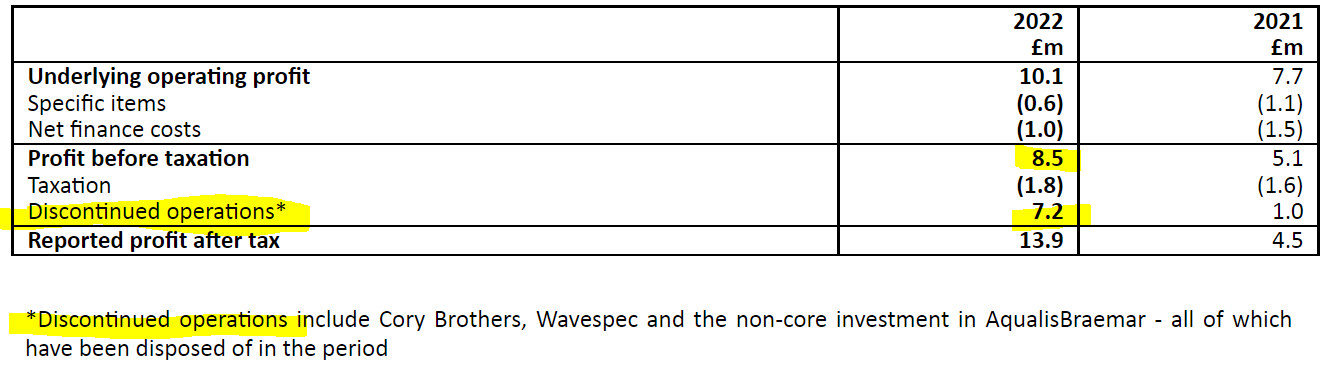

There’s a useful table showing how underlying operating profit of £10.1m turns into reported profit after tax of £7.2m (typo, sorry ) £13.9m , due to profit from disposals (which it says are to simplify the business) -

.

Increasing scale, and “generally favourable market conditions” are mentioned.

Underlying EPS is 27.95p (up a very impressive 100% on LY).

Although there are a variety of EPS figures given, and the most relevant one seems “Underlying continuing operations” of 23.06p (up 48% - much less of an increase than the number above).

Dilution - normally, diluted (i.e. allowing for share options yet to be exercised) EPS is similar to basic EPS, and a worse case scenario would normally be 10% dilution maximum from share options. I’m waving an amber flag here, because underlying EPS (cont ops) drops from 23.06p to 18.79p, due to 4.27p dilution effect from share options. That’s 18.5% potential dilution from share options, which seems horribly excessive. Note 11 says there are 6.94m share options issued. Why is this so high?

Note 28 has a section on share options. It’s too complicated for me to plough through it all here, with our time constraints.

There seem to be 3 distinct share option schemes, with by far the largest being a “Deferred Bonus Plan” with 6.45m share options (which seem to be nil cost) granted as at 28 Feb 2022. The shares seem to be acquired in the open market, and are held in an employee shares ownership trust, for granting share options.

To further complicate things, note 28 c) i) says this -

No option may be granted under any scheme which would result in the total number of shares issued or remaining issuable under all of the schemes (or any other Group share schemes), in the ten-year period ending on the date of grant of the option, exceeding 10% of the Company's issued share capital (calculated at the date of grant of the relevant option). Options are granted at a 20% discount to the prevailing market price.

What's the point is having share option schemes which could result in more shares being issued, but then not being allowed to issue them under this rule? All rather confusing, but this is a key area to get your head around if you’re thinking of buying or holding this share, I’m just flagging it up. But it does make me wonder whose benefit this company exists for - its shareholders, or its management? Is the balance right, or too generous to management?

Pension deficit - looks small, with note 27 providing more detail. Deficit recovery payments are £450k p.a., and expected to be eradicated by Jan 2023. So that looks OK.

Balance sheet - has about £81m intangible assets (nearly all is goodwill), so if we lop those off, NAV of £75.1m becomes NTAV of £(5.9)m - not very good.

There seem to be lots of unusual items on the balance sheet, e.g. long-term receivables of £5.6m, a deferred tax asset of £3.7m, investments, and an associate, convertible loan notes, derivatives (re forex forward contracts), provisions, warrants, the list goes on & on. I’m not sure management have simplified the business as much as they think! The more complexity there is, generally that can mean there are more things that could go wrong, in my view. It's unusual to find all this in a small cap.

It held cash of £14.0m, but debt of £28.3m (of which £5.1m is leases) so £23.3m bank debt.

Note 24 shows a very high accruals figure of £31.1m, which it says includes “accrued bonuses and other general accruals” - as the number is so large, I think this needs further explanation. How much is bonuses, in particular?

Receivables are covered in note 21, and look high at £38.8m. Although £6.5m is disposal proceeds, received 2 days after the year end date. It mentions employee loans (no number provided) - why is the company lending money to its staff? How much?

Note 21 also shows the ageing of receivables, which concerns me. It has £4.0m that is 3-6 months outstanding, and another £4.0m 6-12 months outstanding. Smallish provisions have been made against these numbers, but why are these customers taking so long to pay? Why is Braemar incurring bad debts at all? There’s another £2.4m more than 12 months overdue, but that has been largely provided for. But again, why are bad debts arising? If customers can’t pay, why do business with them? Why isn’t it requiring cash up-front from wobbly customers? I’m not sure the financial controls here are adequate.

Outlook - this all sounds very encouraging -

OUTLOOK

We have seen strong trading at the start of this financial year, and activity has been particularly high in the derivatives, sale and purchase, and corporate finance markets. The simplification of our business and our ambitious strategy to double our annual underlying operating profit is yielding strong trading results.

Our team has seen elevated numbers of newbuilding orders, principally in the container and gas carrier sectors. As a result, capacity at many shipyards is now unavailable well into 2025. For shipowners in other sectors this is making it challenging for them to renew their fleets and they're turning instead to the second-hand market. These dual factors have created significant opportunities for our Sale and Purchase desk, and they have capitalised on them. Over the next couple of years, these factors are likely to prove positive for our chartering desks too, as reduced ability to replace retiring ships is expected to constrict vessel supply and consequently create a higher floor on future charter rates.

We believe our ability to seize the opportunities available over the last year and maintain our high levels of activity are due to our investments in people, technology, and new offices. I look forward to another strong year of trading as these benefits continue to compound.

Trading Update - this is a separate announcement, presumably to draw attention to how good current trading is. Usually companies just include a trading update within the outlook section of their results.

This sounds fantastic, but note that favourable currency is a major positive factor (which could stop, or reverse in future periods possibly) -

Trading during the first five months of the new financial year has been exceptionally strong. The Group continues to benefit from the increasing scale and breadth of its broking operations, which have yielded a strong rise in transaction volumes across its diversified portfolio of shipbroking services. The board believes that these increased activity levels, combined with generally favourable market conditions will yield an outturn for the current financial year ending 28 February 2023 of not less than £20m (2022: £10.1m) of underlying operating profit, very materially ahead of the board's previously upgraded expectations of £12m.

In addition to the Group's increased scale, this year's trading is also benefitting from the strength of the US Dollar in which the majority of the Group's revenues are denominated. The strength of the US Dollar is expected to contribute approximately £5m to the growth in underlying operating profit over the previous year.

My opinion - there are lots of issues here that need further, careful research. But providing you can get comfortable with those points, then Braemar seems well worth considering.

It’s obviously in a sweet spot, and raising current year guidance from £12m to £20m u/l operating profit is remarkable, even if most of this increase is due to favourable forex movements.

I can certainly understand why bulls are happy with this company’s performance! These are impressive results, and an even more impressive current trading & outlook.

Stockopedia likes it too, with a StockRank of 77 - likely to rise shortly, as the big rise in guidance today filters through to broker notes - see Research Tree, for notes from Cenkos and Edison. Cenkos is forecasting 51p EPS this year! That would make the PER less than 7, although it might not be possible to maintain such a high level of profits longer term, time will tell.

.

Graham’s Section:

R&Q Insurance Holdings (LON:RQIH)

Share price: 102.25p

Market cap: £387m ($452m)

This is a Bermuda-based owner of run-off insurance portfolios (i.e. portfolios that are winding down, as new policies aren’t being added to them).

It sounds like it should be a sleepy business with little controversy attached. But somehow, it has ended up as the venue for a boardroom battle involving the Chairman, a founder of the business, and a well-known fund manager.

Chairman William Spiegel gave a presentation to Investor Meet Company in September 2021: here’s the link.

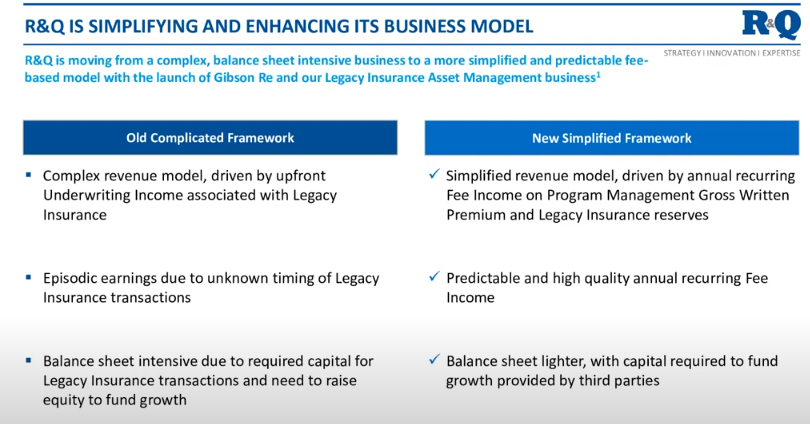

Spiegel has been spearheading a new strategy that will see R&Q adopt a fee-based, capital-light business model. Here is a key slide from his presentation that describes the change:

On April Fool’s Day of this year, R&Q recommended that it be acquired by its major shareholder Brickell, who would also inject £100m of fresh equity into the business. The new money was needed to cover losses associated with an old reinsurance contract.

However, that deal fell through and it looks like R&Q managed to annoy all of their major shareholders as a result of this episode.

Brickell pulled out of the deal, alleging that R&Q was “in breach of certain obligations under the implementation agreement [related to] the proposed transaction” (details not given).

But fellow shareholders Slater Investments and Phoenix weren’t happy with the proposed deal, either.

Phoenix CIO Gary Channon has written a new letter to R&Q shareholders.

In it, he details how Slater contacted him back in April about the proposed takeover. Slater wanted help to block the deal.

But Phoenix were concerned that if the deal didn’t go through, R&Q might breach its banking covenants, and had initially voted in favour of it.

In the end, the deal collapsed. The company raised the funds it needed in a $125m placing in June. But the top shareholders weren’t willing to just forgive and forget. It looks like they’ve had enough of the William Spiegel era at R&Q.

Phoenix Investments certainly has. In his latest missive, Gary Channon writes:

We and other investors have seen the performance of the business deteriorate under the leadership of William Spiegel… William Spiegel is not the right person to be leading the company…

From what we have heard, if there is a difference of opinion with other shareholders it is not about whether William Spiegel should go, it’s about how his exit should be achieved…

At Phoenix we think of these assessments in three categories: competence, alignment and integrity in ascending order. We find William wanting in all three.

According to Mr. Channon, William Spiegel “struggled with intelligent capital allocation at a company level”.

It’s a damning letter, and includes allegations of excessive pay and extremely poor communications with shareholders.

It includes the claim that R&Q accepted Brickell’s initial bid for the company and only the next day, informed Brickell that it needed £100m of emergency funding to avoid breaching its covenants.

Channon wants Spiegel out and they want him replaced by Ken Randall, one of the founders who gave the company its name.

Brickell, perhaps unsurprisingly, also want Spiegel to go.

Slater are presumably enthusiastic for change, too. This suggests that the top three shareholders are all in agreement on the matter:

In its response published via RNS today, the board of R&Q “reiterates its unanimous support for William, its respect for him, and confidence in the strategy he and his management team are executing”.

They also take collective responsibility for the company’s actions and decisions, which is fair enough. The Executive Chairman can only do so much without the support of his fellow directors.

My view

What makes this episode remarkable to me is that Phoenix was never previously an activist investor. Instead, they are a long-term value investor with certain idiosyncrasies, such as a “reading room” on their website. For certain job openings, they will not accept email applications and ask for handwritten letters to be posted to them.

They always struck me as a place where people spent their time reading obscure industry journals (in the style of Buffett) and made a trade once every two years. In other words, they did not strike me as the type of people to get involved in Bill Ackman-style conflict.

But maybe that has changed?

After all, Gary Channon became the interim CEO of Dignity (LON:DTY) last year.

Maybe they feel they’ve reached a point where they can reluctantly add value by getting more actively involved, when necessary?

I say “reluctantly” because they’d clearly prefer if Dignity hadn’t needed a turnaround, and if R&Q’s management did not need to be replaced.

Indeed, Gary Channon says that his original plan was to simply sell out of R&Q and move on:

…we decided to sell our entire holding in R&Q… If shareholders should choose to keep William Spiegel, then we will respect that and go back to where we were, disengaging from the company. We didn’t seek the role of activist here, it found us. We were quietly on our way, exiting stage left, before this came along and that is why our initial reaction was to just accept the Brickell bid.

My view on Phoenix and on the Phoenix UK Fund is that they are proven to be capable of beating the FTSE All-Share Index (see their long-term returns - past results are no guarantee of future performance).

If they are engaged in activism from time to time, I see no problem with that, as I expect they will be able to add value in situations involving companies which they have been studying and have owned for a long time.

The major risk with activism is that it can be time-consuming and can use up energies that would have been better spent studying companies that didn’t require any intervention at all. So hopefully Phoenix don’t allow themselves to get too distracted!

As for R&Q, the situation looks finely balanced in terms of whether William Spiegel will be forced out, and the co-founder brought back in.

R&Q’s board say that shareholders representing 40% of the votes have already stated that they intend to oppose the resolutions brought by Phoenix to the special meeting.

On the other hand, according to the Stockopedia graphic, Brickell, Phoenix and Slater add up to 36.5% of votes.

So I don’t know which way it will go.

Since I’m inclined to trust that Brickell, Phoenix and Slater are correct in their view of management, I think it would be bullish for R&Q if the resolutions are passed.

However, if the resolutions are not passed, then in addition to the management issue there would also be a technical overhang with the shares, as I expect that Phoenix would start selling again. Maybe another shareholder would mop up that liquidity?

These shares are superficially quite cheap, and remember that it has recently been refinanced so the balance sheet should be fixed for the time being at least:

But in the words of Phoenix, R&Q is “very opaque”. It’s not easy to look under the hood and see what is happening with the underlying policies and contracts. That might change with the new fee-based strategy but even that strategy might be revised if new management is installed.

In other words, there is a great deal of uncertainty at play here. If I put my bullish hat on, I would note the company’s stated ambition to earn $90m in “run-rate” pre-tax operating profit by the end of 2023. That’s the goal of the current Chairman.

Either he will be given a shot at achieving that, or a (hopefully better) Chairman will be installed to replace him. Either way, at a market cap of around $450m and with some excellent investors working on it, perhaps it’s worth a second look?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.