Good morning from Paul & Graham.

Agenda -

Paul's Section:

Gear4music Holdings (LON:G4M) - a mild profit warning was reported on 9 Sept 2022, which I belatedly look at today. Profits from the pandemic boom have largely evaporated now, so maybe the market's brutality towards the share price is justified? It's looking good value to me now, if you can cope with the increased debt.

SThree (LON:STEM) - it's another positive update, ahead of expectations. This remains a firm favourite value share for me. The outlook sounds a little more cautious though, hardly surprising given macro conditions. Strong balance sheet, nice divis, and a low PER. Should be fine long-term, even if we see possibly tougher conditions in 2023.

Graham's Section:

Jarvis Securities (LON:JIM) (£42m) - a bombshell RNS on Friday afternoon resulted in JIM’s shares selling off by almost 50%. Something has prompted the FCA to intervene and to require JIM to hire regulatory consultants at its trading subsidiary. In addition, this subsidiary won’t be able to pay dividends to Jarvis or engage new clients without the FCA’s consent, and this will have some real (albeit hopefully limited) impacts on both the business and ultimately on Jarvis shareholders. Only insiders will know the nature of the investigations and whether or not Jarvis is guilty of any regulatory breaches. While I can’t rule out the possibility of very serious problems (and the market hates this sort of uncertainty), I would view the shares as underpriced on the basis of my opinion that most companies emerge from these reviews with their reputations intact and/or with fines which don’t break the bank and allow them to continue trading.

Appreciate (LON:APP) (£47m) (+2.7%) [no section below] - this Liverpool-based gift voucher provider publishes a trading update for its AGM. Trading is in line with expectations. With actions taken to emphasise profitability in the consumer business, and improve retention levels in the corporate business, it is set up “strongly” for the key Christmas period. The company thinks that seasonality might be even higher this year as both individuals and businesses adjust their budgets. I guess this reflects broad restraints on discretionary spending, apart from Christmas gifts. The company is currently looking for both a permanent CEO and a permanent CFO. The former CEO Ian O’Doherty oversaw some disappointing years for Appreciate, obviously not helped by Covid, and the company needs to be reinvigorated. I continue to find it interesting as a possible value investment, and the StockRanks share my interest with a StockRank of 93, and a ValueRank of 87. The market is rightly pleased to see it performing fine despite the lack of leadership at the top. [no section below]

eve Sleep (LON:EVE) (£1m) (-36%) [no section below] - the fat lady has had a glass of water, has cleared her throat, and is about to start singing. Eve Sleep reports another underlying EBITDA loss for H1, worse than last year, on declining revenues. As of 31st August, the mattress company had cash left of just £1m after drawing £0.7m from a borrowing facility. Big ticket items are being hit hard as consumer confidence reaches arguably its lowest ever level, and eve Sleep - an unprofitable, speculative business even in the best of times - is the type of company that goes bust in this environment. Great efforts have been made to cut costs and the CEO argues that there is now a “greatly reduced breakeven point”, for whoever is willing to continue funding its expansion plans. Unfortunately, the formal sales process has not yet resulted in any firm offers, and more funding will be needed in October. Without new funds or a firm offer, “the Board will take the appropriate steps to preserve value for creditors”, which will presumably involve the company going into administration. I can’t imagine that the existing equity is worth anything here - future plans are likely to be determined in talks between administrators and new investors.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Gear4music Holdings (LON:G4M)

112p (last week’s close)

Market cap £24m

Gear4music (Holdings) plc, ('Gear4music' or 'the Group') (LSE: G4M), the UK's largest retailer of musical instruments and music equipment…

This update came out on 9 Sept 2022, and updates us on progress so far, for FY 3/2023.

"As previously reported, we were expecting inflationary pressures to restrict operating margins during FY23, and despite the weaker consumer environment we are pleased to have achieved sales growth during Q1. Trading during July and August has, however, been further impacted by the widely reported cost of living crisis and unusually hot weather across Europe.

We expected a return to a more normalised seasonal trading pattern during FY23 with less demand during summer months than winter months, and early indications are that trading has improved in September. However, given the lack of visibility over the timing of any improvement in consumer sentiment and wider macroeconomic conditions as we approach H2, we believe it is now prudent to moderate our full year expectations accordingly.*

We now expect FY23 revenue to grow to approximately £155 million with EBITDA of £9m. In line with our stated strategy the Group will continue to focus on delivering profitable growth as its first priority.

Our pipeline of growth orientated projects, including AV.com, continues to make good progress, and we are seeing strong results following last year's investment into our new European distribution hubs. We remain well funded and profitable and the Board retains its confidence in our medium and longer-term profitable growth strategy.

* Gear4music believes that consensus market expectations for the year ending 31 March 2023 prior to release of this announcement were revenues of £163.9 million and EBITDA of £11.9 million.

That doesn't sound a disaster by any means, and seems a sensible trimming of current year expectations, given that consumers are generally being more cautious.

But just look at what the share price has already anticipated, which seems quite extreme -

.

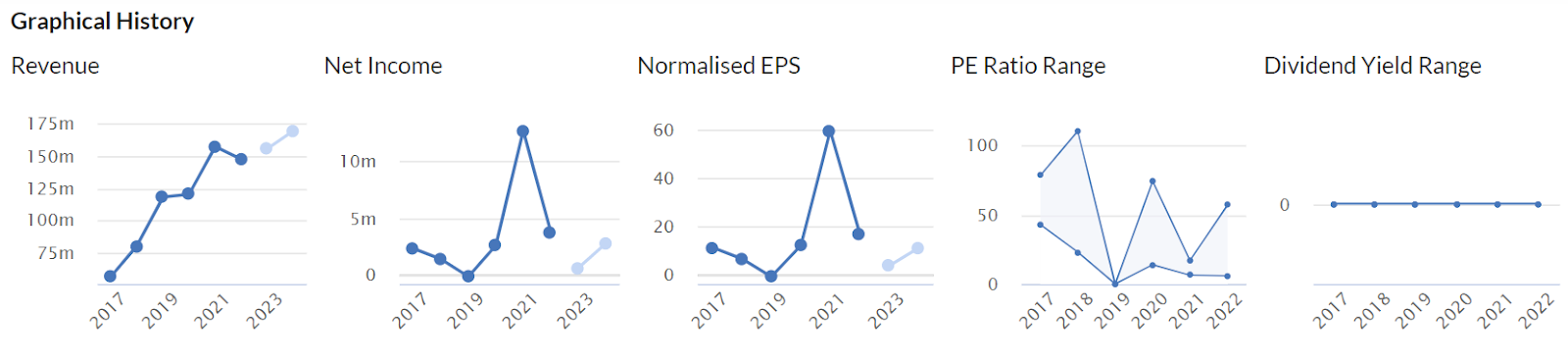

This share is a really good example of why I’m seriously questioning the wisdom of a long-term buy & hold strategy with small caps.

The Stockopedia historical graphs, as usual, encapsulate things so well - very good revenue growth, a rollercoaster ride of profitability as the pandemic boom came & went, wild variations in stock market sentiment on valuation, and no dividends (as it’s a growth company).

.

Valuation - I don’t like the focus on reporting EBITDA, because as with many companies, it’s not a meaningful number here in the real world (or as close to it as I get, anyway!).

Adj EBITDA of £9.0m (the latest company guidance) is only adj PBT of £1.3m, per the latest Singers forecasts (with my thanks), a large gap.

Balance sheet - so important these days, as economies slow, and bank managers get more nervous. Looking back at the FY 3/2022 balance sheet, the most noticeable things are a big increase in inventories, and increased gross long-term bank debt - to fund acquisitions. That could make some investors nervous in these trickier times.

However, the good thing about eCommerce businesses, is that most costs are variable, not fixed. So if G4M were to run into cashflow problems, it could run down inventories (which don’t perish, and are not subject to fashion risk), and slash marketing spend if required.

For that reason, I’m not ringing the alarm bells over balance sheet or cashflow.

My opinion - eCommerce is such a difficult sector at the moment. I’ve been waiting for a sector recovery, but there’s no sign of it so far, and given that we’re now in mid-late September, then it looks like a duff theme for 2022. But who knows, sentiment can turn on a dime, and things are not driven by arbitrary dates like year ends.

Is the current share price oversold? That depends on your longer-term view. Looking at the shorter term, this time last year, brokers expected G4M to generate about 40p in EPS for FY 3/2023. Current forecasts are only about one tenth of that. It’s such a reminder that profits are operationally geared, and it doesn’t take that much of a movement in revenues and margins, to make profits collapse - a lesson that I continuously forget in bull markets, and then have to re-learn again, every time there’s a bear market.

With G4M, I’m confident that management is committed & capable. I’d rather it hadn’t taken on more bank debt recently, but it looks OK given that inventories are higher than gross bank debt, so could be run down (inventories were deliberately increased, to improve availability of a very big range of products, given supply chain issues). It strikes me as nowhere near a crisis liquidity or gearing situation.

Overall then, the £24m market cap looks a potentially nice entry point, for investors who are prepared to take some risk. So it remains on my watch list.

.

SThree (LON:STEM)

366p (up 5% at 08:23)

Market cap £491m

SThree plc ("SThree" or the "Group"), the only global pure-play specialist staffing business focused on Science, Technology, Engineering and Mathematics (‘STEM’) skills, is pleased to issue a trading update covering the period 1 June 2022 to 31 August 2022.

STEM has a year end of 11/2022.

Headline - looks good -

Full year profit performance expected to be ahead of consensus

The Board now expects that profit before tax for the 12 months to 30 November 2022 will be at least 7% ahead of market consensus(3)

(3) Current consensus PBT expectation is £71.2m for FY22. Source: SThree compiled consensus.

There’s lots of additional detail in the announcement, but the key point is that Q3 net fee income was strongly up at +19% - even more impressive as it’s said to be against a strong prior year comparative.

Net cash is a healthy £57m as at end August 2022.

Visibility looks good -

- "Contractor order book(2) up 24% YoY, underpinning continued confidence in our full year performance"

The only slight negative I can see, is that it sounds as if staff are being over-worked (see clarification below) -

- "As previously guided, we expect productivity to remain above pre-pandemic levels, though it will reduce from the current exceptional levels over time, as the Group’s headcount grows."

"Good progress has also been made in the execution of our wider strategy, with the investment in our people, talent acquisition and digital infrastructure moving forward as planned. This investment is designed to underpin our long-term success, with costs starting to be incurred in Q3 as previously indicated.

Whilst we remain mindful of the macro-economic uncertainty across global markets, with all developments and lead indicators of the Group’s performance monitored closely, our strong market position underpins our confidence in the medium to long-term future of the Group.”

My opinion - this is the latest in a series of impressive updates from STEM. Although maybe the outlook comments are starting to sound a little more cautious? Hardly surprising, given the grim macro outlook.

It looks as if STEM should be heading for about 40p EPS this year, hence its shares are only priced on a PER of 9, despite it operating in what seems a resilient niche.

There’s a decent divi yield, and strong balance sheet too. Obviously we don’t know if, or when a downturn might come, but this business looks a quality outfit that should be fine longer term.

EDIT: the company's advisers contacted me after the above was published, and wanted to clarify over my point above saying that it sounded like staff are overworked. They said it's more about expansion, and taking on new consultants, who take a bit of time to gradually build up to peak productivity. Rather than existing people being overworked. That makes sense to me, so am happy to clarify this point. End of edit.

Graham’s Section:

Jarvis Securities (LON:JIM)

Share price: 94p (-49% on Friday)

Market cap: £42m

Commiserations to holders of this one, who saw the share price collapse by 49% on Friday afternoon.

At 2.39pm, just before the long weekend, it published a “Company Update”:

The facts

Jarvis have hired the regulatory consultants Ocreus Group to review the systems and controls at Jarvis Investment Management Limited (JIML).

(JIML is the trading company, while Jarvis or JIM is the holding company. I hope that’s not confusing!)

In simple words, the FCA has ordered this review. Here is some background reading on the relevant legislation:

Under section 166 of the Financial Services and Markets Act – known as s166 – the regulator has the power to require a firm to appoint a ‘Skilled Person’ to produce a report on specified matters or to appoint a skilled person directly. This could be, for example, a review of past business in a particular area or sales of a particular product; a review of a firm’s compliance with the client money and asset rules; or a review of a firm’s systems and controls.

In addition, JIML has “voluntarily” agreed to restrictions with the FCA (although I doubt they had much of a choice).

The restrictions include:

1) not taking on new clients at JIML’s “Model B” service without the FCA’s consent, until Ocreus has provided assurance re: JIML’s systems and controls.

2) JIML can’t pay dividends to its holding company Jarvis without the FCA’s consent.

Jarvis provide the following brief comment:

The outcome of the Skilled Person's review is not yet known but, in the meantime, the restrictions should have a limited impact on JIML's forecasted revenue and profitability as anticipated new business from Model B clients is not reflected or built into the published forecast. The additional professional fees and associated costs, and the asset restriction, however mean dividends payable to the Company (and therefore dividends payable by the Company) may be reduced and/or delayed pending FCA approval. JIML will continue to work with the Skilled Person and FCA with the aim of having the restrictions lifted as soon as possible.

My view

Despite the RNS only being a few paragraphs in length, it torpedoed the Jarvis market cap and leaves us with much to ponder.

Let’s first assume that the problems are not serious. What costs would Jarvis and its shareholders face?

- Professional fees - Ocreus will not be cheap. Perhaps a few million will be spent on the review, which could take up to six months.

- Revenue - even though “Model B” clients were not expected to grow to any meaningful extent, this is one source of revenue growth which has been cut off.

- Reputational - this would be unfair, but the perceptions associated with an FCA review might have an impact on future business at JIML’s Model B service (in case you’re wondering, “Model B” refers to outsourced settlement and custody services).

My view is that if the problems are not serious, then Jarvis is today worth almost the same as it was worth last week, before we knew about the possible existence of regulatory problems and the FCA review.

However, the share price was knocked lower by 50%. From the simple point of view of implied probabilities, it seems to me as if the market was pricing in an almost 50% chance that these problems were going to utterly ruin Jarvis as an investment.

Of course, the problems might be serious and could, in a worst case scenario, lead to large fines and other serious consequences that could indeed be ruinous.

While of course I agree that Jarvis shares should have been marked down on Friday, I can’t get on board with a 50% markdown. In many cases, won’t a Skilled Person review lead to little more than a slap on the wrist?

We are in a horrible market for any stock that has a regulatory problem, a profit warning, or faces uncertainty. On Friday afternoon, Jarvis went from a stock which had none of these problems to a stock which had all of them.

From that point of view, it’s understandable that many people will have rushed for the exits. In the fullness of time, they might be proven correct as the issues, whatever they are, may turn out to be very serious.

However, I do believe that the 50% markdown was premature, on the basis that many companies emerge from reviews such as this with their reputations intact and even if fines are imposed, they are often far from ruinous. But of course we can only speculate as to what issues might currently be under investigation at Jarvis.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.