Good morning, it's Paul & Graham here!

Today's report is now finished. Sorry we had to cut a few corners today, due to Mello, but hopefully we still covered enough to keep you happy!

Autumn Statement day, which I'm listening to. I'll probably comment on in this weekend's podcast, once I've studied the detail. Here's a snapshot of what I jotted down during Hunt's speech -

- It's a half:half mixture of tax rises & spending cuts, totalling £55 bn.

- Investors are being hit with effectively the phasing out of both the dividend allowance (£2k to £1k, then £0.5k over 3 years), and the same for CGT allowance (£12.3k to £6k to £3k) - that's a nasty measure, which will particularly hurt small investors.

- High earners also hit, with the 45% rate of income tax threshold falling from £150k to £125k.

- Income tax personal allowances frozen for another 2 years, so a big continuing stealth tax there.

- Windfall taxes increasing from 25% to 35% for energy company profits, and a new 45% windfall tax on electricity generators, combined will raise £14bn next year.

- Business rates revaluation will go ahead in 2023, which he claims will help smaller shops & pubs pay less.

- Nuclear power prioritised, with Sizewell C going ahead.

- Largest ever increase in national living wage, to £10.42

- Pensions triple lock maintained, increasing it by £872, largest ever increase (but it would be, in £ terms)

Those struck me as the main points, but I'll look at the detail again at a later stage.

Agenda

Paul's Section:

Water Intelligence (LON:WATR) - a detailed Q3 update, which is in line with expectations for profit. Shares look expensive, but the track record of earnings growth is impressive. Probably priced about right. No divis.

Ilika (LON:IKA) [quick comment] today’s update looks awful. Expecting a £9m EBITDA loss for FY 4/2023, with projected £14m cash remaining at that year end. So the cash runway is looking like it will be back with the begging bowl (again) probably in late 2023 or early 2024. Ilika has been promising jam tomorrow as a listed company for 12 years now, but not delivered anything of commercial substance. Occasionally there’s a speculative mania in its shares, e.g. last year was the biggest ever. It’s down almost 90% from that peak now. The market cap is £43m even after today’s 40% fall. Anyone buying or holding this share needs to recognise it’s a total punt, so for optimistic gamblers only. [no section below]

Crest Nicholson Holdings (LON:CRST) [quick comment] Trading update today for FY 10/2022. PBT in line with guided range of £135-140m. Weaker trading in recent weeks (as I would expect). Good visibility of pipeline for FY 10/2023, but forward sales of 2,038 houses is well down on LY 2,502. Net cash throughout the year, and £276m at end Oct 2022 - that's half the market cap! Complains about planning delays. We've seen peak earnings in this sector, with forecasts for 2023 reducing sharply in recent months. Also note the 4% surcharge on profits over £25m, that will hit medium to larger housebuilders. My view - CRST looks stunningly cheap, even allowing for profits to fall a lot, and is more than fully backed by NTAV. Note the big increase in cladding remediation provision, in the last interims - another sector headwind. [no section below]

Graham's Section:

Begbies Traynor (LON:BEG) (£211m) - a reassuring H1 update from Begbies, who are “confident” of meeting full-year market expectations. Organic growth is not spelled out for us, and we will have to wait longer to see the unadjusted numbers, but the adjusted numbers are looking good for the year so far. This stock continues to offer many attractive features, including excellent leadership and counter-cyclicality. I suspect that its current valuation is about right but perhaps the coming wave of insolvencies and administrations can push it even further.

Finsbury Food (LON:FIF) (£117m) - trading has continued strongly at this maker of bread and cakes since its year-end in July. Sales are up 15.7% mostly thanks to inflationary price increases but also to a little volume growth. This company has been listed for many years and has had more than its fair share of challenges over that time. A modest price to earnings multiple makes sense here but with the positive trading momentum that is underway, shareholders can hope for something better than the current 8x.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Water Intelligence (LON:WATR)

688p (up 6% at 11:29)

Market cap £134m

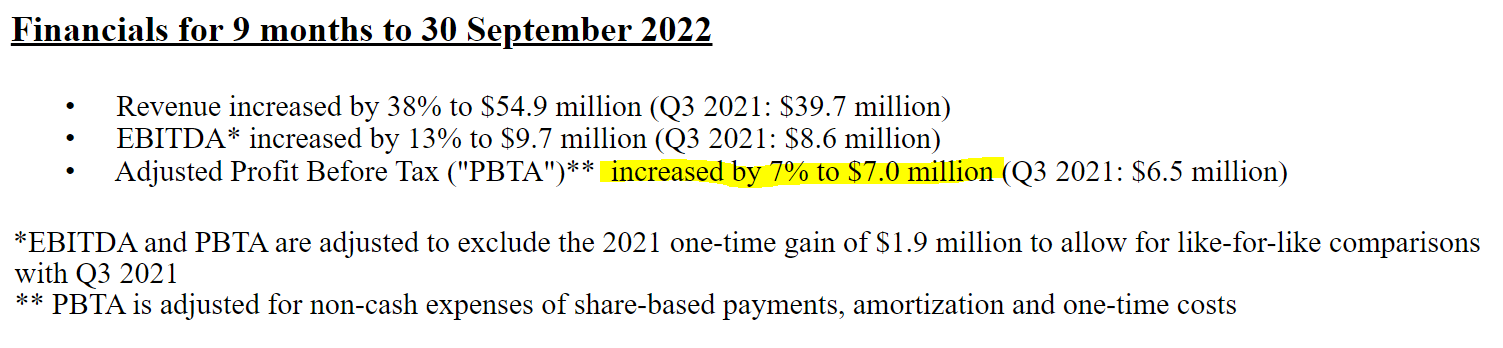

Water Intelligence plc (AIM: WATR.L) ("Water Intelligence" or the "Group"), a leading multinational provider of precision, minimally-invasive leak detection and remediation solutions for both potable and non-potable water, is pleased to provide a trading update for the nine months ended 30 September 2022.

It’s in line with expectations -

The Group is on track to be at the upper end of analyst expectations for revenue and to be in line with expectations with respect to profits for full year 2022.

Note below that revenues are up a lot, but profit is up a little -

Net cash of $4.5m

No dividends.

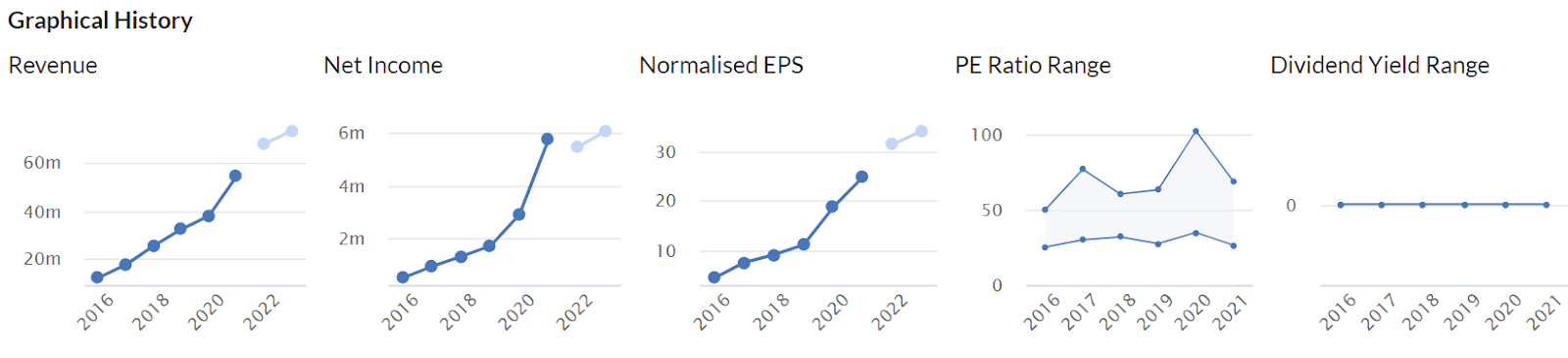

My opinion - it’s expensive, on a forward PER of about 24, but as you can see below, the track record of earnings growth is very impressive. So probably priced about right, in my view.

Graham’s Section:

Begbies Traynor (LON:BEG)

Share price: 136.75p (-0.2%)

Market cap: £211m

This morning we have a brief H1 update from this “business recovery, financial advisory and property services consultancy”.

The company is “confident of delivering market expectations for the full year”.

Headline numbers::

- Revenue +12% to £58.5m

- Adjusted PBT +13% to £9m

I also need to know organic revenue growth and reported (i.e. unadjusted) PBT, but we don’t get those numbers today. Begbies is highly acquisitive, and its numbers are heavily adjusted.

Net debt is thankfully low at £2.4m, despite over £7m in acquisition-related payments during the six-month period.

Divisional performance

- Business recovery/financial advisory: revenues +10%, with more insolvency appointments including “larger, mid-market insolvency and restructuring cases”. Begbies has 14% market share of the overall market, and 10% market share of administrations (measured not by revenues but by number of appointments).,

- Property advisory and transactional services: revenues +18%, “reflecting resilient income streams in a challenging economic environment”. This division brings in around a quarter of total revenues.

Comment by Ric Traynor (the largest shareholder in the business):

As corporate financial distress levels rise in a deteriorating economic environment, we anticipate continued momentum in activity levels in insolvency and restructuring and we are better placed than ever to take advantage of this with our expanded presence and enhanced service offering.

My view

When I read “confident of delivering market expectations”, I think: could there be a chance of an eventual earnings beat? After all, we have only just finished H1.

According to Equity Development this morning, their current year (FY April 2023) forecasts suggest £117.7m in revenues, £19.7m in adjusted PBT, and 10p of adjusted EPS.

The devil is in the detail and my own view on this stock remains influenced by my (perhaps excessive) caution in how I treat the adjustments to the numbers.

The earnings adjustments do show up when it comes to the company’s assets and equity: tangible balance sheet value was less than £10m as of April 2022.

And it is clearly a “people business” whose most important assets leave the building and go home every day.

But I accept that it does have real earnings power: for example, last year’s cash flow statement showed £18.1m in (after-tax) cash from operating activities, if we are willing to exclude some large acquisition-related payments.

I also remain of the view that this stock can provide a welcome counter-cyclical economic hedge for many investors.

And I’m reassured by the continued leadership (since 1989) of Ric Traynor, and by his continued presence as the largest shareholder. There’s no question about his alignment with investors.

At a market cap of around £200m and a share price of 136p, Begbies has achieved a respectable PE ratio of between 13x and 14x. Would we really want to pay multiples of 20x, for accountancy and advisory firms with fairly empty balance sheets? Personally, I don’t think so.

So these shares look fairly and fully valued to me. Even so, the economic winds could carry it higher in a recession and for that reason alone it remains interesting.

Finsbury Food (LON:FIF)

Share price: 90p (-1%)

Market cap: £117m

This “leading UK specialty bakery manufacturer of cake, bread and morning goods for both the retail and foodservice channels” has been holding its AGM this morning.

Paul covered their recent full-year results in detail here.

Today we have the following news:

The robust performance of the previous financial year to 2nd July 2022 has continued into the current financial year. Sales for the first four months of FY23 grew by 15.7% to £122.8m, driven by a mix of volume growth of 1.1% and price recovery of 14.6%. Our retail business continues to perform well, foodservice continued to bounce back, and our overseas division continued to see strong growth.

I wish every small company was so transparent in explaining where its revenue growth was coming from (volumes versus price inflation). At Finsbury, we can understand from the above that most of the recent revenue gains are derived from inflation, and that makes sense.

Food and beverage inflation is currently running at 16.4% according to the official numbers, so this all adds up.

There is no relief yet from these trends:

The macro-economic and cost inflation headwinds that we have had to face throughout the opening months of the new financial year have been at levels in excess of those experienced in FY22.

The solutions? “...revised commercial arrangements, operational improvements and other supply chain and overhead initiatives.”

Given the increased cost of living, and the need for consumers to get value for money, Finsbury thinks there could be a boost in supermarkets’ own label sales, which would be good for business.

My view

I won’t rehash Paul’s analysis of the finals, so there isn’t too much for me to add. I will reiterate that I think food and fuel-related stocks are a nice place to be invested when it comes to the inflation trend, as they should have little difficulty passing on increased costs to their customers (“revised commercial arrangements”, in Finsbury’s language). There are exceptions, but most food producers seem able to do this.

As it’s a commoditised industry, food manufacturers do tend to trade cheaply. So I agree with Paul that the likelihood of a PE re-rating is somewhat limited. Although having said that, FIF has achieved 12x-13x from time to time. That suggests up to a 50% boost from the current 8x, if trends remain positive.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.