Good morning from Paul & Graham!

13.55. This report is now finished. Thank you for the comments and the feedback as always!

Agenda

Graham's Section:

Safestyle UK (LON:SFE) (£34m) - a profit warning from this double glazing company. October orders were too low, and November orders were too high! The November orders have helped to boost the order book to a very high low, but also have the effect of increasing costs without generating any revenues for the current year (FY 2022). Therefore, FY 2022 is now set to produce a loss. Estimates are slashed for the current year and despite the increased order book, both revenue and profit forecasts for next year have been cut, too. This company always seems to have problems and while it could make for an entertaining bet on the economy, I don’t see it as a stock that’s suitable for holding long-term.

Altitude (LON:ALT) (£23m) - interim results are in from this platform that provides services to suppliers and distributors of promotional products. We already had a trading update last week so there are few surprises in here, but it’s good to see confirmation that the company is trading close to breakeven and still has a net cash position, plus a small borrowing facility giving it some headroom. While the stock got overheated in 2019, the market might not be giving it enough credit now for its reasonable financial performance and the possibility of operational leverage in the years ahead.

Record (LON:REC) (£173m) - excellent interim results from this currency specialist. Performance fees are back, boosting the bottom line, and management fees are up too thanks to eighteen months of strong net inflows. The inflows aren’t showing up in AUME (“assets under management equivalent”) yet, due to negative market movements. But customers are clearly happy, as they continue to sign up for Record’s services. The company, and I, are excited to see what it can achieve with fund management and other currency-related products. To that end, a new fund has been launched in Luxembourg. The shares still don’t strike me as expensive even after recent strength.

Supreme (LON:SUP) (£120m) - I attempt to make sense of the interim results at this fast-moving consumer goods business. The lighting division has seen its performance collapse due to retailer destocking and the revenue performance is only saved by strong growth in vaping. The company is confidently raising expectations for the full-year despite poor profitability in H1. Looking further ahead, there is no change to earnings expectations for FY 2024. It’s a really mixed bag and I’m left scratching my head: my instincts say that this business deserves to trade on a modest earnings multiple and I can only assume that the market is about right, pricing it on a PE ratio of 10x. In this uncertain economic climate, an improved balance sheet probably makes more sense for it than chunky shareholder dividends.

GB (LON:GBG) (£850m) (-4%) [no section below] - this stock is rarely covered in the SCVR, since it’s more of a mid-cap than a small-cap! In 2018, I noted a valuation multiple of nearly 40x and suggested that it was prohibitively expensive. The share price is down by one third since then, and valuation is more interesting at 16x earnings. Today’s results show a 3.4% growth in adjusted revenues at constant currencies, and a 1% increase in adjusted operating profit to £28m. The statutory numbers are much worse, however: operating profit falls to just £2.5m, largely due to the amortisation of acquired intangibles. The adjustments made by this company to its statutory numbers are both large and numerous.

More positively, the outlook statement tells us that H2 has started in line with expectations, and there is no change to forecasts. Net debt currently sits at around £118m. This is a large and reputable business providing advanced digital intelligence services to some of the world’s biggest businesses. However, there are many different moving parts to understand, and I perceive it as a black box type of investment. It is in my “too difficult” tray at this time. The StockRanks are also unconvinced, only awarding it a score of 26. [no section below]

VP (LON:VP.) (£277m) (+3%) [no section below] - this equipment rental group provides a wide range of products to sectors such as construction, engineering, rail, and oil & gas. Today’s interim results show revenue growth of 6% to £186.5m, adjusted PBT also +6% to £21.5m, and a return on capital employed of 14.4%. It’s reassuring to see ROIC listed so prominently at the top of the statement, to see it coming in at a very acceptable level, and to see that it has improved compared to last year! Statutory PBT comes out at £17.9m, so the level of earnings adjustment is modest.

Inflation has affected everything from transport to wages, and is being “actively managed”. I expect that VP should be able to pass on costs without too much difficulty or too much of a lag. Trading is in line with expectations. Net debt is currently around £149m: the company issued two private loans (total value £93m) to PGIM, maturing in January 2027. It also has a £90m RCF maturing in June 2024, and this will involve a floating interest rate. There are economic risks here that lie beyond VP’s control; arguably these have been priced in at a PE ratio of 8x and a yield of 6%, for what appears to be a successful and diversified rental business. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Safestyle UK (LON:SFE)

- Share price: 24.3p (-21%)

- Market cap: £34m

A profit warning from this “leading UK focused retailer and manufacturer of PVCu replacement windows and doors for the homeowner market”.

Orders in late September/early October were 7.6% below expectations, and 2.7% below the prior year. The costs of winning this business were higher than expected, too.

Why was trading so poor?

The Board attributes this to the well-reported political and economic news and events that have had a direct, adverse impact on consumer confidence.

Things picked up in November: order intake returned to expected levels (+30% year-on-year) and lead generation costs also returned to normal.

But since there is a lag between order intake and revenue generation, the November orders aren’t going to result in any revenues for FY 2022. In fact, the November orders only serve to increase costs for FY 2022.

Overall, therefore, these trends “will significantly impact FY 2022 profitability”. The only bright spot is an order book “that will close the year significantly ahead of our original expectations”.

Operational update: Safestyle is switching suppliers of PVCu profile, causing a small, temporary impact on manufacturing capacity. This will be completed by the end of the year. Installation capacity is unchanged.

Borrowing facility: new agreement in principle for a £7.5m replacement RCF with its existing lender Aurelius (not a mainstream lender).

Outlook: pre-tax profit for FY 2022 will be materially below expectations. Net cash will be lower than expected at c. £9m.

Looking ahead into 2023, there remains limited visibility on the strength of demand for next year, but the Board expects that the market will continue to be sensitive to negative sentiment. The Board reiterates that demand levels have improved recently and points to the fact that the Group operates in what has historically been a resilient and consistently-performing category despite previous challenging macroeconomic conditions.

Forecasts: the company’s broker has reduced the operating profit forecast for the current year from £2.1m to a loss of £3.4m. It has also reduced next year’s operating profit forecast from £10.1m to £4.6m, on reduced revenues.

My view

This company, in my experience, always seems to have problems.

A few of the challenges faced by the company, off the top of my head:

- Staff leaving to set up / join competitors.

- Cyber attack.

- Hot temperatures.

- Extremely sensitive to economic sentiment.

Today, we’ve learned that orders which arrive too late in the financial year have the effect of pushing up costs without generating any revenue: yet another factor affecting short-term profitability.

At least it is not currently using its borrowing facility, which would increase the risk profile considerably. Lender Aurelius says that it serves companies “who are unable to access the mainstream banking market for some or all of their capital requirements”.

I view this business as extremely high-risk and would certainly put it on a single-digit earnings multiple against the earnings that it makes in a “good” year. Possibly a low single-digit multiple.

The market had already priced it cheaply though, as it turns out, not cheaply enough:

Since the stock is so sensitive to economic sentiment, it might be attractive to those with strong views on the economic outlook. But it’s not, in my opinion, something that can be a buy-and-hold candidate.

Altitude (LON:ALT)

- Share price: 32p (-6.6%)

- Market cap: £23m

I’ve taken a renewed interest in this stock lately: could it become a valuable “platform” business? A marketplace where buyers, suppliers and distributors of promotional products come together, generating valuable commissions for Altitude?

Company description:

Altitude is a technology company and has developed an industry specific marketplace which provides various design tools, applications, and web site pop-up stores for promotional product distributors and suppliers. We have developed a robust e-commerce enabled and scalable trading platform that facilitates the execution of both offline and online promotional product transactions.

The website for Altitude’s operating business, “AIM” (not the stock exchange) can be found here. Distributor membership at AIM has increased to 2,425 (last year: 2,200).

It has two revenue streams: “Services” (designed to help other companies sell their products) and “Merchanting” (sales made by Altitude itself, using affiliates).

Bullet points for today’s interim results:

- Revenues +29% to £7.7m

- Within this figure, “services” are up 36.5%, while “merchanting” is up 23%.

- Gross profit +39.5% to £3.9m

- Adj. operating profit increases from £0.5m to £0.76m.

In H1 last year, the company received an employee retention credit worth £0.5m. This was included in the “adjusted” numbers last year, even though it was clearly not going to be a permanent source of income.

If we deduct that item from last year’s result, we could argue that adj. operating profit has really moved from zero to £0.76m.

The elephant in the room, however, is currencies. This is predominantly a US business, and I think we need to see figures in dollars to fully understand what is happening (a point well made by mojomogoz in the comments). Perhaps the company should simply stop reporting in pounds and report in dollars instead?

Profits and cash flow: the statutory pre-tax loss is only £0.1m (last year: £0.4m). The total net cash outflow is just £0.2m. It’s comforting to see the company so close to breakeven but it would also be nice to see a bigger cash pile: balance sheet cash is just £800k. Additional headroom is provided by a £700k credit facility.

Outlook: no change to outlook (we already had a trading update last week, saying that the company was on track to meet expectations).

My view: I remain intrigued by the possibilities here. It’s certainly at the speculative end of the spectrum, but I’m encouraged by the decent revenue growth, the fact that it’s already trading around breakeven, and the possibility that operational leverage could kick in at some point.

The £23m market cap gives a P/S multiple of less than 1x if we use the FY March 2024 revenue forecast of £23.7m.

It’s not so easy to kick the tires when there’s a (mostly) US business, listed in the UK. So perhaps it deserves to trade at a discount, especially given the lack of clarity around its results at constant exchange rates. But I still think this share has plenty of potential at this market cap: it was overvalued in 2019, but it could be undervalued here.

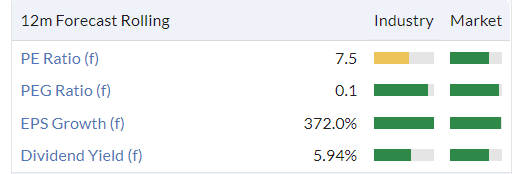

Record (LON:REC)

- Share price: 87.3p (+8%)

- Market cap: £173m

This is a currency specialist where I’m a former shareholder.

Back in June, I noted that the company was branching out into fund management, after many years of suffering price erosion in currency services. Today, it announces interim results for the six months to September 2022.

Key points:

- Revenues +35% to £22.1m

- PBT +46% to £7.5m

- Assets under management equivalent falls slightly to $80.8 billion

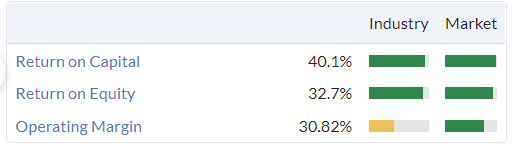

- Operating profit margin 34%

I’ve been a fan of this company over the years due to its excellent cash generation, strong balance sheet, and high returns:

I eventually sold out due to a lack of growth, especially in its high-margin services.

But in good news for shareholders, it appears to have gained a second wind:

- Management fees and performance fees are up, with “strong performance across all product strands”. Performance fees of £2.8m (last year: £0.5m) are a big boost to the bottom line, but are hard to predict.

- Diversification into “higher revenue and more scalable products”.

- A licence to operate in Germany has been granted, and a range of funds have been launched in Luxembourg.

CEO statement - excerpt

Record is known as a traditional currency manager, and has built its reputation in that area. Therefore, while it is more interested in other higher-margin activities in future, it doesn’t want to leave its past completely high behind:

While a lot of our future growth might come from products other than pure currency, traditional currency products are and will remain a cornerstone of our brand and our reputation. Promisingly, we are seeing some growth in our traditional business and expect this to continue whilst mindful these are at lower fee rates than other areas of focus… While we are devoted to diversification as a source of growth and improved margins, we would not want our investors or stakeholders to forget our currency roots.

Fund management work “is starting to bear fruit and will begin to have a bigger impact on our bottom line in the coming year”. Record now has a team based in Zurich, Amsterdam and Dusseldorf.

Venture capital: Record has started investing in VC funds and even directly into start-up and early-stage companies. I’m not sure what to make of this - do they have the skillset to pull this off? I don’t know. They do have lots of spare cash but maybe they should give it back to shareholders instead of using it for VC investments?

The strategy is now a bit of everything:

It is crucial to remember that all the elements above are part of a plan to diversify Record and make us a meaningful asset management business, fit for the next generation, and well balanced between opportunity, risk and return. No single revenue line is ever intended to dominate, and we are always very much aware of the Board's measured approach to risk appetite in everything we do.

Market review - I recommend reading this section, if you want to see what currency experts think of recent macro developments.

AUME - it’s worth noting that while assets under management equivalent declined 2.8% in dollars, they rose 14.6% when measured in GBP. The company enjoyed net inflows of $8.6 billion.

This table demonstrates that market movements are responsible for the decline in AUME:

Over the last six quarters, Record has enjoyed net inflows of $11 billion to AUME. That’s a huge thumbs up from customers, even if there hasn’t been any progress in AUME. But the inflows do show up in increased management fees.

Costs are up 33%, with generous movements in personnel costs.

Also note that between 25% and 35% of operating profit (before bonuses) gets paid out in the form of a staff bonus. 33% of pre-Bonus operating profit was paid out in H1.

The company still earns very healthy margins for shareholders, so everybody is a winner.

Interim dividend increases to 2.05p (the final dividend and the interim dividend are usually the same). After today's share price increase, the yield here is probably around 5%.

My view

I have some regrets about not holding onto this share, but it was difficult to keep holding when it seemed to be making very little progress for quite a long time!

Under its reinvigorated strategy, I continue to think that prospects remain bright. What I’m really excited about is to see an increase in its fund management income, which I think could turn it into a very high-quality financial stock. The company's funds are still in their infancy, and so some more patience is required on that front.

I’m less enthused about the VC investments, and I’d like it if they decided to focus on 2-3 activities instead of trying to do too many things at once.

But I still don’t think these shares are expensive:

Remember that the founder Neil Record is still the Chairman and the largest shareholder (28%). With this stewardship at the top, I anticipate that it will keep doing well.

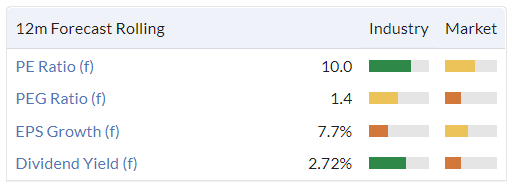

Supreme (LON:SUP)

- Share price: 103p (-5%)

- Market cap: £120m

This is “Europe’s leading manufacturer, brand owner and distributor of fast-moving staple products”. Among many other things, they own 88Vape.

Today’s interim results show a “credible trading performance”, in the words of the CEO.

Revenues are up 6% to £64.6m, within which there is a 47% increase in vaping (both organic and acquisition growth).

- Gross margin falls from 30% to 28% (we should not expect high margins on these products).

- Adj. PBT down 31% to £5.8m

- Actual PBT down 48% to £4.4m

- Net debt more than doubles to almost £20m

The lighting category appears to have been a disaster: revenues more than halved, “in line with the slowdown across the market”. I knew that the market for lightbulbs was volatile, but this takes the biscuit!

Gross profits in this category are down by 58%, as retailers unwind the overstocking they did over the past two years.

Dividend: the company declares an interim dividend of 0.8p. This looks like a very big cut compared to last year’s equivalent, although they don’t explicitly state this. They do say that their new policy is to pay out 25% of after-tax profits.

Debt: the company has a £25m RCF with HSBC, from which it has borrowed around £18m. The net debt to EBITDA multiple is around 1x, which is traditionally considered to be a modest leverage multiple.

Outlook

Positive start to H2 2023, with trading now ahead of market expectations for FY 2023

Vaping category expected to deliver a robust performance in H2 2023, reflecting positive impact of both organic and acquisitive growth

The business continues to navigate global trading challenges arising from raw material cost price increases, and inflationary increases to its overhead base

The company has been buying forward whey, to control the costs of its protein products, as an example of what it’s been doing to manage risk during a time of high inflation.

Investor presentation: Equity Development are hosting a presentation to investors today at 3pm: see here.

My view: I don’t have a strong view on this stock as it’s not one that I’ve studied in detail before.

Some of the key features are:

- Modest profit margins (goes with the territory)

- These margins are under pressure, as you might expect for a consumer-facing business during a cost-of-living crisis.

- My sense is that its brands probably do have good consumer awareness and recognition, but only very limited pricing power. They are very much in the “staple” category.

Given the volatility of demand in some categories, especially lighting, and the economic environment, perhaps it could have cancelled its dividend entirely, to ensure that its balance sheet is safe?

It’s also curious that the company is raising expectations for FY March 2023, and yet the share price is down today. I note that the analysts at Equity Development haven’t raised their outlook for FY 2024.

Overall, my instincts say that this stock should trade at cheap levels - perhaps the pricing is about right currently?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.