Good morning from Paul & Graham! Today's report is now finished.

I typed up last week's podcast summary, here it is.

Agenda

Paul's Section:

On Beach group (LON:OTB) - I take a favourable view of this share, as a well-financed, recovering travel business, with good flexibility from a low fixed cost base. Shares seem good value. Very vague outlook comments, and who knows how it's likely to be affected by the consumer slowdown? Overall though, for patient investors, I think this deserves a thumbs up.

Focusrite (LON:TUNE) - results for FY 8/2022 look pretty good - it's held on to most of the pandemic boom growth. Balance sheet is sound, outlook comments seem reasonable. There are a couple of points to note - heavy capitalisation of developments costs, and profit includes a one-off forex boost which should really be adjusted out. Overall, I see this as a quality business, with good pricing power. Shares look priced about right. Thumbs up overall.

Vertu Motors (LON:VTU) [quick comment] - a very large acquisition (Helston Garages) is announced, at a cost of £117m (VTU’s mkt cap is £169m), so shareholders need to scrutinise this deal carefully, as it’s so material. Interestingly, VTU is leveraging some of its large portfolio of freeholds, by taking out a 20-year commercial mortgage of £74.8m via BMW financial services. Zeus says this deal will increase forecast EPS for FY 2/2024 by 19%, then 25% the following year, as synergies kick in. Sounds exciting. VTU shares remain remarkably cheap in my view, and remember that forecasts already factor in a normalisation of car supply & residual values. (no section below)

In Style group (LON:ITS) [quick comment] - poor H1 results, loss-making. Over-stocked, like many retailers, with inventories having doubled, despite lower revenues. Still solvent. CEO throws in the towel, so the founder returns to the top job. Strategic review implies that being listed is a waste of time & money effectively (which it is, as there’s no liquidity, due to the way it was floated in large chunks to institutions, as with so many small caps). Has put itself up for sale, but no interested parties as yet. My view - it’s been a dead loss since day 1, so I’ll be glad to see this hopefully de-list. (no section below)

Purplebricks (LON:PURP) [quick comment] - H1 results look grim to me. FY 4/2023 guidance confirmed, at EBITDA loss of £(4.0)m to £(11.3)m range. It’s cutting costs. Cash pile is depleting fast. Can the new CEO turn it around before the cash runs out? Positive going concern statement says the £31m cash pile is enough. Management reckon it should become cash generative in early FY 4/2024 - which could be interesting, if it happens. Very well known brand name. Tough market to be attempting (another) turnaround. I’ll keep an eye on it, but at the moment, a turnaround seems a tall order. (no section below)

Mears (LON:MER) - many thanks to Samscvb, who flagged up a positive trading update from Mears, which we missed. I had a quick look, and posted my thoughts in the comments below here - it gets a thumbs up. Looks good, trading well, and cheap. Plus a generous divi yield. I like the look of this.

Graham's Section:

S&U (LON:SUS) (£255m) - the December trading statement from this family-owned lending group confirms that their receivables book continues to grow rapidly. Even more importantly, collections remain strong in the motor finance division and the level of defaults in the property bridging division is considered to be low (only 7 technically defaulted accounts). I can understand that investors will be very cautious towards this type of stock in a recession that includes both a cost-of-living crisis and falling property prices. But I believe that the Coombs family shares this cautious attitude, and have excellent alignment with other shareholders.

Numis (LON:NUM) (£202m) - this investment bank posts weak full-year numbers, as expected. The expectations from the summer weren’t met, as H2 saw weakness spread from the public markets over to the private markets. The share price is down by 30% since I covered it last and is now hovering around the value of the company’s balance sheet net assets. This company has a great track record of share buybacks and dividends and I expect that profits are going to recover nicely, although the timing is beyond their control.

Redcentric (LON:RCN) (£177m) (+5%) [no section below] - this managed IT business reports interim results for September 2022. It made three acquisitions during the H1 period, and more during the prior year, and accordingly reports a very large percentage increase in H1 revenue (to £61.5m). The company provides several measures of H1 profits but it’s more useful to look ahead into future periods: recently upgraded forecasts now anticipate that the company will make £18.7m of adjusted PBT in FY March 2024, on £150m of revenue. The acquisitions are bedding in with £10m of annualised savings so far, and another £7m planned. CEO Peter Brotherton says “the outlook for organic growth is also favourable, with positive net new business achieved in each of the last six months to 30 November 2022”.

As discussed in November, Redcentric’s net debt has risen to £39m. The company does enjoy substantial headroom on its RCF and net debt/EBITDA is only around 1.2x. Furthermore, net debt is forecast to reduce to £21m by March 2024. Given the rapid pace of change, it might be sensible for Redcentric to focus on hitting that target instead of making further acquisitions in FY 2024. I am cautious in this sector and so the moderate valuation multiples attached to these shares make sense to me, but if they demonstrate some organic growth during the year ahead then I’d be open to the argument they are undervalued. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section

On Beach group (LON:OTB)

109p (down 13% at 10:18)

Market cap £181m

The founder/CEO is stepping down in the next year, and being replaced by the CFO. Although the outgoing CEO is staying on as “Founder Director”.

Preliminary Results - for FY 9/2022

About On the Beach

With over 20% share of online sales in the short haul beach holiday market, we are one of the UK's largest online beach holiday retailers…

A strong bounceback in performance, driven by re-opening after the pandemic.

Revenue for FY 9/2022 was £144.3m, up 373% on LY, and almost back to pre-pandemic £147.5m in FY 9/2019.

Pandemic disruption affected the first 4 months (omicron), so these are not completely normal trading figures, hopefully next year could be better.

Heavily adjusted PBT is £14.1m, well below pre-pandemic £34.5m

Adjustments - the share-based payments charge of £4.7m stands out as excessive, and is exactly a third of the adj PBT above of £14.1m - how can that be justified?

Statutory PBT is only £2.1m

Regulatory reform - this section is worth reading, as it explains how after the failure of Monarch & Thomas Cook, the heavy losses incurred by consumers & taxpayers, means reform is necessary (maybe ring-fencing of customer funds). That could have far-reaching effects on travel companies which use customer funds to finance their business. OTB seems to already segregate customer cash, as £69.4m “Trust account” appears as an asset on the balance sheet. So OTB looks well set up.

Balance sheet - NAV is £156.8m. I always deduct intangible assets, £74.3m in this case, giving NTAV of £82.5m. That’s 46% of the market cap, so a fairly decent level of asset-backing.

Note that £11.0m of website development costs were capitalised in the year, much larger than the £5.3m amortisation charge. That flatters profit by £5.7m, a significant amount.

Cash is £64.5m, with no interest-bearing debt. The negligible P&L charge for debt interest suggests that it rarely, if ever, utilises the available bank facility.

Higher interest rates could benefit OTB, as it presumably could earn interest now on its own cash, and the customer trust account? Maybe a couple of million profit opportunity there?

Bank facility - note 18 details this, it’s £60m with Lloyds & Nat West, expiring Dec 2025.

Overall then, balance sheet & liquidity look fine to me, no concerns. Insolvency/dilution risk look very low, although the obvious risk of another pandemic has to be factored in. Do we want to invest in the travel sector at all, now we know how vulnerable it is to lockdowns?

Going concern note - an interesting read. It says even in a “remote downside scenario” of a travel shutdown until March 2024, OTB wouldn’t need to use its bank facility. That’s impressive. As note 6(a) shows, the biggest expense is marketing (£38.7m), which is greater than staff costs of £28.0m. Since marketing spend is very flexible, and can be quickly shut down in an extreme scenario, I think this gives us considerable comfort that OTB could weather any future storm. That’s arguably a much better business model than travel companies with large, owned assets, that incur considerable costs whether they are in use or not (e.g. airlines, cruise ships).

Dividends - nothing. However, it did pay divis pre-pandemic, so I would expect these to resume in future.

Outlook - if there was an award for vagueness, this would be on the final shortlist -

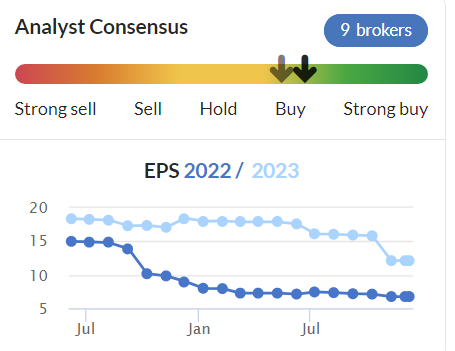

Broker research - the StockReport says 9 brokers cover OTB, but none of it finds its way onto Research Tree, which seems a glaring omission. The company should do something about this, as private investors need research notes. We create the liquidity in the shares, and set the price effectively, so it’s surprising this aspect has been neglected by mgt.

Actual (basic) EPS came in at 6.3p, which is close to the 6.7p consensus figure Stockopedia has below.

.

Is it reasonable to have higher forecasts for next year FY 9/2023? Given that FY 9/2022 was partially impacted by omicron, then it probably does make sense to assume the new year might perform better. Although we’ve now got the cost of living headwinds to deal with, and we don’t yet know to what extent consumers might cut back on holidays. Also, how much pent-up demand is there, after 2-3 years of disruption from the pandemic? For lots of people, holidays are sacrosanct, and they might make economies elsewhere, we’ll see in due course.

My opinion - I quite like OTB shares, as a good business on a reasonable valuation, so will give it a thumbs up.

Bull points are -

- Reasonable valuation

- Solid balance sheet with plenty of net cash

- Flexible business model, able to withstand another pandemic

- Prepared for regulatory reform, which might hamper competitors

- Should be further earnings recovery

- Well-known brand, and meaningful market share in a big niche.

Bear points that I can think of -

- Profits boosted by heavy capitalising of IT costs.

- Sector risk - maybe travel shares should be on permanently lower valuations, now we know how vulnerable they are to pandemics?

That doesn't seem enough, have I missed anything? If so, post a comment below!

Note the share count has gone up from 131m pre-pandemic, to 166m, up 27%.

A share price similar to the bottom of the pandemic, seems surprisingly low.

Note the grim StockRank, but this should improve as post-pandemic numbers begin to feed into the data shortly.

.

Focusrite (LON:TUNE)

790p (down 9% at 12:15)

Market cap £464m

There’s a 9% drop in share price today, but this needs to be seen in the context of a strong recent rally. As long as shares are not making new lows, then this could be seen as reassuring.

.

Focusrite plc (AIM: TUNE), the global music and audio products company, announces its Final Results for the year ended 31 August 2022.

The financial highlights table below looks pretty good to me, in the circumstances - that Focusrite’s core business was a big beneficiary from the pandemic. So have held on to most of that growth is impressive I think.

.

52p adj EPS is ahead of the 47.0p broker consensus shown on the StockReport, assuming they’re calculated on the same basis.

Adjustments are explained in note 2, and look fine to me. The main difference is £5.1m amortisation relating to acquisitions, which it’s customary to ignore. Hence I’m happy to value this share on the adj EPS figure of 52p - giving a PER of 15.2 - which looks about right to me.

Finance income - I’ve spotted an anomaly here, which artificially boosts profit by £2.3m, so I think we should be adjusting this out, which isn’t done in the company’s adjustments.

Finance income of £2.3 million (FY21: £nil million) includes a large gain from retranslation of US dollar balances within the Group, which is not expected to re occur.

There’s no broker research available, maddeningly.

Declines in revenue have been more than offset by the benefit of acquisitions.

Outlook comments seem OK to me, and supply chains & freight costs easing could be nice tailwinds for this new year maybe -

For the current year, our first quarter trading has finished in line with our expectations.

Overall demand for the Group's portfolio of products has remained strong.

We remain mindful of the current significant global economic and political challenges, as well as the ongoing cost pressures in the supply chain, but we have worked hard to build back our inventory position. This provides greater resilience against supply chain volatility and ensures we are able to meet demand as we head into the key holiday season in FY23.

We have also introduced a number of measures to maintain margins, through pricing actions and ongoing review of our production costs. With new product launches across the product portfolio planned for FY23 and beyond we remain confident that the Group continues to have significant organic growth potential within our existing brands.

In tandem, the Group has proven that it has the capability to successfully execute on its proactive M&A strategy, carefully considering potential acquisitions that are not only earnings enhancing, but can also add to our market potential, expand our R&D footprint, and add scale and dynamism to our business.

All these factors combined leave us optimistic about our future prospects.

Balance Sheet - OK overall. NTAV is £29.6m, or £38.7m if we eliminate deferred tax (which is often related to intangible assets, so it makes sense to get rid of it).

Net debt is negligible, at £0.3m.

Working capital looks heavy - with both inventories and receivables having grown a lot, so these need to come down in future.

Note there is a large increase in capitalised development spend, at £8.4m (LY: £4.9m) which flatters profits, and renders EBITDA meaningless.

My opinion - this is an impressive company, which we like here at the SCVR.

My main worry was that the big pandemic boost might have unwound, as it has for many other companies. However in this case, TUNE has held on to most of that growth.

Overall, I think the shares look fairly priced right now. In the past it has commanded a premium valuation, so there could be upside from a re-rating, possibly?

I’ve been told by musicians that TUNE’s products are excellent, innovative, and they command good pricing power, as we can see from the good profit margins. So it looks a quality business, at what seems a reasonable valuation. I could see this share being a decent candidate for inclusion in a portfolio of high quality, long-term investments. Thumbs up from me.

Graham’s Section:

S&U (LON:SUS)

Share price: 2100p (pre-market)

Market cap: £255m

This is the motor finance and property lender managed by the Coombs family. We haven’t had an update since August.

Fortunately, trading has been good since then:

S&U continues to trade well despite a period of economic and political chaos unprecedented in most of our lifetimes. A change of government and of economic strategy, rising inflation, taxation and interest rates and an incipient recession is not exactly the ideal economic landscape for any business.

Nevertheless, trading is very good, focusing on the excellent quality of our customer relationships and the receivables which we derive from them.

Total group receivables continue to rise strongly and now stand at £404m, “with continued good collections and profitability during the period”.

At the most recent year-end (January 2022), total receivables were just £323m. So that’s a 25% increase, without making any acquisitions.

Motor Finance - profitability has been in line with expectations. Higher revenues are offset by “increased customer servicing and collection costs, designed both to protect customer collections quality and to retain staff as living costs rise”.

There has been no problem with customer defaults yet, as bad debts remain below budget. In light of the cost-of-living crisis, the loan underwriting criteria are constantly being revised.

Property Bridging (“Aspen”) - this newer business continues to grow at an impressive pace. Receivables are now at £108m (from £64m in January 2022). Given the volatility in the housing market, I was interested to read how Aspen might have been affected:

Credit quality at Aspen is strong, although refinance arrangements and legal processes are taking longer than usual. The extended beyond term list remains small and there are only 7 technically defaulted accounts as customer repayments during the period have been good.

Higher bank rate and interest costs mean that loan rate increases have been made to protect Aspen's margins.

Outlook - Anthony Coombs gives nothing away in today’s outlook statement.

My view

I have no reason to change my view on this stock. The property bridging division could be seen as a potential area of vulnerability, given that it lacks the track record of S&U’s motor finance division. So it may require some additional monitoring by investors.

And this property division, known as “Aspen”, is growing at a fierce rate. S&U has increased the use of its borrowing facilities and ploughed additional funding of £43m into it this year. It now accounts for a quarter of S&U’s entire receivables book: if it keeps going at this rate, it won’t be long before it matches the size of the motor finance division!

I would like to do a bit more digging into Aspen, to understand better how they are managing risk. But I believe that S&U as a whole is very well-capitalised, with a large equity cushion to allow for any mishaps.

So I continue to view these shares as offering good value. They trade at only a modest premium to book despite a remarkable track record which includes 30 years of dividends and an attractive return on equity.

Numis (LON:NUM)

Share price: 183p (-0.6%)

Market cap: £202m

This investment bank’s share price has weakened considerably since the last occasion that I covered it, in July. It has fallen back to Covid-era lows, which were a great buying opportunity:

In July, I noted that Numis was still trading at a significant premium to book value. On balance I thought that was fair, given the strength of its name in the industry.

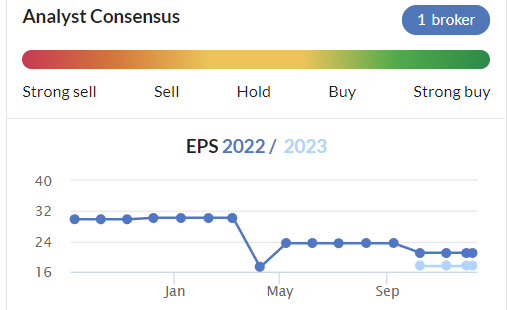

However, it has missed the expectations which prevailed then, for FY September 2022.

- Revenues: expectations were £145.8m. Actual: £144.2m.

- PBT: expectations were £25.1m. Actual: £20.9m.

Expectations for 2023 are now subdued, too (the light blue line):

These full-year results contain some stark figures:

- Revenues down 33%, as “market conditions deteriorated from highly supportive levels”.

- PBT down 72%, “reflecting operational gearing in the business”.

UK equity trading volumes fell to a 10 year low (!).

Outlook

The capital markets outlook remains challenging with deal volumes remaining subdued and unfavourable conditions persisting as the market digests the impact of sustained inflation and higher interest rates. However, momentum in our M&A business has been maintained in FY23 with a strong near-term pipeline of transactions due to complete in the first half of the year. Our equities business has benefited from an improved financial performance in the first two months of FY23, driven by strong trading gains.

The last sentence offers some light at the end of the tunnel. Maybe, just maybe, bear market sentiment reached a low point below which it could not fall any further?

Balance sheet

Net assets are £185m and cash is £106m. We are fast approaching the territory where this becomes a “deep value” stock!

Strategy

Investment banking revenues were down 39% in FY 2022, as the UK IPO market ground to a halt. But the outcome would have been worse had Numis not developed businesses in M&A advisory and fundraising for private companies. These activities helped to pick up some of the slack although Numis says that even the private market slowed down in H2:

…the downturn in public markets, notably the de-rating in listed growth stocks, had a corresponding impact on private markets in the second half of the year. This resulted in deals taking longer to execute and some transactions being postponed or aborted which impacted second half revenues.

EU expansion - Numis now has an office in Dublin, from which it will look to grow its European institutional client base.

My view

I hold Numis in high regard and now that its market cap has fallen so close to book value, I can’t help but view this as a possible buying opportunity. The fact that it still earned PBT of over £20m, in some of the worst financial conditions imaginable for small-caps and mid-caps, demonstrates to me its resilience.

It’s a well-diversified business and in the good times, I expect it to make much more than £20m of annual PBT. So I have to rate these shares positively at a market cap of £200m and with very strong balance sheet support.

The stock already passes two of Stockopedia’s Ben Graham stock screens: The Ben Graham Enterprising Investor Screen and the Ben Graham Deep Value Checklist.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.