Good morning! It's Roland here with today's report, I'm picking up the reins from Graham. Today's report is now finished (11.00).

In the last few days before Christmas, company announcements are thinning out as the City prepares to take some time off! However, there are a handful of stories in our small-cap universe that merit a look.

Agenda

Roland's Section:

Goodwin (LON:GDWN)(£246m) - today's half-year results from this family-controlled British engineering group impress me. The order book is significantly increased and profitability has also improved. Although this is too illiquid for traders, I think Goodwin is a class act, and could be attractive as a long-term compounder.

Xpediator (LON:XPD) (£53m)(+25% ) [no section below] - this fast-growing logistics group has received a possible offer of 42p per share from a private-equity consortium led by the firm's former chief executive, Stephen Blyth.

Mr Blyth remains the largest shareholder through his vehicle Cogels Investments, which I believe has a 26% stake. No firm proposal has been made yet, but this looks opportunistic to me after the stock's recent sell off -- XPD traded over 60p earlier this year and hit 80p in 2021.

The latest trading update was positive and confirmed full-year guidance. The shares still don't look expensive to me, so I would be minded to continue holding here if I was invested.

Nanoco (LON:NANO) (£128m)(-1%) [no section below] - AGM statement from this nanomaterials specialist. Financial performance during the four months since August is said to have been "comfortably in line with the Board's expectations".

Nanoco says it is continuing to deliver R&D services under a number of contracted programmes with customers in the sensing market. Management has "a high level of confidence" that the firm will receive production orders in calendar 2023, based on visibility of customer validation plans.

An ongoing patent infringement case against Samsung is also noted as a possible source of "potentially significant shareholder value".

However, for now Nanoco remains in the jam tomorrow camp, as far as I can see. Consensus forecasts show full-year revenue of just £2.9m, with a £3m loss. Although the firm appears to have enough cash to operate for the coming year, I wouldn't bet against a further fundraise here. Nanoco is too speculative to be of interest to me.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Roland's section:

Goodwin (LON:GDWN)

Share price: 3,150p (10am)

Market cap: £246m

Shares in this 139-year-old family-controlled engineering group have 30-bagged over the last 20 years. Today’s results look very positive to me, and suggest to me that Goodwin’s long-term growth trend may have further to run.

Goodwin’s operations are divided into two divisions:

- Mechanical Engineering (47% of H1 profit): produces mechanical and electronic components and complete systems for industries including defence, mining and energy (including nuclear). Examples include air-traffic control radar and components for naval and military aviation programmes.

- Refractory Engineering (53% of H1 profit): produces mineral-based products to sectors including mining, construction, and jewellery. Examples include products such as vermiculite, silica sands, jewellery casting plasters and moulding rubbers.

Profit margins are notably higher in the refractory division (~16%) than the mechanical business (~9%).

Commentary on recent trading and order intake is very positive:

“I am pleased to report that at the time of writing the workload has increased to £242 million (2021: £157 million). This increase relates to the materialisation of some of the major projects that the Mechanical Engineering Division has been pursuing within the military and nuclear waste re-processing markets.”

Chairman Timothy Goodwin notes that Goodwin has been moving away from oil and gas into business streams that are more likely to avoid the effects of a global recession he thinks is “almost certainly going to feature over the next two years”.

Financial highlights: Today’s numbers show a healthy performance during the six months to 31 October.

- Revenue +18.8% to £89.3m

- Trading profit +17.9% to £9.1m

- Trading profit margin: 10.2%

- Pre-tax profit +58.4% to £12.2m

- Earnings per share + 58% to 113.9p

Trading profit represents operating profit excluding unrealised derivative gains, so it's a realistic measure of operating profitability.

The company’s reported pre-tax profit for the period was distorted by an unrealised £3.1m fair value gain on an interest rate swap. This derivative caps the group’s interest rate at 1% on the first £30m of debt and extends to August 2031. I’m not sure when the swap was taken out, but it’s clearly likely to pay off handsomely for Goodwin.

Net debt rose by £11.3m to £46.1m during the period and free cash flow was negative. This is due to ongoing investment in increased inventories and CO2 emission projects, such as solar panels. Based on current electricity prices, the payback period for a recent solar panel project is expected to be just two years – a good investment.

I don't see have any concerns about Goodwin's debt levels or balance sheet.

Inventories/working capital: inventories have risen by £6m to £43.3m over the last 12 months, which I estimate is equivalent to around three months’ supply. The company says this investment has “significantly aided the Group’s ability to meet [customer] demand”.

Outlook: although macroeconomic risks are a concern, the company says that "activity and profitability levels are expected to increase over the next twelve months as a result of the increased workload."

Goodwin doesn't appear to pay for broker forecasts and the firm hasn't provided any guidance on the timeline for delivery of its increased order book.

However, past years have seen a fairly even split between H1 and H2 profits. Assuming this remains the case, I think it's reasonable to expect the 18% increase in H1 profits to be extended to the full-year result.

My view: I’ve not spent a lot of time looking at Goodwin before, but I can see plenty to like here. This appears to be a good, well-run business, operating in some attractive niches.

The current valuation does not look unreasonable to me:

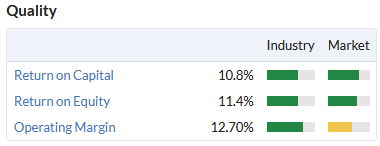

Quality metrics are fairly good for a capital-intensive manufacturer, too:

Liquidity is limited, with a free float of just 33% and an indicated spread of 5%.

However, for investors looking for businesses with the ability to deliver long-term compound growth, I think Goodwin could be worth further investigation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.