Good morning from Paul & Graham! Almost Christmas :-)

Just FYI, if the markets are open on any particular day over the Christmas/New Year break, then there should be an SCVR, but it won't necessarily be on time, depending on how much Malbec and Baileys has been swilling around in the Scott household the night before.

Agenda

Paul's Section:

Yourgene Health (LON:YGEN) - we've only covered this speculative, cash-burning company a couple of times here before. Yesterday afternoon it announced a horrific fundraise, at an 83% discount, along with poor interim results. So I'm flagging this up as another example of how cash-hungry speculative companies are in the last chance saloon right now, with discounts of 80%+ seemingly becoming the norm. So once again, I urge readers to check every position in your portfolios, and chuck out the ones that need to raise fresh equity from a position of weakness. (more detail below)

WANdisco (LON:WAND) - I covered this one yesterday, with a big contract win. There's another one announced to day! Although I'm confused as to why the revenue guidance for FY 12/2022 still seems so small. This share does look very interesting, but it's absolutely impossible for me to value at this stage, as it remains heavily loss-making. It's tempting to have a small punt on it though. (more detail below)

Tekmar (LON:TGP) [quick comment] - up 52% to 10.25p, which caught my eye. I’ve not looked at TGP since June, when it issued a pretty awful update, and put itself up for sale. Getting up to speed today, I see there have been several updates since June, and it seems to have an interested party that might make a strategic investment, to sort out the finances - but at what price, if it happens at all? Meanwhile the bank has been supportive, and liquidity looks OK. Today there is news of a big-sounding (no details provided) contract win for the North Sea Dogger Bank offshore windfarm (set to be the largest in the world, amazingly). My view - this looks an interesting, albeit risky special situation. (no section below)

Graham's Section:

600 (LON:SIXH) (£11m) - I’ve done my best to approach this one with an open mind. It fixed its balance sheet this year with the help of a disposal, but I’m not sure that its remaining businesses are big or profitable enough, on their own, to justify a stock market listing. The financial results for H1 certainly suggest that they would be much better off without all the expenses that go with being a publicly traded company. As things stand, I’m afraid I can’t find any good reasons for investors to want to get involved with this one. (more detail below)

Ground Rents Income Fund (LON:GRIO) (£46m) (unch.) [no section below] - this investment trust, currently managed by Schroders, has never been mentioned here before. I just can’t help noticing that its market cap is only £46m, versus an independent valuation of its assets at £109m as of September 2022 (prior to the payment of a small dividend). After accounting for leverage, balance sheet net assets were £90m as of the most recent half-year report (March 2022).

There are usually reasons for such a discount and in this case we have legal uncertainty due to new regulations around building standards and the funding of building defects. GRIO is a landlord, not a developer, but the new Building Safety Act has nevertheless “increased the challenges associated with resolving complex building safety issues”. There are many legacy issues involved with this one, and it needs to survive a continuation vote (which would, if shareholders allowed it, force the liquidation of the trust’s portfolio at depressed prices). To add insult to injury, the uncertainties around valuation could cause the publication of full-year results to be delayed. Not for the faint-hearted, this! But could its problems be priced in at this savage discount to book value given that it offers a diversified portfolio of ground rents, traditionally considered to be safe and steady investments? [no section below]

NWF (LON:NWF) (£132m) - a solid update from the fuel and food distributor NWF. Volumes haven’t improved but price increases and margins are strong, resulting in H1 performance ahead of expectations. Full-year estimates are left unchanged as we head into the important winter months. NWF has been a solid performer and it also offers an acquisition growth story. The company has made a new £10m purchase of a fuel distributor that will increase its market share and improve its geographic coverage. For me, the shares are priced correctly at current levels but its excellent track record might still attract new investors, even after the share price gains achieved in 2022. (more detail below)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section

Yourgene Health (LON:YGEN)

0.38p (down 80% yesterday)

Market cap £2.7m

I’ve only reported here on this share twice in the 10 years the SCVRs have existed. That’s because it’s always been unclear if the company had a viable business model, with repeated losses and cash burn. Also we don’t normally cover speculative medical sector shares, as it requires specialist sector knowledge I think. YGEN hit a nice patch during the pandemic, with covid testing, but even then couldn’t turn a profit, and that’s fizzled out now.

Interim Results - issued yesterday afternoon look poor to me. Revenues have dropped a lot, and losses and cashflow are both poor, with the cash pile largely disappearing, from £8.4m at the start of the 6 months, and only £2.4m left by the end, at end Sept 2022.

There was also £4.1m of borrowings (excluding lease liabilities) - a loan from SVB (Silicon Valley Bank). In brief, it’s run out of cash, so has been forced into doing a disastrous…

Fundraising - a placing, Director subscription, and a retail offer through BookBuild (I can’t find any details on this platform, do any readers know it?) to raise “a minimum of £5m” in total. (see update further down here)

Here’s the killer - the price is just 0.3p per share, a disastrous discount of c.84% to the previous share price. So existing equity is almost wiped out.

My opinion - as we’ve discussed here several times recently, we are currently in a savage market for companies which need to raise fresh equity. Institutions are generally unwilling to provide more funding for companies that are disappointing with their performance & outlook. We can exit those shares, but institutions can’t, due to lack of market liquidity. So they just have to sit and watch their investments go down the pan. If those companies need more cash, the institutions just name their price. Discounts of 80%+ are now becoming the norm.

For this reason, I urge all readers to once again review everything in our portfolios, and chuck out anything that looks under-funded - especially the smallest stuff, with repeated losses, and cash burn. We’re already seeing a mass exodus of such shares from the market, with some de-listing, and others going bust. Even the ones that survive are now seeing existing shareholders almost wiped out by deeply discounted fundraises. Why take the risk? As much as anything, this is a memo to self, as I have a couple of things that are probably under-funded.

Update this morning - successful completion of the placing & subscription. It seems to have raised more than originally indicated, £6.4m raised, plus possibly £1.0m more from the retail offer (details to be announced tomorrow). It doesn't seem to be an open offer, for existing shareholders, but I may be wrong about that, as we don't yet have details. So existing shareholders have to decide whether to throw good money after bad, or just walk away.

A deal like this is effectively transferring ownership of the business to the (mainly institutions) who are prepared to put fresh money in now, and will end up owning the bulk of the company. Existing shareholders are watered right down. The next step after that? Either commercial success (how likely is that, given the track record?!) or a de-listing in 2023 after the share price has dropped even further. Maybe a final fundraise in some punitive form, like convertible loans, then a de-listing?

I sometimes wonder if institutions want failed shares delisted, so they can sweep their embarrassing mistakes under the carpet, and deal with the wreckage away from the glare of public market scrutiny? Everyone makes mistakes, even fund managers.

Director dealings - Interestingly, the Directors don't seem to have sold any shares all the way down, so they must have believed in the company, and are stumping up £1m in the current fundraising. They were repeat buyers of shares in the market, although looking at the list, all quite small deals - nothing over £100k individually (which are the deals that make me sit up and take notice).

WANdisco (LON:WAND)

890p (up 2% at 08:14)

Market cap £614m

$12.7m Contract and Trading Update

The newsflow at this software company is getting more remarkable by the day. We’ve already covered it 7 times this year here in the SCVRs. The first 3 times were bearish, due to terrible figures and cash burn. But we started to see the newsflow becoming more positive from late June onwards. So when the facts change, we also change our view.

I covered it yesterday here, with announcement of a $31m deal, half being paid up-front by the customer - very positive to be getting a significant part of the deal up-front in my opinion, and that could also defer or negate completely the need for another fundraise, if deals like this keep flowing.

Today’s deal announcement is different, as it’s a one-off, with c.$10m revenues being recognised this year, FY 12/2022 - unusual, as it’s a lot additional revenue to secure in the dying days of a financial year.

This sounds highly impressive -

WANdisco was chosen due to its proven ability to migrate petabyte scale data.

The customer is an automotive manufacturer, and this sector is seen as a “core and growing” market for WAND.

Revised guidance -

Following this new Agreement, the Board expects that FY22 revenues will be significantly ahead of market expectations and no less than $19m. In addition, bookings for FY22 are expected to be in excess of $116m.

Given all the contract wins, FY 12/2022 revenues of only $19m seems very small. Particularly as c.$10m of that seems to be coming from this one contract announced today. That seems to imply that revenues would only have been about $9m without it, well below $13.9m consensus forecast revenues. So maybe this contract has saved the day? WAND is too keen on announcing bookings, when it's really revenue and profit that matters most.

Also with bookings, we need to be told the timeframe over which they will turn into revenues. E.g. if it's a 10-year contract, then the annual revenues even on $116m wouldn't move the dial much on revenues, and would still leave the company heavily loss-making.

Confident outlook -

As we exit 2022, we look forward to 2023 with confidence; not only do we expect to convert the significant opportunities we have in our pipeline but we hope to see increased consumption from all of the agreements signed in 2022, providing increased revenue visibility as we progress through the year."

My opinion - the large scale of recent contract wins suggests to me that WAND has reached a key, positive tipping point, after years of trying. Therefore, the emphasis for me is less about the dismal historic financial performance, and more on the upside potential.

That said, even on upwardly revised forecasts, it’s still set to be heavily loss-making both in 2022 and 2023. So bulls need to be very sure that the big contract announcements about bookings are actually going to turn into revenues, and ultimately profits.

Conceptually though, if a customer is prepared to pay $12.7m just to move some data as a one-off, then it does suggest WAND could have some really special (and hence valuable) technology. Providing of course that it doesn't get overtaken by a competitor that can do the same thing, or better? Nothing stands still after all, especially in IT.

This share looks a very interesting idea to me, but I don’t have the expertise to assess the software. There were big spikes up in the share price in 2013 and 2018, both of which completely fizzled out. Although from memory, the bookings announced were nothing like on the scale we’re currently seeing.

I’m tempted to have a small punt on this, but with my eyes open, in that the share price could be very volatile.

Note that the share count has roughly doubled since 2016.

Graham’s Section:

600 (LON:SIXH)

Share price: 9.55p (-19%)

Market cap: £11m

It’s been a while since we’ve covered this small engineering group that specialises in laser systems.

The last time I wrote about this one, I described its balance sheet as “a mess”, with net debt in the region of $17m-18m (too high relative to its profitability, in my opinion).

It found a solution to this problem: it sold an entire operating division for $21m, and flipped over to a net cash position.

Here are the results for the six months to September 2022:

- Revenues +12% to $17m

- Net underlying operating loss $0.7m (H1 last year: profit $0.7m)

- Back into a net debt position of $2.5m.

It’s unfortunate to see it back in net debt, but at least this is a manageable number, unlike what it was carrying before!

Order book - this has been “maintained”, if you exclude a large one-off order from last year. So it is actually down on last year.

I’m afraid I consider this to be dubious order book reporting. If you go to last year’s interim results, they did not adjust their order book for a large one-off order. Quite the contrary! They said things like:

…our orderbook not only reflects increased demand for our products, but also an improvement in the quality of future earnings.

If you study enough companies, you’ll notice this from time to time: adjustments being made when “one-off” orders in the prior year don’t repeat, but no mention of any orders being “one-off” in nature during the prior year!

Chairman comment - profitability, according to the Chairman, has been impacted by “supply issues and cost inflation resulting from the aftermath of the Covid pandemic and conflict in Ukraine”.

Balance sheet - inventories have increased by $2m to $10m, as the company has sought to secure supply and hedge against inflation. It also holds more “work in progress” as manufacturing times are longer.

Receivables are also up $2.4m, to $9m. The explanation below doesn’t sound great from a shareholder perspective, but hopefully new orders can be agreed on better terms:

a number of orders were taken during the pandemic… with reduced margins and extended terms to cover overheads and keep our skilled workforce together which, due to the long lead times on manufacturing, are only just working through the system.

Outlook

The outlook puts a positive spin on fairly poor results:

Whilst there will continue to be concerns over a recession, COVID variants and supply chain disruption, given the continuing good orderbook activity and backlog and the move to higher specification and custom products, the Board believes the Group is more resilient to market changes and this strategy will lead to improved shareholder value in the future.

My view

The market is deeply unimpressed and has marked these shares down by about 20% this morning.

While the company did sidestep insolvency by offloading a large division, it’s not clear to me that the remaining operations are worthy of a stock market listing.

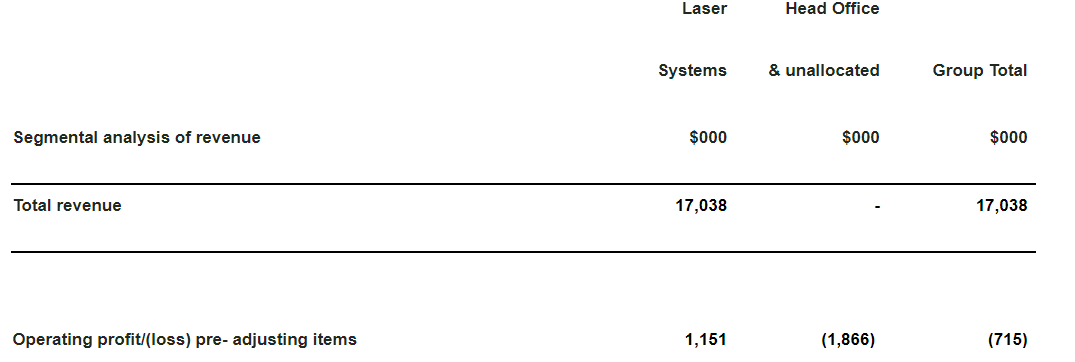

To see what I mean, here’s the “segmental” analysis of the company’s H1 results:

What this says is that if you exclude 600 Plc and focus only on the operating subsidiaries, the company did make a profit in H1.

However, all the hangers-on in Head Office, and overhead costs, added up to nearly £2m, resulting in a net loss for the period.

With the company now so small, perhaps the next step is for it to find a graceful way to delist and save on the costs associated with a public listing and other corporate overheads? Perhaps a buyer can be found? Unless it’s going to raise money and go for growth (probably impossible in this environment), then I think it needs to shut down Head Office as a priority.

But I’m not running this company. Instead of becoming a lean private business, it looks like it’s going to remain a marginally-profitable or unprofitable PLC, for the time being.

I’m afraid I can’t find any attractions with this share.

NWF (LON:NWF)

Share price: 266.9p (+5%)

Market cap: £132m

This is a distributor of fuel, food and animal feed (feeding one in six cows!).

Trading update - all divisions ahead of expectations in H1

Volumes actually fell in both the fuel and the animal feed divisions, but NWF has benefited from inflationary price increases and from strong margins. As I keep saying - these commodities are a safe haven in times of high inflation.

Outlook - unchanged for the full year. Despite the strong start, the company isn’t willing to raise expectations at this point. The share price is up 5% anyway, so investors are happy, but it seems prudent for management to wait and see how the winter goes. No need to assume that trading will remain this strong for the rest of the year.

Acquisition - NWF announces the £10m purchase of a fuel distributor based in Oxfordshire, paid out of its existing cash resources and bank facilities.

The Acquisition further expands and infills NWF's geographic coverage of its Fuels business within the UK and is aligned to the Group's development strategy of consolidating the highly fragmented fuels market whilst expanding its existing geographical footprint.

Sweetfields made PBT of £1.2m in FY 2021. If that’s a reliable indicator of profitability, I don’t think anyone can complain too loudly about the price paid (and duplicate costs will be eliminated, boosting profitability further).

CEO comment

The industry remains highly fragmented, with many small operators, which provides us with further opportunities to consolidate the market and increase our market share. Our pipeline of acquisition prospects remains healthy and this remains a focus for our development activity.

My view

This has been a steady performer: really low margins, but it has continued grinding out profits through the years:

Do I trust the acquisition strategy - it seems like they can afford it, so why not? Increasing market share by adding on complementary businesses can’t be a bad thing, if it’s done without taking on too much financial risk or complexity.

And it has offered wonderful inflation protection, with the stock price increasing in a year which has seen so many other businesses suffer (Momentum Rank: 91).

For me, the earnings multiple looks about right at the current level, given that it’s a distribution business, but it might still be low enough to attract new investors who want to hold it long-term. The StockRank is a magnificent 98.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.