Good morning from Paul (hardly any news, so Graham's doing other stuff today). There's hardly any news today, so this report is now finished.

We're braced for a very busy month, with lots of 2022 trading updates about to hit us, some of which are bound to be profit warnings, given current tough macro conditions.

Agenda

Paul's Section:

Hospitality sector - the Propel daily news email today contains alarming news for trading in Dec 2022 for late night bar operators - a flash survey of 200 nightclubs and bars shows that revenues were down 20% on pre-covid (Dec 2019). That’s going to leave many struggling to survive in 2023. This whole sector looks really grim at the moment, with reduced demand colliding with much higher costs (especially wages and energy). It’s difficult to see much changing any time soon - the days of generous Govt support measures seem to be over, and disposable incomes seem likely to remain under pressure. So I think we need to brace for many bars going bust in 2023, and the ones remaining just hoping to gain more market share in a smaller market. It's far too expensive to eat/drink out these days, in my opinion. Hence I'm very worried about this whole sector.

Heiq (LON:HEIQ) - a nasty profit warning from this innovative fabrics group, which has missed its 2022 numbers by a long way, citing a plunge in demand in Q4. We've never liked this share here at the SCVR, and now the company is loss-making, it's difficult to see any bull case at all. On the plus side, the balance sheet looks robust overall, with net cash. Although inventories & receivables look too high, so there might be some nasties lurking in those. It's just a punt now really, on a possible recovery, so might be of interest to traders? For me though, I'll continue avoiding it, so a thumbs down I'm afraid, on fundamentals.

Concurrent Technologies (LON:CNC) - a rather underwhelming update for 2022, with both H1 and now H2 only being just above breakeven. The cash pile has depleted a lot too, although credible reasons are provided (inventory build due to supply chain problems), hence that should reverse in future. The main interest here is a bulging order book, so a much better performance is credibly expected in 2023. I think the valuation looks solidly underpinned for now, although further upside would need out-performance against existing forecasts to justify it.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Heiq (LON:HEIQ)

55p (pre market open) - update at 08:53: down 52% to 26.5p

Market cap £77m - update: £37m now, so £40m wiped off the value of the company today.

This company floated in Dec 2020, reversing into a listed shell called Auctus Growth.

I’ve only reviewed HEIQ twice, most recently being underwhelmed by interims here on 29 Sept 2021. We didn’t write about HEIQ in 2022 at all, as the figures didn’t look of interest. Interims to 6/2022 showed another fall in operating profit, to only $1.2m. It expressed “cautious optimism” that FY 12/2022 forecasts would be met.

Today’s news is this -

HeiQ Plc (LSE: HEIQ), a leading company in materials innovation and hygiene technologies, announces a trading update for its year ended 31 December 2022 (FY 2022), as well as the acquisition of Tarn-Pure Holdings Ltd.

I’ll summarise today’s update (profit warning) -

Q3 trading “remained reasonable”

Q4 saw “significant deterioration” in demand.

Reasons?

- Customers over-stocked, and themselves saw reduced demand.

- China especially bad, with sales down 50% vs forecast (blames regional covid lockdowns)

- Brands “more hesitant” to buy innovative products - delayed orders for new products.

Revised guidance - FY 12/2022 revenues to be $54-55m, c.20% below market expectations. Gross margin also lower at c.47-48%.

Now loss-making - expecting $(2.5)m to $(3.5)m loss before tax for the year. This compares with profits of $2.7m in 2021, and $7.1m in 2020. So a very poor trend.

Stockopedia is showing broker consensus at a $4.1m profit after tax for FY 12/2022, so this is a big miss today, ending up loss-making.

Also note that HEIQ made a $1.2m PBT in H1, so that means H2 is a loss of $(3.7)m to $(4.7)m - clearly bad news.

This guidance is preliminary, and subject to audit, as I would expect coming immediately after the year end.

A small acquisition is also mentioned, for £850k.

Outlook - I’d say this is not great, but not a disaster either - if it can strip out a lot of cost, then returning to profit in FY 12/2023 would be a relatively OK outcome - if that happens of course, which it might not (I wouldn't rely on anything management say, given the track record of over-confidence) -

The Industry expects global markets to continue to experience low demand for at least another six to nine months.

The Company also expects trading for FY 2023 to be below market guidance, with anticipated sales and gross margins maintained at FY 2022 levels.

Given the macroeconomic headwinds the Company has started to implement cost savings and will continue to review and adapt its cost basis with the objective of returning to profit before tax in FY 2023.

Is it going bust? I’d say no. The last balance sheet, at 6/2022 is quite strong, with cash of $9.5m, less $2.2m in borrowings.

I do have concerns over both inventories & receivables looking too high at 6/2022. The interims commentary says receivables reduced after the period end, but that some Chinese distributors were paying slowly - that worries me, because today's slow payments often develop into tomorrow's defaults.

Overall though, I’d say the balance sheet looks strong enough to weather a period of poor trading, so no immediate concerns here.

My opinion - how on earth do we value HEIQ shares? It now seems as if the previous big profit in 2020 was a one-off, and it’s now loss-making, and having to cut costs to target breakeven. So the bull case (which was always wobbly in my opinion, see our archive here) has gone out of the window now.

Looking back at my notes, this SCVR from 27 Jan 2021 is interesting - where a presentation by management spectacularly back-fired, with the share price plunging the next day by 23%. I remember it actually, and commented at the time here that a one-off good year didn’t convince me at all that the company was worth c.£200m.

So HEIQ looks like yet another opportunistic float at peak earnings, stuffing investors with over-priced shares that subsequently have gradually collapsed, as profits melted away, now into losses.

For that reason, I don’t think I’d be interested in investing in this share at any price really - I’m not convinced it has a viable business, and I see the poor financial track record (despite plenty of ramping about the company’s potential) as off-putting.

It’s a possible recovery situation, but why would we want to take the risk of things getting worse?

Note the very low StockRank of 16, and the “Sucker Stock” classification on Stockopedia. It also only qualified for 1 screen - the Beneish M-Score Screen for short selling (worth a look actually, it's here).

Hence it has to be a thumbs down from me.

The share price is down 53% at the time of writing, at 25.5p, so it’s a difficult decision for shareholders, whether to just ditch it and move on, or tuck away and hope for a recovery at some stage - not entirely a bad idea, given that solvency risk isn’t an issue (assuming that the accounts are true).

Concurrent Technologies (LON:CNC)

77.5p (up 7% at 10:27)

Market cap £57m

We looked at CNC 3 times in 2022, so I’ve just re-read our articles here to get up to speed quickly. I liked the strong balance sheet, and saw positive potential. Although supply chain problems blunted performance, with only breakeven for H1 to 6/2022, but upbeat outlook comments indicating good interest in, and orders for, new products.

Here’s the latest news today -

Concurrent Technologies Plc (AIM: CNC), a world-leading specialist in the design and manufacture of high-end embedded computer systems and boards for critical applications, is pleased to announce an update on trading for the year ending 31 December 2022 ("FY22").

Revenues c.10% ahead of market expectations of £16m, so that’s about £17.6m actual revenues, which gives us a split of £7.4m H1, and £10.2m H2, a useful improvement in H2.

Profit before tax “at least in line with market expectations” of £0.1m - hmmm, not very exciting, so that’s effectively breakeven in H1 and breakeven in H2.

Supply chain - shortages extended lead times, causing delays to product manufacturing & hence revenues. Inventories increased to smooth over shortages.

Although they’re not out of the woods -

Whilst overall supply chains are seeing a degree of recovery, the Company is in many cases dependent on some very specific components, and hence FY23 forecasts remain prudently cautious.

Cash position - has deteriorated a lot, but for reasonable-sounding reasons. Note that cash was £9.3m at 6/2022, so this is a big fall in H2 -

Cash was depleted throughout the year as a result of the Company's declared strategy of investing in R&D, systems, and growth of its home markets in the US and UK. The additional investment in components holdings to mitigate supply shortages, resulted in a cash low point at the end of FY22, at a value of circa £4M.

With the increased shipping of product in November and December 2022, the Company anticipates strong cash generation at the start of FY23, with further episodes of cash generation as components become more available

I think that’s OK, and am happy with the explanations given for the temporary drop in cash. It’s good to be in a position where there was a decent cash surplus to start with, which has absorbed these issues without increasing risk.

Growth strategy confirmed, both organic and by acquisitions.

Order book - so far, I’ve been underwhelmed with this trading update, but the order book details sound much more positive. With c.50% gross margins, it’s easy to see how revenues could step up once supply shortages ease, resulting in a nice operationally geared boost to profits -

Following a record order intake in FY21 of £25M, the Company is proud to announce order intake for FY22 in excess of £31M, an increase of over 25%. The FY22 closing backlog was also very strong, in excess of £26M. These figures indicate that, as supply chains ease, the Company has potential for significant revenue growth. A further cause for optimism is that the Company expects to run double shifts throughout Q1 FY23, maintaining its increased capacity.

2022 order intake of >£31m compares very favourably indeed with reported revenues of c.£17.6m. A closing order book of >£26m means that I imagine 2023 revenues should be strongly up on the £17.6m in 2022. Definite grounds for expecting a much better 2023, based on firm orders, not just hope. I like that!

Dividends - nothing for 2022, but that looks a temporary issue, given that previously divis have been fairly generous. So I would invest on the basis that divis should return in 2023, that looks a reasonable assumption taking everything into account.

Broker update - many thanks to Cenkos for an update note, which pencils in £22.1m revenues, and £2.7m adj PBT for FY 12/2023. That looks achievable to me, and might even be beaten, given the strong closing order book more than covering the full year’s forecast for 2023.

I don’t find PER valuations particularly useful in situations like this, where profit is rebounding from a breakeven starting point, as the potential range of outcomes can be quite wide. But it’s worth reasonableness-testing the numbers. In this case, Cenkos estimates 3.7p adj EPS, on what I think looks quite conservative, which is a PER of 21x - not cheap, but shareholders will no doubt be expecting that the forecasts are beaten, a not unreasonable assumption in my view.

My opinion - this looks pretty good. I think I’ll give it a thumbs up, since the downside risk seems so well covered by the big order book, and upbeat comments about demand for new products.

I also like the strong balance sheet, so no risk of insolvency or dilution (unless they decide to do an acquisition that needs funding).

Purely looking at the numbers & commentary, I think this share looks worthy of readers doing the more detailed research necessary to assess what the company’s longer-term potential might be.

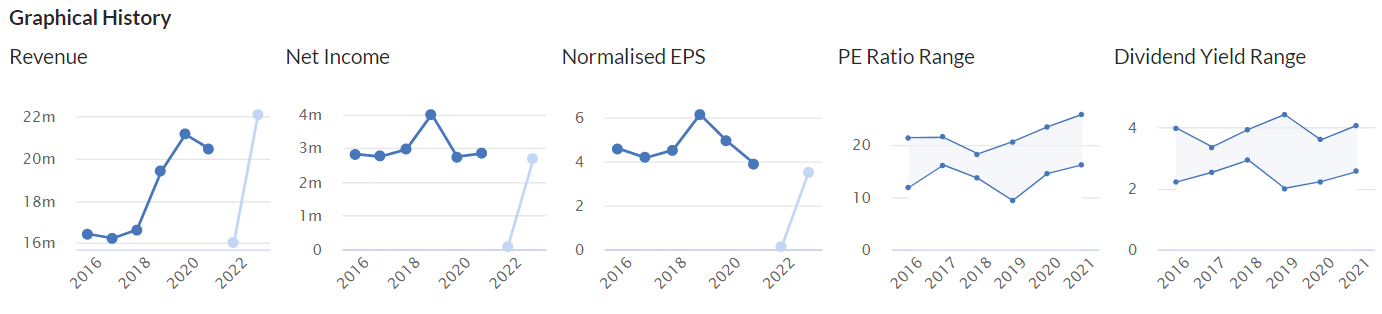

As the Stockopedia graphs below show, in the past it’s been a steady performer, but not much evidence of growth. It could get more exciting if management’s growth plans do result in a faster pace of profit growth. It needs that to happen, as the £57m market cap currently is quite hefty for a company that has only produced typically £3m pa net profits in the past.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.