Good morning from Paul & Graham!

Today's report is now finished.

Weekend podcast is here. Also the typed version is here for Stockopedia subscribers. Thank you for all the feedback, much appreciated! Most people seem to like them, and it's a useful process for me too, collecting my thoughts after each week's busy report writing.

My top 20 small cap ideas - I've also written another post here, which lists my top 20 watchlist ideas for small caps (with a value/GARP focus). I'll also publish another article with my top 20 speculative small/micro cap ideas, for more adventurous punters, next weekend.

When I spot good share ideas writing these reports, I add them to a watchlist, so I can monitor them, and consider a purchase. This weekend, I reviewed my watchlist, and thought it might be helpful to readers if I distilled it down to my best 20 ideas for companies that I think have solid finances, low risk of dilution or insolvency, are trading well, and look cheap or reasonably priced. These are listed in this article.

As always, I have no idea what the share prices will do, because facts, and market sentiment change in real time. Some shares on the list could do well, others won't - again, that is completely normal. But I hope it's an interesting list with some ideas for readers to research further, with explanations from me as to why the shares could be interesting. I'm hoping that about 60% might do OK to well, and 40% probably won't do well. As we're going into a recession, there's a heightened risk of profit warnings, so I'm fully expecting some to disappoint on earnings, especially in the first half of 2023. So it's not a list of trades, it's more solid companies that I think should do well medium to longer term, with some bumps along the road expected. There are also plenty of good dividend payers in my top 20 list. Anyway, check it out, and do leave your feedback, and your own lists (top 3, top 10, top 20, whatever you like!) of favourite shares (with explanations as to why) in the reader comments, so we can all share our best ideas.

As always our approach here is to do your own research & take responsibility for your own portfolios. So we're not recommending anything, just sharing ideas and opinions. I know it's tiresome to have to keep endlessly repeating this, but we get a handful of people who, for reasons only known to themselves, seem to have a conspiracy theory that somehow we're secretly recommending things (why on earth would we want to do that??!), which of course is complete nonsense. We want everyone to DYOR, that's the whole point! (not just mindlessly follow tips).

By the way, you don't need to "request access" from me to any of my spreadsheets (which a few people have been doing). Just clicking on the link opens it as a viewer. I obviously won't be granting editor access to anyone, as they could then change things in the spreadsheets. But you can download your own copy locally, and change anything you like within your own copy - or add information & your own notes in new columns, sort by different criteria, etc. The live price formulae in column K can sometimes be temperamental, but are the correct syntax.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda

Paul's Section:

N Brown (LON:BWNG) - my review below looks at the balance sheet in particular, with the shares trading at a huge discount to NTAV. Opportunity, or signs of problems? It announces today a £50m settlement (cost) of the big legal case with Allianz, over mis-sold PPI. That's not a good outcome, being about double the provision on the balance sheet, but it does remove a major uncertainty. There seems enough liquidity to pay it. I think it's a poor quality business, so doesn't interest me, although the huge discount to NTAV, and controlling family shareholdings, might make it a candidate for a takeover bid by the Alliance family. Why would they be generous though?

Nanoco (LON:NANO) [quick comment] (41.25p down 26% at 11:06) - this news has been handled badly I think. Friday’s triumphant announcement about reaching agreement with Samsung (with no specifics) is tempered by an update today saying, “the value and terms of any final agreement are not yet certain”

Also, it’s now guiding us towards expecting a one-off settlement (with “no forward royalties”), and “at the lower end of the range of expectations” than from a jury trial.

This is a much more cautious tone today, and blows a hole in the argument that NANO might have seen major royalties as part of the settlement, which I’ve seen some bulls suggest. Although effectively winning the case through a compromise in its favour could mean negotiated royalties on future sales perhaps? I also very much like that NANO has fought and seemingly won, defending its IP, with a huge organisation Samsung. Why makes me wonder why Samsung doesn’t just buy NANO? Overall - still quite an interesting situation, but I have no way of valuing the company until we get details (which might take a while, as subject to confidentiality, so might have to be gleaned from future accounts). Today's update sounds like NANO is trying to temper investor expectations on the settlement deal. Time will tell! I'm neutral, as I can't value the share without more information.

Anpario (LON:ANP) - profit warning means it looks set to miss FY 12/2022 forecasts by about 25%, by my calculations (I can't find any broker updates, so worked the numbers out myself). Lovely balance sheet. Shares look significantly overpriced now, so I have to give it a thumbs down based purely on lack of growth, and excessive valuation. It could improve in future of course, but why pay up-front for growth that hasn't happened?

Graham's Section:

Frontier Developments (LON:FDEV) (£240m) - a huge profits and revenue warning from this video game designer and publisher. The key F1 Manager title has failed to sell as many titles as expected, and the company slashes its full-year revenue estimate (for FY May 2023) from £135m to only £100m. The operating profit estimate for the year is reduced from £20m to £2m. I still like this company but it’s concerning to see such a massive cut in estimates with only four full months left in the financial year. Ultimately, what this proves is that the stock remains a concentrated bet on a small number of key titles. With the share price now down by over 80% from its peak in January 2021, I remain neutral, leaning towards a positive view. The enterprise value is around £200m and it’s conceivable that operating profit can get back into the £10-20m range over the coming years.

Devolver Digital (LON:DEVO) (£249m) (-5%) [no section below] - continuing the video game theme, this US company listed at 157p in November 2021. As I noted in September, it was not the most promising IPO (it was organised by Zeus, mostly for the purpose of giving existing shareholders an exit). It is now down 60% from the IPO price.

Today’s update for FY December 2022 confirms that revenue recovered in H2, as anticipated. However, “Normalised Adjusted EBITDA” has missed expectations due to the “ongoing cost impact of three underperforming titles”. This EBITDA measure is now expected to come in at $20-22m (previous estimate: $27-32m). That strikes me as quite a large profit warning to suffer after the end of the financial year, especially considering that the prior estimate was reiterated in late September. On top of the weak adjusted EBITDA performance, the company is also expecting “material” cuts to the carrying value of its capitalised development costs, i.e. impairments as previous work turns out to be less valuable than previously assumed. Unfortunately I can’t find any attractions here, as it looks like a poor-quality IPO where maybe not all of the cockroaches have been revealed to shareholders yet?

Paul's Section:

N Brown (LON:BWNG)

27.7p (up 10% at 08:23)

Market cap £129m

This relates to a large, and long-running dispute between BWNG’s subsidiary JD Williams, and insurance company Allianz Insurance, over who is responsible for costs related to mis-selling of PPI.

Good news - a full and final negotiated settlement has been agreed, so this should be the end of the matter - a major uncertainty resolved.

Bad news - the cost is a lot more than expected, at £49.5m that BWNG needs to pay to Allianz (almost double the £25.5m provision in BWNG’s balance sheet as at 27 Aug 2022). Although this is less than the £70m (including interest & costs) that Allianz was claiming.

Can BWNG afford to pay it?

The answer sounds like a firm yes - this sounds positive -

The Company has sufficient liquidity to meet the cash flow requirements of the Settlement, including unsecured net cash of £82.9m as at 31 December 2022 as well as access to a RCF of £100m and overdraft of £12.5m, which are both fully undrawn as at 9 January 2023. Payment is expected to be transacted before the end of January 2023. After satisfying the Settlement the Company will retain a strong unsecured net cash position with material additional liquidity facilities remaining undrawn.

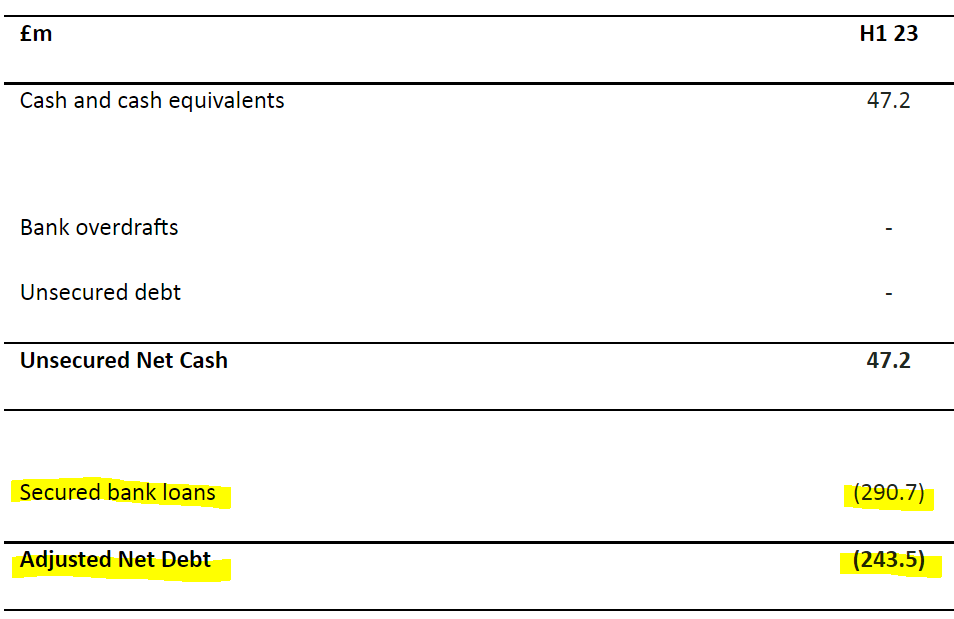

Hang on a minute though! I thought BWNG had substantial borrowings, to fund its extended payment offer to customers? Checking the last accounts (interims - 26 weeks to 27 Aug 2022), the full picture on net debt is this -

.

Today’s announcement doesn’t mention the large secured bank loans at all, which is selective reporting I would say! Although to be fair, today’s update is just talking about liquidity, not overall net debt.

The customer receivables book at BWNG was £492.0m, so it’s important to recognise that the net debt is just under half of the money receivable from customers (in instalments).

I’m not comfortable with this business model though, as the expected customer receivables losses are gigantic - many of them default - eg, just in H1 this year, the net impairment charge was £59.3m. As we saw with Studio Retail (which went bust) the actual numbers can be nothing like the published numbers, since a huge receivables book from customers who routinely default in large numbers, is very sensitive to whatever assumptions are made in the bad debt provisions - especially during an unprecedented disposable income squeeze, I would guess.

Balance sheet overall, when last reported at 27 August 2022 had NAV of £440.8m. I would delete the £108.3m intangible assets (which is all described as “software”) so has zero resale value I would suggest, so should be written off. Clunky legacy software could even be seen as a liability for this type of company, due to the cost of maintaining it.

This brings NTAV to £332.5m - which is massively above the market cap of £129m. So the stock market is effectively saying it (a) doesn’t think the net assets are completely real, and need a hefty write-off, or (b) the shares are woefully undervalued, or ( c) somewhere in the middle of those two extremes.

This balance sheet is very much stronger than rival Studio Retail (which went bust), so I suspect BWNG is probably in little danger of going bust, unless there’s a huge black hole in the accounts (as there turned out to be at Studio Retail).

Ownership - BWNG is controlled by the family of Lord Alliance of Manchester, who seem to own over half the shares. Hence I would say there could be a good chance of them taking it private - after all, why bother with a listing, when the shares are so woefully valued, at a >60% discount to NTAV?

The question is whether the Alliance family would be generous in a takeover bid, to take it private? I can’t see why they would be generous, but that’s guesswork.

My opinion - BWNG isn’t really making any profits or cashflows at the moment. It’s not a good business in my view - selling things online, in order to make profits providing expensive instalment credit to customers that often don’t repay the debt. Forecasts are for minimal profit this year, and a loss next year.

Next (LON:NXT) recently said that, due to full employment, it doesn’t see any reason to expect increased defaults on its customer receivables book. But Next sells things to more affluent people, and it’s well managed. BWNG sells to people who are financially struggling (why else would they want to use expensive credit instalments?), who we know are bearing the brunt of the cost of living crisis, since food & energy makes up a much higher % of the spending for poorer households. Therefore, I would expect defaults at BWNG to significantly increase. That could easily tip it into losses worse than forecast.

I can see why investors might be attracted to the huge discount to NTAV, but that in itself is telling us something about the quality of the net assets.

Getting the Allianz (not Alliance!) issue out of the way is a relief, but it’s not a good outcome, costing almost £50m in cash. I don’t think this threatens solvency, as liquidity is fine. Although investors should carefully check the bank covenants for the secured loans, and anticipate what might happen if BWNG started reporting big losses from receivables write-offs later this year.

It’s not for me, but good luck to holders.

The chart's looking quite nice now, as do lots of shares, so it could be of interest to traders, as well as investors who like deep discounts to NTAV maybe?

Anpario (LON:ANP)

420p (down 12% at 12:01)

Market cap £100m

Anpario, the independent manufacturer of natural sustainable animal feed additives for health, nutrition and biosecurity, provides the following trading update for the year ended 31 December 2022.

Q4 weaker than expected.

Not helped by delays in shipments which missed year-end cut-off.

Inflation - higher raw materials & logistics costs reduced margins (but H2 improved on H1)

Reduced volumes of product sold - blames cost pressures at clients.

Costs re aborted acquisition (announced in Sept) - will be adjusted out, it was £0.2m.

Revised guidance for FY 12/2022 - revenues at least £33m, adj EBITDA at least £5m.

FY 12/2022 revenues of ££33m means that H2 is identical to H1 at £16.5m.

Adj EBITDA was £3.0m in H1, so H2 is £2.0m, a significant deterioration.

H1 gross margin was down heavily at 42% (previously 50%). So we are now told there’s some recovery in H2, but not how much.

Put that together, and it must mean admin costs rose considerably in H2 vs H1. Otherwise static revenue but higher gross margin would have led to increased H2 profits, when it's actually lower by £1m.

Depreciation is only about £0.5m pa and there shouldn’t be any finance charges, so I reckon £5m EBITDA turns into real world PBT of about £4.5m. Take off normalised future corporation tax of 25%, and we get PAT of £3.4m. Divide it by 24.0m shares, and I’m arriving at 14.2p per share. That’s well below the 20.3p that the StockReport shows for broker consensus. Even if I use 19% corp tax, it’s 15.2p EPS, well below forecast.

So this is a significant profit miss of about 25%.

Valuation - using my reworked estimates above, I’m getting a PER of almost 30 - that looks way too high.

Outlook - sounds mixed -

We expect the global economy to continue to be challenging, however, we are encouraged by the improvement in our gross margins in recent months as a result of our actions to increase sales prices and are experiencing an easing of raw material price inflation, both of which are helping the Group to rebuild its margins. We continue to invest in our global sales teams and product development which will help deliver profitable growth of the Group.

Cash is healthy at £13.6m, and could improve further from planned de-stocking. Balance sheet overall I described as superb when last reviewed here in Sept 2022 when interim results were published.

Diary date - 22 March 2023.

My opinion - I’ve never understood why this share attracts such a high valuation, and today's update strongly reinforces that view.

Profits for 2022 now look to be giving up all the (modest) growth of the last 2 years, and back to c.2019 level.

Shareholders have to hope that the company can get growth, and margins moving upwards. Without that, the current valuation doesn’t look sustainable. I think this share looks significantly over-valued right now.

Graham’s Section:

Frontier Developments (LON:FDEV)

Share price: 613.7p (-38%)

Market cap: £241m

This games designer and publisher has issued a horrible profit warning today.

Note that H1 ended in November, and its full financial year ends in May.

Summary

Frontier generated revenue of £57m in H1, a poor performance compared to prior full-year revenue forecasts of c. £135m.

F1 Manager

This is currently Frontier’s flagship title, and 600,000 units have been sold. But it hasn’t met its sales targets:

Player engagement at release in August 2022 and during the initial period after release was strong, and broadly in-line with original expectations. Unfortunately, sales performance during key holiday season price promotions fell materially below original expectations, potentially due in part to increased player price sensitivity related to worsening economic conditions.

As this is the flagship title for the company, it’s a major disappointment to see it missing expectations.

Also, I’m not sure we can lay the blame on economic conditions, as the company suggests.

The video game industry has its own business cycle that is in many ways distinct from the economy as a whole. When quality hardware and quality software are released, people tend to buy it, regardless of the latest trends in GDP.

Or as the Washington Post puts it, video games are “sort-of” recession-proof, because the value of a game, in terms of hours of entertainment, is much better value than many other forms of entertainment (e.g. eating out, cinema).

So I wouldn’t allow the economic conditions to excuse much of the performance here.

F1 Manager received good reviews from critics and from audiences alike, but clearly did not generate enough of a buzz to see it fill as many Christmas stockings as Frontier wanted it to.

One point worth mentioning is that it’s a multi-year franchise and the game will be developed and improved upon in future years. Hopefully Frontier will learn from any shortcomings the original title may have.

Existing portfolio

The existing portfolio of other titles performed in line with expectations in H1 (up to November), but then fell below expectations in December.

Economic conditions are mentioned again, with “some evidence of increased player price sensitivity”.

3rd-party publishing (“Foundry”)

In recent years, Frontier has been publishing titles for other studios, but it seems unsure if it wishes to continue doing so:

Given our mixed experience of third-party publishing in terms of financial success to date, we are assessing our strategy for Foundry in light of such experiences and competitive trends in the market. In particular, we are reviewing the return on investment achieved by Foundry.

Perhaps it wouldn’t matter too much if Frontier stopped publishing 3rd-party titles, as most of these games do look very niche and small-scale. There are no new 3rd-party titles planned for release in FY 2024.

Note that Frontier has recently bought the studio behind the successful Warhammer game it publishes, so I guess that is not a 3rd-party title any more!

Outlook

Excerpts from the outlook statement:

…the Board no longer expects to achieve the FY23 market consensus forecasts for revenue and IFRS operating profit, being £135 million and £19 million respectively.

The Board believes it is still possible to surpass last year's record revenue performance of £114 million, particularly if one of the upcoming Foundry titles is a conspicuous success. However, given the number of variables and the more challenging economic outlook, the Board's revised expectation is to deliver revenue of not less than £100 million in FY23.

What a disaster! The new revenue estimate is 25% lower than previous guidance.

Furthermore, the company explains that with only £100m of revenue, operating profit would fall to c. £2m.

My view

I’ve gone back over my notes from September, the last time I covered this stock in the SCVR.

The share price at the time was over £12.

Having already fallen from a peak of £33, and with the company seeming to trade well, I viewed the company as a “weak buy”, saying “the valuation still requires the company to achieve a lot in the next two years. In particular, it requires the Formula 1 game to be a big success, and it requires a long stream of paid-for expansion packs from existing titles.”

Unfortunately, the F1 game has not been the hoped-for success yet, and the other titles aren’t picking up the slack.

So where do we go from here, with the shares down by over 80% from their peak?

Firstly, I don’t think we need to have any balance sheet concerns as the company’s cash pile at the end of H1 stands at £42.6m.

As for profitability, the company is looking for revenue growth of 5% in FY 2024. Operating leverage is significant here and I would expect that a large percentage of future revenue growth should find its way to the bottom line, particularly in F1 Manager since the base game has already been developed.

The company’s broker, Liberum, expects EBIT to improve from £2m in FY 2023 to £5m in FY 2024.

Compared to those earnings estimates, the stock might still seem very expensive at an enterprise value of around £200m. But I have to emphasise the operating leverage: each incremental £1 of revenue produces around an additional 60p of operating profit, based on the scenarios laid out by the company today.

Overall, I’m going to leave my stance on this stock unchanged. I’m broadly neutral, leaning towards a positive view. The positives:

Net cash

F1 Manager is a multi-year franchise, and can be improved over time.

The games portfolio covers a variety of genres, so there is some level of diversification.

The negatives:

The diversification achieved so far is not yet enough to reduce reliance on a small number of key titles.

The huge sales miss suggests that F1 Manager has a lot of work to do to capture the imagination of its potential fan base.

Blaming the economy for missing sales targets is a red flag in the video games industry.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.