Good morning from Paul & Graham, in these volatile times. I'm (Paul) just typing up some comments on the banking problems (is it a crisis yet? Have CNBC created a new logo for it yet?), so that should be up shortly.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

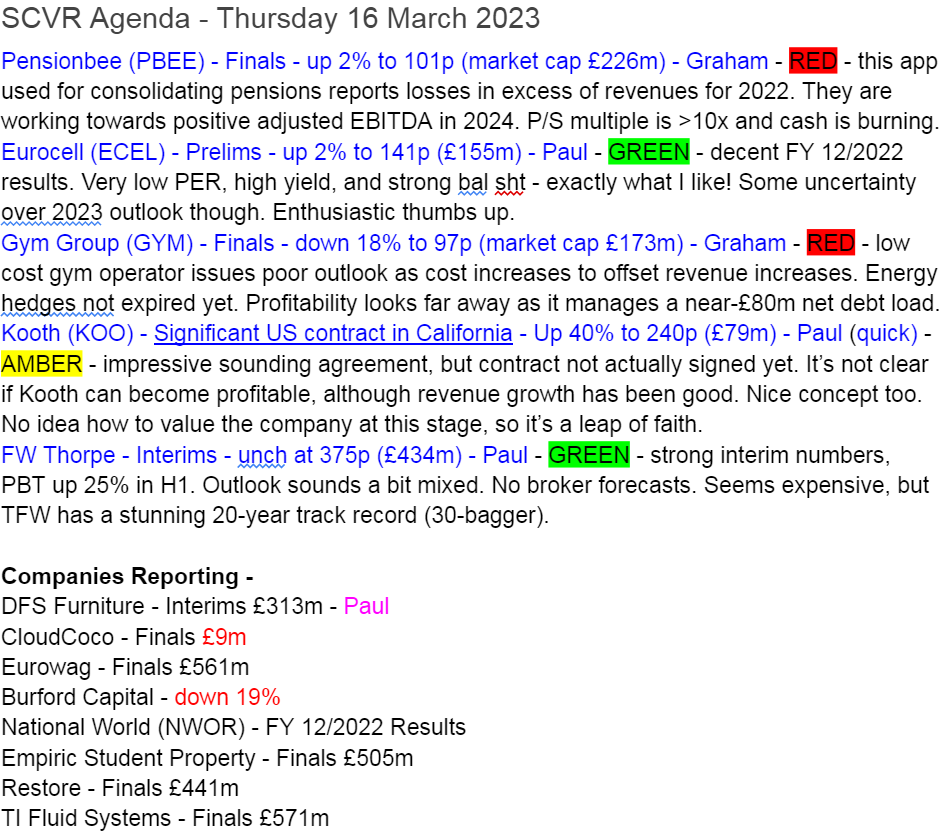

There's a lot on our to do list today, so I can't promise we'll get through all of these, especially if they're just in line with expectations (hence not price sensitive) -

Paul’s Section:

Comments on banking problems

I’m only loosely following what’s going on with the banks, and am not a banking expert, so this section is more a conversation starter than a pearl of wisdom!

As we’re all painfully aware, there has been a nasty sell-off in equities in the last few days, triggered by the strain in the banking sector (SVB going bust, and now Credit Suisse looking distinctly wobbly).

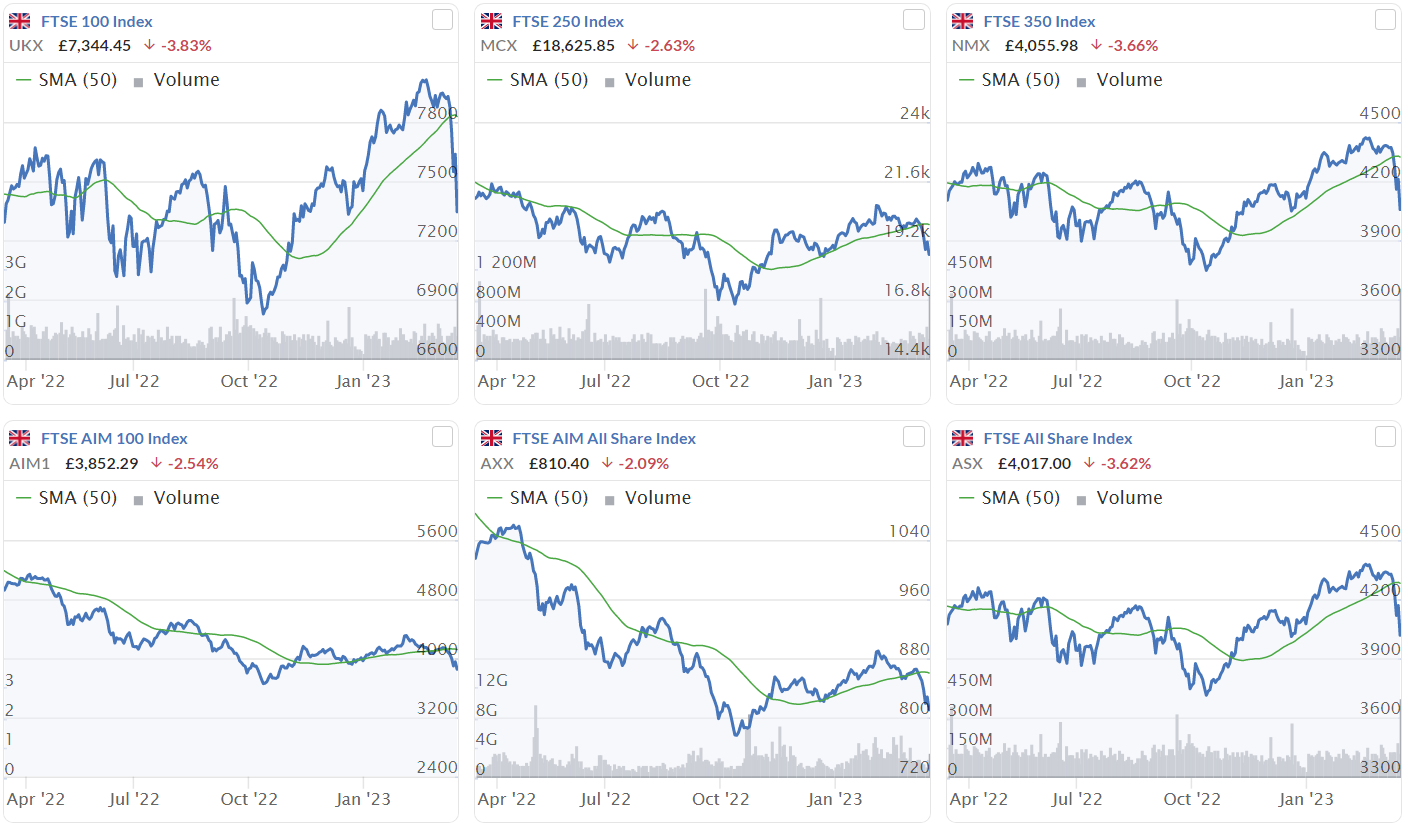

To put it in perspective though, see the UK indices below - 1 year view, with the % change being yesterday's change only. These show the same pattern - that we’ve given back the gains from a strong rally in early 2023, and are now roughly back to where we were at end 2022. Hardly a disaster (so far). This type of move is perfectly normal volatility, although it’s happened quite quickly, and could get worse of course, we don’t know at this stage. Futures (at 07:20) are pointing to a modest rebound today.

International indices look generally similar to the UK ones below.

Banks going wobbly happens from time to time. The problem is that if confidence falls in a particular bank, then the logical thing for depositors to do, is to remove their deposits and put the money in a stronger bank, asap. That creates a vicious circle, that can quickly escalate into a run on the bank.

This is made worse by the instantaneous nature of electronic banking. There was a story on CNBC of a coach load of venture capitalists going to a skiing resort recently (wouldn't they have been in limos, not a coach?!), but they were all busy on their phones, moving large amounts of client money out of SVB. The point being that runs on banks are now more likely to happen faster than in the old days when people formed an orderly queue outside a bank branch.

On the upside, everyone (Govts, regulators, central banks) know exactly what to do in this situation, as 2008 taught these lessons -

Guarantee deposits in full, to stop the run on the problem bank.

This time I think bondholders & shareholders should be left to their own devices, they knew the risks.

Move very fast to rescue the bank - either with a takeover by a stronger bank, or nationalisation.

Forcibly recapitalise banks that are weak, but refuse to strengthen their own balance sheets (as Gordon Brown did with the UK banks in 2008), to prevent further bank runs.

Senior Govt/Central Bank figures need to say strong things to the media (with gravitas) that restore confidence (remember Draghi’s “whatever it takes” comment, that might have saved the Euro from collapse).

It all raises the question, again, of moral hazard, and that the owners & senior management of banks enjoy the profits from risk-taking in the good times, whilst the taxpayer is forced to support them in the bad times, and when they make mistakes. But that’s a conversation for another day once this situation has passed.

I think it also raises the question about central banks raising interest rates, which has happened (just in my opinion, you may disagree) too far, and too fast, causing this crisis by crashing the value of bonds, equities, and property. No wonder banks and other financial institutions (I see Prudential was down 10% yesterday) are feeling the strain, as they’ve got a hole in their balance sheets as previously overvalued (by zero interest rates) assets drop sharply in value.

The whole system relies on confidence. Once that ebbs away, it all goes haywire.

SVB is sorted out, and Credit Suisse is the next one causing problems. The Swiss National Bank apparently extended large liquidity (reportedly $54bn) to it yesterday, but will that be enough? We’ll have to wait and see. Credit Suisse has been beset with problems for several years, so confidence was already ebbing away before this latest crisis. 5 year chart -

What should we do, as small cap investors? That’s up to you - choose whether to play it safe by selling (but probably then missing out on the rebound). Or whether to just ignore this, or even see it as buying opportunity?

At the moment, I’m leaning towards the latter, and I’m not selling anything, and don't intend to.

My reasoning being that everyone knows what to do, to resolve weakness in the banks. So one way or another, it’s going to get sorted. And market timing is not my thing.

Good luck with your portfolios, whatever you decide to do. If you’re good at market timing, then you probably sold a couple of weeks ago, raising the question of when to buy back in? Again, that’s entirely your call, your money!

Overall, my hunch is that we’ll probably see more problems emerge at weaker banks, so this crisis could rumble on for some time to come. But it doesn’t affect my overall investing strategy at all, unless the whole system shakes itself to pieces again, like in 2008 (probably unlikely I’d say).

With no gearing now, I can serenely ignore market share prices, and just wait for the problems to pass. That is a great improvement on the past, where I would probably be a forced seller by now in my geared accounts (discontinued activities).

What’s your view? Am I being dangerously complacent? Should we be hiding under the bed with our savings in cash or gold? Let us know what you think, it’s always good to hear the community’s range of opinions.

Paul’s Section:

Eurocell (LON:ECEL)

138.5p (down 2% at 08:11)

Market cap £152m

Preliminary Results - FY 12/2022

Eurocell plc is a market leading, vertically integrated UK manufacturer, distributor and recycler of innovative window, door and roofline PVC building products

Solid financial performance and continuing to gain market share

I last looked at Eurocell here on 26 Jan 2023, when it issued an in line trading update for FY 12/2022, together with a cautious-sounding outlook for 2023.

Today we get the full numbers for FY 12/2022.

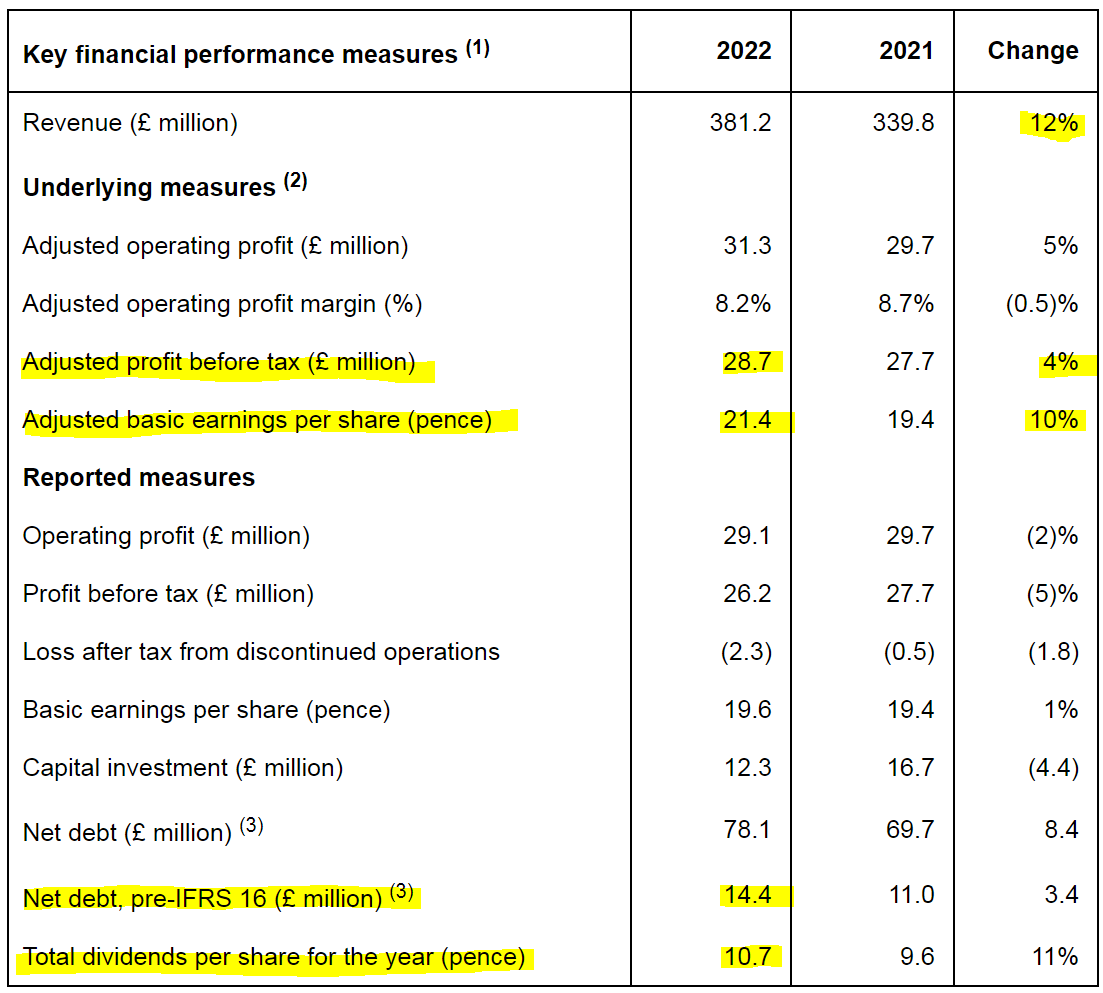

There’s a comprehensive key financials table, I’ve highlighted the most important numbers as I see it -

My comments on the table above -

Decent revenue growth of 12%, mainly through price rises. Note that the reported £381.2m is slightly lower than the £384m previously indicated in the last trading update.

Adj PBT of £28.7m is 7.5% of revenue - that’s a good profit margin, indicating a decent business with some pricing power, and products that customers must like.

Adj PBT is up 4%, but adj EPS is up 10% - the difference is caused by a lower tax charge in 2022 - see note 4 - due to a high £3.1m deferred tax charge in 2021, falling to only £0.2m deferred tax in 2022.

Adjustments to profit - are they reasonable? There were no adjustments in 2021, and in 2022 it was only £2.5m, relating to redundancies, so I think it’s OK to allow these adjs.

Valuation on 21.4p adj EPS is a PER of just 6.5x - but we can expect EPS to fall in 2023, so mustn't get too carried away with this low PER.

Net bank debt of only £14.4m is insignificant, given that annual PBT is about double that figure. Hence we don’t have to worry about gearing. It also has a £75m unsecured (very unusual) bank facility - ample.

Dividends - a superb yield of 7.7%, from 10.7p total divis, divided by share price of 138.5p - very attractive, but with a softer outlook there’s a possibility of 2023 divis being cut maybe?

Outlook - I’ve read most of the commentary alongside today’s results, and it all sounds similar to the previous updates - cautious on the outlook for 2023, but well-prepared for a downturn, having made £5m annualised cost savings already, and raised prices again in Jan 2023. It sounds like a well-managed business. Note that broker forecasts have been managed down recently, which I like, because it means a profit warning should be less likely -

For the current year, the latest construction industry forecasts recognise the currently challenging market conditions and ongoing macroeconomic uncertainty. However, we have acted swiftly on cost to prepare the business for 2023 and we expect our strategy to enable us to optimise performance in our markets.

If we value ECEL shares on the latest (lower) 2023 forecast EPS of 18.0p, we get a 2023 PER of 7.7x - still really cheap! Although this sector tends to only attract modest valuations generally, especially when macro conditions are tough.

So the market seems to be pricing in a miss against this lower forecast, possibly? If the market is being rational, which it may not be!

Valuation - historically, EPS was very steady, at around 20p, so I think we can probably safely use that figure as a long-term way to value the share. Put that on a PER of say 10-12 (not demanding), and I get a personal valuation of this share of 200-240p. Hence its current price of 138.5p looks attractive to me.

Plus, shareholders get paid nice divis to wait for a re-rating. Also, little risk due to the strong balance sheet. It ticks a lot (well, all!) of my value investor boxes! Apart from management shareholdings, which are too low, and remuneration in 2021 looks too high.

Balance Sheet - looks excellent to me. NTAV is almost £100m, which is about two-thirds of the market cap - so this share is doubly supported, by earnings, and also assets.

The last annual report shows that it owned £7.3m freehold property, which is a nice bonus for investors.

My opinion - I really like this share, and give it an enthusiastic thumbs up. It’s exactly the type of solid value share that I should own, if I could stop getting distracted by more speculative stuff!

We have a low PER (both on 2022 actuals, and recently lowered 2023 forecasts), a thumping dividend yield, combined with a strong, ungeared balance sheet. What more could you ask for?

The downside risk is obviously a cautious outlook, and possibility of 2023 being a worse year than expected. Although I think it’s the type of company where I would see any temporary setbacks in trading as being buying opportunities.

It’s also got the financial firepower to make acquisitions, although that’s not a priority for 2023.

A consistently strong StockRank is the cherry on top!

Looking at the long-term chart, this share really does look oversold to me - and there's only been a little dilution from equity raised during the pandemic (now 112m shares in issue, vs 100m in 2016)

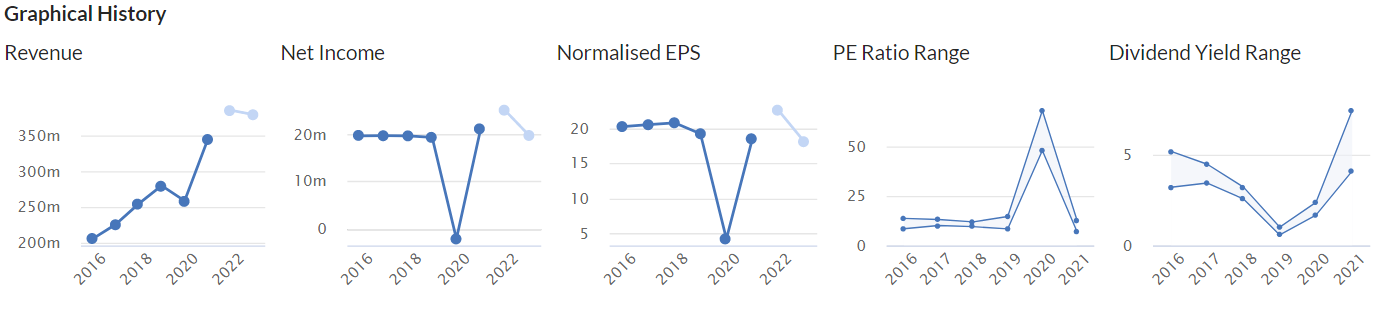

FW Thorpe (LON:TFW)

375p (unch)

Market cap £428m

Owner/managed lighting business.

Interim results to 31 Dec 2022

Strong numbers, with PBT up 25% to £10.6m for H1, on £81.9m H1 revenues, demonstrating a good profit margin at 13% of revenues.

No adjustments to figures.

Supply chain pressures are easing.

Balance sheet is still excellent and ungeared, although note that acquisitions mean goodwill is rising, and quite significant now at £71.6m. Acquisitions are also depleting the cash pile, now down to £21m

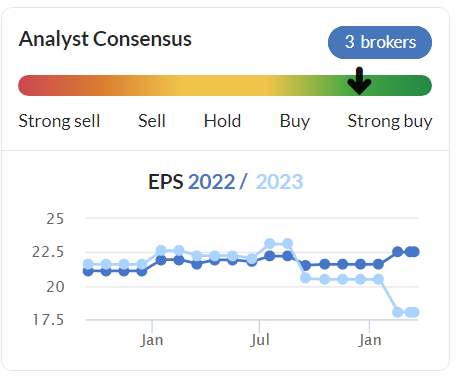

Forecasts - there don’t seem to be any!

Valuation - tricky one, with no forecasts (not even any broker consensus) to work on. It has an H2 weighting to profits. Last year was 17.0p EPS (a big jump on previous year). So if we assume this year might be between say 15-20p EPS, then that gives me a PER of 19-25x which strikes me as a tad too expensive to get me interested.

Although should we really be quibbling over valuation, when the long-term track record is stunning - a major multibagger, over 20 years -

Dividends - are modest, with it yielding roughly 1.7%.

Outlook - a bit mixed, but sounds alright overall. I wonder if the boost mentioned below from the imminent ban might be providing a one-off profit boost? -

High energy costs and the imminent ban on the sale of fluorescent lamps in the UK and EU are both stimulating activity in the Group's key market sectors. The outlook for the second half remains quite positive, although the revenue growth percentage is unlikely to be maintained at such a high level due to the good performance in the second half of last year.

My opinion - I like the business, it has that nice look & feel of conservative accounting, no adjustments, no debt, that you often find at family-controlled listed companies like this.

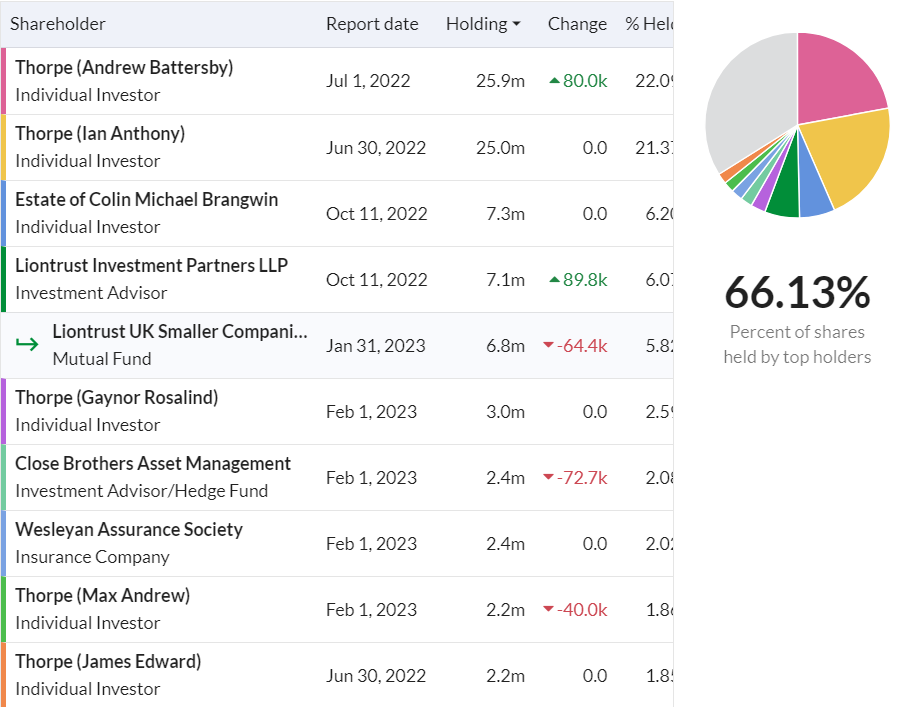

The 2 top shareholders are both Thorpes, and together own 43%, with 3 more smaller Thorpes further down the list! A lot of shrewd investors (e.g. Lord Lee, David Stredder, and others) favour family-run companies with long-term track records, and I agree. Although that comes with the risk that this type of company can be run like a private company with a listing, so you’re along for the ride, and have to just trust that the driver will look after you. Normally they do, in my experience, but it can’t be guaranteed.

Overall I can’t decide whether to go green, or amber. So for a super-long-term buy & hold, I see this as positive (green), due to TFW’s fantastic long-term track record. Even though the shares look too expensive in the short term (even after considerable falls of late).

It has a nice healthy StockRank too, although as I would expect, the Value score element is low, at 25.

Do we have any shareholders in TFW here? If so, do post your views below. It seems tightly held, with few trades most days.

Graham’s Section:

Pensionbee (LON:PBEE)

Share price: 101p (+2%)

Market cap: £226m

This is a 2021 IPO I’ve commented on twice before - see here and here.

It’s an online pension provider, letting people combine their various defined contribution pensions into one pot and manage them on the PensionBee app. The annual charge by PensionBee is 0.5% to 0.95% of assets.

Let’s now take a look at the company’s full-year results for 2022:

Revenue +38% to £18m

Annual run-rate revenue at the end of the year £20m

Pre-tax loss £22m

Assets under administration +17% to £3bn

Invested customers +56% to 183,000

CEO comment:

Encouraged by strong year to date trading driven by customer growth and healthy net flows from new and existing customers, we are on track to achieve our primary objective of ongoing Adjusted EBITDA profitability by the end of 2023 and to become profitable for full year 2024. We will achieve this by continuing to reduce the Cost per Invested Customer, delivering innovative new features and making efficiency gains through our scalable technology platform.

I’ve just checked the note issued in January by Equity Development and it looks like we are still too early to have 2024 estimates. Given that the company’s 2022 losses are bigger than its revenues, perhaps we should rein in our estimates for 2023 and 2024?

If the company was “profitable” (according to adj. EBITDA) in 2024, I do agree that this would be an achievement. Adjusted EBITDA was minus £20m in 2022. According to the note issued in January, it is expected to be minus £9m in 2023.

Over the long-term (5-10 years), the company is pursuing a 2% market share of the defined contribution pension market, which implies 1 million customers and annual revenues of c. £150m.

Cost per invested customer (which measures the cost of customer acquisition) did not improve in 2022 and is currently £248. This is unfortunately still too high as the company only makes a little over £100 in revenue from each customer annually. Pensionbee’s stated acceptable threshold for this metric is £200 - £250, so they are only just within their own threshold.

More positively, I note the amazing reviews that Pensionbee gets on Trustpilot. We have to hope that this is not because the company is overspending on things like customer service. I find it surprising that every single customer gets their own dedicated account manager.

Balance sheet - in 2022, the cash balance more than halved from £43.5m to £21.3m.

My view

I think it’s right to be sceptical of the investment case here.

Some reasons for caution:

The company has already achieved brand awareness of 50% and nearly one million registered customers, of whom only about one-fifth have funded their account. Surely it won’t be very long before most potential customers have already heard of Pensionbee and made up their mind about switching to them or not?

If the company makes an adjusted EBITDA loss of £8m in 2023, the cash burn is unlikely to be any smaller than that. The company’s cash pile could easily fall to c. £10m, increasing the pressure on profitability in 2024 if they don’t wish to raise any new equity.

The current price to sales multiple is in excess of 10x. The market cap is higher even than the company’s long-term revenue target which it is hoping to hit over the next 5-10 years!

Bull points? Pensionbee did earn a barely positive “Adjusted EBITDA before Marketing” in Q4, i.e. their adjusted EBITDA is now around breakeven if you exclude all the costs that go with growing the business. There is the possibility that they could, at some point, pivot their business model from scale-up to profitability (a nice phrase used in FT Adviser in an article discussing the unprofitable Nutmeg).

I’m going to give this share the thumbs down for now - too overpriced and risky.

GYM (LON:GYM)

Share price: 97p (-18%)

Market cap: £173m

I‘ve gone back over my notes from the last time I covered this low-cost gym operator, to help remember what was on my mind in January. The company had at last decided to stop opening quite so many new sites, and was losing its long-standing CEO. With net debt rising to £76m (excluding rents), it looked an increasingly risky proposition.

Today we have full-year results for 2022.

Revenue +63% to £173m

Like-for-like revenues (vs. pre-Covid 2019) of 90%, with like-for-like customer numbers of 81% and yield per customer of 110%.

These are quite poor numbers, I think - remember that given the levels of inflation over the past few years, an increasing yield per customer should be a given. But with average customer numbers per site at only 81% of pre-Covid levels, that suggests a very significant hit taken at particular sites from the work-from-home trend, or possibly a general oversupply of gyms (or both?).

The outgoing CEO says:

It is now apparent that some members have not come back to in-gym workouts post Covid-19; therefore our work to recover pre Covid-19 levels of profitability is continuing.

Some of the members have been displaced because they have not fully returned to office working - just 16 sites out of our 154 sites that were open pre Covid-19 are significantly workforce-dependent and the rest are located in residential areas or have a strong student membership. We believe that there is further membership recovery to come in the medium term but this has been slowed in the short term by the cost-of-living pressures which are having an impact on underlying demand.

Market share in the low-cost gym space for this company is now at 29.3%, versus 16.7% in 2016. Unfortunately, there is little indication of pricing power feeding through to profitability, with this increased scale. There has been an improvement compared to the Covid-impacted 2021, but that isn’t saying much:

Adjusted loss £7m (2021: £28.5m)

Statutory loss £19m (2021: £35m)

Outlook

“Uneven start to 2023 vs Board expectations”

Like-for-like revenue vs pre-Covid at 97% in first two months.

Energy costs to be £10m higher this year (I think GYM’s hedges start to expire next year).

Profitability doesn’t sound very likely very soon:

Expect current difficult macroeconomic environment and its impact on consumer demand to continue throughout the year; therefore now anticipate full year revenue increases from yield improvements and new site openings to be broadly offset by cost increases

At least they have broadly admitted defeat when it comes to the expansion plans. They are now looking to open only twelve new sites in 2023. In January, they said they were going for 20 (it was 25-30 before that).

Succession plan - the Chairman says “we are making good progress in the search for our new CEO”.

Net debt finished the year at £76m, as previously disclosed. There was £15m of headroom on the RCF (seems quite low) and the RCF is due to expire in October 2024, so it will need to be extended or refinanced.

My view

The market cap has taken a hit since I last looked at this but I see little reason to change my view: I’ll stay negative. The company isn’t profitable and the prospects for profitability in the foreseeable future appear weak. It is highly leveraged. What more is there to say?

I remarked previously that the cost-of-living crisis was a factor here. It’s an interesting point because you might think that a low-cost operator would do well as people traded down from more expensive gyms. However, it might also be the case that when the economy was stronger, the low-cost operators attracted marginal gym goers who might not previously have joined any gym. Those marginal members appear to have left for good now - or until the economy picks up again.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.