Good morning from Paul!

I'm hoping for a quiet news day today, so I can catch up on some of the backlog things on my list.

Today's report is now finished. Have a lovely weekend!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £1bn. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk.

Agenda

This is my plan for today, below. I'll start with the 2 profit warnings, then I really want to finish off MSI, which I looked at in detail last night, as it looks an interesting company (a podcast mystery share in late 2022), and has a bulging order book. Something interesting seems to be going on there, and we're already GREEN on it anyway, so a recap would be useful for results that were issued yesterday. [EDIT: sorry, I'll finish MSI over the weekend, there wasn't enough time today]

Hotel Chocolat (LON:HOTC)

Down 13% to 121p (£166m) - Trading Statement (another profit warning) - Paul - RED

Hotel Chocolat Group plc, a direct-to-consumer premium chocolate brand, today updates on recent trading.

Background - the current financial year is FY 6/2023. Checking my previous notes here -

6 Dec 2022 - I mystery shopped Islington store, and found product disappointing & expensive. AMBER.

20 Jan 2023 - 209p - H1 (Dec 2022) in line. Guidance £8m PBT FY 6/2023. I’m sceptical about valuation. Brokers forecast large increase in profits in future years - realistic? AMBER.

27 April 2023 - 158p - Profit warning, now says only breakeven for FY 6/2023. Remains over-priced at 158p. I move to RED.

Today’s update -

Cost cutting has been slower than expected

Sales in line with market expectations (footnote: £201.8m)

Profits lower - “underlying marginal loss” for FY 6/2023, below £0.3m current guidance. Doesn’t sound too bad, but what’s a “marginal loss”? £1m, £2m, £3m?

Cash generation healthy & has £19m cash (down from £28m at Dec 2022) with no interest-bearing debt - the balance sheet is solid at HOTC, so providing it doesn’t start generating massive losses, then I think solvency (and dilution) are very low risk at the moment.

Outlook - this is the bad bit, as they can’t pass this off as a timing issue -

For FY24, the Group expects sales and underlying PBT to be lower than current market expectations due to ongoing weakness in consumer sentiment and continuing inflationary pressures.

Guidance for FY 6/2025 is reiterated, but in my view wasn’t credible to begin with, and now looks like pie-in-the-sky -

For FY25, the Board clarifies its guidance for the target of 20% pre-IFRS EBITDA to be achieved towards the end of the year, with the full benefits being achieved through FY26.

Broker update - many thanks to Liberum’s analyst Wayne Brown for his detailed update this morning, this is really helpful, and I'm aware that a lot of work goes into these broker notes with detailed forecasts. He’s answered my question above, by pencilling in adj PBT loss of £(1.5)m for FY 6/2023, down from a previous forecast of positive £0.8m. That’s a mild disappointment, but not a disaster, as I see it.

The real damage is a massive cut in FY 6/2024 forecasts - the unrealistic £20.3m adj PBT now becomes only £6.0m. Given macro, personally I’d be surprised if they even achieve that reduced figure.

The FY 6/2025 forecasts were bonkers previously, at £33.1m profit, which has now been greatly reduced to £14.3m, but still seems optimistic.

Paul’s opinion - I remain highly sceptical. The only positive thing is that shareholders don’t have to worry about financial stability, as it has a nice strong balance sheet with cash, no bank debt, and £20m freehold property. Lease liabilities might become a problem though, if shops become loss-making.

The company has repeatedly over-promised and under-delivered. I think the share price has much further to fall, as the bull case unravels further.

Previously the market valued this as an international growth company, but that's now fallen flat. It seems much too early to be anticipating a recovery, we need to see some evidence of a turnaround first -

The StockRank isn't good, and I imagine it's likely to worsen, as lower forecasts and a lower share price feed into the momentum and value scores. As for quality - well I don't see this as a quality business at all!

Intercede (LON:IGP)

51p (£30m) - Results FY 3/2023 - Paul - AMBER

Intercede, a cybersecurity software company specialising in digital identities…

Background - we’ve followed this small, specialist IT company for many years here, and spotted a nice turnaround in 2018-19, doing well on the shares which I held personally for about 3 years, as they 3-5 bagged depending on when you bought. It's since given back a lot of those gains though, in the last 2 years.

(the excitement in 2014 was big contract wins, which were not repeated)

Old management had a high cash burning strategy, spending on new, speculative projects, but it nearly ran out of cash. So new CEO Klaas van der Leest was brought in 5 years ago to turn it around. He’s done a good job I think, firstly stemming the losses, then moving it into profit, and resolving a convertible loan note debt problem. The finances are now very healthy, with a nice cash pile. It’s also making small bolt-on acquisitions.

So this is a small, profitable, soundly financed, niche software company. The main attraction is its staggeringly impressive client list - very sticky recurring revenues, from US Govt departments, major aerospace companies, etc. Most of its business is in the US, and it seems to be a small part of big IT systems, and is dependent on several long-term, major US contracts, so client concentration is a risk.

FY 3/2023 Results - key points -

Revenue up 22% to £12.1m - small, but very high margin, and good growth (helped by the strong dollar)

Clean accounts, with no adjustments, and all development spend is expensed.

Profit before tax (PBT) only £0.6m (double last year though)

Corporation tax is negative, due to favourable R&D tax credits, so a £685k tax credit, more than doubling the £626k PBT to £1,311k PAT (profit after tax) - although on webinar, CFO said this will reduce to £350-400k in future years.

Diluted EPS is 2.2p (LY: 1.2p), giving a PER of 23x

Dividends - it doesn’t pay any.

Balance sheet - only about £4m NTAV, but that’s fine because working capital works favourably, with customers paying up-front for support, licences, etc. So the £8.3m cash pile has mostly (£7.5m) come from deferred revenue (customers paying up-front), but that rolls continuously, so not a concern.

Outlook -

This has been an encouraging and successful year for the Group. However, to maintain and sustain its current momentum, it needs to continue to invest in its colleagues, IT Infrastructure, product development and sales and marketing.

We embark in to FY24 with good visibility on the pipeline, known and fully resourced internal critical investments and with a clear road map on our acquisition strategy. As mentioned frequently, the focus is on 'growth' and execution of strategic plans to deliver it.

The way I read those outlook comments, is that revenue growth is probably going to be ploughed back into the business, so probably not much prospect of significant profit growth for now (unless it wins a monster new contract). That’s probably the right thing to do, but it does mean shareholder returns could be limited.

Also, staff costs make up most of the overheads, so current wage inflation has forced IGP to give 5-7% pay rises to its (mostly UK) staff, and performance bonuses.

Paul’s opinion - probably priced about right for now.

Bull points:

- Stunning client list of major organisations in the US

- Global specialist in its niche

- Takeover target for a larger IT group possibly?

- Sound finances with £8.3m cash pile (gone up since y/end mgt said in webinar)

- Upside potential if it wins big new contracts, drops through to profit

- Much wider target market now, with new product development, previously just high end

- Capable and trustworthy management that tell it like it is, good shareholder comms (see recent IMC webinar), and have implemented an effective turnaround at a previously problematic company.

Bear points:

- Sluggish revenue growth historically, although +22% this time is better

- Growth likely to be reinvested in higher costs, so limited profit growth?

- Valuation up with events on a PER basis.

- Long-serving staff - great experience, but set in their ways maybe? Are they hungry enough for growth?

Overall - I think there’s a good case for holding this share, so you’re in the right place if/when some major contract wins, or a takeover bid happens, but that's speculation, and may not happen of course! The main downside risk I see, is if one of the really big US Govt clients rips out & replaces their IT without Intercede in it - so client concentration is the main risk I see. Other risks might include catastrophic system failure or security breach.

I’ll keep an eye on it, and hopefully shareholders might be rewarded with an acceleration of growth, and some decent sized contract wins. Good, credible management, are worth backing I think, but I'll stick with AMBER for the time being.

Halfords (LON:HFD)

211p (£472m) - FY 3/2023 Results - Paul - AMBER

I last looked at this motoring/cycling group in Jan 2023 here, when it issued a Q3 profit warning, lowering profit guidance for FY 3/2023 by about 17% to £50-60m range. Shares dropped 20% to 173p, and I took an AMBER view then, based on the facts, figures, and forecasts on the day.

What’s the latest?

FY 3/2023 Results - I haven’t got time to go through this in detail, so will just draw out some main points -

Revenues £1.6bn (up 15% on LY), so a substantial business.

It’s more than just a retailer (61% revenues), with Autocentres (servicing, MoTs, etc) 39% of revenues (£614m)

Underlying PBT £51.5m, towards lower end of range guided in January, and well down on LY, which was boosted by customers’ pandemic lockdown spending.

Adjustments benefit this figure by £8.0m, and in note 4, I think these are rather questionable, especially £6.3m restructuring costs, which I think is fairly normal for this type of business, so personally I would add that back, lowering profit by about 12%.

Underlying basic EPS of 18.8p (LY much higher at 35.5p) - PER of 11.2x

Outlook - there’s a big section, so let me summarise the main points -

Current trading - “good”, positive LFL sales growth, despite poor early spring weather.

Expecting modest profit growth in FY 3/2024 - comfortable with £53.3m u/l PBT from brokers (barely any change from £51.5m FY 3/2023 actual) - so it could easily move over or under, given the large numbers & uncertainty.

Net cost headwinds expected at £30m - wages, FX, energy, “partially offset” by lower freight costs on imports.

Aiming to offset this cost headwind with lower cost purchasing of products, and efficiency gains, a third already delivered.

H1 expected to be below LY (which benefited from a forex gain), but H2 above LY.

Expects to end FY 3/2024 with “small net cash position” (excl. leases)

Further out, it says -

Looking beyond FY24, we expect strong profit growth in FY25 as we take a significant step towards our mid-term expectation of £90-110m underlying PBT, as outlined at our Capital Markets Day in April 2023.

I think it’s too early to forecast that far ahead, so I’d take this with a pinch of salt for now, until macro becomes clearer.

Balance sheet - NAV is £563m, but deducting £482m intangible assets gives us £81m NTAV - OK, but not a lot given the size of the business. Note that NTAV has fallen in the year, from £109m last time.

Given the not particularly strong balance sheet, I question Halford’s strategy of both paying fairly generous divis, and continuing to make acquisitions. The danger here is that it erodes its NTAV, building up goodwill, but weakening the overall financial position.

I think this also makes the divis not particularly safe. In the event of a big consumer downturn, HFD would have little choice than to cancel its divis. Just something to bear in mind.

Net debt was eliminated in the year, from £46.1m at 1/4/2022, to net cash of £1.8m at 31/3/2023. Although given the large size of the business, I wouldn’t get too excited about year end snapshots, as the daily figures are likely to yo-yo all over the place during the year, when large payment runs to suppliers, payroll, VAT, etc are paid. Whereas daily cash inflows will be fairly level and predictable, being retail cash coming in from the card processing merchant divisions of their bank. What we need, for all companies, is the average daily net cash/debt figure. I’ve done a search using CTRL+F for the word “average”, but it doesn’t throw up anything relevant. However, note 5 shows only £1.4m finance charge on bank borrowings, which suggests it's probably not using the RCF excessively, and intermittently, which is what it's there for!

Cashflow statement - looks amazing, but the £154.8m operating cashflow is a nonsense number, because it excludes rents! These are lower down, in financing activities, and are £8.8m + £80.5m, so that lowers genuine cashflow to a more realistic £65.5m, which is not particularly good for a company valued at £472m.

Also look closely at the “investing activities” section, with £32.6m spent on acquisitions - fine, it’s buying up and rebranding car servicing businesses. Note £25.4m “purchase of intangible assets” - I don’t like the look of that, it sounds like capitalised development spend on IT, which I think should be expensed, not capitalised. Although the P&L does include a £17.9m amortisation charge. Net these off, and it looks as if profit is boosted by £7.5m through this policy. Physical capex is £29m.

Two unusual items are £22.7m “Receipt relating to supplier financing”, and an offsetting £23.5m “Payments relating to supplier financing”. I don’t recall seeing that before, so am curious what it is, a good question to ask management to explain this, although it’s not material overall.

Dividends - total divis up 11% to 10p, yielding a nice 4.7%, but as noted above, I don’t see the dividend paying capacity as being particularly good.

Paul’s opinion - the really detailed outlook/guidance section suggests to me that this seems a well managed business, where management and finance people are really in control of everything, and unlikely to be caught out by unexpected things within the business. External factors are obviously unknown.

The year reported faced big challenges, so to come out still profitable, isn’t bad.

On closer inspection, profit, balance sheet, and cashflow are OK, but nothing special.

Outlook sounds strong, but is only forecasting a tiny increase in profit for FY 3/2024, and the numbers are so large, with a really small PBT margin of only about 3%, that it wouldn’t take much to move that number a lot. There could be upside, or downside, who knows, as there are so many moving parts right now.

This share looks priced about right to me. Given macro uncertainty, personally I wouldn’t be interested in buying any at this stage.

But if you think Halfords can out-perform, and deliver better than expected numbers in future, then it could appeal.

Not a growth share, long-term, but nice divis are the main reason to hold. Could it re-rate once the economy improves? Each 1% on the margin would be an extra £16m profit.

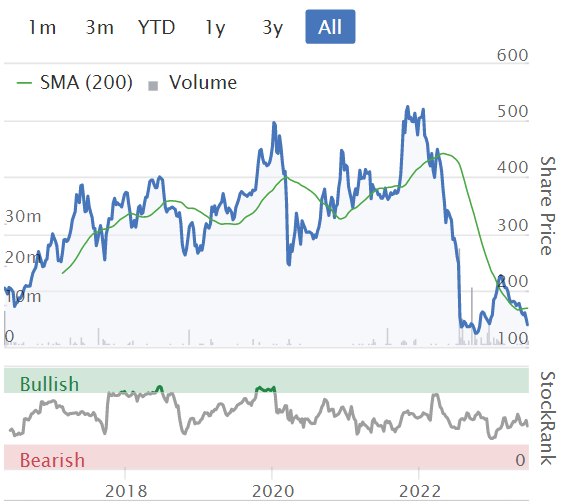

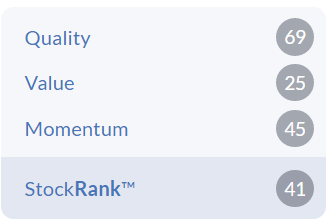

Audioboom (LON:BOOM)

Down 26% to 210p (£34m) - Trading Update - Paul - RED

This is an interesting company. It produces & distributes podcasts, mainly in the USA I believe. Shares have boomed & busted twice now, as you can see from the long-term chart below. I recall reporting very negatively on it for a few years, when the fundamentals were terrible.

However, more recently new management did manage a decent turnaround, with very impressive revenue growth, and the market got excited about it being a tech company in the latest pandemic tech boom, causing the shares to 10-bag up to a peak of c.2000p. It’s not really a tech company though, it’s more an advertising company, using podcasts to generate ad revenues.

Ad revenues are now under pressure, hence the share price falling all the way back down again.

Checking my notes from earlier this year -

23/1/2023 - concealed profit warning in an upbeat-sounding update. I thought it was maybe fairly priced at 405p based on the facts/figures/forecasts at the time, so AMBER.

24/3/2023 - 435p - OK figures reported, but management nicked all the profits in share options charges. This greed tipped me into a RED view, calling it uninvestable.

Latest news - the share price has halved to 210p since the above comments. This market is not taking any prisoners!

Key points today -

Advertising markets have remained challenging for longer than expected.

Revenue & adj EBITDA for FY 12/2023 “lower than previously anticipated”.

Claims good KPIs, and growth, but excludes a (presumably large) podcast that it lost!

New records set for downloads & ad impressions - So what? If profit is lower than expected?! Must mean ad rates are lower?

Liquidity sounds OK, and apparently no cash burn (a bugbear in the past, when it was much smaller) -

Group cash at 31 May 2023 of US$5.2 million (31 March 2023: US$5.1 million) with a further US$1.8 million available via an undrawn overdraft. The Company has collected in excess of US$30m to date in 2023

Paul’s opinion - we need to know what the revised forecasts are. Unfortunately, Finncap issues a brief update today, saying it is putting its forecasts under review (ie. withdrawing them). So we’re now completely in the dark.

Therefore I don’t have any choice than to reiterate my view as RED. The main problems are -

- We now don’t know how it’s trading.

- Also it’s not a very good business, even in the good times, only making a very low gross margin - podcasting is competitive, and the most popular podcast creators shop around for the best deal from the various platforms. Not an issue that has as yet cropped up for me!

- Finally, management greed with share options that seem completely out of kilter with profitability, finishes off the bull case for me. Although hote one Director has been a repeat, smallish buyer in the open market for a while.

The bull case might include -

- £34m mkt cap is cheap now relative to the previous spikes, so traders might get involved and take it higher once they see a favourable chart pattern in the future perhaps?

- Takeover potential?

- Shares could recover once ad markets rebound.

- Solvency doesn’t appear to be an issue, but that depends on the numbers, which we can’t see at the moment, due to lack of broker forecasts.

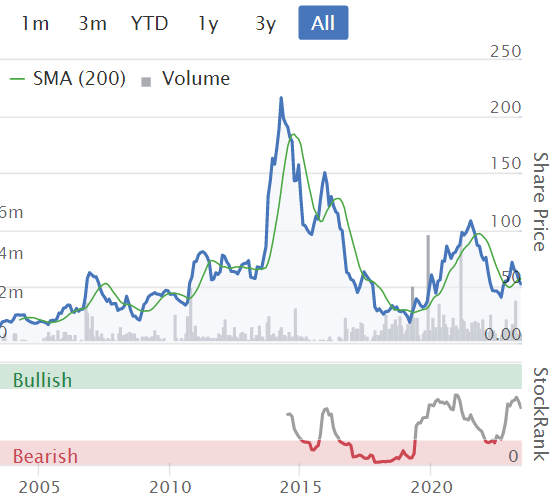

Gear4music (HOLDINGS) (LON:G4M)

98p (£20m) - Final Results - Paul - AMBER

Gear4music (Holdings) plc, ("Gear4music" or "the Group") (LSE: G4M), the largest UK based online retailer of musical instruments and music equipment, today announces its financial results for the year ended 31 March 2023.

Graham last covered G4M here on 6 April 2023. I remember it well, as I was enjoying the sun on holiday in Gozo, and I decided to buy a few at 79p, but have since sold them, to bank a modest profit, and recycle the money into something else - just in case anyone wanted to know if I still hold this. Also, we always disclose our personal positions, since that might introduce unconscious bias. So we're not just announcing our trades for the sake of it, which is pointless (and can be irritating to readers - unless you're Warren Buffett, nobody cares whether you've bought or sold!).

Although 6 April was a profit warning, what did impress me was a substantial reduction in net debt, from worrisome, to probably OK. For me, that offsets the downside of profitability which fell from the pandemic boom peak, to only expecting around breakeven for FY 3/2023.

Actual FY 3/2023 Results - key numbers -

Revenue £152m - exactly as guided.

EBITDA is meaningless, but it’s £7.4m, within the £7.3m to £7.7m range guided.

Net debt reduced from £24.2m in Mar 2022, to £14.5m at Mar 2023 - as guided, and this is the most important and positive point I think, in greatly reducing risk to investors of dilution or worse.

HSBC has renewed £30m facility for another 3 years. Great, but memo to management - please don’t use it! It’s risky in a downturn.

Outlook - this seems to be suggesting that H1 won’t be very good -

Market conditions have continued to be challenging since our last update in April, and we are taking the appropriate and necessary actions to ensure our business is correctly configured, resourced and positioned strategically for long term success. To ensure the Group can return to profitability during FY24 H2, we will focus on product margins, efficiency and overhead cost reduction ahead of revenue growth, whilst we continue to develop new growth initiatives for the longer term."

Balance sheet -

Looks adequate, but not strong, because bank debt is needed to part-fund the large inventories. NAV is £37.2m, but includes £22m intangible assets, which I always write off, giving NTAV of £15.2m.

Whilst net bank debt is £14.5m, this includes a gross bank loan of £19.0m (variable rate, linked to SONIA), which still feels too much to me, for a company trading at breakeven. Although the bank is obviously happy, as it’s extended it for 3 more years, and has seen it reduce substantially from £28m a year earlier - proving that G4M can indeed reduce inventories (still quite high at £34.4m, but down from £45.5m a year earlier) to generate cash. This might have hurt margins a little too, discounting to sell slow moving lines?

It’s got freehold property remember, so that is a strong positive of £7.7m book value (£550k downward revaluation, see note 8).

Cashflow statement -

Cash generation is high, due to big reduction in inventories, reversing last year’s increase, so this is excellent to see.

Very heavy capitalised development spend on IT, of £5.3m. Amortisation charge was £3.0m, so if we remove these items, it means the company is loss-making.

Cash generation was used to repay £9m of bank borrowings.

It doesn’t pay divis.

Overall then, not a cash generative business really, at this stage. Once it’s bigger, that would be the hope.

Paul’s opinion - it’s got through a really tough year, and looks a lot more secure now, with bank debt substantially reduced. I’d say this looks a fairly low quality business, with no pricing power at all really, as we’ve discovered with a lot of eCommerce companies, once the market euphoria from rapid growth has subsided.

What does the future hold? I think G4M looks set to slug it out with competitors, growing market share, and seeing also-rans fall by the wayside. People can just buy items from Amazon, etc, but musicians tell me that they prefer to buy from G4M because of fast delivery, and no-quibble customer service if anything goes wrong. Whereas buying from Thomann (the main European competitor) can result in 2-week, or uncertain delays, a benefit to G4M from Brexit!

Bottom line is price. Is £20m a fair valuation? I think it’s cheap, so I may well crop up as a small shareholder again at some point in future, on a buy the dips basis, if funds are available. There again, there are so many companies that look attractive buys at current valuations - how to choose?

Lower freight costs, stronger sterling, and supply chains normalising should all be helpful. Whereas staff wages rising is probably the main headwind.

More for value investors, than quality investors, I’d say.

Management are good I think, tenacious & committed, with Andrew Wass holding 23% still, and sitting on a big cash pile (c.£24m!) from well-timed previous sales! Well good for him, it shows he’s shrewd, and he didn't deceive anyone, he just tells it like it is I've found, on my occasional calls/meetings with management.

This is a really lucky share for me. I caught both the big bull runs, with large positions, happily sold near the top - more luck than judgement. So I will be eternally grateful to management here.

Will G4M shares make it a hat-trick, or is it destined to remain Bactrian? Only time will tell.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.