Good morning from Paul!

Today's report is now finished. Thanks for all your interesting comments this week, and I'll record this week's podcast tomorrow morning. Have a relaxing weekend, we need it!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Quiet today, so I'm catching up on backlog items -

Summaries

Gear4music (HOLDINGS) (LON:G4M) - down 7% to 125p (£26m) - H1 Trading Update - Paul - AMBER

Confirms trading in line with FY 3/2024 expectations (a modest £1.2m PBT). But cost cutting in H1 should boost H2 and next year's profit maybe? I like the strategy, but question whether low margin eCommerce companies that have largely gone ex-growth will ever command premium valuations again? There might be some upside here maybe?

Hollywood Bowl (LON:BOWL) - up 3% to 241p y’day (£413m) - Trading Update FY 9/2023 - Paul - GREEN

Is it ahead of expectations or in line? Fudged wording has left me unsure. PER of 12x, >5% dividend yield, and self-funding growth, with pots of cash in the bank - a very attractive investment proposition I'd say. So another thumbs up from me.

Saietta (LON:SED) - down 29% to 27p (£28m) - FY 3/2023 Results & Resumption of trading - Paul - RED

Just awful. Shares have come back from suspension, due to late FY 3/2023 accounts. Material uncertainty red flag in going concern statement. Probably out of cash, or close to it by now. Could easily be a zero. I've deployed my bargepole, and borrowed another one from a friend, just to be sure!

IQGeo (LON:IQG) - 255p (£157m) - Call with management - Paul - AMBER

See my notes below from a call with management yesterday. They wanted to talk me through my balance sheet concerns, which I'm pleased to say seem OK. This looks a very interesting rapid growth company. I would be green, were it not for the rather high valuation. Well worth people taking a look at IQG, if you are prepared to pay up for exceptional growth. Now profitable and cash generative too.

PROCOOK (LON:PROC) - down 13% to 18.7p (£21m) - Q2 Trading Update - Paul - RED

Shops and eCommerce seller of kitchen goods. Q2 saw a continuing fall in sales, although slightly better than Q1. Looks on track to make another loss this year, I reckon. Tiny free float - delisting risk? Why get involved, when there's no sign of a trading recovery yet?

Paul's Section:

Gear4music (HOLDINGS) (LON:G4M)

Down 7% to 125p (£26m) - H1 Trading Update - Paul - AMBER

Gear4music (Holdings) plc ("Gear4music" or "the Group"), the largest UK based online retailer of musical instruments and music equipment, today announces a trading update for the six months to 30 September 2023.

H1 (quieter half) revenues down 6% - not a problem, as the stated strategy is now to focus on profitability, not sales growth.

“Challenging market”

Net debt £18.1m, down £3.7m on a year ago, but up £3.6m from the 31 March 2023 year end figure of £14.5m. It says this is due to normal seasonal inventory build-up for peak trading over Xmas.

Cost savings - some serious inroads into overheads have been made, £4.0m annualised savings already implemented, mostly in software team salaries - which did previously strike me as a rather excessive level of spend.

Outlook -

* Gear4music believes that current consensus market expectations for the year ending 31 March 2024 are revenue of £161.7 million, EBITDA of £9.8 million and profit before tax of £1.2 million.

That’s good to see they’ve included the consensus PBT figure of £1.2m, I think that’s new. In the past it was the highly misleading EBITDA figure only that was quoted. Look at the gulf between them: £9.8m EBITDA and only £1.2m PBT!

Paul’s opinion - I like the strategy of focusing on lean costs, and profits, ahead of revenue growth.

How to value it? Modest PBT of £1.2m this year (FY 3/2024) could be improved on next year (FY 3/2025) possibly, as a full year of cost reductions should help, and possibly something of a consumer recovery maybe, as real incomes have turned positive again? Singers seems to be thinking along the same lines, and has a jump from £1.1m adj PBT this year, rising to £2.7m for next year. In EPS terms, that’s 3.6p to 9.2p. What PER? In a future bull market, maybe 20x, so that’s 184p, a handy 47% upside - not really enough to get me excited, when I’m surrounded with opportunities for shares that could easily double or triple in the next bull market.

Therefore, I think I’ll stick with AMBER - no strong view either way. £26m plus the debt, means an EV of c.£40m (using year end debt, rather than the seasonal peak at interim period end), which is probably enough for a very low margin business that’s gone ex-growth arguably.

It’s difficult to imagine that racy valuations for eCommerce businesses are likely to come back any time soon, if at all. I caught both of the big surges in G4M over the years, so this has been a very lucky, and lucrative share for me. It's difficult to see how a similar surge would happen again.

Hollywood Bowl (LON:BOWL)

Up 3% to 241p y’day (£413m) - Trading Update FY 9/2023 - Paul - GREEN

Hollywood Bowl Group plc, ("Hollywood Bowl" or the "Group"), the UK and Canada's largest ten-pin bowling operator, announces a trading update for the financial year ended 30 September 2023 (FY23).

Excellent financial and operational performance in the UK and Canada following continued strong customer demand.

Revenue £215m (up 11%, or up 16% underlying: one-off VAT benefit for LY adjusted out)

90% of revenue is UK, 10% Canada.

LFL revenue growth (excluding new sites opened) was +4.1% in the UK - OK, but below inflation. Canada a much more impressive +15.1% (constant currency).

Odd wording here - I don’t like companies messing around with the wording of comparisons to market expectations. They’re either ahead, or not, this muddies the water -

The Group expects to report EBITDA growth (pre-IFRS 16), ahead of market expectations

There are not any broker notes, so I’m in the dark as to whether this is an earnings beat, or not?

Lots going on, with new sites, and refurbs, all self-funded from cashflow.

Net cash of £52.4m, plus undrawn £25m RCF.

Final divi of at least 7p. Stockopedia shows a forecast yield of 5.3%, very nice. Especially as the likelihood seems to be that future divis could continue increasing, as the business expands. Self-funding growth, and paying a 5.3% yield, impresses me a lot.

Paul’s opinion - I’m always GREEN on BOWL, because it’s a cracking business, reasonably priced, and always seems to trade well, regardless of macro factors.

Assuming no change in forecasts, then Stockopedia has it on a forward PER of only 12.0x - that seems smashing value, for a high margin, self-funded growth company, with plenty of net cash, that is paying a >5% dividend yield.

Why is it such good value? The only reason I can come up with is the risk of possibly customers losing interest in bowling, and over time increased competition. There doesn’t seem any sign of that happening though. Or it could just be due to general malaise in small caps - more sellers than buyers, for reasons unconnected with the fundamentals of the business maybe?

Considering how much progress in size, and profits, that BOWL has delivered in the last 6 years, despite the pandemic, energy and cost of living crises, nothing much has happened to the share price. This is really surprising I think.

Hence it has to be another GREEN view from me on BOWL shares. Are we missing something here? If any readers take a more bearish view, do post a comment.

Saietta (LON:SED)

Down 29% to 27p (£28m) - FY 3/2023 Results & Resumption of trading - Paul - RED

Lifting of suspension of its shares was done at 12:30 yesterday, after publication of overdue FY 3/2023 results.

I can remember that we previously thought this share was a steaming pile of rubbish, based on the appalling facts & figures. Checking my notes confirms that recollection. We flagged high risk and heavy cash burn, marking it RED on 6/12/2022, 12/4/2023, and 25/9/2023, warning readers away from it in the strongest possible terms. Meanwhile, unscrupulous paid PR promoters were pumping this stock to the gullible. Same old story at the bottom end of AIM, I’m afraid.

FY 3/2023 Results - already 7 months out of date almost.

Saietta Group plc (AIM: SED), the multi-national business which designs, engineers and manufactures complete electric drivetrain (eDrive) solutions for electric vehicles, announces its full year results for the 12 months ended 31 March 2023 and provides an operational and financial update.

RED FLAG! Material uncertainty in going concern statement -

Furthermore, the forecasts also include payments from Saietta VNA, the Group's joint venture in India, for equipment for fully automated production of AFT motors. The Group has spent £3m on such equipment and this amount is to be reimbursed by Saietta VNA. In the absence of such reimbursement there may also be a need to raise additional funding

Whilst the Directors expect that additional funding can be raised this is not guaranteed and when continuing with an accelerated expansion this presents a material uncertainty which may cast significant doubt over the Group's and the Company's ability to continue as a going concern

FY 3/2023 figures -

Revenue £2.1m (up 52%)

Operating loss of £(19.4)m - this is not a typo. The previous year was a loss of £(10.9)m.

There’s an additional £7.9m loss from discontinued operations on top.

I can scarcely believe these figures, they’re so bad.

Balance sheet - cash has reduced from £18.4m to £7.2m between March 2022 and March 2023. On that trajectory, there’s probably nothing left by now.

Paul’s opinion - this is a disaster. I see the CFO announced his resignation on 6 Oct 2023, effective once the late accounts were filed.

As things stand, the company looks likely to go bust imminently, or be forced into a highly dilutive fundraise. Or, a miracle might happen, who knows?

I’ll happily look at it again with fresh eyes, once it has refinanced, but at the moment it’s a double bargepole.

It’s possible that SED’s technology might be world-beating, but as we’ve seen with many companies like this, commercialising it is quite another thing, and always takes far longer, and costs far more than originally planned. People who invest in these IPOs nearly always get taken for a ride, over the cliff, like boarding a highly efficient, but doomed electric rickshaw perhaps? Maybe it’s the investing equivalent of Thelma and Louise, but with less engine noise and wheelspin? It rarely pays to be an optimist, with cash burning minnows on AIM. Why get involved, when it’s almost certainly dangling by a thread in terms of cash?

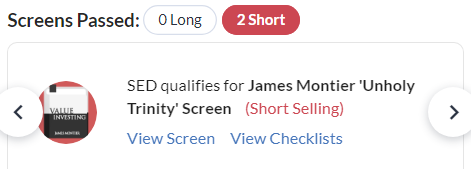

The only Stockopedia screens that SED qualifies for, are James Montier style shorting ones - although something this small isn't really practical to short. Also I would never personally short anything tiny, because the risk involved is potentially ruinous. A friend once shorted something at 1p, certain it would go bust, and it spiked up to 31p. Imagine that - a £10k position suddenly became a £300k loss, when something completely unforeseen happened.

Another friend lost about £1m shorting some Chinese fraud. Everyone knew it was a fraud, but when the shares were suspended (worthless), the Chinese promoters had cornered the market, and his broker was forced to buy back the short at a ludicrous price demanded by the Chinese. So I would strongly urge everyone here to not even think about shorting small caps, it's way too risky and could ruin your life. It only needs one to go spectacularly wrong.

IQGeo (LON:IQG)

255p (£157m) - Call with management - Paul - AMBER

I reviewed the interim results from this interesting software company here on 26 Sept 2023. I was very impressed with the big organic growth of 83% in H1, turning 2023 into a breakthrough year where years of losses have now moved into profit. So definitely a company I want to research in more detail.

It offers specialist cloud-based geo-spatial software mainly for telecoms and utility companies, globally. Customers use the software to plan, record, and manage their large networks of physical assets (eg. fibre networks, other cables and pipes, etc). The rapid growth clearly demonstrates that the product is resonating with clients, hence why I’m keen to learn more about the company.

I also flagged a couple of negative points - valuation of the shares strikes me as too high, although that’s subjective, and rapid growth companies are rarely cheap!

Also I had a concern about the very high level of receivables on the balance sheet at June 2023, presenting a risk that customers might not pay maybe?

An adviser reached out, and offered me a call with management, to resolve my queries, and also so I could learn more about the company, ask questions, see a presentation slide deck, etc. So I had a most interesting online meeting with management yesterday, and thought I’d update readers here on my balance sheet query in particular.

High receivables - the CFO said a number of factors had boosted year-end receivables, including a £1.8m invoice paid a few days after the period end. Plus another £1.2m where a customer had got into an accounting muddle, since resolved.

All bar £21k of the 30 June receivables have now been paid by customers, which is the key point - obviously I’m basing this on trust.

Another point, which I hope isn’t commercially sensitive, is that deals done with some customers allow them more time to pay on an agreed basis. You can see that from the 2022 annual report anyway, which shows that overdue invoices are nearly all 0-90 days overdue, so not seriously overdue.

Also the rapid growth means receivables look high compared with revenues, because the most recently billed things will be much larger than revenues billed 6 months earlier.

It’s not ideal having extended receivables, but the explanations from the CFO seemed credible, and there doesn’t seem to be a broader problem.

So I’m happy to say I think this looks OK, but I’ll keep an eye on future balance sheets, as we do need to see receivables reducing as a percentage of revenues.

Product/market - this was very interesting. It seems that IQG is in a sweet spot, where its software is providing what utilities want, in the right way. Whereas competition is said to be mainly older established, non-cloud based. IQG reckons it’s 2 years ahead of the competition, with better software, in the cloud.

Land & expand strategy, so a lot of growth is coming from customers who trial part of IQG’s offering, then buy more modules, and more users. It eliminates “swivel-desking” (what a great phrase!) where users have to use several different software systems to do different parts of their work.

IQG’s software is mission-critical, and customers are very sticky - typically each contract win sets up a 20-year+ relationship with the client, with recurring revenues, upgrades, etc.

Very good markets, “riding the wave” of big telecoms spending on fibre networks.

Market size is massive, and global. IQG targets larger customers first, and management seem ambitious about securing a decent market share over time - and I keep coming back to that stunning 83% organic growth in H1 revenues. Obviously large % gains inevitably moderate over time.

Just won a competitive technical tender, where the customer was prepared to pay substantially more for IQG’s system, because it was better than the competition.

Drivers for demand are waves of capex being undertaken by utilities, and replacing outdated systems.

Flexible cost base, making use of some consultants for implementations, etc.

Very low customer churn.

65% of revenues are N.America - I wonder if it could be a takeover target maybe (although this wasn’t mentioned on the call).

Typical contracts are 3 years initial, then rolling annually.

See customer testimonials on website.

Investor meeting at Cavendish’s office on 29 Nov 2023.

Capitalising c.65% of development spending.

Moving to cashflow positive this year, so cash pile looks adequate I think - low dilution risk, unless they do more acquisitions, and high market cap means a little dilution wouldn’t worry me.

Addressable market c.£2.5bn ARR - plenty to go for.

Key advantages are - fast moving nimble business, global presence & huge markets, low staff turnover, acquisitions have gone really well, cashflow positive & profitable now, very rapid organic growth shows the product is in demand (in a sweet spot).

Paul’s opinion - I was previously AMBER/RED, due to my balance sheet concerns. Those are now resolved satisfactorily, and having learned more about the company, I’m much more positive about its potential. So leaning towards a positive view, but the high valuation means I think I’ll go up to AMBER for the time being.

Overall then, IQG looks a really good, rapid growth company, but a little too expensive for me at this stage. I could see this company being a long-term winner though. A bit like Cerillion (LON:CER) (different niche, but in a similar area), which is another growth company I really rate highly, it could be worth just paying up for these two shares. Long-term, investors who paid up for quality a few years ago, have been very well rewarded.

Here's a short video presentation from management, re recent interims - gives a flavour for the top team, who I think seem strong -

PROCOOK (LON:PROC)

Down 13% to 18.7p (£21m) - Q2 Trading Update - Paul - RED

ProCook Group plc ("ProCook" or "the Group"), the UK's leading direct-to-consumer specialist kitchenware brand, today reports on Q2 trading results for the 16 weeks ended 15 October 2023.

The current financial year is FY 3/2024.

There’s a slightly improving trend re % sales decline from Q1 to Q2, but for H1 as a whole, sales of £26.3m is down 3.8% on LY, and down 4.4% on a LFL basis. At a time of considerably increased costs (eg wages and energy especially), this can’t be good for profitability. It doesn’t provide any clear guidance on profitability, just saying -

However, the Board remains cautious with regards to the FY24 outlook given the highly challenging market conditions which persist, and the current trading volatility and sales trends over recent weeks, with customers seeking more value and taking more time to research before committing to purchase.

Trading in September and into early October has been markedly softer…

Net debt is £3.2m - slightly up on £2.8m six months earlier. Available liquidity of £12.8m sounds good, but I wouldn’t be surprised to see bank facilities reduced at some stage.

Paul’s opinion - I’d be very surprised if it gets anywhere near the £3.5m net profit figure shown on the StockReport. Another loss strikes me as more likely, but we’ll see. FY 3/2023 saw a small underlying loss of £(0.2)m - not a disaster, but I can’t see any signs of recovery yet. The last balance sheet at March 2023 looks adequate, with about £9m NTAV.

The O’Neill family completely dominate the shareholder register, and there’s hardly any free float. Hence I would say delisting risk here looks very high - I cannot see why they would want to continue with a stock market listing that hasn’t worked (due to poor performance after the 2021 boom turned to bust).

We’ve been RED in our previous reviews, on 14/12/2022, 19/4/2023, and 28/6/2023. I think we’d need to see firm evidence of a trading recovery to consider moderating that to amber. Given the continued soft trading, and the delisting risk, I’ve got to stick with RED for the time being. Why get involved?

.

Another vintage 2021 float -

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.