Good morning from Paul & Graham!

Mello Monday is tonight from 17:00 - a couple of interesting companies that we follow here are presenting, namely Solid State (LON:SOLI) and Sosandar (LON:SOS) (I hold).

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Agenda for today - at the moment Graham and I are scratching around, trying to find anything interesting to write about, so we can avoid having to spend any time on Team Internet! ;-)

Summaries

FDM (Holdings) (LON:FDM) - down 12% at 411p (at 08:08) £451m - Trading Update (2024 profit warning) - Paul - BLACK / AMBER

Profit warning, slightly below for 2023, but warns for 2024. Big (18%) drop in consultants currently hired out. Strong balance sheet confirmed by me, and generous dividend yield, since all earnings are paid out to shareholders. Could be an interesting one for a cyclical recovery at some point (maybe not yet though?). Nice quality business. (Edited below to include new forecasts from Shore).

British Land (LON:BLND) - up 6% to 333.4p (£3.1 billion) - Half-year report (strong rental growth) - Graham - GREEN

Rental growth is expected at the top end of previous guidance as BLND continues to sign up tenants at very strong prices across its portfolio of campuses, retail parks and urban logistics. At a hefty discount to official NAV and a divi yield of 7%, I like the look of BLND.

XP Power (LON:XPP) - 1,217p (£293m) - Fundraising - Paul - AMBER/RED

I'm pleasantly surprised by the generosity of shareholders, injecting fresh equity at an impressive premium from the recent lows. That triggers the bank slightly relaxing covenants, although debt remains uncomfortably high. An excellent rebound from the recent lows, but there are still questions hanging over this company - mainly, what caused profits to plunge? Is that just a one-off, or sign of a deeper malaise? I don't know, so am keeping clear for now.

Paul’s Section:

FDM (Holdings) (LON:FDM)

Down 12% at 411p (at 08:08) £451m - Trading Update (2024 profit warning) - Paul - BLACK for spreadsheet / AMBER on fundamentals

FDM Group, a global professional services provider with a focus on Information Technology, today provides the following trading update.

Tricky one this. Is it a profit warning? I’d say yes - a slight miss (“broadly in line”) for FY 12/2023, but performance for FY 12/2024 will be “impacted” by “lower than previously anticipated” number of consultants assigned to clients.

The numbers have fallen a lot - this is down 18% for Oct 23 vs Oct 22 -

Consultants assigned to clients at the end of October 2023 were 4,136 (end of October 2022: 5,014), (30 June 2023: 4,602).

Reasons given - client caution (which we’re hearing from quite a few B2B companies at present) -

Since the publication of our Interim Results announcement on 26 July 2023, macro-economic and geo-political uncertainty has continued to cause clients to delay and defer decisions around project commencements and Consultant placements.

Nonetheless, levels of client engagement continue to give us encouragement and there are some signs that confidence is slowly beginning to return, albeit varying by geography.

Balance sheet - it says this today -

The Group has a robust balance sheet, with £35.3 million cash at 31 October 2023 (31 October 2022: £34.4 million), (30 June 2023: £38.1 million), and no debt. An interim dividend of £0.17 per share, amounting to £18.5 million, was paid on 13 October 2023.

I always have to check balance sheets myself, as you simply cannot rely on what companies say about their own balance sheets. Often it can be a contrary sign when management claim to have a strong balance sheet!

The good news here is that FDM does have a healthy balance sheet, with minimal fixed assets, and plenty of working capital, with £38m net cash at June 2023.

Paul’s opinion - this looks a very nice business. It makes a good strong profit margin, from training and hiring out IT consultants. It's a glorified specialist staffing company really.

It has a clean, capital-light balance sheet with ample cash and working capital.

The cashflow statements are also very impressive - lots of cash generated, which is pretty much all paid out in divis, because there’s negligible capex required.

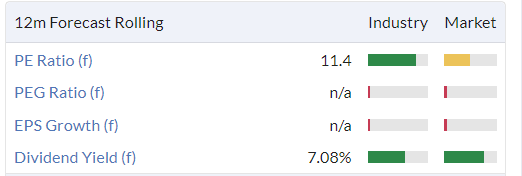

Stockopedia shows a forecast divi yield of 7.9% based on a share price of 467p (Friday’s close). I imagine the share price is likely to take a tumble today, as lower earnings are now expected for 2024. This means probably a lower divi, as all earnings are paid out in divis.

There has been a sharp fall in activity recently, which is going to hurt profits in 2023 a little, and more in 2024.

I haven’t yet seen any broker notes available, but Shore Capital normally covers it. EDIT: see below for updated Shore figures.

It’s maybe too early to start thinking about bottom-fishing here for a bargain.

Note that FDM shares have already crashed a lot, and once sellers have done their worst today, it’s probably going to be not much above the 2014 main listing float.

Although note that it was previously listed on AIM, but management nicked it off us (I was a shareholder at the time), taking it private with Inflexion Private Equity for a song (£33m) in 2010, then re-floating it 4 years later for £200m! So they very much look after themselves first and foremost, although that’s probably true of management at pretty much all listed companies.

At some stage though, I would say FDM shares would be a nice recovery share, as it’s a fundamentally decent business.

So for now, and with incomplete information, I’ll go with AMBER.

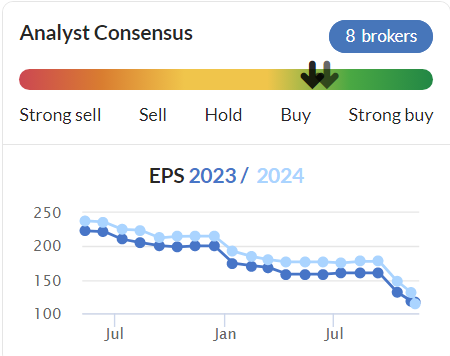

EDIT: an update note has just come through from Shore Capital, via Research Tree, many thanks to both. Revised forecasts are now -

FY 12/2023: adj EPS revised down 6% to 33.2p

FY 12/2024: adj EPS revised down 25% to 26.6p

That’s quite a sizeable reduction in forecast earnings. What multiple should we value the company on? I would say 12x 2024 forecast should be a fairly safe base case valuation, so that’s 319p. The current share price is 397p (at 10:05), a PER of 14.9x the reduced 2024 forecast. Not exactly a bargain, but that depends on whether you see 2024 as a one-off bad year, and recovery to come in 2025 (or 2024 itself might surprise on the upside).

Since the macro outlook is very uncertain at present, I remain of the view that it feels too early to jump in here, hoping for a recovery. So I’ll stick with AMBER, as above.

XP Power (LON:XPP)

1,217p (£293m) - Fundraising - Paul - AMBER/RED

This is an international group, making electrical power converters - examples of its products are here.

After a long bull run, which saw it roughly 40-bag from 2008 to 2021, the wheels have really come off in the last 2 years -

Our coverage here quickly summarises recent events -

2/8/2023 - AMBER 1950p - Roland worried about high debt. But saw it as possible value, and a turnaround.

2/10/2023 - RED - Profit warning crashes shares 46% to 1286p. Possible covenant breach.

6/10/2023 - RED - Lurches down another 10% to 730p on divi canx. Looks high risk.

27/10/2023 - RED - 1094p - Q3 trading stabilising. Hints at a placing.

We had no choice but to stick with RED, until it managed to refinance. Remember our traffic lights are not intended to predict the future! We’re just flagging risk, and you can make up your own mind if the reward outweighs the risks or not.

Investors who held their nerve have been nicely rewarded, with a c.57% rebound from the 776p recent low to today’s 1,217p - good to see!

Refinancing - this is the news I want to look at today. A placing of £44m and small retail offer up to £1.5m was announced on 6/11/2023. This is a 20% enlargement of the share count. Price was noteworthy, at 1150p per share, a premium of 6% on a share price that had already bounced strongly from the lows.

Note that net debt was £163m on 2 Oct 2023, so this placing is only dealing with about a quarter of the debt.

Debt will remain high -

The Funding Plan is expected to leave the Group's leverage broadly at the top end of the Company's previously stated target range by year end 2024.

Borrowing facilities amended, to slightly relax the covenants, dependent on completion of the fundraise.

Opportunistic bid approaches rejected -

Since the trading update of 2 October 2023, a small number of parties have expressed indicative, non binding interest in acquiring the Company at prices which the Board considers fundamentally undervalue the Company and its long-term prospects. Having considered each of these unsolicited expressions of interest, with its advisers, the Board does not believe that any of them are at a value which merits further engagement with any of those parties and has had no hesitation in unequivocally rejecting them.

Outlook -

While, as previously announced, 2023 will not deliver the financial progress the Company had forecast earlier in the year, it is expected to result in a trading performance similar to the prior year in what have become increasingly challenging end market conditions.

While it is too early to provide specific guidance for 2024, the Board expects to enter the new financial year with a sizeable order book, largely for delivery in the year. The Group will also benefit from the recent significant action taken on costs and cash.

Longer term, the Group has a strong pipeline of potential design wins, and existing product, combined with end markets that have excellent through the cycle growth drivers. The Board therefore expects, on average, to grow ahead of its markets while returning margins and cash to historic levels.

Revised forecasts - nothing detailed is available I’m afraid. But we have got broker consensus numbers, showing c.115p EPS for both FY 12/2023 and FY 12/2024 - very much lower than previous forecasts -

Valuation - on the latest forecasts, and at 1217p/share, the PER is about 10.6x.

That doesn’t strike me as a particular bargain, given that XPP will still have a heavy debt burden.

Paul’s opinion - what an interesting situation, where it seems likely that existing shareholders strongly supported the company with fresh cash for new equity, to protect the value of their existing holdings. Management must have delivered some impressive investor presentations to get this degree of support, with a placing at a 6% premium on an already strongly rebounded price. That’s a surprising outcome for sure in a bear market.

Well done to anyone who caught the bounce, but I don’t see anything attractive in the current price. It’s still not clear why earnings plummeted from previous expectations.

I see this fundraise as a case of avoiding disaster, rather than a comprehensive solution to XPP’s problems.

Further upside could come from a recovery to historic margins, which management talks about. I wouldn’t want to bet on that happening, when I’ve not had it properly explained why margins crashed in the first place.

So it’s not for me.

Although to reflect the reduced risk from the placing, I’ll move from RED to AMBER/RED.

Graham’s Section:

British Land (LON:BLND)

Share price: 333.4p (+6%)

Market cap: £3.1 billion

This is one of the largest UK REITs. For an overview of the sector, I recommend Roland’s article from July.

As interest rates rose from 2022 until now, the BLND share price has responded as you might expect, down by nearly 50% from peak to trough:

Let’s take a look at today’s interim results.

Headlines:

Underlying profit growth 3.4% to £142m

Underlying EPS growth 3.4%, to 15.2p

Dividend per share growth 4.8%, to 12.16p

The StockReport suggests an EPS forecast for the current year (FY March 2024) of 27.4p, putting this on a PER of about 11x, or perhaps more like 12x after this morning’s share price increase.

Balance sheet highlights are quite interesting:

Net tangible assets per share (calculated using EPRA methods) are 565p, nearly 70% above the current share price. Among other things, this calculation excludes the taxes that would be payable if properties were sold.

Loan to value 36.9%; looking at this figure in isolation it suggests to me that leverage is modest.

Net debt to EBITDA 6x; this would be high for a normal operating business but real estate companies can be treated differently.

Other key points around the balance sheet: the company has an investment-grade “A” credit rating from Fitch, enormous liquidity of £1.7 billion in undrawn facilities and cash, and another £350m of new loans since H1 ended.

Occupancy is excellent at 96%. New deals with tenants have been signed at an average 12% premium to the estimated rental value used in portfolio valuations.

Valuation is down 2.5%, with the main driver being a 4% fall in the estimated value of campuses. Of course the stock market is going to be more pessimistic than this (e.g. BLND share price down 20% year-to-date). It’s noteworthy that rents are going up even as valuations are going down.

Outlook is positive with estimated rental value growth at the top end of previously guided ranges for FY March 2024. So that means rental growth of about 4%-5% in each category.

Additionally, BLND are “comfortable with current market expectations”.

Graham’s view

We don’t cover REITs very often in this report, and we have never covered BLND. However, on a quiet news day, there is no harm in taking a quick look.

Should small-cap investors take an interest in these? Well, given that valuations are so beaten up at the bottom end of the market, I would be more interested in the higher-risk, higher-reward situations available down there.

That said, anyone who is looking to de-risk while still enjoying a decent return might find that large REITs are a reasonable proposition. Of course it’s still necessary to diversify and to research the individual REITs that you are investing in.

My own view on BLND is that it’s offering investors a pretty good deal right now. The disparity between the company’s balance sheet value (around £5.4 billion) and market cap (£3.1 billion) could probably be explained by a combination of economic concerns - exposure to retail - and a demand for higher rates of return than the BLND property valuation implies.

Investors might also be concerned about the office portfolio, although BLND insists that demand and occupancy remain high. The typical tenant of its prime London office portfolio is the UK headquarters of a large corporate.

At its current official valuation, the yield on BLND’s portfolio is just over 6% (the “Net Equivalent Yield”).

But with inflation still at 6.7%, and with low-risk fixed rates of 6% available, perhaps it makes sense that investors aren’t willing to mark the BLND portfolio at its official fair value.

Instead, the BLND share price is discounted low enough that the dividend yield on the shares gets up to 7%. The underlying earnings yield on the shares is another step higher again.

While I think there are many bargains in the market right now, I do think that BLND is probably one of them. If I was looking to park some money in a lower-risk way than the small-cap end of the market, I’d certainly consider this.

So I’ll give this one the thumbs up.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.