Good morning from Paul & Graham!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

.

Summaries

System1 (LON:SYS1) - up 25% 218p (£27m) - Interim Results - Graham - AMBER

Some strong earnings upgrades at this marketing platform with higher margins, operating efficiencies, and a positive outlook statement all contributing to a brighter picture here. A robust cash balance also strengthens confidence. Might be worth looking at again.

Graham’s Section

System1 (LON:SYS1)

Share price: 218p (+25%)

Market cap: £27m

System1 Group the marketing decision-making platform www.system1group.com announces its unaudited interim results for the six months ended 30 September 2023 ("H1", "H1 FY24").

We last covered this one in September, when it announced that it would beat expectations for the current financial year (FY March 2024).

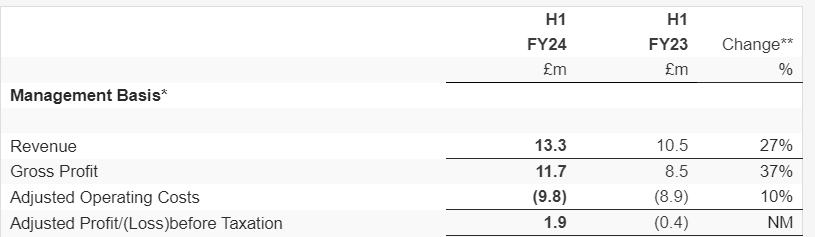

Today’s adjusted numbers are a significant improvement on last year, with the company crossing over from a loss into profitability, and with a 27% improvement in revenues:

The company was previously forecast to generate adjusted PBT of less than £1m for the entire year - but in fact we have £1.9m in H1 alone.

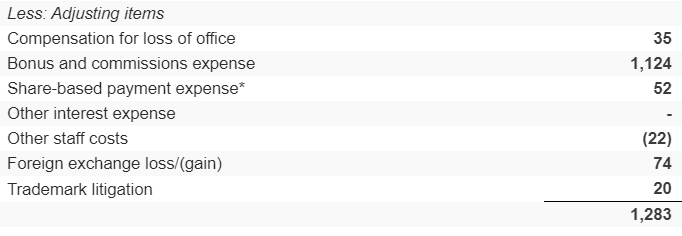

However, before we go any further, let’s make sure we are comfortable with the definition of “adjusted” PBT. Here are the costs that get adjusted out:

“Bonus and commissions” are not something I would be inclined to adjust out, and so personally I can’t sign off on the idea that the adjusted numbers are more meaningful than the actual numbers.

Here are the actual H1 numbers (this year highlighted in yellow). They are still a significant improvement on last year:

SYS1 reached a settlement with another company using the name “System1”, and is going to receive payments over time from this other company. The total value of the payments is confidential but they are included within “Other Operating Income” (£0.3m in the above table).

Cash balance rises to £6.3m.

H1 Highlights

136 new clients (H1 last year: 69) and improved retention of existing clients.

Gross margin 87.8% (H1 LY: 81.5%), and cost of sales down, “due to platform and supply chain efficiencies”.

Current trading/outlook: mostly positive.

Second half of the year has started well, and at this stage we expect H2 revenue to exceed H1.

Gross profit margin to date remains close to that achieved in H1, and well above recent historic levels.

Despite a difficult economic environment in some key markets, and challenging conditions for media owners and advertisers, we believe System1 can continue to grow profitably by gaining market share from large incumbents that we believe have less predictive products.

CEO comment proudly mentions the large number of new clients, which include “a global top three advertiser, a leading global breakfast foods company, a leading European car manufacturer, a leading budget airline, a 'big four' UK supermarket, and a multinational consumer goods company.”

Estimates: Canaccord Genuity have upgraded their adj. PBT forecast for the current year from £1m to £1.6m, thanks to higher expected margins and operational gearing. The revenue estimate is nudged only slightly higher to £26.9m.

Graham’s view

I’ve been amber on this one for some time, and I’m inclined to maintain this stance for now.

However, the share price reaction this morning suggests a great deal of interest in developments here:

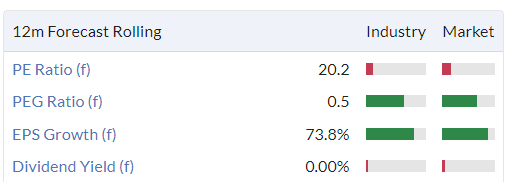

The most generous way to value this would be on adj. PBT and to treat it as a growth stock, with a growth multiple. With 27% revenue growth in H1, it might be possible to justify that.

The strong balance sheet is another factor here; cash of £6m means the “enterprise value” is only £21m, even after this morning’s gains.

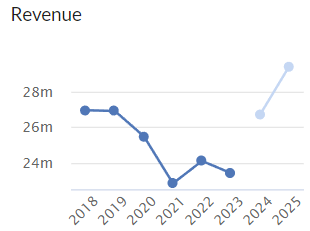

Bear points: the company’s overall revenue profile has been uneven, as its business model has evolved:

Also, there is “only” revenue growth of 10% expected for FY April 2025; not a bad result but I’m not sure that it would help to justify an above-average earnings multiple for the stock.

So for now, I’m inclined to think that this stock remains around fair value. But this morning’s H1 results were very good: hopefully this is a sign of more good things to come.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.