Good morning from Paul & Graham!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Summaries

Hollywood Bowl (LON:BOWL) - Up 1% to 285p (at 08:28) £490m - Final Results FY 9/2023 - Paul - GREEN

FY 9/2023 results look in line with forecasts that were raised several times in 2023. This is a lovely cash generative business, with little working capital required, so it's sitting on a decent cash pile of £53m that's now earning interest income. I can't fault this share, still reasonably priced too.

Keywords Studios (LON:KWS) - up 2% to £14.45p (£1.14bn) - Acquisition - Graham - AMBER

This support services provider to the video game industry saw its share price double during the Covid boom. Having now returned closer to our normal market cap territory, today’s £76.5m acquisition sounds promising. KWS may possibly have grown into this market cap.

Paul’s Section:

Hollywood Bowl (LON:BOWL)

Up 1% to 285p (at 08:28) £490m - Final Results FY 9/2023 - Paul - GREEN

Hollywood Bowl Group plc, the UK and Canada's largest ten-pin bowling operator, announces its audited results for the year ended 30 September 2023 ("FY2023").

EXCELLENT PERFORMANCE DRIVEN BY STRONG CUSTOMER DEMAND

AND THE SUCCESS OF THE GROUP'S FOCUSED INVESTMENT STRATEGY

These results look good to me, after allowing for the one-off boost which last year enjoyed from VAT relief (a pandemic support measure).

Revenue £215.1m (mostly UK £192.6m, plus Canada £22.5m)

LFL revenues (excl new site openings) up 4.5% - not bad, but behind inflation.

Group adj PBT £47.8m is actually down £0.9m on FY 9/2022, but that is distorted by a one-off VAT gain last year of £8.6m.

Stripping out last year’s VAT boost, results in £47.8m vs £39.9m LY adj PBT, a healthy progression of +20% in profitability - I think this is a fair adjustment, showing us the underlying improvement.

Commentary says performance exceeded management expectations, but it’s only slightly above market expectations, adj EPS actual of 21.48p vs broker consensus of 21.4p. Note that broker forecasts have been raised during 2023, so this looks healthy to me, given tough macro -

PER is 13.2x based on Friday’s closing price of 283p - hardly demanding, still good value I’d say, even after a strong recent run upwards in share price.

Total divis (incl. a special) of 14.54p, that’s a 5.1% yield (incl special)

Share buyback of £10m announced.

Adjustments to profit boost it by £2.7m, but do look reasonable to me - relating to the Canada acquisition costs & adj to consideration, so I think it’s fine to strip those costs out to show the underlying trading.

Note that interest earned on cash is £1.4m vs negligible last year, a nice boost there.

Finance expense of £10.4m nearly all relates to leases under the rubbish IFRS 16 rules. I’m pleased to see that BOWL says it will keep reporting pre-IFRS 16 EBITDA, as that’s what investors (and banks) want.

Outlook - encouraging start to the new year, it says, but no detail provided.

Balance sheet - actually isn’t as strong as I was expecting, with a relatively modest £59m of NTAV, after I write off £89m of goodwill.

This is absolutely fine though, because BOWL hardly has any inventories or receivables, which means almost all the NTAV is net cash of £52.5m.

Property is nearly all leased, with large lease entries on the balance sheet, showing a deficit of £43m - which suggests it might have some under-performing sites? That is also possibly why there were some write-offs against fixed assets both this year and last? Something to ask management if you speak to them, or on a webinar, if they’re doing one?

Cashflow statement - is smashing, this is a reliable cash generative business. It generates a lot of cash, which not only funds hefty capex (c.£22m pa) plus acquisitions, and generous divis, all from internal cashflow - no borrowings required. It has a £25m unused bank facility.

Paul’s opinion - a really impressive business, no doubt about that. Its listed competitor TEG was recently bought out by a US investor, for around the same earnings multiple as BOWL currently sits on. So I wonder if it might also become a bid target?

It’s difficult to see much, if any downside risk with BOWL.

All I can think of is that gross margin is very high (since the bowling alley revenue has no direct cost of sales), which means profit is highly geared to a downturn in demand. Although given that BOWL seems to have ridden out the cost of living crisis with aplomb, there doesn’t seem any sign of that happening. I like that BOWL says it’s keeping prices competitive, with some food items not having increased since 2019. We could even see geared upside to profit from a consumer recovery in 2024, now that wages are rising faster than inflation, and the 2% NIC cut kicks in from Jan 2024.

All in all, this looks a very good business to me, at a reasonable price, so it has to be GREEN again.

It's really surprising that the share price has almost gone nowhere in 5 years - given that the business and profits have roughly doubled over this period below.

Graham’s Section:

Keywords Studios (LON:KWS)

Share price: £14.45 (+2%)

Market cap: £1.14 billion

This is one of the top 10 AIM stocks by market cap (source) and is strictly speaking beyond our market cap limit. Let’s take a little look at today’s news:

Keywords Studios, the international provider of creative and technology-enabled solutions to the global video games and entertainment industries, is delighted to announce that it has acquired The Multiplayer Group Ltd, a multiplayer focused game development studio headquartered in Nottingham, UK, for £76.5 million.

The current owner of The Multiplayer Group (“MPG”) bought it in 2019, for an undisclosed sum. It’s interesting to see it changing hands again, a little over four years later.

Keywords has a long history of acquisitions in the field of video games support services, and MPG is a co-developer or fully outsourced developer for some of the largest studios in the world. So they appear to be a good match for each other.

MPG’s management team will remain in place and take part in an incentive plan based on targets over the next two years.

Payment: this is a cash purchase.

At its most recent interim results, Keywords had net debt of €11m, very small versus adjusted operating profits for the six-month period of nearly €60m. So it looks like they should be comfortably able to afford this c. €90m acquisition.

Some more info on the financial consequences of the deal:

The business has a strong pipeline of work and is expected to deliver double-digit percentage revenue growth in 2024, with margins in line with those of Keywords' Create division. The transaction is expected to be EPS accretive in its first full year post acquisition and fall within the Group's targeted valuation range of five to seven times EBITDA.

Keywords was already forecast to generate double digit revenue growth in 2024, so I’m not expecting any major change in the revenue growth profile from this acquisition..

The first full year post acquisition is FY December 2024, so MPG should boost EPS next year.

Valuation of 5-7x EBITDA is probably a fair price.

Graham’s view

This seems to be a nice deal for Keywords, with an acquisition that should fit in and hopefully make a meaningful contribution to the group.

Checking the archives (e.g. here and here in April 2019), I previously thought that it might be difficult to justify the valuation of Keywords at £13-£15. This was pre-Covid.

The Covid boom then doubled the company’s share price, but it has since come back to earth. There has been some inflation of the share count over this time. Here’s the 5-year chart:

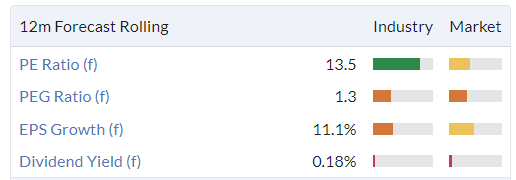

Nearly five years later, the company has grown very well over this timeframe, and has arguably grown into its valuation:

So I’m open to the idea that this could be a more attractive purchase now than it was pre-Covid.

The H1 accounts were a little disappointing to my eyes: free cash flow in H1 was only €11m.

I’ll keep a neutral stance on this share for now but remind me to keep an eye out for its 2023 full-year results. The accounts are likely to be adjustment-heavy but strong full-year cash flows could justify a more bullish stance.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.