Good morning from Paul!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Paul’s Section:

Treatt (LON:TET) - down 3% to 480p (£293m) - Trading Update (AGM) - Paul - COLOUR

Treatt, the manufacturer and supplier of a diverse and sustainable portfolio of natural extracts and ingredients for the beverage, flavour and fragrance industries, provides the following update on trading for the three month period to 31 December 2023 ("Q1")

This financial year is FY 9/2024.

Q1 revenues is down on last year, “as anticipated”, due to (customer) destocking.

Demand expected to normalise in Q2.

Pipeline “healthy”

Cash generation & debt reduction on track, as expected.

Outlook - is this in line or not? Why didn’t they say either way?

Whilst we are mindful of ongoing macroeconomic pressures, we are encouraged by current trading, underpinning our confidence in our trading performance for the year ahead.

Paul’s opinion - I don’t like this announcement. It’s devoid of any figures, and the fact that they don’t directly say whether trading is in line or not, but use an alternative more vague form of words, raises more questions than it answers. Particularly since Q1 was weak, and they’re hoping to catch up in Q2.

This sounds to me as if the risk of a profit warning just increased.

Not good news for a share that’s rated at 19.9x forward earnings.

The big new factory was supposed to increase production & margins, so Q1 being down on last year for revenues is all the more perplexing to me.

I can’t see any broker updates, so overall I’m left slightly uneasy by this vague update.

For that reason, I’m shifting down slightly from green to AMBER/GREEN.

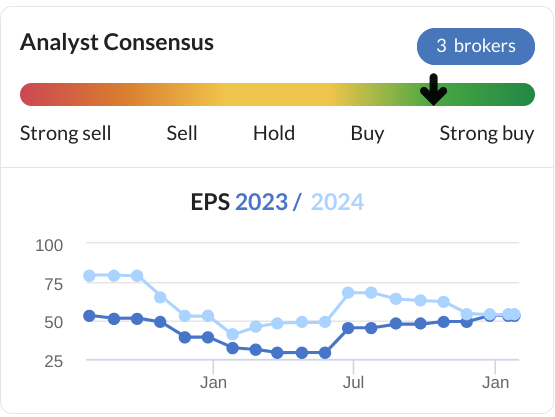

PPHE Hotel (LON:PPH) - up 3% to 1225p (£521m) - Trading Update - Paul - AMBER/GREEN

PPHE Hotel Group, the international hospitality real estate group which develops, owns and operates hotels and resorts, announces a trading update for the year ended 31 December 2023.

FY23 revenue and EBITDA above previously upgraded expectations

See the wide range of EPS forecasts in recent times - for 2023 and 2024, ranging from 25p to 75p, and currently around 53p for both years -

The commentary sounds upbeat -

Fully recovered to pre-pandemic levels (of what? EPS has not matched 80-90p of 2018-2019).

“Extensive development pipeline” of £300m will begin to produce results in 2024, >£25m incremental EBITDA.

Positive “trading momentum”

“we enter 2024 optimistic for a further strong year for the Group."

Only marginal increase in property values.

Guidance for 2023 guided up -

FY 2023 results are expected to be above expectations with revenue of at least £413.0 million (previously £400.0 million) and EBITDA of at least £127.0 million (previously £120.0 million).

Broker notes - nothing available. So I need to work out myself, using previous accounts, how EBITDA turns into actual profit (after large depreciation charges).

In H1 (to June 2023) it did £45m EBITDA, which became only £3.6m in “normalised” PBT.

Clearly it has a big H2 weighting to profits, as the £127m+ FY 12/2023 EBITDA guidance today implies c.£82m in H2 (vs £45m in H1). Assuming everything else remains the same, then I make that adj PBT of c.£40m in H2, giving c.£44m PBT for FY 12/2023.

Taking off say 23% tax, that gives me earnings of £34m PAT, usefully above the £25.5m PAT (“Net Profit”) shown as broker consensus on the StockReport.

Divide my PAT figure of £34m by 42.4m shares (little changed for the last 6 years), I arrive at 80p/share EPS, which is a long way above broker consensus of c.53p.

Maybe my figures are not right, but it does at least show how highly leveraged profits at PPHE are to occupancy, room rates, etc. This is because the company has a high level of bank borrowings, the finance cost of which consumed most of the operating profit in the slower H1 period.

So checking out the terms (cost, variability, covenants, etc) of the bank borrowings is crucial research here.

Asset backing? Stockopedia shows the price to NTAV of 1.72, so fairly decent net asset backing, but earnings & cashflows are key drivers of the share price I’d say.

Paul’s opinion - it’s ahead of expectations, with EBITDA guidance raised from £120m to >£127m, which is obviously good.

Outlook comments are vaguely positive.

It would need a lot more research to properly understand the company and its prospects, and it has some added complications from historic deals to sell hotel rooms, which I’ve not looked into today.

We warmed to PPHE last year, moving up from amber to green. I’m leaning towards viewing this positively too, as the big operational gearing could see profits considerably improve as the effects of the lockdowns continue to wear off. As Whitbread (LON:WTB) says, there’s also a structural under-supply of branded hotels, with a lot of independent operators having shut down and properties turned to alternative uses in recent years. Hence I think hotels are a good place to look for investors at present, maybe. That depends on your macro outlook (my view is quite positive). If you’re negative on macro, then the operational gearing in this sector (big fixed costs) would obviously make it something to avoid.

Interest rates are also key, but that depends on what hedging or fixes PPHE might have in place, I’ve not looked into that here.

I’ll go AMBER/GREEN overall.

System1 (LON:SYS1) - up 2% to 370p (£47m) - Trading update [ahead] - Paul - COLOUR

System1, the marketing decision-making platform www.system1group.com today issues an update on trading for the quarter ended 31 December 2023 (Q3).

Increase in Full Year Guidance

It splits out revenue growth to highlight the main business (“platform”) is delivering excellent growth of 46% in Q3 and 44% YTD. This is blunted somewhat to 28% YTD (still very good!) by declining revenues from consultancy.

If Q4 is similar to Q3, then it’s heading for c.£30m revenues for FY 3/2024. Good going, but SYS1 has done £24-26m pa revenues over the last 6 years, so it’s good but not a step change overall.

Cash is £6.4m, and we’ve commented in the past how we like the cash position.

I’ve checked the last balance sheet, and it’s healthy, with c.£8m NTAV, mostly cash - because it’s a capital-light business model, using know-how rather than plant & equipment.

Impressive client wins -

System1 won over 60 new clients in Q3, and over 200 new clients in FY24 Q1 - Q3. These new clients include Pfizer, M&S, Tesco, easyJet, Toyota, Muller, B&Q, and Just Eat.

Outlook - sounds good to me, if this momentum can be maintained (performance has been patchy at times in the past) -

The Group enters the final quarter of the year with good trading momentum following a consistently strong December quarter. As a consequence, the Board believes that the Group is now well placed to deliver results ahead of previous expectations. Revenue for the current financial year is expected to be at least £29 million (FY23: £23.4 m) and statutory profit before tax to be comfortably above £2 million and materially ahead of current consensus (FY23: £0.7m).

Brokers - any updates? Yes, thanks to Canaccord. It ups forecast EPS to 13.7p (FY 3/2024) amd 19.6p (FY 3/2025). Those are already on the StockReport, and turn into PERs of 26.3x and 18.4x, pricey but I can see why, given that SYS1 seems to have achieved considerable earnings momentum in recent months.

This is how those forecasts look in historical context -

Paul’s opinion - I’m sorry we were too cautious on this one. Checking our previous notes, we stayed amber despite the company making positive noises on 2/8/2023, then ahead of exps on 27/9/2023, although Graham was warming to it by 6/12/2023 Interim results, suggesting it was worth taking another look, at 218p. Amazingly, it’s soared 70% since then, so well done to anyone who took the plunge.

Have we missed the boat now? I don’t know, it depends if the company can keep this strong surge of performance going, or if it fizzles out again, as has happened previously.

I can’t possibly stay amber after 2 profit upgrades, so it has to be GREEN. Definitely worth doing some more detailed work on the services it offers. I do recall that it has been investing in a new ad platform of some kind for several years, so if that is now paying off, there could be further upside perhaps? Looks interesting, I think it’s worth you taking a closer look. We may be late to the party, but we’ve received a warm welcome, and handed our bottle of Asti Spumante to the hosts!

As always, we very much want to hear reader views on this (and all) shares, as we don’t usually have time to really dig into the detail, competition, etc.

Zoo Digital (LON:ZOO) - 41p (£40m) - Trading Update - Paul - AMBER

ZOO Digital Group plc (AIM: ZOO), a leading provider of end-to-end cloud-based localisation and media services to the global entertainment industry, today provides an update on trading.

Checking our previous notes this dubbing/subtitling company delivered excellent results for FY 3/2023, but then had a series of awful profit warnings, indicating a huge £(13.8)m loss for FY 3/2024. The main issue seems to have been the long-running Hollywood strikes, so we were hoping for a recovery, hence rather too optimistically stayed at AMBER (helped by its healthy cash position thanks to a very luckily-timed equity fundraise just before trading & the share price collapsed).

The latest news is yet another profit warning, but mitigated by reassurance that demand is returning after major disruption from the strikes -

ZOO has now been notified by its largest customer of orders giving a pipeline and confidence of work for the next two quarters which is expected to deliver a strong recovery of revenues, and indicates demand for services and languages that are aligned with ZOO's investment strategy. However, it is now clear that the completion of entertainment products is taking longer than expected. This will result in Q4 revenue being significantly lower than anticipated leading to a greater loss than previously expected for the full year.

The pipeline is consistent with current market expectations for FY25 and a return to profitability.

So this looks like a situation where investors are being asked to write off FY 3/2024 as an annus horribilis, and draw a line under it as things hopefully recover.

Cash doesn’t seem to have run out -

On 31 December 2023, the Group had net cash of $8.9 million and expects to maintain a positive balance with unused debt facilities available at the March year-end and an improving cash balance in the first half of FY25 due to the recommencement of orders.

Paul’s opinion - tricky one. Obviously performance has been dire, but it still has enough cash. Should be hold on at AMBER, expecting a recovery that does at least seem to be credibly in the pipeline? Or should I move down to amber/red, to reflect that I don’t think this is a very good business model at all? It’s also vulnerable to obviously strikes, but also I believe has client concentration risk, and lots of competition. I don’t really believe the bull case. I’ll sleep on it, and decide in the morning!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.