Good morning from Paul!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Paul's 2023 share ideas, with live prices.

New SCVR summary spreadsheet from July 2023 to date, updated at weekends (very useful quick reference tool, search for ticker using CTRL+F). Hover over cell for pop-up notes.

Frozen SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Quiet for news again today, so I'll do a few catch up items -

Other mid-morning movers (with news) -

Fiske (LON:FKE) - up 29% to 60p (£7m) - Interims from this tiny wealth mgt company. £429k PBT in H1, much improved on LY. Strong bal sheet, with £4.1m net cash. Upbeat commentary. Investment in “Euroclear”. This actually looks quite interesting, worth a closer look for microcap investors.

Audioboom (LON:BOOM) - up 8% to 258p (£42m) - Non-regulatory RNS Reach, trumpets growth in audience numbers for its podcasts. 38.6m monthly downloads in Jan 2024, up 9% on Q4 2023 average. See our archive for the negatives too, including expensive mistakes made on legacy contracts, and mgt greed.

Summaries

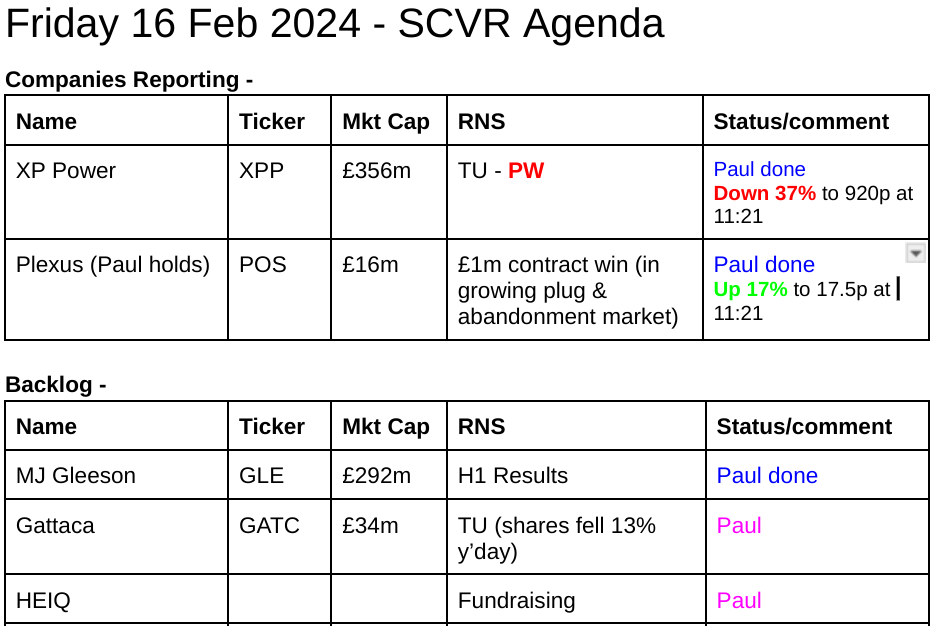

MJ GLEESON (LON:GLE) - down 1% to 496p (£289m) - H1 Results - Paul - AMBER/GREEN

Interim results to Dec 2023 are poor, as expected, but trading is in line with recently lowered expectations FY 6/2024. Not the amazing bargain it was a year ago, but still good value in my opinion. Share price is 100% backed by tangible net assets. As with other housebuilders, the outlook comments suggest the housing market is beginning to recover.

Plexus Holdings (LON:POS) (Paul holds) - 15p (pre-market) £16m - £1m contract win - Paul - GREEN

I'm biased, as this is by far my largest personal portfolio position, but hopefully I'm still being objective, or trying to anyway. A £1m contract win announcement today is significant as it's in the plug & abandonment area, which Plexus has been saying offers plenty of opportunities in the N.Sea especially. Contract wins need to keep flowing, but this is a positive step forward I think. Risk of dilution has greatly reduced, given $5.2m cash received from SLB recently for a perpetual licence for use in non-core areas. Higher risk, so not for widows or orphans.

XP Power (LON:XPP) - down 37% to 950p (at 11:57) - £224m - Trading Update (PW) - Paul - BLACK (profit warning flag) - AMBER/RED on fundamentals

This seems quite a substantial drop in 2024 earnings, but we're not told directly, and no broker notes are available. I've been able to join the dots, and estimate that 2024 EPS could come in as low as 32p, down two thirds on previous forecasts. I don't like the look of this, show am shifting down from amber to AMBER/RED.

Paul’s Section:

MJ GLEESON (LON:GLE)

Down 1% y'day to 496p (£289m) - H1 Results - Paul - AMBER/GREEN

Results for the half year ended 31 December 2023

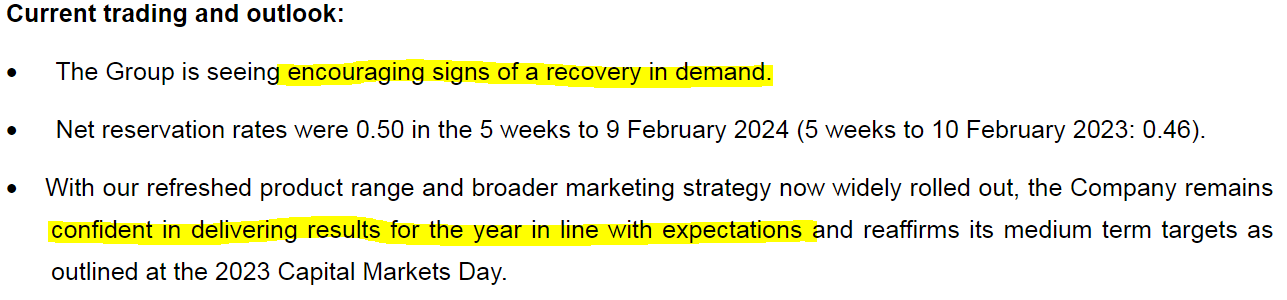

"The results for the half year reflect a robust performance given conditions in the housing market during 2023. Gleeson Homes entered the second half of the year with a strong forward order book and we are seeing encouraging signs of recovery in reservation rates.

We’ve reviewed this affordable housing builder many times in recent years. The big discount to NTAV, and more defensive characteristics of building low cost housing, persuaded me to add Gleesons to my top 20 share ideas for 2023. Despite considerably uncertainty at the time, this idea is now looking good at +44% since the start of 2023, with our entry price being luckily at the 5-year low.

Despite a strong rise in share price, the 5-year chart is making me wonder if this could be the early stages of a new bull run? Particularly as GLE has such a strong balance sheet (like most other housebuilders) that it didn’t need to issue fresh equity either during the pandemic, or in the energy/cost of living/Truss/interest rates crises.

GLE did however blot its copy book recently, with a profit warning which I reviewed here on 9 Jan 2024, Liberum slashed forecast EPS for FY 6/2024 by 22% and by 26% for FY 6/2025, yet amazingly this didn’t seem to trouble the market much, if at all.

GLE did have a big discount to NTAV, but that has now been eradicated by the share price rise, and the StockReport shows shares now trading at about par with NTAV - which is actually still quite attractive, given that it seems likely we’re entering the start of an improvement in housing market transactions again, and household nominal incomes are in some cases 15-20% higher than they were 2 years ago. Which means that more people can afford to, and probably are regaining the confidence to think about buying an affordable new starter home.

H1 results (Dec 2023), key numbers -

Revenue down 11.4% to £151.5m

Profit before tax down 55% to £7.2m

Basic EPS down 56% to 9.6p

H1 divi down 20% to 4.0p

Broker consensus seems to be 33.7p EPS for FY 6/2024, implying a significant H2 bias, given that H1 was only 9.6p EPS.

At 496p/ share, the PER is 14.7x, which isn’t cheap, but we could be looking at earnings being at or near the low point in the cycle, but nobody knows for sure. Hence PERs do tend to look highish at a cyclical low for earnings.

Balance sheet - as is the sector norm at the moment, the balance sheet is ludicrously strong, and hardly has any gearing. Net debt was only £18.7m.

NAV of £287m becomes NTAV of £287m, because there are no intangible assets on the balance sheet. This is almost identical to the £289m market cap, so owning shares in GLE means it’s fully asset-backed. The big asset being inventories of £358m - being houses under construction, plus land, most of which should turn into cash within a reasonable timescale, likely to produce a profit on top of the book cost.

Paul’s opinion - I think GLE still looks very good risk:reward. Buyers in early 2023 have made a very nice profit to date, which they deserve for taking a perceived risk when everyone else was in panic mode, but they were actually buying pound notes for 70p! (the discount to NTAV at the time).

I think the easy money has maybe been made now, but with the housing market cycle now clearly on an improving trend, which we’re hearing from everyone in the sector, I think picking up GLE shares at par with NTAV still looks an attractive option, for more patient investors maybe?

I had a wobble when the profit warning hit on 9/1/2024, dipping to amber to be on the safe side. However, skimming these latest numbers & narrative, it strikes me as reassuring. Also I think the desperate need for affordable housing, and likely stimulus measures from whoever is running the country going forwards, combined with inflation now being down to 4% and lower interest rates seeming quite likely, which is good for housing affordability, I think I’ll move up a notch to AMBER/GREEN. Not as cheap as it was, but this still looks an attractive, and I think pretty safe share to consider for further, deeper research. The sector has had a very nice rebound in the last 3 months, so I don’t know what immediate upside there might be, or whether these shares might need to consolidate for a while? That’s more a consideration for traders, than for my reviews of the fundamentals here.

Plexus Holdings (LON:POS) (Paul holds)

15p (pre-market) £16m - £1m contract win - Paul - GREEN

As mentioned before, this is by far my largest personal portfolio holding, so obviously that makes me heavily biased (but hopefully still objective).

Good news to have a decent-sized £1m+ contract win announced today. Note that revenues in recent years have only been c.£2m pa, so a £1m contract win today is quite material to the historical numbers.

I assume this is another rental + services deal, as it mentions the contract starting for 9 months from Q2 (calendar, I assume) 2024. The company has said before that contracts often expand once they start, as happened with the special contract which was initially announced as £5m, but soon grew to £8m (this was the trigger for me buying into POS shares last summer). So maybe this latest deal might also expand? Who knows, that's just me speculating.

Plexus have been saying for a while that they see big opportunities in plug & abandonment of expired oil/gas wells, a growing area, so I feel that today's news confirms & validates what it's being saying.

I don't fully understand how this contract links to the SLB deal, does anyone know?

"Exact™ Adjustable Wellheads and Centric Mudline Systems are part of the Plexus licence/collaboration agreement with SLB..."

Once again, this news reinforces my view that Plexus is proven tech, and the company is coming alive again, due to demand driven by methane leak becoming a big environmental issue, and also it seems Plexus is making progress in P&A.

All for £16m market cap, and with the cash situation sorted out, with only 5% dilution from the sale of treasury shares.

Management have protected small shareholders from what could easily have been ruinous dilution, using their own money.

There are useful research notes from Cavendish, available on Research Tree, for more information. Due to 2 large one-off deals, it is forecasting revenues to rise almost 10x in FY 6/2024, and after years of losses, a return to profit of £3.5m. That’s obviously why the shares have multibagged in the last year.

Not for widows & orphans that’s for sure, but the company is now in a very much better position today than it was a year ago, with net cash now.

Very volatile share price, indicates that the market doesn't really know how to value this share yet -

Low StockRank, as I would expect from a company that has generated multi-year losses. Although that should change when the (forecast to be £3.5m profit) FY 6/2024 results are published in the autumn.

Zooming out, the company's heyday saw it valued at c.£300m (and with a similar number of shares in issue as today). I can remember writing about Plexus here c.10 years ago, but dropped coverage once industry & political headwinds saw oil & gas exploration in the N.Sea dry up in 2015-16 -

XP Power (LON:XPP)

Down 37% to 950p (at 11:57) - £224m - Trading Update (PW) - Paul - BLACK (profit warning flag) - AMBER/RED on fundamentals

XP Power, one of the world's leading developers and manufacturers of critical power control solutions for the Industrial Technology, Healthcare and Semiconductor Manufacturing Equipment sectors, provides an initial view of the outlook for the year ending 31 December 2024 ("2024" or "the year").

As you can see below on the 12-month chart, unfortunately XPP has today given up almost all the recovery in share price since its last bombshell profit warning just over 3 months ago. That necessitated an emergency equity fundraise with dilution of 20% additional shares being issued at a surprisingly generous price of 1150p - indicating good support from institutions. That was part of a package involving relaxed banking terms. Since then, investors had been giving the shares the benefit of the doubt.

However today’s latest bombshell once again shows that the share price chart is frequently not all-knowing, and we now know had detached from how the company was actually trading, which happens a lot. Otherwise we wouldn’t get vertical moves up or down in share prices.

Here’s today’s profit warning, for FY 12/2024 -

The Board has concluded that there is likely to be a shortfall in revenue in 2024, leaving the outlook for 2024 significantly below market expectations. This is based on recent order intake, revenue performance and discussions with customers, particularly within the Healthcare and Industrial Technology sectors, which confirm unusual, temporarily soft demand conditions and destocking. These softer trends have also emerged within our direct industry peers.

De-stocking again, that’s a theme we’re hearing from quite a lot of companies at the moment.

Cost-cutting - it says today that more savings have been identified.

Audit adjustments (costs) of £4m have been discovered which reduce 2023 profit.

Outlook -

In general, we expect the weakness we are currently seeing to be relatively short lived and indeed there have been some more encouraging signals from certain customers, especially for 2025, in recent weeks. The timing and speed of the recovery is hard to predict however. We expect 2024 to be significantly second half weighted with an improvement in trading as the year progresses.

Broker updates - infuriatingly, we don’t have access to any broker updates, so is often the case with some companies, private investors are left in the dark, whilst professionals and institutions can deal with better information than we have.

“Significantly below” market expectations covers a wide range of possibilities, so I have no way to quantify the impact of this latest profit warning.

We’ll just have to wait until broker consensus figures update next week, or if any readers have seen any broker updates today, perhaps you could kindly post a reader comment with the revised FY 12/2024 EPS forecasts?

Edison’s forecast (from 11/1/2024) was 2023 EPS of 111p (down 31% on 2022), and a further drop to 94p in 2024. We’re now told it will be “significantly below” that 94p level, so what’s everyone’s guess? 50p maybe? Worse?? Who knows, we haven’t been given enough information.

Therefore at present this share is impossible to value.

The market price crashing about 36% (at 12:51) and having made little attempt at rallying today, suggests to me that we’re probably looking at deep cuts to 2024 forecasts.

Liquidity - this section might allow me to work out the impact on profit -

The Group's cash generation toward the end of 2023 was ahead of expectations, as reflected in the year-end net debt position of £112.7m, and we expect this to continue in 2024 with net debt below our prior assumption.

A trading performance in line with the Board's expectations would leave net debt/EBITDA at 31 December 2024 at or below 2.5x versus a covenant limit of 3.5x. The Group maintains significant levels of liquidity.

If I assume that net debt might reduce to say £100m by end 2024, then this implies EBITDA of about £40m in 2024. The last Edison note forecasted £59.7m for FY 12/2024. This turned into £28.2m normalised PBT.

If I assume that the £30.5m difference between EBITDA and PBT remains the same, then this suggests adj PBT for 2024 would now be c.£10m. Take off 25% tax, that’s £7.5m PAT, which divided by 23.7m, turns into my estimate of only 32p EPS for 2024 - two thirds down on the existing forecast.

Paul’s opinion - XPP had a good long-term track record, so it’s perplexing to see it delivering now multiple profit warnings, and seemingly only limited visibility.

I need to see the full accounts, and updated broker forecasts, before being able to accurately assess this.

Looking back at the last fundraise, it was still expected to have quite heavy net debt afterwards. So with a further drop in profitability, gearing might rear its ugly head again as a problem, although the company says today it expects to stay within bank covenants . If another equity raise is expected, I’d be surprised if institutions were as generous on price as last time.

For this reason, two profit warnings, and potential problems with debt resurfacing, plus what looks like a deep reduction in 2024 forecasts, I’m going to shift us down from amber to AMBER/RED. But I’ll happily revise that once we have more information.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.