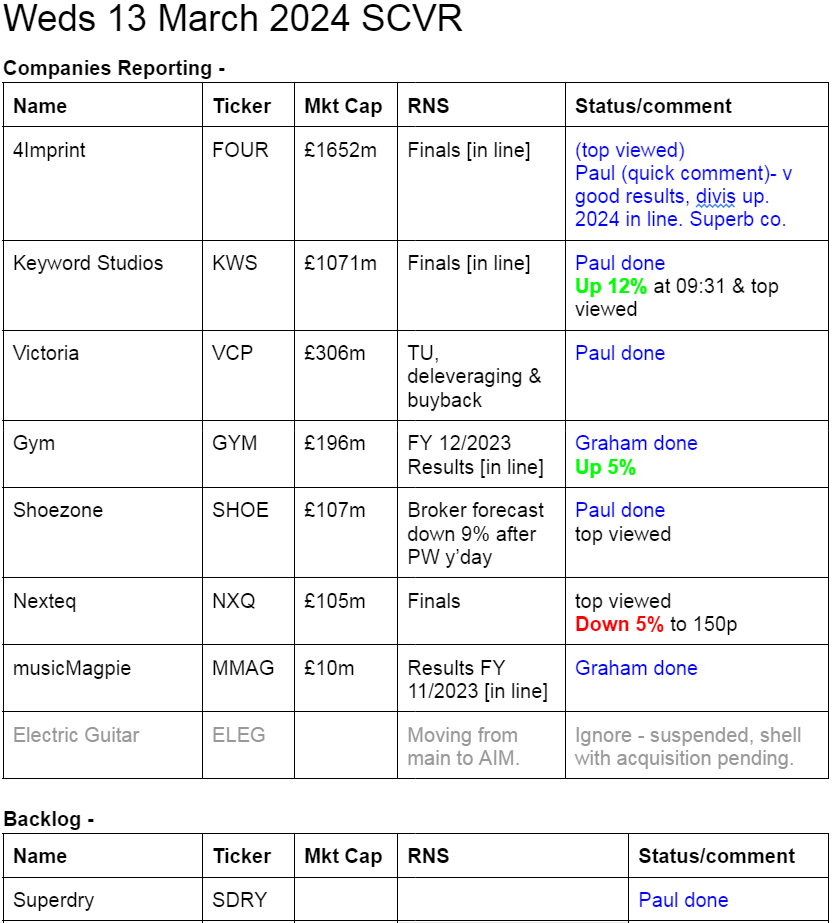

Good morning from Paul & Graham!

Masterclass reminder!

The latest in this series is today at noon - I wrongly assumed it would be this evening, so apologies for not flagging this earlier. The topic is investing strategies. These series of masterclasses are terrific, and I know that a lot of work goes on behind the scenes to prepare them, so I shall be trying to multi-task from 12:00, writing more sections here whilst listening in to the masterclass!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Paul's 2023 share ideas, with live prices.

New SCVR summary spreadsheet from July 2023 to date, updated at weekends (very useful quick reference tool, search for ticker using CTRL+F). Hover over cell for pop-up notes.

Frozen SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Other morning movers (with news) -

Balfour Beatty (LON:BBY) - up 9% to 370p (£1.98bn) - positive market reaction to increased share buyback (£50m existing, upped to £100m) and to FY 12/2023 Results with underlying EPS down 21% to 37.3p, in line with expectations. Massive £16.5bn order book. Large complex business, low margins, negligible NTAV. Outlook sounds good, with growth expected in 2024 & 2025. Paul’s view - none, it’s not one I’ve looked at in detail. Shares have gone in a sideways range for 15 years, so it’s navigated lots of potholes better than most industry peers. Could infrastructure/contracting shares be coming back into fashion now maybe? The devil’s in the detail of all their contracts, info that we probably won’t know about. But I can see that the lowish PER, and encouraging outlook, make this something that sector experts might want to look into further.

CAP XX (LON:CPX) - down 81% to 0.076p (£negligible) - Corporate update - we haven’t covered this since 2017 (apart from here on 1/2/2024 when I flagged it was almost bust), as it looked so bad - serial loss-maker, cash burner, and equity issuer - typical of many AIM shares unfortunately! - which is why we usually ignore this type of thing, but they’re coming up constantly on my new morning movers section - have I created a monster?!

Anyway today’s update is saying things have only got worse, and cash now “highly constrained”, and it needs fresh funding by the end of this month. No debt options available, and efforts to raise equity taking longer than expected. Paul’s view - existing equity looks worthless, as mentioned last time. Time to call it a day as a listed company. RED obviously.

IXICO (LON:IXI) - down 22% to 6.8p (£3m) - Profit-warning, with FY 9/2024 now expected to show another decline in revenues. I’ve done a 10-minute review, and it’s not a complete basket-case (yet). It did make small profits in the past, but more recently reported a loss for FY 9/2023, and revenues have since continued falling. It had £2.8m cash remaining at 29/2024, down from £4.0m at 30/9/2023. It says sales pipeline is growing though. Providing management can conserve the cash, and not come back to an unreceptive market for more equity, then this could be a survival/turnaround story, possibly. Delisting risk is considerable though. So one for gamblers only, but as a fun money punt, I can see some attraction, if they don’t run out of cash.

Victoria (LON:VCP) - down 6% to 229p (£265m) - Trading Update, De-Leveraging & Buyback (profit warning possibly? Unclear) - Paul - AMBER/RED

Trading - near-term conditions remain tough, but forward indicators improving. Market demand down 20%, interesting as this is what Headlam (LON:HEAD) also said recently. FY 3/2024 - underlying EBITDA now expected to be c.£160m, but nothing said about what it was previously expected to be - infuriating, and no broker updates available to us proles! Mentions “pressure on earnings” from higher labour costs, and restructuring, so I assume this must be a profit warning, but we need more information to be sure. “substantial permanent” reductions in overheads, and improved efficiency (not quantified).

Says margins will be 250-350 bps higher, when demand returns.

Asset sales - non-core & surplus land has been sold for E31m already, with E50m more expected. Quite hefty numbers.

Working capital - says it can squeeze £30m out of inventories in FY 3/2025.

Share buyback - a strange thing for a very heavily over-indebted company to decide, but it says there is an “intention” for a “potential” £25m share buyback.

Bond repurchases - has bought back E11.1m of its own 2026 Bonds, at a 21% discount vs par value. Target is E25m total but there isn’t enough market liquidity to do this, they say. The coupon on these bonds is only 3.625%, but buying back at well below par produces a good overall return to maturity.

Paul’s view - the problem here is not market “noise” as the Chairman seems to think, it’s that mgt at VIC have greatly over-geared the balance sheet, with last reported NTAV of £(371)m. So I didn’t respond well to their rather dismissive commentary today - the share price has crashed precisely because of their high gearing strategy, combined with poor market demand. Mind you, borrowing through fixed interest bonds rather than a regular bank, is looking an inspired decision now that interest rates are higher. Overall, I could see this share multibagging in a flooring market recovery, aided paradoxically by its precarious balance sheet - we’ve seen this play out before, if you look at the long-term chart. So it could be an interesting share for risk-takers who can live with its hideous balance sheet & high debt. I’ve got to flag the higher risk, so will go with AMBER/RED. It’s likely to move big in one direction, I just don’t know if that will be up or down! Not much use to you then really!

Summaries of main sections

Superdry (LON:SDRY) - down 13% to 27p (£27m) - Response to media speculation - Paul - RED

Super-high risk now, given increasingly alarming press reports over various advisers being called in, and a (company confirmed) need for a further £20m of borrowings from lender of last resort Hilco.

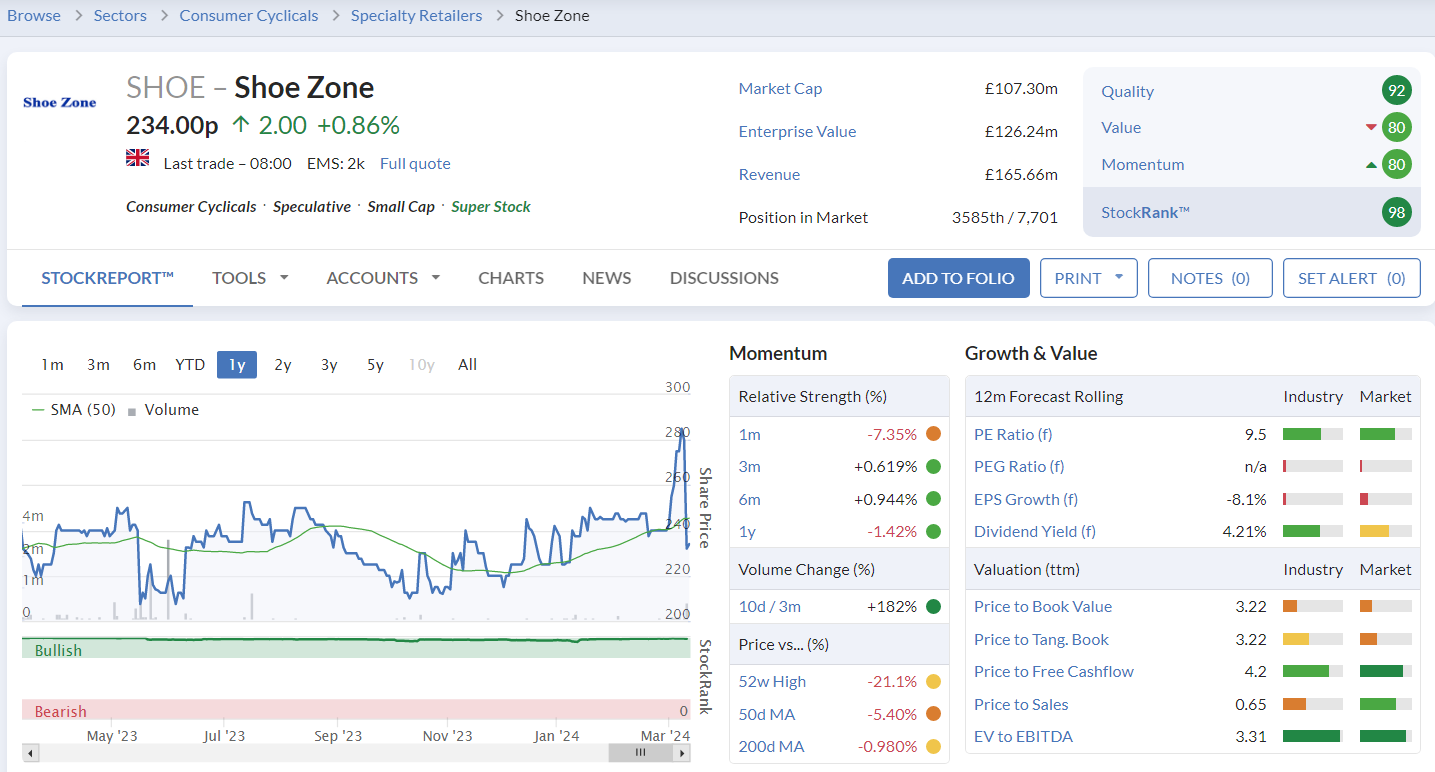

Shoe Zone (LON:SHOE) - 232p (pre-market) £107m - Zeus update note - Paul - GREEN

Zeus drops forecasts EPS by 9%, which is more than I was expecting from the mild profit warning issued yesterday. It still looks a good quality (high scores) business, and good value too. Although [trigger warning!] Chinese direct to consumer Shein/Temu (and other?) aggressive competition worries me.

Musicmagpie (LON:MMAG) - down 1% to 8.9p (£10m) - Full Year Results - Graham - RED

Not much cheer for MMAG shareholders this morning as revenues fall, net debt grows, and the pre-tax loss expands. Recent trading is in line with expectations but I don’t see how investors can have faith in this company becoming sustainably profitable.

GYM (LON:GYM) - up 5% to 115.6p (£207m) - Full Year Results - Graham - RED

2023 results from this low-cost gym operator are in line with guidance and the company reports a good start to trading in 2024. It remains ambitious for growth despite already having over 200 sites and carrying substantial debts. Too risky for me.

Keywords Studios (LON:KWS) - Up 12% to 1544p (£1.21bn) - FY 12/2023 Results. - Paul - AMBER/GREEN

Overall I'm pleasantly surprised with these 2023 results, which look pretty good, if you're happy to accept the large adjustments. A major acquisition spree leaves it with net debt (although not excessive, providing it remains decently profitable). Worth a closer look I think.

Paul’s Section:

Superdry (LON:SDRY)

Down 13% to 27p (£27m) - Response to media speculation - Paul - RED

It’s strange how news from Superdry typically first comes out via Sky News, and then the company responds. The latest news is that SDRY confirmed on Mon evening that it was seeking an additional £20m lending facilities (£10m for restructuring, and £10m for seasonal peak trading in the autumn). “No certainty that such changes will be agreed”.

Paul’s view - SDRY is looking increasingly financially distressed, and doing all the things I would expect from a company that’s at considerable risk of going bust. There have also been press reports that it was considering its debt options (of which there are very few, in my view), and has called in various advisers, again often a precursor to some form of insolvency in my experience. Maybe it can pull another rabbit out of the hat in IP sales, but I think that would only be postponing the inevitable.

We've been warning here for a long time that SDRY is looking increasingly risky, and I confirm that I’m treating this share as super-high risk now, with the most likely outcome being a 0p outcome for shareholders. Although who knows what might happen? Remember that the brand will survive, but maybe with a different owner. Be very careful, this one is only for gamblers now, hoping for a miracle. Remember also that Hilco are experts at dealing with insolvencies, and as the main (secured) creditor, they will legally rank higher up than trade creditors, let alone shareholders who are at the bottom of the heap and usually end up with nothing in financially distressed situations.

Why would anyone bid for the existing equity, and take on all those onerous leases for the many loss-making shops? Doing a pre-pack administration is the obvious route to take, which of course would almost certainly wipe out existing equity. Similar to what happened at Joules (where I lost a packet, so am not making the same mistake twice).

An outdated, failing brand? Down over 98% from the Jan 2018 peak, with the bulk of the collapse in share price happening before the pandemic began in early 2000. It's a reminder that mid-market brands come and go - what's fashionable for one generation may become cringe-worthy for the next -

Shoe Zone (LON:SHOE)

232p (pre-market) £107m - Zeus update note - Paul - GREEN

Yesterday we had a mild profit warning from SHOE which I covered here, blamed on NLW, Suez, property costs, and slower A/W trading. SHOE told us trading was “marginally below expectations”. Shares sold off sharply, giving back all of a recent surge seemingly triggered by a couple of media buy tips.

This morning broker Zeus updates us (many thanks), and it seems worse than the announcement yesterday seemed to suggest. Zeus has lopped £1.4m off its adj PBT forecast for FY 9/2024, reducing from £15.2m to £13.8m. Forecast adj EPS comes down from 24.7p to 22.4p - a c.9% reduction, which doesn’t fit the description from SHOE of “marginally below expectations”. Zeus says it’s being prudent, but even so, this has not been handled very well by the company. It should have said “below”, not “marginally below” in yesterday's RNS. I’ll make a mental note of that for future reference when interpreting announcements from SHOE - that they might be reluctant to accurately divulge bad news.

In the short term then, I feel SHOE has blotted its copybook somewhat. However, once the dust has settled, people may take into account that it’s only giving back a bit of a previously very positive forecast earnings trend (not yet updated for today's forecast revision to 22.4p) -

The numbers are still very good, and the valuation modest still, especially after this recent pullback, so I’m sticking at GREEN.

I do still have background worry about potential erosion of sales from the aggressive direct-to-consumer Chinese companies, eg Shein and Temu. This seems to trigger some readers, who think it’s a preposterous idea. However it’s real - I’ve bought shoes from Temu, they squash them down in a bag, with no box, and they don’t seem to worry about making profits - they’re more interested in killing the competition, and apparently have no qualms about working conditions at the factories to achieve lowest cost price. That’s a big worry, when SHOE is also sourcing its products from China and making a fat gross margin on them - an open goal for Shein/Temu I would say, and they only need to erode a small % of SHOE’s sales, to dent its profits badly, due to the operational gearing. Returns rates are low on shoes, as you just buy the size that you are, and it usually fits. That said, most customers will probably still want physical shoe shops to try on the fit.

Anyway, for now I remain positive on SHOE, but am starting to have some doubts, given that it seems to have lost short term trading momentum.

There’s lots of green on the StockReport, and a terrific StockRank of 98, so maybe I’m needlessly worrying? I’d be interested to hear all opinions from readers, whether you’re bull, bear, or somewhere in between. As always, don't let bulls shout you down, we want to hear a range of well-argued opinions.

Lots of green here (the longer bars, or higher numbers, for the colour-challenged) -

Keywords Studios (LON:KWS)

Up 12% to 1544p (£1.21bn) - FY 12/2023 Results. - Paul - AMBER/GREEN

We’ve covered this share very little here in the SCVRs as its market cap was too big, but after recent falls, and us spreading upwards into mid-caps, here it is! Graham did review KWS here in Dec 2023, taking an amber view, and saying it had grown into a more reasonable valuation.

Quite good results today I think, given the carnage elsewhere in video games sector. KWS seems to provide services to bigger computer games companies, including 24 of 25 of the largest it says - impressive.

Reporting in Euros, main numbers are -

Revenue up 13% (5.6% organic) to E780m

Adj EPS flat at 112.9c (Euros)

Statutory EPS much lower at 25.3c, so very large adjs

Adj operating profit up 7% to E122m.

Statutory PBT is down 49% to E35m, so you have to be comfortable with the large adjustments here -

Moved from net cash of E81.8m to net debt of E67.5m due to heavy spending on 5 acquisitions.

Total divis of 2.61p (up 10%), but insignificant yield of c.0.17%

Outlook - I’m impressed with all this -

Share-based expense - is way too high, excessive even, at E22m in 2023, and E18.7m in 2022. How can that be justified? But I suppose the market cap is £1.2bn, even so mgt nabbing 1-2% of the company for themselves each year, on top of other forms of remuneration, puts me off somewhat.

Finance costs have shot up, and finance income dropped by two thirds, as it moves from net cash to net debt.

Balance sheet - has been strikingly geared up, to pay for the acquisitions. NAV of E599m contains E632m intangible assets, so NTAV is now negative at E(33)m, which might put off some value investors.

Paul’s opinion - KWS does look interesting, if you’re OK with all the accounting adjustments, and the rapid & expensive acquisitions spree. Given all the turmoil in this sector, and Hollywood strikes, these results do strike me as “resilient”.

Outlook comments sounds upbeat too, helped by the 2023 acquisitions contributing a full year in 2024.

I’ve only done a quick review, and it’s not a company I’m familiar with, so take my view with a pinch of salt. Based on what I’ve seen, I quite like this, and will go with AMBER/GREEN, it’s something that seems worth a closer look by readers maybe. Pity there are no broker updates out since last summer available to plebs like us!

I’m drawn to this chart too, as possibly a good entry point, combined with today’s resilient results, who knows? -

Graham’s Section:

Musicmagpie (LON:MMAG)

Share price: 8.9p (-1%)

Market cap: £10m

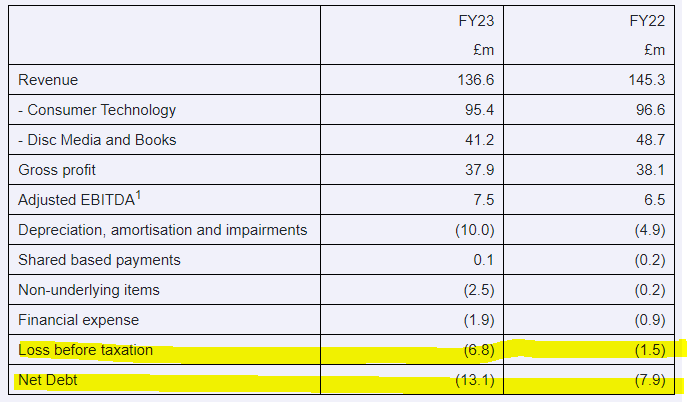

musicMagpie, a circular economy pioneer specialising in refurbished consumer technology, disc media and books in both the UK and US, announces its audited full year results for the year ended 30 November 2023 ("FY23").

The company has put a brave face on when it comes to presenting these results, and in some ways they aren’t too bad. But then you get down to the bottom two lines of the highlights table:

The company has two major categories: Consumer Technology, and Disc Media and Books.

Disc Media and Books - the sale of new and second hand games and DVDs in disc format - is an activity that is inevitably going to continue to decline in my view, as there is simply no reason for games and movies to be stored on a disc instead of downloaded.

My opinion on this has evolved; a few years ago, I still liked having the physical disc of a game and thought there was value in owning that disc (e.g. being able to share the disc with your friends after you’re finished with it). But I don’t believe these arguments are very strong these days.

These days, if you install a game from a disc onto your games console, you will most likely be prompted to download the latest updates to the game. These updates can be very large. So why not simply download the entire game?

I agree with this article which says that the real point of game discs these days is as a proof of purchase that enables the user to download the game, not as a format that actually stores the game. This makes it a legacy format that in many ways doesn’t need to exist any more.

Music Magpie’s Disc Media and Books division saw revenues fall from £48.7m to £41.2m:

…declining as expected, mainly owing to the continued reduction in the sale of both new and second-hand physical media as consumers increasingly consume content in different ways, for example online streaming.

We are starting to see a deceleration in this sales decline as the more rapidly declining DVD and gaming segments become much less significant and books, which are more resilient therefore generate an increasing share of overall sales.

The trend suggests that this will eventually become a Books division, as Disc Media will not be a thing.

The larger Technology division also saw declining revenues, from £96.6m in 2022 to £95.4m in 2023:

Within this segment, the Rental business grew from £5.3m to £8.25m as active renters increased from 30,500 to 37,100…

The second component of Consumer Technology, outright sales, saw revenue decline by £4.0m to £87.2m (2022: £91.2m), but gross profit was static at £16.0m. The Group has focused on expanding its margin on outright sales via a number of initiatives as well as managing the sale of stock across the various sales platforms in a more sophisticated manner in order to achieve minimum expected gross margin targets.

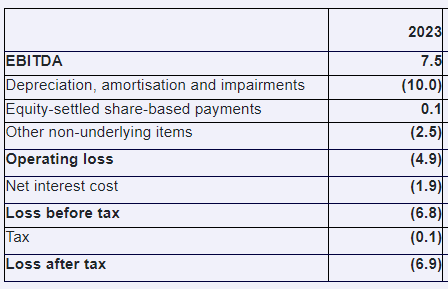

Profitability

Let’s see how large EBITDA becomes a large loss:

Is there anything here that doesn’t represent a real cost? Not much, I’m afraid. The depreciation charge (on devices out on rent) seems fair to me, as does the amortisation charge.

Within “other non-underlying items” (£2.5m), you could maybe argue that the impairment of goodwill (£1.1m) is not a real cost. There is also a loss relating to electricity prices - the company hedged its electricity costs at prices above current market rates - and investors might choose to ignore this.

Therefore, in my view, only the “other non-underlying items” can potentially be adjusted out and ignored by investors.

Balance sheet has notional net assets of £12m but if you exclude intangibles this falls to zero.

Bank loans: the company has a £30m RCF with HSBC and Natwest. £20.5m was outstanding at the end of 2023, vs. £14.7m at the end of 2022. Rates charged are reasonable but the banks have security over nearly all of the company’s assets.

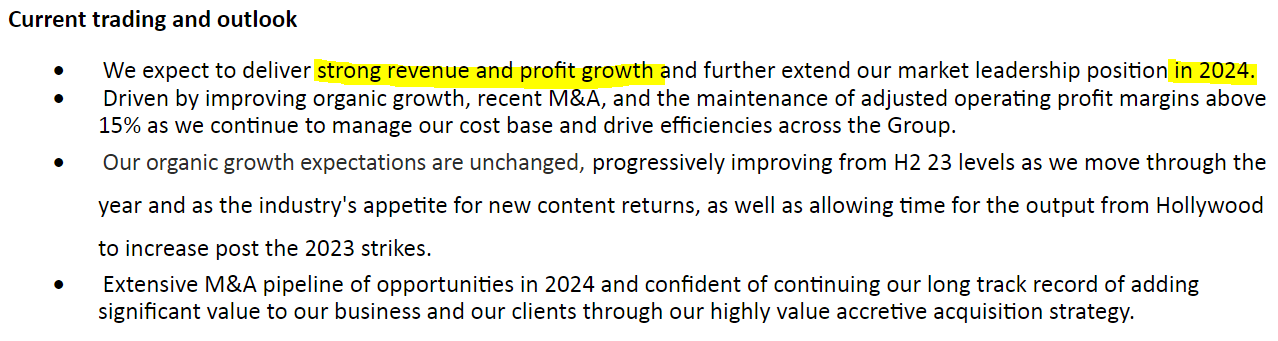

Q1 Trading and Outlook

Q1 FY24 has recently closed and trading was in line with management's expectations. This positive start to the new financial year, combined with the recent changes made in the US to the Group's Consumer Technology buying strategy and operations, cost reduction exercises in the UK and lower investment levels into our Rental offering, give the Board confidence in the Group's FY24 and medium-term prospects.

CEO comment excerpt:

We expect second-use markets to continue to grow which will complement our strategy of unlocking a 'world of inventory' from consumers homes and providing them with a solution that is 'smart for you, smart for the planet' across of our existing product categories and potential new product categories. As such we remain confident in musicMagpie's future prospects.

Graham’s view

Unfortunately I don’t see an easy route to profitability for this one. And given that it’s in a net debt position, without any proper asset backing, I’m not sure if the equity is ultimately going to be worth anything at all.

In that sense I’m relieved to see that the market cap is only £10m; if it was something more substantial I’d be extremely worried for shareholders! At £10m, it might still be worthless but there is at least the chance of a reasonable outcome for shareholders if performance miraculously improves.

The StockReport warns us that this stock is involved in a “takeover situation”; the reason is that on 27th November 2023, Music Magpie said that it “continues to seek potential buyers” for it, after two potential buyers ruled themselves out.

Stranger things have happened, but I would be shocked to see a buyer paying a big premium here. Why bother taking that risk, when it might be possible to do a deal with the bank at some stage?

These shares are already priced as options and do have multi-bagging potential if the company pulls a rabbit out of the habit. On the basis of the poor figures, however, I’m giving this one the thumbs down.

GYM (LON:GYM)

Share price: 115.6p (+5%)

Market cap: £207m

Let’s take a look at this low-cost gym operator’s full year results for 2023.

From a technical point of view, perhaps the shares have found a base?

Here are the highlights:

Revenue +18%; like-for-like revenue +8%

“Group Adjusted EBITDA Less Normalised Rent” is up 1% to £38.5m but this strikes me as a totally meaningless number.

Adjusted pre-tax loss £5.5m, same as the previous year.

Statutory pre-tax loss £8.4m, an improvement from a £19.4m loss in the previous year.

Net debt (excluding leases) improves from £76m to £66m.

Management - during 2023 the company recruited a new CEO and will have a new CCO this month.

Current trading and outlook sounds quite good:

Good start to trading in 2024; revenue after two months has grown by 16% year on year, reflecting a 3% increase in average members and 13% growth in yield, benefitting from price taken earlier in the year. Like-for-like revenue up 12%

Like-for-like revenue in 2024 to increase by 4-5% overall as the impact of the early price increases normalises later in the year

Plan to open 10-12 new sites in FY24; leverage expected to remain within the range of 1.5 to 2.0x. Next Chapter growth plan aims to deliver c.50 site openings with average ROIC of 30% over three years, funded from free cashflow.

The forecast of 4-5% like-for-like revenue growth for 2024 implies that there will be some real revenue growth, assuming that inflation falls from the current 4%.

However, the leverage multiple of up to 2.0x still makes me feel uneasy. GYM has struggled to show a profit ever since Covid, and pre-Covid profits weren’t particularly high to begin with.

They already have over 200 sites, which presumably includes all of the areas they might have considered low hanging fruit. Increased rates of working from home in recent years may have changed their calculations to some extent, but the question remains: what is going to change to make this company profitable?

Cash flow: the company presents “free cash flow” (excluding expansionary capex) of £27m. Therefore the bullish argument for this stock is that if you ignore expansionary capex, then you can get a cash flow number like this which is actually quite good. So I’ve answered my own question: the argument for this stock is that its financial performance could improve when it stops expanding.

However, it’s unlikely to stop expanding in the short-term. The CEO comment argues that the market can sustain the creation of more low cost gyms:

We have maintained positive momentum in revenue through the second half to deliver results that have offset cost inflation, in line with our guidance. With a strong start to 2024, and clear signs that demand for health and fitness has never been stronger, these are solid foundations on which to build our Next Chapter growth plan… There continues to be substantial headroom for low cost gyms in the UK and we are fully focused on our aim of making high value, low cost fitness even more accessible for all."

Graham’s view

There is a bullish argument to be made for GYM, but I’m afraid I’m not sold on it yet.

On the positive side, it has managed to push through price rises that have enabled revenues to keep pace with inflation and it plans to do so again this year.

Its cash flow performance is also not bad, if you exclude expansionary capex.

On the negative side, it is carrying significant financial debt, on top of enormous property leases. And its statutory numbers are poor, to say the least.

I’m therefore inclined to keep my negative stance on this stock for the time being. Maybe it can surprise me and prove me wrong, but I see substantial risk here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.