Good morning! We have a busier set of updates than usual this Friday.

1pm: all done! Have a great weekend everyone.

Spreadsheet accompanying this report (updated to 10/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Petershill Partners (LON:PHLL) (£2.9bn) | Q4 AUM Update | AuM raised in 2024: $32bn, ahead of guidance of $20-25bn. 2025 outlook: AuM raise of $20-25bn. | |

Big Yellow (LON:BYG) (£1.7bn) | TU | LfL store revenue +2% for Q3, +3% year-to-date. Confident in further modest EPS growth. | |

Spirent Communications (LON:SPT) (£1bn) | TU | Ongoing challenging market conditions. Full year adj. op profit to be similar to 2024. | PINK (Takeover planned at 201.5p.) |

Ninety One (LON:N91) (£910m) | Q3 AUM Update | AUM £130.2bn (Sep 2024: £127.4bn). | |

Johnson Service (LON:JSG) (£540m) | TU | Organic rev +3.8%. Op profit in line with expectations. 2025: well placed to mitigate higher costs. | |

DFS Furniture (LON:DFS) (£314m) | TU | Order intake up 10% in H1. Results for FY25 now expected to be first half weighted. | |

Evoke (LON:EVOK) (£309m) | TU | H2 sales growth (+8%) and adj EBITDA at the top end of communicated guidance. Ahead of market expectations. | AMBER/RED (Graham holds)

High-risk situation, high-reward if they successfully deleverage. |

M&C Saatchi (LON:SAA) (£218m) | 2024 Full Year TU | Revenue growth of 3.5%. PBT in line with expectations. | |

McBride (LON:MCB) (£176m) | TU | Trading in line. Annual dividends re-instated. | AMBER/GREEN (Graham)

Trading at a PER of 5x, seems reasonable to target something moderately higher than this. |

IG Design (LON:IGR) (£140m) | TU | Profit warning. Adj PBT now only expected at breakeven (from current expectations of $32m). | BLACK/AMBER (Graham)

Net cash and high NAV so I prefer not to take a RED stance. |

Character (LON:CCT) (£48m) | TU | FY25 in line with exp, despite difficult trading conditions. | GREEN (Graham)

Not trading at bargain levels and conditions remain challenging but I like the company's track record and financial strength. |

Everyman Media (LON:EMAN) (£46m) | TU | Profit warning. Box office performance in Q4 not as strong as anticipated. BoD now more cautious around 2025/26. | BLACK/RED (Graham)

Losses are pencilled in for at least the next few years and I don't have faith that meaningful profits will follow after that. |

Oxford Biodynamics (LON:OBD) (£2m) | Result of fundraising | Only £350k of the proposed £500k raised. |

Graham's Section

IG Design (LON:IGR) - down 61% to 56p (£55m/$67m) - Trading Update - Graham - AMBER

Commiserations to anyone holding this overnight, as it is down by over 50% today.

For a company that makes greeting cards, wrapping paper, and Christmas crackers, it can’t afford to have a bad Christmas. But apparently it did:

Challenging market conditions and retail trends experienced in H1 across a number of our markets have continued into H2, and they have more than offset the benefits resulting from [cost-saving] initiatives

Trading across both divisions since H1 has been impacted negatively over the important Christmas season, with DG Americas particularly affected, due to challenging retail conditions affecting customers

It sounds like a major loss of confidence at IGR’s customers, who themselves are struggling under the forces of competition. Key points:

The 4th largest customer of IGR’s American division has filed for Chapter 11 bankruptcy. “A number” of IGR’s American customers are in financial distress. IGR has made provisions of c. $15m to allow for its exposure to them (accounts receivable/inventory).

The sales performance of IGR’s products over Christmas has led to “a number” of IGR’s customers reducing or delaying forward orders.

Outlook

Revenue for FY March 2025 to be 10% below last year.

FY 2025 adj. PBT to be around breakeven, vs. expectations of $32m.

The plan to restore margins to pre-Covid levels is obviously not going to happen now. “Our aspirations will have to be re-planned and re-set”.

Most worryingly, there is no guidance for the years beyond FY25.

FY25 to include impairments at its American division. A new CEO has joined this division.

Comment by the Chair:

These developments and their impact on the Group are clearly very disappointing, and we will continue to strengthen our business model to better withstand the emerging market reality. Notwithstanding external factors, fundamentally, our business is robust and we remain focused on our strong customer relationships, and with the continued commitment of our strengthening team, we will re-map our path to stronger and more consistent delivery.

Graham’s view

The only bright spot is that IGR says it will still have “a strong net cash position” at its financial year-end, albeit below expectations.

However, they do not say what that cash position might be. Checking a broker note from Canaccord this morning, I see that they have not published any numbers for FY25, let alone FY26 and beyond. According to a note published in November, the net cash forecast for March 2025 was $105m. I think this is a post-Christmas seasonal high, but it’s still an interesting figure for a company with a market cap equivalent to just $67m.

We must write that cash balance lower by $15m for the provisions relating to distressed customers, and then write it lower again for the profits ($32m) that have failed to materialise. But perhaps IGR might still have net cash of $50m+ at year-end?

More fundamentally, what are we to make of this profit warning? This is a stock where, a year or two ago, I thought the turnaround plan made for an interesting investment opportunity, as it strove to restore margins to pre-Covid levels.

Today’s profit warning kills off the idea that we might see pro-Covid profitability again any time soon.

With impairments looming, it also provides final proof that IGR’s £90m acquisition in the United States was value-destroying. IGR raised money then at 694p per share - more than ten times the current share price - to finance that acquisition.

When I read about the US consumer over Christmas, I don’t find much evidence of doom and gloom. December retail sales were officially up 0.4% (give or take 0.5%), according to figures released yesterday. Unemployment is only 4.1%. The economy is growing. According to the National Retail Federation (AP), holiday sales over November and December were up 4%.

All of which is to say that IGR can’t point to the US economy or the US consumer as the reason for its woes. Instead, I suspect that the root cause is simply the fierceness of competition in a product category (wrapping paper, greeting cards, etc.) that is highly commoditised. IGR references “the very competitive US retail market” in today’s update.

With no forward guidance available, and since I think the root cause of IGR’s problems is that it’s struggling to compete, there is no chance that I can maintain the AMBER/GREEN stance that we've had on this one recently.

However, I also don’t want to be overly negative on it, because it may be trading at only a small premium to net cash and should achieve a result of around breakeven this year (before impairments), not a loss.

Therefore, it’s a decision between AMBER and AMBER/RED.

Checking the most recent balance sheet (Sep 2024), I see that it had tangible net assets of over $300m. The biggest items - inventory and receivables - will have to be written down to some extent. But still, that’s a lot of NAV for a company with a market cap of less than $70m.

I think the correct assumption must be that IGR will not be able to restore decent profit margins for the foreseeable future. However, I also think it’s possible that the stock offers some deep value at these levels, given the balance sheet value and net cash.

I’m therefore going to put this at AMBER for now, rather than anything lower. Existing holders have had a torrid time, but we must remain forward-looking and I’m not yet convinced that this is heading to zero.

Evoke (LON:EVOK)

Up 9% to 75.75p (£266m) - 2024 Post-close Trading Update - Graham holds - AMBER/RED

At the time of publication, Graham has a long position in EVOK.

This is “one of the world's leading betting and gaming companies with internationally renowned brands including William Hill, 888 and Mr Green.” I’m a reluctant shareholder since the pre-William Hill days, when it had a cash-rich balance sheet and the 888 ticker!

These days, EVOK struggles under the weight of an enormous debt load.

Key points from today’s update:

Q4 revenue up 13 - 14% at constant currencies (up 12 - 13% at actual exchange rates).

Online growth 18 - 19%

There were “operator friendly sports results” in Q4. This contrasts with Entain (LON:ENT) which suffered “customer-friendly” results in the US.

H2 revenue growth therefore c. 8% (previous guidance: 5 - 9%).

And there is great news on the profit front:

Strong cost control and an increasingly efficient operating model mean that adjusted EBITDA is expected to be at the high end of the previously communicated guidance range of £300-310m for the full year, and well ahead of market expectations.

Adj. EBITDA of £310m is of course a remarkable figure against a market cap of just £266m, but we need to consider the debt position.

The consensus EBITDA forecast was £294m, so we have a beat of 5% against that.

Continuing with the CEO comment:

While we were helped by some operator-friendly sports results in Q4, the significantly improved underlying momentum in the business gives me real confidence that the turnaround is working and we are well positioned to continue our growth trend into 2025.

2024 was a pivotal year as we started to implement our new strategy for success, radically transforming almost every area of the business, and moved decisively and at pace to position evoke for mid- and long-term profitable growth. We go into 2025 with improving momentum…

Graham’s view

I’ve tried to be objective about this, giving it an AMBER/RED in July after a poor H1 trading update (share price at the time: 79p).

The UK Retail division, i.e. William Hill stores, are a problem area and I remain concerned that they will drag the entire business down.

Net debt as of June 2024 was £1.7 billion. Shareholders such as myself will not be able to relax until this starts to meaningfully reduce, and this hasn’t happened yet.

Thankfully most debt does not mature until 2027, when €478m of senior secured notes expire.

Management’s plan is to grow their way out of the problem and to achieve a net debt/EBITDA multiple of less than 3.5x by the end of 2026. I guess if that is achieved, then refinancing should be possible at reasonable terms.

For now, the debt load creates a heavy interest burden which in turn impinges on the company’s ability to pay down debt. Credit rating agency Fitch has a negative outlook on their rating for EVOK, which currently stands at B+.

With net debt last seen at £1.7 billion and trailing EBITDA of £310m, we have a leverage multiple of about 5.5x. To get this multiple down to 3.5x by the end of 2026, they would need to (for example) pay off £100m of debt each year for two years, and grow EBITDA by 33% over that timeframe.

If they did, then we’d have £1.5bn of net debt and EBITDA of £400m+, and then the leverage multiple would be close to 3.5x.

Is that possible? I’ve been saying this for a while, but I still think so. I still think there’s a chance that the company can get through this narrow financial gap. These are difficult targets but they are not impossible.

Much will also depend on the attitude of lenders when the time comes to refinance, and general conditions in terms of interest rates and risk appetite.

I’m therefore inclined to leave this at AMBER/RED for the time being, to reflect the high-risk nature of these shares (Paul was RED, while I was AMBER/RED).

Fitch’s analysis makes for sombre reading and is available here.

On the bright side, if the leverage multiple does reduce to 3.5x over the next two years, then we should see a very nice recovery in the share price. But there is no doubt that it’s a gamble.

McBride (LON:MCB)

Up 18% to 120p (£209m) - Trading Statement - Graham - AMBER/GREEN

McBride, the manufacturer of private label cleaning products, is an example of what can happen when a company survives a debt scare:

Today’s update is officially in line:

H1 adj. operating profit up 8% vs. last year, with full-year adj. Operating profit expected to be “in line with internal expectations”.

Zeus aren’t listed as a broker to McBride (link) but they do publish on it, and today they have upgraded their PBT and EPS forecast for the company by 4%, for every year out to FY June 2027.

They now suggest that adj. PBT for FY June 2025 will by £49m, rising to £52.4m for FY June 2026.

It would be much preferable if MCB put their expectations in the RNS or on their website, instead of forcing investors to play the game of chasing broker notes to see what the expectations actually are.

Continuing with today’s update:

Revenue up 2.9%, volumes up 5.9% (so average prices have fallen this year?)

Two new multi-year contracts with large FMCG clients over the past six months caused a surge in contract manufacturing volumes (up 69%).

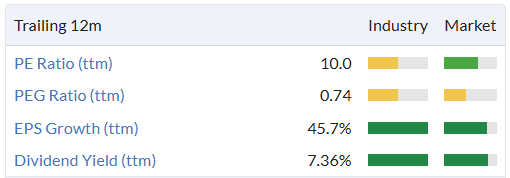

Net debt at the end of year was £118m. Net debt to EBITDA only 1.3x. It looks to be in a safe place now.

Dividends: thanks to a new €200m credit facility (announced in November), MCB will be able to start paying dividends again. Details to be announced with full-year results in September.

Graham’s view: I was AMBER/GREEN on this at 119.7p in September and it seems reasonable to stay positive on it today as the company continues to trade well and make progress on a number of fronts.

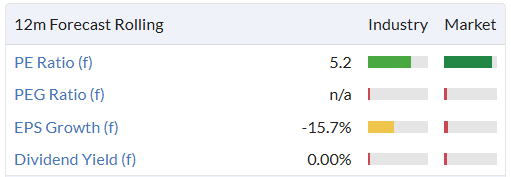

Why not make it fully GREEN? Perhaps I should do that, but I tend to think that manufacturers (who don’t also own valuable brands) ought to trade cheaply.

For example Zeus, looking at MBC’s peers, suggest a price target of 180p which they say would be a PER of 8x. That chimes with my own view that a high single-digit P/E multiple would be a fair price for this type of business. So I do think there’s an opportunity from the current level (PER only 5x), and I am positive on it, but I’d be a seller if the PER ever made it to double digits.

Well done to those who correctly called this and took a chance on it when the situation looked dire - they've cleaned up.

Character (LON:CCT)

Down 3% to 251p (£47m) - Trading Update - Graham - GREEN

I played with this idea of putting this on my 2025 watchlist, but instead gave it an honourable mention in my 12 stocks of Christmas.

Today the company announces an in line trading statement with respect to profitability for the current financial year, FY August 2025.

However, trading conditions “have continued to be challenging”. Sales and PBT this year are expected to be “at similar levels to those reported in the previous year”

Last year, sales were £123.4m and adj. PBT was £6.6m (actual PBT: £5.7m). Existing forecasts suggest something very similar again.

Aside from the difficult external conditions, the company itself seems to be in good shape:

Coupled with its strong stable of products for 2025, Character continues to benefit from a robust balance sheet, with a healthy net cash position and substantial unutilised working capital facilities in place.

Graham’s view: no complaints from me about Character, I like the company and I like the stock. The current £2m buyback doesn’t excite me too much as these aren’t bargain levels, but it doesn’t hurt:

Character enjoys a StockRank of 90 and I’m going to leave this at GREEN, a reflection of its strong, tangible balance sheet, net cash position, long history of profitable operations, and its shareholder orientation as demonstrated by dividends and buybacks.

Everyman Media (LON:EMAN)

Down 11.5% to 44.7p (£41m) - Trading Update - Graham - RED

This full-year update (for a 53-week period) starts off ok, but it doesn’t mention performance against expectations:

Revenue is up 17.9% to £107.2m (but this includes new venues, so it’s not like-for-like).

EBITDA £16.1m (2023: £16.2m) (GN note: I consider this metric to be irrelevant for a cinema).

Market share 5.4% (2023: 4.8%)

Net debt falls from £19.4m to £18.2m.

Checking a broker note from Canaccord (thanks to them for publishing this), it confirms that these figures are below expectations. They also cut expectations for FY Dec 2025 and FY Dec 2026, both of which are expected to be loss-making.

The revenue forecast at Canaccord for 2024 was £108m (actual £107.2m), while the EBITDA forecast was £19.3m (actual £16.1m).

The “Current Trading and Outlook” section explains the poor trading in Q4 and raises concern around the outlook for the next two years:

Box office performance in the fourth quarter was not as strong as anticipated, the most notable underperformer being Joker; Folie à Deux. This was followed by congestion in the calendar on remaining blockbuster releases, with five in five weeks, leading to titles competing against each other negatively impacting the period.

Guest spend per head, whilst still in growth for the full year, softened during November and December due to the higher than expected proportion of family content.

As a consequence of increased uncertainty arising from the Autumn statement, the Board is more cautious around the outlook for 2025 and 2026.

Of course it wasn’t EMAN’s fault that Joker 2 flopped: it was the Director’s fault, who decided to make a superhero/musical movie. I’m one of the few people in the world who likes both genres, but I still wish he hadn’t done this!

Looking forward, EMAN “has confidence in the film slate for 2025” which includes the next installment of Wicked.

With respect to their balance sheet, “the Group's focus continues to be on controlling net debt and materially reducing leverage over the next two years”. There is a year-on-year reduction in net debt to £18m.

Graham’s view: I’ve been RED on EMAN (e.g. see here when I was RED with the share price at 60p), as this is another one where I think the company should have posted meaningful profits by now.

But it hasn’t done so, and instead distracts us with EBITDA numbers which I’m afraid I think are meaningless.

The company has suffered some very bad luck such as Covid and then the Hollywood strikes, and I’d love to think that performance could improve.

But at the end of the day, this is a loss-making, capital-intensive and indebted business with lots of fixed costs.

Losses are pencilled in at least until FY Dec 2026, and I don’t see why they won’t continue after that.

I hope they prove me wrong, but I’m afraid I don’t see any point in investing in this one.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.