Good morning! Happy May Day - or Calan Mai, Beltane, Labour Day, or whatever you prefer to call it!

As it's Friday, I'll attempt to catch up on interesting stories we missed during the week.

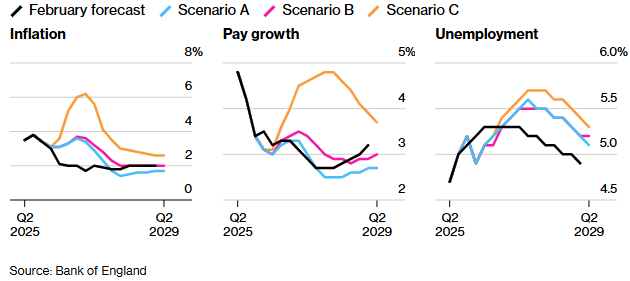

Bank of England/ECB: there was lots of discussion yesterday about the need for rate hikes.

At the ECB, where rates are starting from a lower base, they considered hiking yesterday - but ended up pushing the decision back to June.

The Bank of England gave us a thought experiment - different inflation scenarios based on second-round effects kicking in from the oil supply shock.

No probabilities were attached to each scenario, but the one referred to as Scenario C was "likely to warrant a forceful tightening in monetary policy".

The consensus reads: "there is a risk of material second-round effects in price and wage-setting, which policy would need to lean against".

Markets are now pricing in two BoE rate hikes this year, although there is clearly the potential for more than that. Chief Economist Huw Pill wanted a hike yesterday.

The bottom line? Domestic stocks are unlikely to get a boost from rate cuts any time soon.

All done for today, have a good weekend! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Natwest (LON:NWG) (£51.4bn | SR85) | Attributable profit £1.4bn, EPS +15.5% compared with Q1 2025. ROTE 18.2%. TNAV per share 400p (share price: 585p). “Based on our latest expectations for interest rates and economic conditions, we now expect income excluding notable items to be at the top end of our previously guided range of £17.2 - 17.6 billion.” | GREEN ↑ (Graham) [no section below] This ROTE return is excellent and I note that the full-year result was even better at 19.2%. We’ve been moderately positive on this one (see Roland’s coverage last year) but at that sort of ROTE I don’t know how I can avoid upgrading it. The P/E multiple is now 8x and it trades at a premium to book value, so it’s a little expensive in sector terms, but the earnings growth and returns appear to justify that. If it wasn’t a bank, I’d be very interested to buy a stock with this value-quality combo! The CET1 ratio of 14.3%, which has increased since Dec 2025, says that it’s still being run conservatively despite the strong returns generated. | |

Pearson (LON:PSON) (£6.5bn | SR73) | Underlying sales up 4%. On track to deliver 2026 guidance. £350m share buyback programme progressive well. | ||

Rotork (LON:ROR) (£2.5bn | SR39) | Q1 performance in line with expectations, full year guidance unchanged. Revenues up by a low single digit percentage on organic constant currency basis. | ||

Newriver Reit (LON:NRR) (£323m | SR70) | LTV reduced to “close to medium-term guidance level of <40%”. FY March 2026: Underlying Funds From Operations per share and EPRA Net Tangible Assets per share expected to be in-line with analyst consensus. | AMBER/GREEN = (Graham) [no section below] Roland reported on this retail REIT last month, noting that the <40% LTV target hadn’t been reached yet (it was 42.3% last September). That remains the case today, but NRR says it is “close” to hitting the target. The difference of an extra 1-2% in LTV doesn’t matter if the properties are performing, and that appears to be the case with funds from operations in line with consensus (i.e. around £37.2 million). Disposals are happening in line with book value, at least in the aggregate, implying that net tangible assets per share (107p) may be a realistic figure. With a share price of 75.5p, representing a 29% discount, I’m happy to leave our moderately positive stance unchanged. If I was investing primarily for yield, this would be high on my list of candidates for further research. The retail environment might be fragile but I don’t think NRR is taking on all that much financial risk. And it has borrowed cheaply: at less than a 200 basis point premium to base rate. | |

Serabi Gold (LON:SRB) (£252m | SR99) | Revenue of $155.8 million (2024: $94.5 million) reflecting higher production and gold price. Inaugural annual dividend payment of 5p. Net cash $42.1m. “Whilst our stand-alone strategy envisions growing the Palito Complex and Coringa into a consolidated +100,000 ounce per annum producer, we remain amenable to inorganic growth opportunities…” | AMBER/GREEN = (Graham) | |

Redcentric (LON:RCN) (£208m | SR58) | Successful completion of the sale of its entire data centre business for estimated £122.85m. Initial payment of £115.4m was received on 30th April 2026. Enables “a substantial return of capital to shareholders, significant debt reduction, and a sharpened strategic focus on growth opportunities within the remaining Managed Services Provider business.” Tender offer proposed for >£90m at 160p. | ||

Mkango Resources (LON:MKA) (£176m | SR10) | Pre-tax loss $17.8m. Cash $3.1m at year end. Subsequently raised net proceeds £11.7m. HyProMag Ltd (UK): Evaluation underway for a phased expansion of capacity starting next year. HyProMag GmbH (Germany): plant was officially opened by the German Federal Ministry for Economic Affairs on 28 April 2026. HyProMag USA: lease agreement in Texas signed in December 2025. | ||

MJ GLEESON (LON:GLE) (£134m | SR44) | Net reservation rates for the 11 weeks to 24 April were 0.88 per site per week (last year: 0.86). Excluding bulk reservations: 0.59 this year, 0.64 last year. New provisions for remedial works: £5.2 - 7.1m. Outlook: Adjusted PBT in line with market consensus. | ||

Shield Therapeutics (LON:STX) (£93m | SR27) | Net revenue $18m (Q1 2025: $7m). EBIT $2.5m (Q1 2025: $4.4m loss). | ||

accesso Technology (LON:ACSO) (£88m | SR85) | Following a “long-planned transition period”, a new CEO has been appointed. He joined as COO in Jan 2025. | ||

Pulsar (LON:PULS) (£54m | SR42) | Revenue £61.2m (2024: £62m). Adjusted EBITDA £10.4m (2024: £9.3m). Pre-tax loss £9.5m (2024: £6.7m). “We are at a clear inflection point in our cash generation profile, with a strengthened balance sheet and significant operational momentum...” | ||

Proservice Building Services Marketplace (LON:PRO) (£31m | SR34) | “As previously announced, FY27 is expected to be a transitional year and this is now set against an uncertain macro-economic backdrop… Given the potential volatility in the UK economy, the Board believes a prudent approach is required and therefore FY27 underlying EBITDA is expected to be between £9 million and £12 million.” |

Backlog

Synthomer (LON:SYNT)

Up 41% today to 97p (£159m) - Final Results - Graham - AMBER/RED ↑

There has been a stampede into this polymer stock today, although its results were actually released yesterday.

We’ve been RED on this, flagging it as a high-risk situation (e.g. coverage last month). But high-risk situations sometimes work out well.

The key news is around refinancing:

· Stable financial position to support delivery of strategy including divestments and earnings recovery

− Bank facilities refinanced with maturities extended to 2029

− Net debt: EBITDA covenants reset; security and guarantee package provided by certain group companies

Bank support is necessary considering the following:

2025 revenue down 10%

Underlying operating profit down 21% to £37.6m

Statutory loss £120m (last year: £87m loss).

And in terms of the debt burden:

Year-end net debt £575m, many multiples of the market cap.

Net debt:EBITDA multiple 4.7x

The required leverage multiple was 5.25x, so they passed that test..

New covenant tests:

The net debt:EBITDA ratios required under the covenant for year end 2026, 2027 and 2028 have been set at not more than 6.25x, 5.25x, and 4.25x respectively…

These are all higher multiples than what is typically considered acceptable. Anything above 3x is risky in most industries.

Also, the balance sheet provides little tangible support. Net asssets are £54m after excluding intangibles.

Outlook: “Q1 2026 in line with expectations and ahead of prior year; expecting robust Q2 2026”

And this is encouraging:

Full year expectations of year-on-year progress driven by self-help actions unchanged at this stage. Given the current conditions, risks are to the upside but longer-term effects of the Iran conflict remain uncertain

Graham's view

Normally I would be RED on a business with net debt standing at many multiples of its market cap.

However, Synthomer looks like it may be on a path to survival.

The largest shareholder - a Malaysian company called Kuala Lumpur Kepong Berhad - has helped to bail it out by buying £50m of its receivables. Its RCF lenders and UK Export Finance are also standing behind it.

But a word of warning: its €350m bond was still trading yesterday at just 63 cents on the euro, signalling that it's still viewed as high risk in the bond market:

According to the Deutsche Börse website, the yield on this bond is over 27%.

Buyers of the common stock have seen this four-bag since the March lows.

But I think the bonds might also be worth a look: earning 27% until 2029 is not to be sniffed at!

I’ll upgrade our stance on this to AMBER/RED, reflecting that it’s still a high-risk situation, but one where most of the lenders remain supportive.

Whitbread (LON:WTB)

Down 5% since yesterday at 2280p (£3.8bn) - Preliminary Results & Outcome of Business Review - Graham - AMBER/GREEN ↑

A big shakeup is on the cards here.

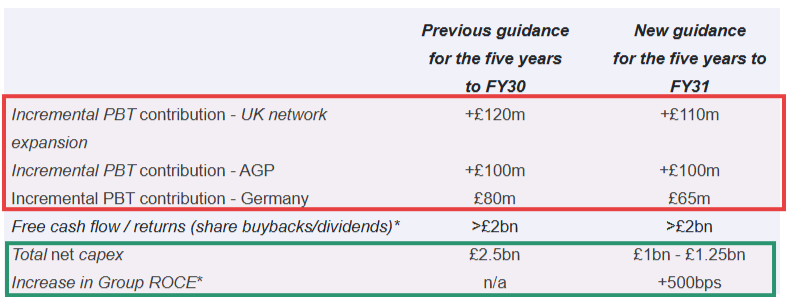

Let’s focus on the Outcome of Business Review announcement.

Background: “in light of significant cost increases in the form of business rates and National Insurance, as well as the implied market discount to our inherent value, we've looked hard at the options open to us to maximise value creation…”

The main three planks of the plan:

Network expansion: Reallocating capital spend to the highest returning opportunities while growing rooms (£110m incremental PBT contribution by FY31).

Accelerated growth: Replace all 197 branded restaurants with a more efficient integrated restaurant offering. 110 of the restaurants to be sold as going concerns. A 100% integrated food & beverage offering will allow more rooms and a 15-20% return on capital, with £100m incremental PBT by FY31. Job cuts: 3,800.

Lower capex: £1bn capex reduction in total capex vs. the previous Five-Year Plan. Recycling £1.5bn of freehold property. Looking to grow on a leasehold basis from now.

The new target is £275m of total incremental PBT by FY31, compared to FY26.

For context, adjusted PBT in FY26 was £483m. So I think they are looking for compound profit growth of about 9% p.a.

The plan will turn Whitbread into “a higher-margin, higher-returning pure-play hotel business.”

Graham’s view

Here’s a summary of the financial changes to the Five-Year Plan. What’s striking to me is that the PBT targets haven’t changed all that much (in red):

The really big change is in capital intensity: lower capex and higher ROCE.

The company calculates its own ROCE at 11% in FY February 2025 and FY February 2026, and is now targeting 15-20% by FY 2031. Investors should beware that the company's heavily adjusted calculations come up with much higher historic ROCE figures than Stockopedia does.

There is no change to the free cash flow forecast over this timeframe but I would expect higher cash flows and more cash available for shareholders in the subsequent years.

The plans should placate US hedge fund Corvex, who have been agitating for change (and Board representation):

Revealing its stake in December, Corvex said:

“…following the recently announced UK Budget and changes to rateable values and business rates, we believe the Company should undertake a strategic review to assess its capital allocation priorities and overall strategic direction…

In particular, we believe the Board of Directors… should review the Company's current five-year capital plan, which contemplates approximately £3.5 billion of investment—an amount approaching the Company's current market capitalisation.”

That £3.5 billion total investment figure given by Corvex doesn’t match the net capex figure supplied by Whitbread itself (£2.5bn), but the overall point is understood. Either the market cap is too low, the planned spending will generate very weak returns, or some combination of the two.

I’m happy to upgrade our stance on Whitbread by one notch, to AMBER/GREEN, as it’s not particularly expensive here and ROCE should improve, freeing up cash for shareholders in the long run.

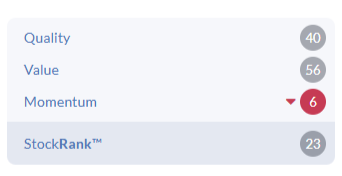

Historic performance is unimpressive, and the stock has been a dog, which is reflected in the StockRanks:

The new strategy moves Whitbread towards the Travelodge model: a simple restaurant with a limited, standardised menu. It's fair for guests and employees to have mixed feelings about this - but it makes sense for shareholders.

Graham's Section

Serabi Gold (LON:SRB)

Up 1.5% at 338p (£257m) - Audited Results for the year ended 31 December 2025 - Graham - AMBER/GREEN

Excellent results here, as expected, at an average gold price of $3,481.

The live gold price today: $4,576.

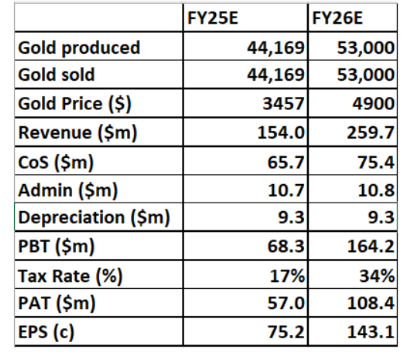

In February, Mark covered this one and gave us the following table:

His numbers for FY25 are impressively close: actual revenue comes in at $155.8m, and after-tax profit (PAT) comes in at $53.9m.

For FY26, each $100 move in the average gold price changes the revenue and profit figures by $5.3m, pre-tax. Or maybe slightly more - production guidance is for 53,000 to 57,000 ounces.

Assuming that the difference converts cleanly to profits, there is a 1.6% change in PBT for every 1% move in the gold price.

Which makes this a very effective bet on the gold price, as it has been for years now:

The All In Sustaining Cost in 2025 is $1,816, which I understand to be above industry averages - but very profitable in the current gold price environment.

Cash balance: $49.2m.

Inaugural Dividend: 5p per share, value $5.4m.

2026 shareholder returns: 20-30% of free cash flow to be returned via dividends or buy-backs.

Comment by the Chair: they are targeting 60,000 ounces of gold from 2027 onwards, with an aggressive brownfield exploration programme in Brazil:

…the Company drilled 38,400m which has already contributed to the growth of our consolidated M&I [measured and indicated] resource to 731,000 ounces of gold and Inferred resource to 653,000 ounces of gold. Whilst a significant discovery was made at Coringa, there were many additional veins which were drilled on both properties and incorporated into the updated mineral resource estimate. The results of the first year alone, reinforce the Company’s understanding of the wealth of brownfield mineralisation available near its mines and we therefore remain optimistic that the second year of our brownfield exploration programme will achieve the targeted growth range.

Graham’s view

I’m not going to rock the boat by changing our stance here.

We are AMBER/GREEN, but our stance is almost redundant - the main driver is the gold price.

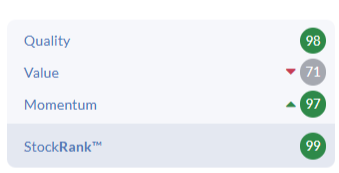

The StockRanks continue to love it:

I have personally only ever invested in one mining stock: Orosur Mining (LON:OMI). This was a long time ago - somewhere in the early 2010s, back when it was a gold producer in Uruguay.

I had done my research, and understood that the cash flow being produced was enormous relative to the market cap.

But I soon learned my lesson. The cash flow from successful production operations was reinvested into various other projects, including exploration.

If the cash had been delivered to shareholders, it would have been a successful investment. Instead, it was spent on various other projects, some of which worked, and some of which didn't. I sold and never looked back.

At least Serabi is promising to spend 20-30% of its free cash flow this year on shareholder rewards. That’s a solid sign of shareholder orientation. But if I was invested here, I’d be asking for even more.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.