Good morning!

We had several hundreds of viewers watching last night's webinar, and participating with comments and questions - I hope you enjoyed it!

Turning to today, as it's Friday, I'll attempt to catch up on interesting stories we missed during the week.

Have a great weekend! Cheers.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Mondi (LON:MNDI) (£3.7bn | SR42) | Market conditions remained challenging resulting in an underlying EBITDA of €212m including €8 million of forestry fair value gain (Q4 2025 €214 million, including €1 million of forestry fair value gain). “These pressures persist into the second quarter and we are taking pricing actions to mitigate their impact. While there is an inherent time lag, we expect these measures to take full effect in the third quarter.” | ||

Computacenter (LON:CCC) (£3.6bn | SR95) | “We now expect to deliver a much stronger performance in the first half of the year than previously anticipated… we now anticipate delivering full-year results comfortably ahead of market expectations.” | ||

Serica Energy (LON:SQZ) (£1.06bn | SR71) | Planning to arrange fixed income investor meetings. A new 5-year senior unsecured bond issuance may follow, to repay the Reserve Based Lending debt. Production has increased significantly, Q2 average so far 49,100 boepd. Guidance for 2026 remains unchanged. | ||

Redcentric (LON:RCN) (£190m | SR50) | “The proposed capital reduction will create additional capacity to deliver further returns to shareholders while maintaining a strong balance sheet.” | ||

Record (LON:REC) (£106m | SR80) | Positive net flows $1.4bn. AUM falls from $115.9bn to $114.6bn (negative asset movements/FX movements). Average fee rates “broadly unchanged”. Earnings expectations for the full year unchanged. | ||

Cyanconnode Holdings (LON:CYAN) (£28m | SR18) | FY March 2026: expects revenues >£20m (FY25: £14.2m). “The Company continues to make steady progress with several long-term prospective projects in the APAC region and the Middle East. These opportunities are moving closer to order stage…” | ||

Celsius Resources (LON:CLA) (£24m | SR30) | Trading of CLA shares to be restored on the Australian exchange. Dispute is ongoing re: the acquisition by Sodor, Inc and its affiliate of shares in Makilala Mining Company and the mineral processing company for the MCB project. | ||

Manolete Partners (LON:MANO) (£22m | SR64) | Strong H2. FY26 revenue £28m in line with expectations. Net debt £11.5m. £4.7m exposure to debtors who have not paid. May make £1.5 - £2.0m provision. Expects “adjusted realised profit before tax” of £1.9m before any adjustment for these debtors. | ||

Light Science Technologies Holdings (LON:LST) (£16m | SR24) | FY November 2025. Revenue £8.6m (2024: £12m). Loss before tax £0.89m (2024: £0.03m). Cash £0.7m. Raised £6.6m post-period end. “The enlarged Group is strongly positioned to capture a greater share of value chain…” | (Graham) - These results are very late, but the company has been busy in recent months with fundraising and acquisitions. |

Backlog: BRCK, ASC, DIAL, FOXT, DOM.

BRCK (LON:BRCK)

Up 4% to 50.58p (£163m) - Graham - GREEN =

There was lots of news from Brickability - now called “BRCK” - yesterday evening.

3.57pm: “Response to Rule 2.8 Announcement from Atlas”

The Board of BRCK Group… notes the statement made by Atlas Holdings… earlier today confirming that it does not intend to make an offer for BRCK.

At the end of March, there had been a “non-binding indicative proposal” from Atlas to buy BRCK at 65p, rejected by BRCK’s Board.

There followed a period of due diligence and consultation, to see if an improved offer might be made and accepted.

The end result: the two sides are walking away from each other.

4pm: Pre-close trading update

BRCK Group expects to report another year of revenue growth at approximately £645.0 million, an increase of c.1.2% over the prior year (FY25: £637.1 million). Furthermore, FY26 Group adjusted EBITDA before share based expense is expected to be c.4.4% ahead of the prior year at approximately £52.3 million (FY25: £50.1 million).

This announcement is in line with expectations.

Net debt is £60.5m (leverage multiple 1.15x)

It wasn’t all plain sailing:

Many of the Group's businesses were impacted by the continued challenges of the housing market during the second half of the financial year and, as widely reported, adverse wet weather also negatively affected the beginning of 2026, the final quarter of the Group's financial year. In addition, some of the secured projects within the Contracting Division were impacted by continued delays in the receipt of Building Safety Regulation… approvals to commence works.

THE CEO says: “we are exceptionally well-placed to capture significant value from the enduring structural demand across our end markets.”

Graham’s view

I covered the offer from Atlas here, noting the large premium (50% to 60%) over the prevailing share price

Based on the cheap earnings multiple and the interest from a reputable private equity outfit, I was comfortable upgrading our stance on this by one notch, to fully positive.

After an in-line update, there is no need for me to change stance today.

The private equity buyer has walked away for the time being, but they were willing to pay 65p. So if their analysis is right, then fair value is likely to be a good bit higher than that!

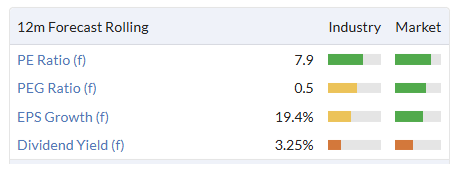

A reminder of some of the value metrics here:

Net debt of £60m is significant but the leverage multiple of 1.15x tells us that it should be a manageable amount of borrowings.

It’s not a sleep-soundly-at-night type of stock. Leverage plus cyclical housing market demand is not the type of combination which I’d want to bet heavily on.

But there’s a price for everything, and this seems to be priced for shareholders to do well - probably.

I always seem drawn to these stocks categorised as Contrarian by the algorithms.

The only weak point is Momentum - and that seems to be picking up:

Asos (LON:ASC)

Up 2% to 254p (£304m) - Interim Results - Graham - RED =

We already got the H1 trading update here.

Yesterday, the results were published.

The main point is that FY26 guidance is unchanged.

This is all copied and pasted from the trading update:

GMV to show an improving trajectory throughout the year, 3-4ppts ahead of revenue

Gross margin improvement of at least 100bps to 48-50%

Adjusted EBITDA of £150m-180m

Broadly neutral free cash flow

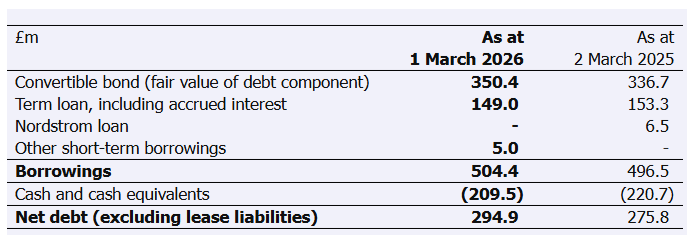

Net debt is up by £19m year-on-year, reaching £295m.

That gives a leverage multiple of 1.8x forecast adj. EBITDA (using the midpoint of the range).

Ordinarily, a leverage multiple of 1.8x is considered OK.

But that assumes we are talking about a profitable business.

Adjusted EBITDA is positive (£64m in H1, £150-180m for the full-year), but adjusted EBIT is negative.

And if the results aren’t shielded by adjustments, they are truly awful: the H1 pre-tax loss is £138m.

ASOS is forecast to remain loss-making for the foreseeable future, although adjusted EBIT may turn positive next year, if the forecasts are to be believed.

CEO commentary

I like the CEO’s goals:

ASOS has the ambition to be the most inspirational destination for young fashion lovers on the planet. This ambition is built on three core pillars: our capacity to provide the most relevant product to our customers; providing the most inspirational shopping experience; and underpinning this with an efficient and flexible operational model. It is the combination of these three pillars that differentiates ASOS and will turn us into the reference of the online fashion market.

In addition to their own brands, they “a broad and carefully curated selection of established and emerging brands from around the world, making us both a destination for leading brands and a platform for discovering new brands and new fashion.”

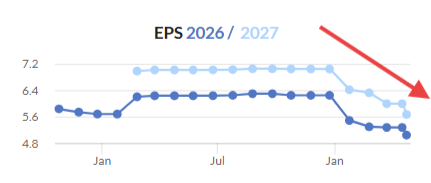

The turnaround is in full swing, with some improvement in the trend for Gross Merchandise Value - although it’s still declining for now, down 9% year-on-year.

The focus is on creating a more efficient operating model, controlling costs, reducing inventories, and fundamentally changing the relationship with their customers: “moving from a promotion-led model to one centred around excitement, with customers engaging with ASOS to discover something great rather than hunting for a bargain.” Moving up the value chain, in other words - not easy when catering to a young demographic struggling with student loans, etc.

Graham’s view

As I said last time, I agree with the logic of avoiding head-on competition with Shein and Temu, as that’s unlikely to end well.

If they were approaching this with a clean slate, I’d be encouraged.

The problem is the balance sheet - how long can they afford to be unprofitable while they evolve?

The latest debt picture:

I’ve checked the footnotes: the convertible bonds have a conversion price of £79.65, so they aren’t going to get converted (the share price would have to increase by 3,000% to exceed the strike price).

There are about £250m of these convertible bonds left outstanding, with some of them having been repaid in the last two months. They charge 11% interest - a hefty burden for a business in the middle of a turnaround.

In conlusion, I’d rather be a bondholder here, rather than a shareholder. I’d say the bondholders have a decent chance of getting their money back, e.g. with the help of an equity refinancing next year.

But as I don’t think the equity is safe, I’m staying RED here at a £300m market cap.

Diales (LON:DIAL)

Up 23% this week to 27.2p (£14m) - H1 Trading Update - Graham - AMBER ↑

This describes itself as “the leading global professional services consultancy to the construction and engineering industries”.

Yesterday’s H1 trading update was “at least in line with expectations”:

The Group expects to report revenue from continuing operations of £23.7 million (H1 FY25: £21.6 million) and deliver a 43% increase in underlying operating profit from continuing operations in the region of £1.0 million (H1 FY25: £0.7 million). On the basis of current trading, the Group expects to deliver FY26 results at least in-line with market expectations.

Cash has improved from £3m (Sep 2025) to £3.9m (March 2026).

CEO comment:

"The Group has entered H2 FY26 with increasing confidence as our transformation strategy gathers pace. For the last four years we have consistently enhanced our profitability, expanded our talent base and deepened our presence across key markets. Despite ongoing geopolitical pressures creating uncertainty for many of our clients, demand for our specialist expertise remains robust.

Estimates at Equity Development are unchanged.

FY Sep 2026 revenue £44.4m, adj. PBT £1.5m, adj. EPS 1.9p

FY Sep 2027 revenue £45.5m, adj. PBT £1.7m, adj. EPS 2.1p

Graham’s view

It’s been a long time since we last looked at this one.

We were a little negative on it before, which no longer seems appropriate for a Super Stock that’s performing “at least in line” (i.e. potentially ahead of expectations).

However, it is still a consultancy business, and I’m not sure why it should deserve a particularly high earnings multiple. With adjusted EPS of about 2p, it’s trading at 13-14x earnings. That does seem rather aggressive to me, for the sector.

Perhaps this is a little too cautious, but I’m only going to upgrade our stance by one notch, to neutral.

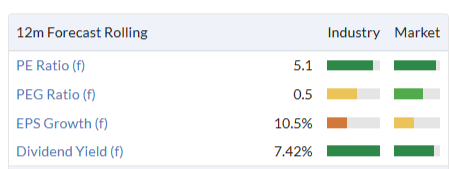

Foxtons (LON:FOXT)

Up 3% at 43p (£124m) - Q1 2026 Trading Update - Graham - AMBER =

Let’s get an update on the London property market from Foxtons.

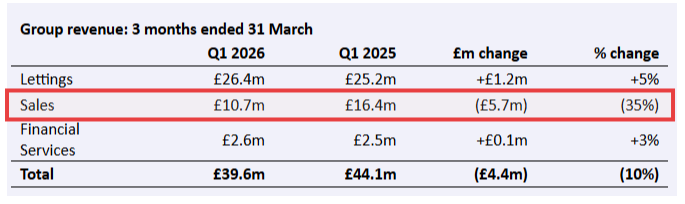

Overall revenues are lower, dragged down by weak Sales:

Lettings: the 5% growth is largely from acquisitions. “A pipeline of further acquisition opportunities exists and is currently being worked on.”

Sales: this is the standout movement, driven by the impending tax changes in the corresponding quarter last year, which made for a difficult comparison, plus “a more challenging market backdrop”:

Sales revenue declined by 35% to £10.7m (Q1 2025: £16.4m), reflecting an exceptionally strong prior‑year comparator that benefited from elevated transaction volumes ahead of the 31 March 2025 stamp duty deadline, as well as a more challenging market backdrop in Q1 2026.

They note that compared to two years ago, Sales revenue was slightly higher this quarter.

With mortgage rate increases and lower mortgage availability right now, Foxton “is taking action to reposition the Sales business to current market conditions”.

CEO comment: “Our strategic focus on recurring revenues has ensured that Foxtons has delivered a resilient performance despite recent market headwinds.”

Graham’s view

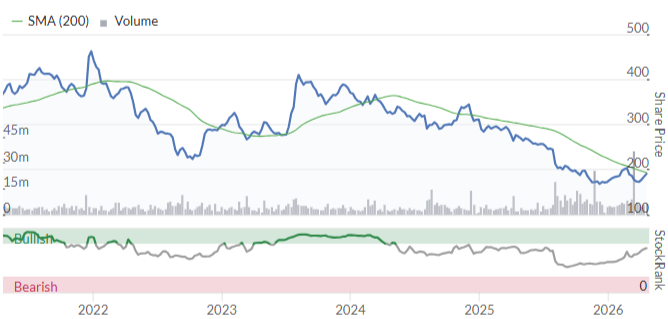

This share has already de-rated considerably over the past year, with a really poor share price performance in 2026 year-to-date:

I turned neutral on it in January, when forecasts were downgraded at Panmure Liberum (although the trading update itself did not explicitly cut guidance).

Yesterday, Panmure left forecasts unchanged. But I think staying neutral here continues to make sense.

The shares are cheap:

But that’s for a good reason:

This isn’t a quality compounder, and I think it’s priced about right here.

The bigger point is about the housing market, and the implications for other companies we follow here. London is seeing a slowdown that goes beyond just the instability caused by tax changes in Q1 last year.

If conditions improve, hopefully Foxtons will be one of the first companies to give us a sign of recovery.

Dominos Pizza (LON:DOM)

Up 4% this week to 198.2p (£763m) - Q1 Trading Update - Graham - AMBER ↑

This was an AGM update for Domino’s.

As a counterpoint to the gloom from some consumer-facing stocks, there was no drama here:

System sales +5.8% (like-for-like +4.5%)

Orders +2.3% (like-for-like +0.9%)

They are now selling Chicken - “Boneless Bites, Tenders and Wings” - under the name CHICK ‘N’ DIP.

And at this early stage, they’re on course to meet expectations for 2026:

Despite the well documented macroeconomic backdrop, our costs are hedged for the current financial year with some costs hedged into 2027 and we do not currently foresee any supply-related issues. The Board currently expects to achieve our earnings expectations for the full year.

Graham’s view

We’ve not spent much time on this share over the years - it has been too large, and too mature, to be of interest to small and mid-cap adventurers.

But the market cap is now well below £1 billion, with the share price around the levels it first reached in 2011-2013. That's a lot of optimism that has been squeezed out of the valuation.

5-year chart:

Perhaps it's worth looking at again here?

Stockopedia categorises it as my favourite style - Contrarian.

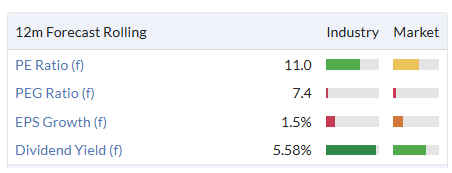

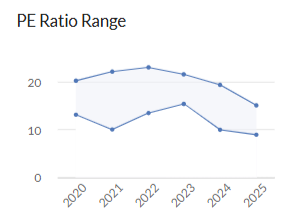

For a quality biz, this is a cheap rating:

And near the bottom of the range in which it typically trades:

Checking the archives, I see that Roland was moderately negative on this one last September, at around the same market cap. He noted that the leverage multiple was 2.3x.and that profits were expected to fall again in 2025.

I see his point, and I won’t suddenly turn us positive on this share. But surely there’s no need for us to be bearish on it at this level?

Net debt was £285m as of December 2025. Leverage was within the company's target range of 1.5x - 2.5x.

This one is starting to look interesting to me. I’m taking us back to neutral.

Have a great weekend everyone, see you on Monday!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.