Good morning!

The FTSE closed down 1.3% yesterday, as it continued to tussle with the 10,000 level.

This morning, it is set to open up 25 points, at around 9,995.

In war news, Trump has given Iran an additional 10 days to negotiate before he will approve strikes on their energy infrastructure.

Brent crude has been bubbling higher again, and is now back over $100. It’s up by around $30/barrel this month.

Israeli strikes on Iranian military assets continue.

So the mood music is still quite negative, but let’s try to find some positivity in the news today, if we can.

Backlog: there’s not much positivity in the backlog yet. I’ve given my views below on three shares that reported earlier this week. Please keep your requests coming, as we might be able to produce another couple of backlog sections today.

New writer: please give a very warm welcome to Dr. James Fox, who joins me in the DSMR cockpit today. James is a highly accomplished share analyst and stock picker, who holds a PhD in Development Economics, and we are lucky to get his perspective on shares today. Let’s try to make him feel at home!

Agenda

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| AstraZeneca (LON:AZN) (£215bn | SR70) | Tozorakimab met OBERON/TITANIA primary endpoints | Positive high-level results from the Phase III OBERON and TITANIA trials in patients with chronic obstructive pulmonary disease (COPD) showed that tozorakimab reduced the annualised rate of moderate-to-severe COPD exacerbations compared with placebo. | |

GSK (LON:GSK) (£83bn | SR92) | The EMA has accepted GSK’s marketing authorisation application for bepirovirsen, a potential first-in-class treatment for chronic hepatitis B. The company’s phase III B-Well trials met their primary endpoints, with statistically significant functional cure rates versus standard of care alone. | AMBER ↓ (James) GSK has genuine momentum and on balance I believe the direction of travel is positive. The valuation is certainly not demanding – at a circa 30% discount to the global healthcare sector and a near 50% discount to AstraZeneca on a simple P/E basis. Improved operating margins and a solid balance sheet also point to this strength. However, there is a genuine patent cliff in the medium term, and investors will need to see more positive signs before the company closes the valuation gap with its UK peer. | |

Herald Investment Trust (LON:HRI) (£1.19bn | SR N/A) | Herald’s board confirms it’s still seeking a mutually agreeable solution with Saba, which would provide shareholders with a choice of outcome. A backstop tender offer will proceed close to the NAV if no agreement is reached. The board is exploring a tax-efficient structure to allow shareholders to remain invested in a non-Saba vehicle. | ||

Senior (LON:SNR) (£1.16bn | SR74) | Advent’s PUSU (Put Up or Shut Up) deadline for Senior plc is extended to 17 April 2026. Senior rejected Advent’s previous approach, which valued the company at 270p cash plus up to 2p final dividend. Discussions with Advent and other potential suitors are ongoing. | ||

Hargreaves Services (LON:HSP) (£236m | SR96) | Hargreaves is launching a £20m tender offer at a price of 850p per share. This represents a 16.4% premium to the current share price. The board recommends that shareholders vote in favour of the buyback. Shareholders may tender up to 7.12% of their holdings. | AMBER/GREEN = (Graham) I appreciate the shareholder-friendliness of this proposal, but I don’t think it should budge me from our existing AMBER/GREEN stance (see Roland’s comments here). Roland was AMBER/GREEN on HSP at a market cap of c. £240m in January. Since then, in March, the company has upgraded its FY27 revenue and PBT expectations by 4%. The share price is also up by 4% since then. I’m therefore going to trust our previous stance and leave this on AMBER/GREEN, while acknowledging that it’s a Super Stock with a StockRank of 96. | |

Cab Payments Holdings (LON:CABP) (£220.1m | SR46) | This is an announcement by the “Helios Consortium”: they already own or control 45% of CABP shares, and proposed to buy the rest of the company for $1.15 per share. They say that the rival offer from StoneX is not deliverable as they (Helios) will not agree to it. Also, the CABP Board is not cooperating with Helios as Helios attempts to put its own offer to CABP’s shareholders. | PINK | |

Seeing Machines (LON:SEE) (£152.3m | SR20) | Adjusted revenue $23.4m (H1 last year: $25.3m). Adjusted EBITDA loss $13.7m (H1 last year: $17.7m loss). Outlook: “...royalties from automotive production volumes are projected to rise significantly in the upcoming quarters... The Company continues to trade in line with market expectations..” EBITDA to be positive in Q3 and H2. | ||

Amcomri (LON:AMCO) (£83.5m | SR61) | Subsidiary GridCore has agreed to buy the National Compliance and Testing division of Enerveo for £1. Revenues in FY25 were £5m, net assets £1.5m. | ||

ImmuPharma (LON:IMM) (£22.9m | SR8) | IMM has received a Combined Search and Examination Report in relation to its UK patent application for P140, filed in September 2025. “The supportive response is as expected by management at this stage of the patent examination process and represents an important positive milestone in the ongoing progress of the application.” | ||

Parkmead (LON:PMG) (£26m | SR55) | Revenue £1.5m (H1 last year: £2.1m). Operating loss £1.2m. As of 26th March, the company has cash and term deposits of £16.1m. Outlook: “the Group is well positioned to take advantage of organic drilling in the Netherlands and to significantly advance its renewable energy portfolio. The year ahead is expected to see multiple growth catalysts…” | ||

Europa Oil & Gas (Holdings) (LON:EOG) (£16m | SR25) | EOG has received consent from the Irish government to extend the Phase 1 of FEL 4/19 to 31 January 2028. Will use the extension to carry out further technical studies and allow more time to secure a partner to advance development of the licence. |

Backlog stocks covered: ASC, KMR, HEAD, FTC, CPI.

Backlog

Asos (LON:ASC)

Up 13% on Wednesday to 239.5p (latest market cap: £278m) - Pre-Close Trading Update - Graham - RED =

This was a H1 update to the end of February/beginning of March.

It provided some reassurance to ASOS investors on Wednesday, after the stock had dropped by around 25% year-to-date:

The company reiterated expectations for FY26. These expectations are:

Gross merchandise value “to show an improving trajectory throughout the year, 3-4ppts ahead of revenue.”

Gross margin improvement of at least 100bps to 48-50%.

Adjusted EBITDA of £150m-£180m.

Broadly neutral free cash flow.

Despite the expected improvement in EBITDA, consensus forecasts say that ASOS will remain loss-making not just in FY26 but at least until FY28.

Some other key points from this update:

Gross merchandise value down 9% year-on-year. The company points to sequential quarterly improvements (from Q4 2025 to Q1 2026, and from Q1 to Q2) - surely this is problematic, given seasonality?

Adjusted gross margin +330bps YoY to 48.5%. This does point to a level of success for the new business model.

Graham’s view

The new business model includes more emphasis on the loyalty programme and on providing suggested outfits for customers, alongside lower inventories and fixed costs.

I have no problem with any of that - it sounds like they are trying to avoid head-on competition with Shein and Temu, which makes sense.

Where I do have difficulty is getting positive on a loss-making business, in a highly competitive industry, that’s also carrying significant debts.

Net debt was last seen at £185m having been reduced by the sale of 75% of Topshop.

Compared to EBITDA, the leverage multiple is therefore only a little higher than 1x.

For a business converting EBITDA into real profits, that’s a perfectly reasonable number.

But as things stand, I remain cautious. I just don’t see enough light at the end of the tunnel - do we think it’s going to be profitable in FY29?

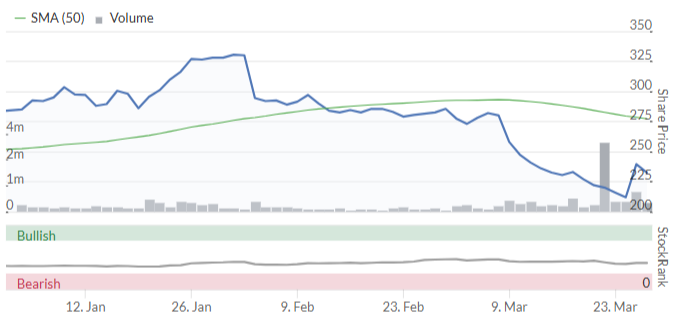

Kenmare Resources (LON:KMR)

Down 11% on Wednesday (latest market cap: £172m) - 2025 Preliminary Results - Graham - RED ↓

Kenmare Resources plc (LSE:KMR, ISE:KMR), one of the leading global producers of titanium minerals and zircon, which operates the Moma Titanium Minerals Mine (the "Mine" or "Moma") in northern Mozambique, today announces its preliminary results for the 12 months to 31 December 2025.

This is an Irish mining company. We’ve had a couple of requests for me to look at it.

The shares have had a rough year:

Overview:

Mineral product revenue of $312.1 million, down 20% year-on-year (“YoY”) due to a 13% decrease in shipments and a 6% decrease in the average price received for Kenmare’s products to $338 per tonne (excluding the by-product ZrTi)

Impairment charge of $301.3 million, inclusive of the $100.3 million impairment charge recognised in H1 2025… primarily due to lower future revenue projections associated with an uncertain pricing outlook and updated assumptions relating to the potential renewal terms relating to Moma’s Implementation Agreement (“IA”)

2025 final dividend suspended in light of elevated net debt and weak market conditions – the Board is committed to resuming dividends as soon as it is prudent to do so and financing facilities permit

The company has posted a loss of $23.7m, vs. a profit of $64.9m in 2024.

Net debt finished the year at $158.8m, up from $25m twelve months previously. This was “due primarily to peak capital expenditure during the year of approximately $156 million on the Wet Concentrator Plant (“WCP”) A upgrade project”.

They say that much lower capex is anticipated for 2026: only $60m, with “discretionary sustaining capital items being deferred where safe and practicable to do so”.

The kicker:

Kenmare is in discussions with its Lender group regarding adjustments to its Revolving Credit Facility (“RCF”), including amendments to covenant levels, in light of the prevailing weak market conditions

Q1 2026 update:

With Q1 almost complete, Kenmare is on track to achieve its 2026 guidance on all metrics and has begun drawing down its finished product stockpiles, in line with its value over volume approach

Graham’s view

Regular readers will know that I’m no mining analyst. I do not profess to be an expert when it comes to Kenmare, Mozambique or titanium minerals.

However, if I do attempt to look at it through the prism with which I study other companies, I’m afraid it’s going to be an automatic RED. The reason is that I’ve heard the keywords "discussions… lending group… amendments… covenants”.

Checking the interim results, I see that the company had equity of over $1 billion, fully tangible.

Even with an additional $200m of impairments, that leaves potentially c. $800m (£600m) of tangible equity. In theory.

However, I have no idea what the Moma Titanium Minerals Mine might really be worth. I do know that I try to steer away from companies that need debt covenant amendments, and an important purpose of our editorial colour rating is to highlight companies that we view as high-risk.

Therefore, while Kenmare might be an excellent long-term investment, the short-term financial risk requires me to put this on RED until further notice.

The StockRanks do not disagree with me, calling it a Value Trap with a SockRank of only 22:

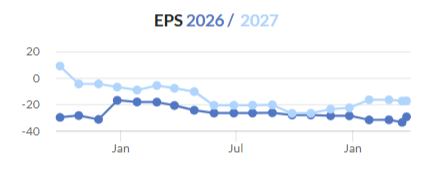

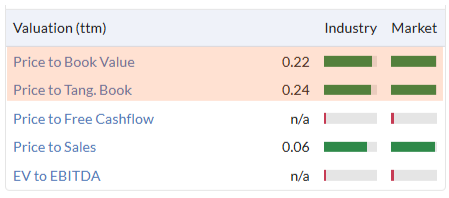

Headlam (LON:HEAD)

Down 6% on Wednesday to 42.1p (latest market cap: £34m) - Full Year Results - Graham - RED =

Headlam Group plc (LSE: HEAD), the UK's leading floorcoverings distributor, today announces its full year results in respect of the year ended 31 December 2025 (the 'Period').

These results are terrible, as expected.

The company is loss-making even at the EBITDA level, both for 2025 and for 2024.

One rule that I follow is to be very harsh on companies that are loss-making even at the EBITDA level - if they are unprofitable even with a high level of adjustments and deductions, I have to think of them as either a turnaround or a startup, not a mature company.

2025 EBITDA is minus £12.5m, while the underlying operating loss is £33.4m.

Without any adjustments used, the pre-tax loss is a staggering £70m.

This triggers another rule I use: to be very careful when a company’s annual losses are higher even than its market cap.

In this case, the annual loss is double the market cap.

Net debt: the company has rapidly moved from net cash of £10.9m into net debt of £31.4m. They have a new asset-backed lending facility that is agreed until 2029.

Asset backing: this is the main source of comfort for investors here.

The Group owns property in the UK valued at £75m. Six properties disposed over prior two years at an average premium of 84% to book value

The £75m figure is the market valuation of the properties, not their balance sheet book value.

Looking ahead, here is an outline of their financial ambitions:

…our transformation plan will create a return to profitability in 2027 and then a return to historic midsingle-digit operating profit margin levels thereafter from the annualised positive benefit of these initiatives.

To fund the strategy and build balance sheet resilience, cash is expected to be generated from property disposals and working capital optimisation. We therefore expect to have significantly reduced Net Debt by the end of 2027 with further improvement thereafter.

They say “The new strategy, specifically focused on profit generation, alters the preceding narrative which was focused on revenue growth.”

The company lost its CEO and “Chief Customer Officer” late last year. It also lost its CFO last month.

The quote about “the preceding narrative which was focused on revenue growth” (rather than profitability) strikes me as a fairly strong repudiation of the strategy pursued by former management.

Graham’s view

We’ve been fully RED on this one since its profit warning in November, and I’m not inclined to change stance today.

My reasoning is similar to what I’ve already said about other stocks today: the company is loss-making, and is expected to remain loss-making for the foreseeable future (until 2027 at the least), despite the company’s plan to produce a profitable result next year.

If they sold all of their properties today for purported market value of £75m, that would eliminate all net debt and leave them with net cash of over £40m.

Deduct anticipated losses over the next year or two, and you are let with maybe £25m of cash, before any adjustments needed for working capital, etc.

Given the market cap of £34m, this could be an interesting deep value play.

Stockopedia has noticed the discount to tangible book:

So this is a case where I think that over the medium-term, the risk:reward is potentially interesting.

I’m definitely open to the possibility of upgrading our stance on this to something a little bit less negative.

But in the short-term, I’m going to follow the simple rules that have served me so well: treating companies with negative EBITDA, and companies with annual losses higher than their market caps, with extreme caution. Headlam is an example of both.

Capita (LON:CPI)

Up 15% yesterday to 240.5p (latest market cap £326m) - Disposal - Graham - AMBR/RED

Yesterday we learned that Capita was selling its private sector contact centre business:

This is a continuation of the strategic simplification of the Group, focusing on areas where we deliver complex, differentiated middle and back-office services in large growing markets where demand for technology-enabled transformation is accelerating.

Some highlights of the deal:

Disposal is priced at £1 (I wonder will that be cash or cheque?).

£6.5m of cash will be left within the business for the buyer, for working capital.

Potential defcon of up to £61.5m, depending on future financial performance and cash availability.

Value sharing with Capita if there is another change in ownership within five years.

The buyer is Inspirit Capital, a UK private equity firm.

It’s clearly a very defensive structure from Inspirit’s point of view: nothing up front, and little risk if it doesn’t work out, beyond any losses that may be incurred in the short-term.

Although those losses could be substantial, based on the historic performance of this contact centre division:

2025 adjusted revenue £398.1m, 2025 adjusted operating loss including overhead allocations £34.9m

Capita will be left holding “only three currently underutilised properties which represent a lease liability of 2025: c. £65m and an associated lease cost c. £10m per annum…”

Also, “c. £25m of Group costs previously allocated to the business will remain with the Group”.

That sounds pretty poor - and it suggests that previous accounting was rather misleading, although that’s not necessarily the company’s fault. Central costs do have to be allocated somewhere, after all. But it’s unfortunate these costs are not leaving Capita with the business that is being sold.

Another way of looking at it is that the adjusted operating loss isn’t real. Remember from what we pasted above: the 2025 adjusted operating loss “including overhead allocations” was £34.9m.

But it turns out that this £34.9m includes £25m of central expenses that are not going away even after the contact centre business is sold.

Therefore, the real loss that’s being removed might be somewhere in the region of £10m, depending on what other adjustments are involved.

That’s very different to removing an annual loss of £34.9m.

Also, there are “Expected transaction, transitional restructuring and separation costs in 2026 of approximately £20m”. Which removes much of the near-term value of getting rid of contact centre losses in the first place.

They do promise £40m of other annualised cost savings over the next two years, from the broader simplification agenda that they are working on.

Snippet from the CEO comment:

The sale of the private sector contact centre business further simplifies the Group and will enhance our margin expansion. It enables us to focus on Public Service and Pension Solutions and invest in our technology capabilities to improve our differentiation.

Graham’s view

I turned moderately negative on this share earlier this month (at a market cap of £360m) and I’m not inclined to change stance again so soon.

This deal probably is a net positive, as it gets rid of a low-margin, loss-making, unexciting business, and simplifies the overall group.

But I’m not convinced it’s going to make all that much difference to the balance sheet or to their net profits in the near-term. Capita is having to spend money to save money, and will rely on the £61.5m defcon to get a favourable outcome.

Please see my comments from earlier this month for a bigger picture view. I do not see any fundamental change arising from this disposal, although the removal of £400m of empty revenues will at least help to improve the clarity of the story it’s able to offer investors in future years.

Our rankings categorise this as a Sucker Stock:

Graham's Section

Hargreaves Services (LON:HSP)

Up 7% to 761p (£252m) - Tender Office and Notice of General Meeting - Graham - AMBER/GREEN =

Hargreaves Services already said they were doing a £15m return of capital.

They are proceeding with this, subject to shareholder approval, and have upsized it to £20m.

The tender price is 850p.

Naturally, the company will not be able to buy back all that many shares at 850p. At that share price, £20m would buy 2.35 million shares.

The company has 33 million shares outstanding, so the tender offer can reduce the share count by 7.1%.

This is the logic behind each shareholder having an “Individual Basic Entitlement to tender approximately 7.12 per cent. of the Ordinary Shares held by them..”

It’s an attractive tender offer, compared to the prevailing share price. Indeed, HSP hasn’t been over 850p in over a decade.

That being so, I would expect the majority of HSP shareholders to tender their full basic entitlement. For every shareholder who doesn’t do that, it will enable others to sell more than their basic entitlement.

This is a share within the Harwood stable - they own 27.9% of the company, and have undertaken to tender their basic entitlement.

Graham’s view

I appreciate the shareholder-friendliness of this proposal, but I don’t think it should budge me from our existing AMBER/GREEN stance (see Roland’s comments here).

A tender offer, in general, is an excellent and perhaps under-utilised mechanism. I think of it as a buyback that’s simply more formally organised than what you get with on-market purchases. Shares are repurchased at a fixed price and in a fixed amount.

In some ways it’s fairer than on-market purchases, as everybody knows when they are transacting with the company and gets exactly the same price for their shares.

Roland was AMBER/GREEN on HSP at a market cap of c. £240m in January.

Since then, in March, the company has upgraded its FY27 revenue and PBT expectations by 4%. The share price is also up by 4% since then.

I’m therefore going to trust our previous stance and leave this on AMBER/GREEN, while acknowledging that it’s a Super Stock with a StockRank of 96.

James's Section

GSK (LON:GSK): (LON:GSK)

Down 0.4% at 2,047p (£83.1bn) – Bepirovirsen accepted for MAA review by EMA – James - AMBER ↓

Today’s announcement was unlikely to be a market move – we heard in January that Bepirovirsen had achieved its primary endpoint in trials.

However, this is a company that seems to have genuine operational and market momentum right now – and that marks a significant shift from where we were a couple of years ago.

FY25 headlines

- Revenue £32.7bn, +7%

- Core operating profit +11%

- Core EPS +12% to 172p

- Oncology +43%, HIV +11%, Specialty Medicines +17%, Respiratory, Immunology & Inflammation+18%

2026 guidance: sales +3-5%, core EPS +7-9%.

The aforementioned momentum has probably gone under the radar, but GSK has now delivered eight consecutive quarterly earnings beats. Revenue has also come in above expectations in every quarter since the split with its consumer healthcare division – now Haleon.

A snapshot of the StockReport from three years ago shows just how far the company has come. The operating margin (%) has improved 234 basis points over the three-year period, while the return on equity (%) is up 480 basis points. This is reflected in GSK’s QualityRank score of 97.

It is worth noting that 2026 guidance was set before the conflict commenced in the Gulf in late February. There could be unquantified headwinds if the conflict is sustained.

Key momentum drivers:

· Oncology is growing fast from a small base. New CEO Luke Miels has been acquisitive early – RAPT Therapeutics ($2.2bn) and 35Pharma ($950m) both bolster the late-stage pipeline.

· Cabenuva – the long-acting HIV injectable, grew 42% in 2025 and is taking share from daily oral competitors.

· HIV pipeline remains highly compelling, with Q4M treatment addressing 30% of patients and Q6M 50% of patients. Cabenuva is administered every one or two months.

“Products are the key in this business, and we need to be more product-centric...”

Sound footing

The Zantac-related overhang is now “materially complete” with GSK settling for $2.2bn – significantly lower than many had been expecting. This allows us to look at the balance sheet with greater clarity, and it’s worth noting that net debt/EBITDA sits at just 1.3x, leaving ample firepower for further bolt-on deals.

Dividends (forward yield sitting at 3.5%) are well covered by earnings (around 2.6 times), further supporting this idea of financial strength.

Broadly, its valuation grades remain strong, with the forward P/E representing a circa 30% discount to the wider healthcare sector globally.

James's view

I don't hold GSK. I find pharma and biotech highly exciting, but it’s also a sector that carries significant operational risk. The risk of a late-stage trial failure, a patent cliff, or an unexpected safety signal means position sizing matters as much as stock selection.

And this is something to bear in mind here. As much as 50% of GSK’s 2025 revenue are threatened by patent expiry in the medium term, and that puts pressure on the company’s pipeline to perform.

The company has four phase III readouts scheduled for H2, and investors will want to see continued execution before the market delivers a re-rating.

For context, it trades at a circa 50% discount on a simple earnings-basis to AstraZeneca, implying that there would be room for a re-rating if pipeline optimism improves and is sustained.

While not directly comparable, AstraZeneca says it has 197 projects in the pipeline – GSK notes 58 potential new vaccines and medicines in their pipeline.

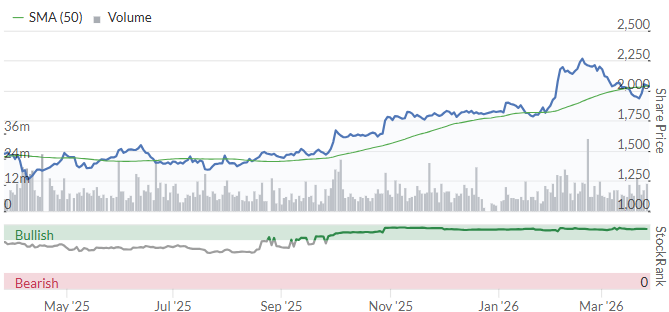

Filtronic (LON:FTC) (backlog story)

Down 0.8% at 180.50p (£400.6m) – $8m amplifier contract win – James - AMBER =

Yesterday’s contract win – an $8m agreement to develop and manufacture amplifiers for satellite communications for an American client – is another positive step for Filtronic. While modest in isolation, it’s a company that appears to have found its moment.

FY25 headlines:

Revenue £53.6m, +121%

Adjusted EBITDA: £17m +248%

Net cash £6.8m (excluding right of use property lease)

Filtronic designs and manufactures advanced RF solutions for the space, aerospace, defence, and telecoms infrastructure markets. Ironically, it went under most investors' radars until April 2024 when it announced a strategic partnership with Elon Musk’s SpaceX.

The partnership, expanded in FY25 and again in FY26, has resulted in the largest contract wins in the company’s recent history. This $62.5m (£47m) contract complements additional wins the likes of Leonardo and Airbus.

Visibility looks really strong for a relatively small company too. The business pointed to approximately 90% of FY26 revenue covered by contracted orders. Meanwhile, Filtronic is set to launch net-gen GaN amplifier systems in calendar year 2026, including an expansion into V-band.

The forward picture may disappoint some investors, however. Management expects to meet current market expectations of £55.5m in revenue and £10.9m in EBITDA for the year.

“With a record order book, increasing customer diversification and the business now operating at greater scale, we have entered the second half confident of continuing our planned growth.”

James’s View

There are very few sectors that excite me more than space right now – equally there are very few companies I want a slice of more than SpaceX. Coupled with rising defence budgets and resilient aerospace demand, Filtronic looks exceptionally well positioned.

Of course, everything comes back to the valuation. At 50.1x forward earnings and 7.5x sales, the business looks richly valued given the current forecast, which essentially shows revenue remaining flat throughout FY26.

I think most would agree that it’s not meaningfully undervalued on current forecasts.

As the $62.5m contract with SpaceX is due to be delivered in FY27, there will almost definitely be a meaningful uplift in revenue next year. My view is that uplift needs to be sustained in order to justify the valuation as we see it today.

Investors also need to consider concentration risk. SpaceX, for example, is very good at doing things in-house.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.