Good morning!

11.10am: wrapping up the report there for now, thank you.

Spreadsheet accompanying this report (updated to 10/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

ME International (LON:MEGP) | Extension with Morrisons | Contract extension for photo booths and laundry machines. | GN’s view: this was issued through REACH, so it’s not material. |

PRS Reit (LON:PRSR) (£606m) | Q2 Update | 5,437 new homes (LY 5,264). 99% rent collection. LfL rent up 11%. Strategic Review/Sale Process. | |

M P Evans (LON:MPE) (£501m) | Crop & Production update | 1.6m tonnes in 2024 at an avg mill-gate CPO price of $823/tonne | |

Judges Scientific (LON:JDG) (£489m) | TU | 2024 results expected to be in line with expectations. | AMBER (Graham) Remain cautious on this. SDI more interesting right now. |

Cerillion (LON:CER) (£466m) | Major contract | “Supports” existing market guidance. | |

Midwich (LON:MIDW) (£299m) | TU | Adj PBT “slightly below” market expectations. | |

Reach (LON:RCH) (£229m) | TU | Strong Q4. FY results to be ahead of expectations. | GREEN (Graham) |

City of London Investment (LON:CLIG) (£192m) | TU | Net outflows of $564m in HY to Dec 24, AUM of £9.9bn. | AMBER/GREEN (Roland - I hold) |

Capital (LON:CAPD) (£162m) | TU | FY24 revenue of $348m, “marginally below” guidance of $355m-$375m. | AMBER (Roland) Teething problems in N. America have caused revenue to miss exps. |

Bango (LON:BGO) (£83m) | TU | 2024 rev $53m. EBITDA >$15.2m. Exps not mentioned; broker’s EBITDA forecast was $15.8m. | |

Van Elle Holdings (LON:VANL) (£42m) | Contract | 8yr/£30m electricity transmission schemes contract award. | GREEN (Graham) No change to f/cs at Progressive, no change to our stance. |

Sanderson Design (LON:SDG) (£38m) | TU | Profit warning. Adj PBT now expected to be £4.0m-£4.8m vs c.£7.5m previously. | BLACK / AMBER/GREEN (Roland) The shares could be entering value territory. |

Pod Point group (LON:PODP) (£26m) | TU | Adj EBITDA loss in line with guidance at c.£(14m). FY25 results will be below expectations. | |

XLMedia (LON:XLM) (£25m) | Tender offer | £16m will be returned to shareholders at 11.5p per share (24% premium). | |

Checkit (LON:CKT) (£19m) | Contract renewals and wins | No description given of any changes to earnings expectations. | |

Croma Security Solutions (LON:CSSG) (£12m) | TU | “Firmly on track to meet expectations.” H1 rev +8% (£4.6m). Cash £4.1m. |

Graham's Section

Reach (LON:RCH)

Up 19% to 85.9p (£273m) - Trading Update - Graham - GREEN

It’s a very short update from Reach:

Trading in Q4 was strong. As a result, we now expect to deliver results ahead of current market expectations for the full year.

Of course it’s churlish to complain about an “ahead of expectations” update, but perhaps they might have added some colour to this announcement, as the saying goes, and said something about where the outperformance came from?

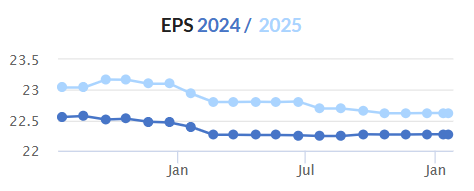

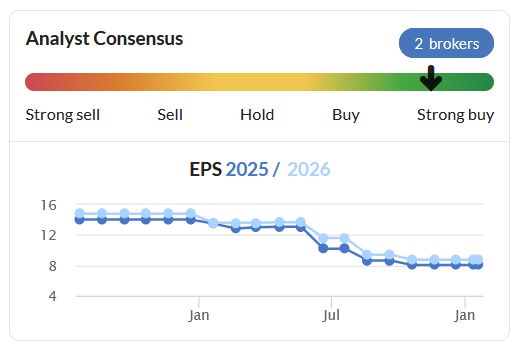

They do helpfully disclose that they consider market expectations to be for an adj. operating profit of £97.8m.

Earnings expectations have been stable for a while, which I think is reassuring as the stock is priced for disaster:

Pension warning: a £5m error was discovered in a pension scheme calculation, resulting in red faces for whoever was in charge of those spreadsheets. RCH will pay this additional £5m in 2025. RCH’s other pension schemes have been reviewed for the same error, and nothing material has been found.

Refinancing: RCH’s banking facilities have been refinanced. It’s a £145m RCF for four years, plus potentially another £72.5m. RCH must keep its leverage multiple below 1.75x to comply with covenants.

Graham’s view

I’ve been positive on this one, e.g. at 97p here. I’ve argued that the bear points - the long-term secular decline of newspapers, and RCH’s large pension liabilities - may already be priced in, leaving an opportunity for a pleasant surprise if/when things don’t work out as badly as feared.

However, the market is slow to agree with me. Even after the bounce in the share price we are seeing this morning, the share price is still lower than it was when I covered it last (marked in pink below):

It will cost over £200m to clear the pension fund debts, and this issue won’t go away until c. 2028.

Revenue is currently falling at about 4-5% p.a.

The arguments here have something in common with the debate over Smiths News (LON:SNWS) (covered last Thursday), where SNWS is the distributor rather than the owner of print publications. Both companies must struggle with the ongoing shift away from print, and in that sense they both face uncertain futures.

But both companies are also being run to maximise current profitability, and are generating very impressive profits relative to their market caps.

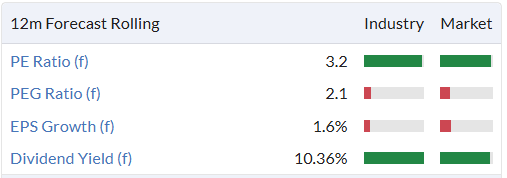

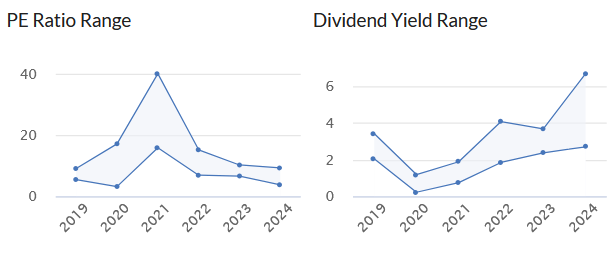

Here were RCH’s value metrics as of last night:

It’s traditionally considered to be a sign of extreme value if a dividend yield exceeds a company’s PE ratio. In the case of RCH, its dividend yield was more than three times the size of its PE ratio! And this for a company where its bankers are relaxed about the situation and have just extended their facility to the company for another four years.

I could be completely wrong about this but I continue to view RCH as a very interesting candidate for investment, though I admit that it’s in the “cigar butt” style.

Judges Scientific (LON:JDG)

Up 2% to £75.38 (£500m) - Graham - AMBER

I’ve been neutral on this one - see my coverage of November’s profit warning here (share price at the time: £88).

Today’s update confirms that 2024 was difficult, affected by Geotek’s lumpy revenue profile and Chinese weakness.

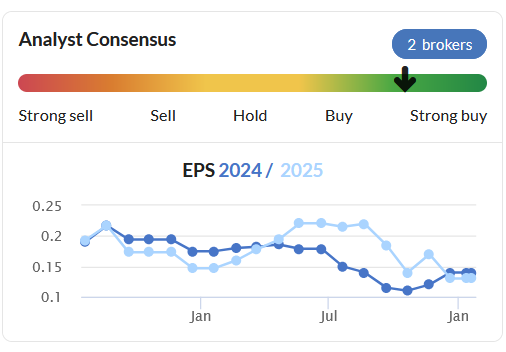

Fortunately there is no further downgrade since November and the full-year result for 2024 will be in line with new expectations for adj. EPS of 276.8p, although this is in the bottom half of the 270p-300p range that we were previously given.

Prior to the profit warning, the EPS estimate was c. 349p.

Review of 2024:

The challenging trading environment resulted in mixed trading across our Group and, as the year developed, the prospect of a 2024 Geotek coring expedition evaporated, resulting in no recognisable revenue in the year. Other headwinds affected our businesses to varying degrees, including a large reduction in orders from China, together with a general weakness in order intake and some customers delaying orders and deliveries.

Order intake: up 2.2%, excluding a large contract at Geotek. With these large contracts having a big effect on the numbers and as they are unlikely to repeat in a predictable way each year, I think it makes sense to exclude them where possible.

Organic revenues: down 5.8% excluding coring.

Outlook: 2025 is off to a good start.

The current year is starting more encouragingly, with Geotek's coring expedition having commenced and a number of the deferred projects from 2024 are now anticipated to contribute to H1 earnings. The Board remains confident in the long-term growth drivers of the business…

Graham’s view

I remain cautious on this for reasons I’ve expressed before. Also see my coverage in September. To summarise, I’m concerned by:

Geotek reducing the quality of JDG (unpredictable revenues and overall quality metrics likely to fall).

The difficulty of finding large acquisition targets that will do better than Geotek, putting a question mark over JDG’s ability to continue to make progress as it did in the past.

Weak orders and revenues across JDG as a whole, particularly from China. Have Chinese customers found Chinese-made substitutes?

The fact that the stock continued to trade a high earnings multiple (over 20x) despite these concerns.

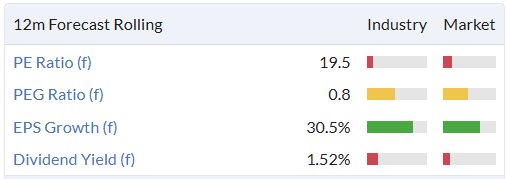

With the share price having been broadly on the decline over the past year, valuation is approaching more reasonable territory:

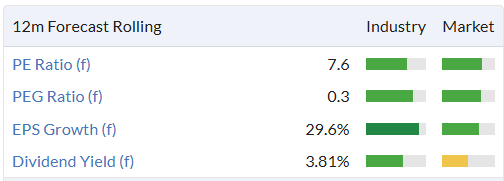

However, I note that smaller peer SDI is only trading at 8x earnings (last covered by Mark here). At that sort of price, SDI could be a more tantalising prospect right now.

Van Elle Holdings (LON:VANL)

Up 9% to 42.5p (£46m) - Eight-year electricity transmission agreement - Graham - GREEN

Another brief update for us to look at today. VANL announces that it has signed:

…an eight-year partnering agreement with Wood Transmission & Distribution Limited ("Wood") to deliver ground investigation, design and construction activities for piling and foundations across several transmission schemes as part of Ofgem's Accelerated Strategic Transmission Investment (ASTI) programme. Subject to performance, the partnership is expected to be worth in excess of £30m to Van Elle over that period.

The CEO notes that the recent acquisition of Stirling-based Albion Drilling will help to provide “a local resource base and specialist skills needed to deliver these important commitments, often in remote and challenging locations”.

Estimates: thanks to Progressive for publishing a note on VANL today. The forecasts they’ve put out are identical to the ones they published last time, including FY April 2025 revenue of £159.1m, and PBT of £6.1m. PBT is forecast to rise to £8.1m next year.

Graham’s view: it would have been more helpful if this RNS acknowledged that there should be no change in earnings expectations as a result of this agreement, or else clarified that the company did think that an upgrade was warranted. Either way I’m going to leave the previous GREEN stance unchanged here, noting a StockRank of over 90 and some cheap valuation metrics:

Roland's Section

Sanderson Design (LON:SDG)

Down 18% to 44p (£32m) - Trading update - Roland - BLACK / AMBER/GREEN

Graham last covered this luxury interior furnishings business in October, when it issued a profit warning. Unfortunately we have another profit warning today. It looks like a big one, too.

As a result of the factors outlined above the Board now expects underlying pre-tax profits for the year ending 31 January 2025 to be in the region of £4.0 million to £4.8 million.

To put this in context, broker Progressive was previously forecasting adjusted pre-tax profit of £7.6m. So today’s warning represents a reduction in around 40% in 2024 profit expectations, on the back of significant cuts to forecasts over the last year:

Let’s take a look to see what has gone wrong.

2024 H2 shortfall: in its October update, Sanderson warned investors that H2 trading would need to improve for the company to hit expectations. Unfortunately, this did not happen.

The company says that full-year sales will be 5% below expectations, at £101m (FY24: £108.6m).

As a quick reminder, H1 sales fell by 11% to £50.5m. This implies that H2 sales are also expected to be £50.5m, versus £51.9m in FY24.

This doesn’t seem like a big fall. Indeed, the numbers suggest H2 revenue was stronger than H1, in terms of the prior year comparison.

However, the company says that an altered sales mix means the hit to margins and profits will be significantly greater than the sales shortfall.

Looking at the detail, performance across the group’s revenue lines appears to have been volatile and soft in some areas:

Brand product sales: retail sales rose by 5% in Dec 2024 and then fell by 13% in the first two weeks of January. Overall brand sales down 9% for the year, at c.£71.7m (FY24: £78.8m). Consumer confidence weakest in the UK, SDG’s largest market

Increased inventory provisions: softer demand, particularly for fabric, is expected to result in an increase in provisions. This reflects accounting charges for stock that may be difficult to sell without discounting. However, the company also says that inventory is expected to unwind in the coming months, so perhaps we’ll have more clarity on this with April’s FY results.

Licensing: good momentum in H2, with FY revenue expected to be £10.1m-£10.9m (FY24: £10.9m).

Manufacturing (3rd party orders): “high margin repeat orders” have declined, while recent new business has been for “smaller print runs” resulting in lower margins due to initial set up costs being spread across lower volumes..

Net cash: expected to be c.£5m at year end (H1 25: £9.6m), reflecting recent capex of £3m and raised inventory levels. Borrowing facilities remain undrawn.

Outlook: Progressive has cut its earnings forecasts by almost 50% today and has also pencilled in a cut to the dividend (this wasn’t mentioned by the company):

FY25 adj eps: 4.6p (previously 8.3p)

FY25 dividend: 1.2p per share (previously 2.4pps)

Based on the last-seen share price of 44p, these estimates price Sanderson shares on a P/E of 9.5 with a 2.7% dividend yield.

As Stockopedia’s handy trend charts illustrate, this valuation is not out of keeping with the company’s historical rating, if we exclude the pandemic boom period:

In a situation like this, my main concerns are cash generation and the balance sheet.

Cash generation: net cash has now fallen from £16.3m at the end of January 2024 to just £5m. The fall reported for the last six months is £4.6m, of which £3m is said to have related to one-off expenditure, classed as capex by brokers Progressive.

The company’s comments suggest the remaining £1.6m may have been absorbed into inventories and working capital. An increase of this size relative to half-year inventory of £27.2m does not seem too alarming to me.

However, it may be worth pointing out that stock turnover is already very slow in this business – Stockopedia shows a figure of 1.2x on the StockReport, in line with my own calculations. This implies Sanderson takes around 10 months, on average, to shift stock.

Balance sheet: Sanderson continues to have net cash with no drawn debt. Lease liabilities also seem manageable at c.£12m, based on the interim accounts.

Checking back to the half-year accounts, Sanderson reported a tangible net asset value of £59.8m and a net asset value of £86m. The stock was already trading at a significant discount to book value ahead of today’s warning:

I estimate that the discount to tangible book value is now approaching 50%. That looks potentially cheap to me.

Roland’s view

My feeling is that today’s update represents – broadly – a continuation of H1 performance. H2 revenue appears to be level with H1 and today’s guidance implies H2 adjusted PBT of £1.8m-£2.6m, versus an H1 figure of £2.2m.

The impression I get is that the company may be suffering primarily from a nasty case of reverse operating leverage, with lower volumes and slower stock turnover causing a geared reduction in profits.

I do not know a lot about Sanderson’s products, but I would guess that demand from affluent customers will recover over time.

These shares have now fallen by around 80% from their 2021 highs and are heading towards micro cap territory, with a market cap of just £32m.

However, I don’t see any fundamental problems with the business and I’m intrigued to see the shares trading at a steep discount to their tangible book value. I share Graham’s October view that this stock is potentially in deep value territory.

While it’s possible that problems will continue to emerge, the shares look affordable to me even reflecting the impact of today’s downgrade. I think it’s worth remembering that this business has some attractive qualities, including high-margin licensing income and some valuable brands.

On balance, I would be inclined to take a closer interest in Sanderson after today. I’m going to maintain our previous view of AMBER/GREEN ahead of April’s results.

Capital (LON:CAPD)

Down 11% to 74p (£145m) - Trading and Operational Update - Roland - AMBER

Today’s full-year update from this gold mining services business includes a revenue warning and has been poorly received by the market (my bold):

As detailed below, FY 2024 revenue was $348.0 million, up 9.3% on FY 2023 ($318.4 million) but marginally below our guidance of $355-375 million.

Today’s revenue shortfall seems to have been driven by two specific issues, while broader operating metrics look more positive.

Drilling business: this is Capital’s core business. Revenue rose by 11% to $239.1m last year. The main problem area appears to be the group’s US business – it has been diversifying away from Africa over the last couple of years, perhaps prudently.

Nevada Gold Mines: this major drilling contract has suffered delays in ramping up. As a result, “contract revenues are not yet supporting the cost base”. Not ideal, but Capital is an experienced drilling contractor and says management have now spent “significant time on the ground” to move things forward.

NGM was originally expected to generate $35m/yr for three years from 2025. There’s no statement on actual NGM revenue in today’s update.

Elsewhere, a number of new drilling contracts are announced at mines in Africa, together with an extension of the scope of work for industry leader Barrick at a mine in Pakistan.

MSALABS assaying business: Capital’s other arm is MSALABs, which runs a chain of laboratories used by mining clients to test and analyse their output.

Results have fallen slightly below guidance due to lower utilisation levels in some labs, including work relating to the Nevada Gold Mine project.

FY2024 revenue of $43.6 million was broadly in line with our revised guidance of ~$45 million

Once again, changes have been made to management to improve performance, including the appointment of a new chief operating office for MSALABS.

Investments: one unusual aspect of Capital is that it takes equity stakes in companies as investments, leveraging its industry knowledge. Sometimes the investees are also clients.

This carries some risk, but is also a potential source of value creation. Recent performance appears good, as we might expect in such a strong gold market.

Capital sold its stake in Predictive Discovery to Perseus Mining (a client) for $31.2m in August 2024

Total investment gains (realised and unrealised) in H2 were $12.4m

Investments were valued at $30.3m at the end of 2024 ($47.8m at June 2024), including the impact of the Predictive sale.

Financial & Operating performance: despite the individual disappointments listed above, Capital’s overall performance appears to have been positive last year:

From this we can see that fleet size increased slightly, fleet utilisation was stable and average revenue per operating rig (ARPOR) rose by almost 10% to $204k per month. This doesn’t seem like a bad performance to me.

Outlook: There’s no update on profit guidance in today’s statement, but broker Tamesis Partners (available on Research Tree) has left its forecasts unchanged. Unfortunately today’s note does not include explicit earnings forecasts, but seems to imply a figure of $0.134 per share for 2024, similar to the $0.14 consensus shown on the StockReport.

Earnings forecasts for Capital have been relatively volatile over the last 18 months:

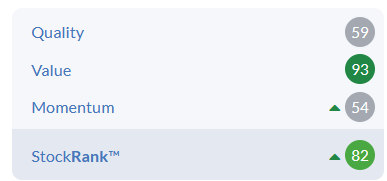

But the StockRanks suggest value and improving momentum:

Roland’s view

Capital appears to be suffering from growing pains in its US business, but this diversification may prove prudent given the increasingly uncertain political environment in some West African countries. I would imagine the incoming US administration is also likely to be supportive of the mining sector.

The shares now trade at a c.25% discount to their last-reported book value and my impression is that net debt should have fallen to a more comfortable level from the H1 figure of $86.4m.

Cash generation may also improve in 2025 as capex falls from $70-80m in 2024 to a new guidance range of $45-55m.

Today’s update did not include any revenue guidance for 2025, but existing consensus forecasts on Stockopedia suggest a further decline in earnings in 2025.

While I think that value could be emerging here, I feel the uncertain outlook means that it’s sensible for me to remain neutral ahead of Capital’s full-year results in March. AMBER.

City of London Investment (LON:CLIG)

Down 9% to 345p (£178m) - Six months to 31 Dec 24 Trading Update - Roland (I hold) - AMBER/GREEN

This niche fund manager focuses on fixed income and equity strategies that involve buying investment trusts at a discount. CLIG reports in USD and the majority of its client base is also in the US.

CLIG shares have performed well over the last year, but have given up some gains today after the company reported (yet another) quarterly net outflow.

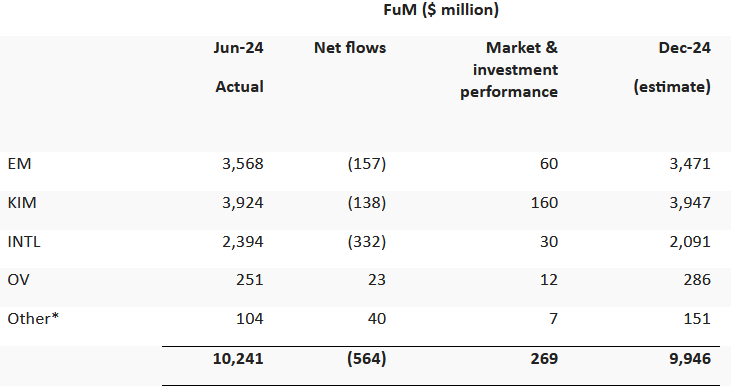

Funds under Management (FuM) were $9.9 billion at 31 December 2024, a decrease of 2.9% as compared to $10.2 billion at 30 June 2024.

The company provides a breakdown of flows by strategy:

CLIG reported net outflows of £195m in Q1 FY25 and positive market performance of £687m. Comparing these with today’s half-year numbers suggests to me that overall performance weakened during the second quarter of the company’s financial year (y/e 30 June):

Q2 FY25 net flows: £(369m)

Q2 FY25 market & investment performance: £(418m)

Despite this disappointment, the company says its main strategies performed ahead of benchmarks during the six-month period:

Investment performance for the rolling six months ending 31 December 2024 and calendar year 2024 were both ahead of benchmarks for the majority of CLIM & KIM core strategies. Strategy returns were in the first or second quartile vs peers over the same periods.

Roland’s view

CLIG’s continued outflows do not make it unusual among UK fund managers. Only a minority are reporting net inflows.

The attractions of this business for me (as a shareholder) are its 30%+ operating margin, strong cash generation, 9% dividend yield and founder ownership.

My perception is that pressure from 31% shareholder and KIM founder George Karpus has helped to give management a much-needed prod over the last year or so.

Higher interest rates are also a meaningful source of income for a business with c.$30m of net cash and I believe the dividend is likely to remain safe for now.

On the other hand, there’s a risk CLIG could continue to struggle to generate positive flows and may eventually become a classic value trap.

I’d like to go GREEN here, but I think it’s probably more prudent to choose AMBER/GREEN, reflecting the risk of continued stagnation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.