Good morning!

In case you missed it, here's a link to the latest Week Ahead with the economic calendar and list of companies reporting this week.

Today's Agenda is now complete.

1pm: all done for now, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

S4 Capital (LON:SFOR) (£202m) | Full Year Results | Results in line with expectations. Net rev -11% LFL, adj op profit -4.5%. Outlook cautious. | AMBER/RED (Roland) Today’s results show genuine free cash flow and some underlying profitability. But the outlook remains challenging and S4’s customer concentration continues to concern me. Today’s 2025 guidance is H2 weighted and broker forecasts suggest earnings could fall slightly this year. I see little attraction and think it’s sensible to remain cautious, despite the modest P/E. |

Science (LON:SAG) (£183m) | Full Year Results | Rev -2.3%, record PBT of £14.7m. Consultancy affected by market instability. Outlook: more buybacks. | AMBER/GREEN (Graham) No change to my stance here. Science has the hallmarks of a good consultancy business with excellent cash flow and a net funds position on the balance sheet. However, I think the investment in Ricardo has raised the stakes and the risks. I'll be surprised if they can resist spending more of their surplus free cash flow on Ricardo shares through the rest of 2025. |

Team Internet (LON:TIG) (£168m) | FY TU | Results delayed by audit. FY24 to be in line with revised exps. Rev -4%, adj op profit -3.3% to $44.2m. | |

Braemar (LON:BMS) (£85m) | TU | Profit warning. Rev c.£141m vs exp £152m. Adj op profit c.£16.5m vs exp £17.5m. Order bk $82.2m. | BLACK / (AMBER/RED) (Roland) Weaker cyclical conditions are putting pressure on chartering profits – the group’s core business. I don’t see anything seriously amiss here. But I think it makes sense to remain cautious at this point, given the risk of further downgrades. |

Quadrise (LON:QED) (£74m) | Interim Results | H2 net loss of £1.7m, cash of £7.1m end Feb post £6.5m placing. Trials underway. | |

Windar Photonics (LON:WPHO) (£41m) | TU | Record revenue +20% to €5.7m but €1.4m delayed sales. EBITDA to be c.€0.4m at lower end of expectations. But H1 2025 will be strong due to the rephasing of a 2024 order plus a new order for the US market. | AMBER (Graham) [no section below] This Danish hardware and software company (for wind turbines) raised £5.9m in December. I also note that NEDs have been paid with fresh equity in lieu of fees for their service in 2024. According to broker forecasts, the company will enjoy net cash from here on out, with revenues forecast to almost treble in 2025 and meaningful profits starting this year (adj. PBT €5.5m in 2025, rising to €9.3m in 2026). I will take these forecasts with a pinch of salt but am happy to take a neutral stance as the company should at least be funded for the foreseeable future. |

EnSilica (LON:ENSI) (£38m) | Contract win | Design and manufacturing services contract. Current and next two financial years. | AMBER/RED (Graham) [no section below] |

Insig Ai (LON:INSG) (£19m) | TU | SP up 8% Q3 revenue £131k. Q4 expected revenue £224k. Improving pipeline. Raises £350k at 16p. | RED (Graham) [no section below] It's a pleasant vote of confidence in this AI-powered financial analysis business, with a £350k fundraise including £150k from the CEO and £50k from the Chairman. The CEO also pledges a further £350k of fresh equity at a share price of 20p, to ensure working capital for the next 12 months. Revenue is picking up from an extremely low base. As this is still at an extremely early stage I'm staying RED on it, to reflect the very high risk that goes with early-stage businesses with limited funding available to them. |

Abingdon Health (LON:ABDX) (£14m) | Half-year Report | SP down 11% Rev £3.1m, negative adj. EBITDA. H2 weighting expected. Full-year revenue to be in line at £8.6m. CEO change: Exec Chairman takes on CEO responsibilities. Former CEO becomes President of US business. | RED (Graham) [no section below] This medical testing business is a serial loss-maker but it is growing thanks to an acquisition and contract wins. According to broker forecasts (which I note have been downgraded today), adjusted EBITDA will hit breakeven next year (FY June 2026) and then positive adj. EBITDA will be seen in FY June 2027. Cash as of Dec 2024 was £3.7m. Both the company and its broker say that according to forecasts, it does not need further funding and the company is keen to emphasise that its revenue expectations for the year are in line with expectations. However, the EBITDA downgrade is not highlighted to the same extent and suggests to me that caution remains the right approach here. The cash balance will fall from the current level and the margin for error might not be very wide. |

RTC (LON:RTC) (£14m) | Final Results | Rev £96.8m (LY: £98.8m). PBT £2.6m (LY: £2.5m). Solid order book. Cautiously confident. | AMBER/GREEN (Roland) [no section below] This recruitment group is building a niche supplying labour for infrastructure projects - e.g. smart meters and rail maintenance. This strategy delivered stable profits last year in a difficult market for recruiters generally. Free cash flow of £1.7m represents strong conversion from net profit and comfortably supports the 5% dividend yield. The outlook also seems reasonable. RTC shares are illiquid with a big spread, but I think they might be worth a closer look for micro cap investors. |

Tandem (LON:TND) (£9m) | Final Results | In line. Rev +11%, adj. PBT £0.5m. “Resilient”. 2025 has started well, in line with exps. | AMBER/GREEN (Graham) Leaving my moderately positive stance unchanged as it is objectively cheap against its balance sheet values and if operational leverage kicked in it would become very cheap against earnings, too. However, the previous management team failed to take the company to the next level of success and I don't know why it will be different this time. |

Graham's Section

Tandem (LON:TND)

Unch. at 172.5p (£9m) - Final Results - Graham - AMBER/GREEN

The Board of Tandem Group plc (AIM: TND), designers, developers, distributors and retailers of sports, leisure and mobility equipment, announces its audited results for the year ended 31 December 2024 ("FY24").

This company is now covered by Cavendish and so it can say that today’s results are in line with expectations.

2024 is an improved year with revenues up 11% to £24.6m and an adjusted PBT of £0.5m (previous year: loss of £1m). See my coverage of the full-year trading update in January.

Three of the company’s four segments saw double-digit revenue growth. Growth at the bike segment was “significantly outperforming the broader sector”. New eBikes have launched under Tandem’s own brands, with more on the way in H1 2025.

The only segment that shrank was a small one, Home & Leisure, where sales reduced from from £3m to £2.3m, “reflecting the effect of unfavourable weather conditions throughout key sales periods”. These periods included the Easter and Summer school holidays and the products affected were the likes of gazebos, outdoor furniture and parasols.

Management seem to be reasonably happy with the performance and with current trading, which is in line:

Amidst a difficult economic environment, there have been encouraging signs. The Group has delivered resilient performance during a period in which multiple industry participants have become highly distressed. The continued success of our initiatives and a strategic focus provide the Board with confidence for the future.

Despite ongoing market challenges and uncertainties, we are pleased to report that sales for 2025 have started well and are in line with the Board's expectations, marking an optimistic beginning to the current financial year.

For 2025 their “Toys, Sports & Leisure” division will benefit from partnerships with Wicked, Jurassic Park, Unicorn Academy, Hot Wheels and Superman. It already has Disney’s Stitch and BBC’s Bluey.

Adjustments

Unfortunately there are £0.5m of “non-underlying items”, pre-tax, which means that Tandem’s actual pre-tax profit for 2024 is only around breakeven.

The non-underlying items include various unexciting items such as “employment costs relating to the planned retirement of the Group's commercial director” and the scrapping of a new IT system.

Balance sheet

Net debt increased to £4.3m due to higher inventories.

Tangible net assets are £18.4m which I believe are largely accounted for by freehold property. Last year’s annual report showed freehold land and buildings worth c. £14m. Tandem owns its Birmingham warehouse/headquarters.

Estimates

Thanks to Cavendish for posting up estimates including 2025 revenue of £27.3m and adj. PBT of £0.5m.

No dividend has been declared or is forecast. Tandem last paid a dividend in 2023.

Graham’s view

I’m a little surprised the StockRanks rate this as a Super Stock:

In terms of value the main attraction is probably the balance sheet, with the large freehold property on its books.

However, that property isn’t worth anything if it’s not being used profitably and profits have been underwhelming at Tandem.

Readers may recall that I am a former shareholder of this company. I owned it for many years, eventually leaving it in frustration - I didn’t make a big loss, but I was frustrated that the company never seemed to achieve much despite being publicly listed for a very long time.

This stock has been listed for decades and never seems to achieve sustained success, despite making plenty of profits over the years. The only conclusion I can draw is that the former management team were very poor at capital allocation: the acquisitions and other decisions they made over the years did not translate into sustained growth in profitability.

Tandem have had a new CEO since May 2022 and a new Commercial Director/Chief Commercial Officer since July 2024.

I’m not tempted to get involved with this one again. The allure of classic bike brands drew me in originally, but the reality of being a small, barely-profitable importer of Chinese-built goods drove me out.

I will leave my stance at AMBER/GREEN as it is undeniably cheap - if operational leverage kicks in again at any point, the earnings multiple will collapse and it will look like a terrific bargain. And then if management were able to allocate earnings wisely, it could be a big winner. But previous management teams failed to do that, and I don’t know why it will be different this time.

Science (LON:SAG)

Up 1% to 415p (£186m) - Audited Results for 2024 - Graham - AMBER

I’ve been covering Science (LON:SAG) a lot recently in relation to its purchase of Ricardo (LON:RCDO) shares.

Let’s see how Science itself is doing:

Revenue down 2% to £110.7m.

Adj. operating profit £21.5m (LY: £20.5m)

PBT of £14.7m (LY: £7.6m) benefited from fewer adjustments.

Year-end net funds were nearly £27m but we already know this has reduced to £14m thanks to the investment in Ricardo.

Exec Chair Martyn Ratcliffe says:

Science Group plc is an international science & technology consultancy and systems organisation. In 2024, Science Group again demonstrated the resilience of its operating model and, in an unpredictable economic and political environment, the Group has delivered another year of record profitability…

He says “not only has the Ricardo shareholding produced a paper profit (in March 2025) since investment, but Science Group retains significant cash resources, enhanced by a new unused debt facility.” Once again, I think he is overemphasising the short-term movement in the Ricardo share price, and underemphasising the effect that Science’s buying may have had on the share price over the last two months.

Consultancy Services: “an international services business providing advisory, product development, regulatory and project management services”. These operations are now unifying under the “Sagentia” brand.

Revenues at this division fell in 2024, “reflecting the more challenging consultancy market”, and I think more of the same is anticipated in 2025 due to “the ongoing refocusing to higher value-add activities in the Defence sector”.

Systems Businesses: this has a submarine systems business and a business that supplies radio chips and modules. The submarine business had an excellent year in 2024, while the radio business returned to break-even.

Investment in Ricardo: I calculate that Science’s Ricardo shares are worth c. £26m at the latest share price. They say “a variety of options to enhance and/or realise value from the investment, over a short, medium or long time horizon, are open to Science Group and all options will be evaluated.”

Balance sheet: I note that Science has two freehold properties; they are held on the balance sheet at cost (£21m) but have been independently valued at an aggregate value “in the range of £16.9 million to £31.6 million”. That range seems extraordinarily wide to me - why could the valuer not provide a narrower range?

As of Dec 2024, tangible net assets were officially c. £43.6m (my calculations). With an unchanged dividend worth £3.7m, buybacks for possibly as much as £6m, and the potential for further purchases of Ricardo shares, the company has plenty of uses for its free cash flow.

Estimates: Canaccord Genuity suggest that 2025 will see revenue up slightly to £112m and adj. PBT of £21.8m.

Graham’s view

I can leave our AMBER/GREEN stance unchanged here as Science retains a number of attractive features from an investment point of view. One of the standout things I’ve noticed today is that Science’s cash flow statement shows positive cash flow from investing activities (very unusual), as no capex was required! So it did genuinely have the cash flow to pay for last year’s buybacks and dividends, with a large surplus left over to help it invest in Ricardo. This is what happens when a capital-light services business performs well.

The big question is whether this Ricardo investment makes sense. As I’ve said here before, I’m wary - I’m concerned that it might take up a large portion of management’s time and attention, and that in the long run it might be very difficult to make a success out of it.

Unlike corporate activity by Science in the past, Ricardo is a larger company where Science will not be able to buy it up in its entirety. It will have to deal with other shareholders and with a Board who have a greater ability to say No.

And if Ricardo is being so badly mismanaged, as alleged by Science, this poses the risk of degrading the investment thesis for Science itself. If you combine a good company with a bad company, you risk being left with something that’s half-way between the two. Unless Science can effect change, all we’ll be left with is a good company (Science) owning a very large stake in an allegedly bad company (Ricardo). That’s hardly an inspiring prospect.

I’m also not sure how much overlap really exists between the two of them - they are both diversified consulting groups with expertise in the industrial, environmental and energy sectors, but with very different points of emphasis. Perhaps Science would ultimately like to see a merger or takeover, boosting their own environmental and energy capabilities?

In summary, I don’t think there’s any need to change my stance on Science. I remain moderately positive on them, but much will hinge on their diplomacy skills when it comes to this strategic investment, and on their ability to keep their core business performing well in the midst of this distraction.

Roland's Section

Braemar (LON:BMS)

Down 9% to 237p (£78m) - FY25 Trading Update - Roland - BLACK (PW) / AMBER/RED

Braemar Plc (LSE: BMS), a leading provider of expert investment, chartering and risk management advice to the shipping and energy markets, announces a trading update for the year ended 28 February 2025 ("FY25" or "the year").

Today’s full-year trading update from shipbroker Braemar is a profit warning, although this is not obvious from the opening line of the RNS:

Braemar is pleased to report that the Group's balanced and diversified business model performed well, during the year, to deliver a robust overall trading performance for FY25.

Reading on, the company avoids stating explicitly that results will be below expectations, leaving readers to deduce it from the language. This isn’t helpful, in my view.

Fortunately, management has provided both previous and revised expectations within today’s RNS, so investors who read the footnotes can make an easy comparison without needing access to broker notes.

Here are the key numbers:

FY25 revenue guidance: “in the region of £141m” (previous consensus £152m)

FY25 underlying operating profit: c.£16.5m (previously £17.5m)

Today’s updated numbers are also below the equivalent FY24 results of £152.8m and £18.1m.

Braemar has had its problems in the past, but today’s commentary suggests to me that today’s downgrade is more likely due to cyclical weakness than any other issues (my emphasis):

Global charter rates, notably in the Tanker and Dry Cargo markets, came under pressure in the second half of the financial year, due to increased geopolitical volatility; however, the impact of this was partially offset by a strong performance in other parts of the Group such as Sale and Purchase

Operating cash flow is said to remain strong, but the company says working capital outflows meant year-end net debt was £2.5m, down from net cash of £3.3m at the half-year market. This situation is said to have reversed during March, returning the business to a positive net cash position.

Outlook: Braemar’s forward order book was $82.2m at the end of February, broadly unchanged from $82.6m at the end of February 2024. Fixture levels achieved last year are expected to be maintained this year.

The company warns of “short-term volatility” in its markets but is confident in the “longer-term prospects”. Such language is often a disguised way of warning of short-term weakness. This appears to be true here.

Consensus estimates on Stockopedia before today were for FY26 revenue of £154m. However, house broker Canaccord Genuity has downgraded its FY26 estimates quite significantly today:

FY26E revenue: -9.4% to £140.9m (prev. £155.6m)

FY26 adj EPS: -9.3% to 28.4p (prev. 31.3p)

Canaccord has also made similar cuts to its FY27 estimates, suggesting a broadly flat outlook over the next couple of years.

These estimates put Braemar shares on a FY26E P/E of 8 with a possible 6% dividend yield.

Roland’s view

CEO (and 3% shareholder) James Gundy says changes made in recent years have “diversified our revenue streams” and “reduced the impact of cyclical rate pressures”.

This may be true, but Braemar still generated 65% of revenue and 61% of underlying operating profit from chartering during the first half of last year. Weaker shipping rates will still hit the group’s profits.

Today’s update looks like cyclical weakness to me, with parallels to the weaker outlook provided by market leader Clarkson (disc: I hold) with its recent results.

Reduced broker estimates extend a run of FY26 downgrades that started nearly a year ago:

Braemar’s share price has also been falling in recent months:

At face value, Braemar shares don’t look expensive after today’s drop.

However, quality metrics are decidedly average – I wouldn’t want to pay a high multiple of (falling) earnings for this business:

This is a highly cyclical sector coming off a period of record earnings. I think it’s prudent to remain cautious at this point and consider the risk of further weakness. AMBER/RED.

S4 Capital (LON:SFOR)

Up 10% to 36p (£224m) - 2024 Full Year Results - Roland - AMBER/RED

Full year results in line with expectations

Investors appear relieved that today’s results from Martin Sorrell’s digital advertising group S4 Capital are in line with expectations. This stock became overhyped during the pandemic boom and has since fallen by 95%:

Do today’s results signal that the bottom is in and that value may be emerging? I can see some positive signs, but I still have some concerns about the investment appeal of this business. Let’s take a look.

2024 results summary: S4 Capital’s results are heavy on adjustments but show a significant reduction in customer fee income (net revenue) over the year:

Billing up 4.9% to £1,963m (includes pass-through costs)

Net revenue down 13.6% to £754.6m (-11% LFL)

Adjusted operating profit -4.5% to £78.3m

Adjusted earnings up 18% to 5.2p per share

The company is heavily dependent on clients in the technology sector, who contributed 45% of revenue last year (FY23: 43%). Unfortunately these clients have dialled back their marketing spend to focus on AI:

Technology clients continue to focus spending on AI-related capital expenditure, rather than operating expenditure, such as marketing.

As Megan highlighted in November, S4 has also lagged larger rivals in the advertising and marketing sector:

There was also some underperformance, when compared to our markets.

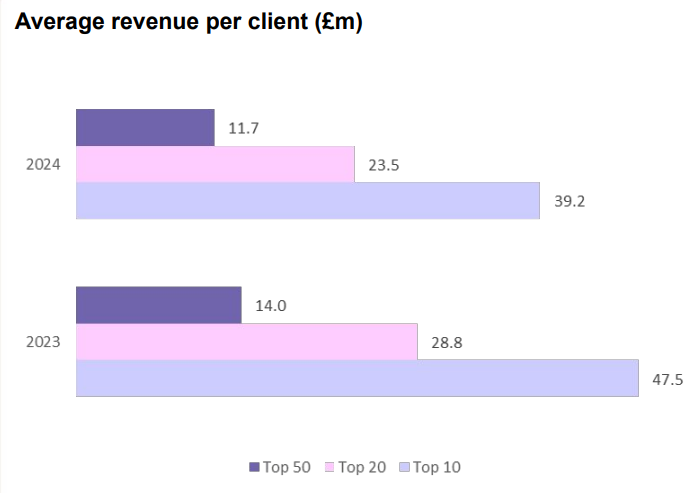

The reduction in revenue per client is highlighted in this chart from today’s management presentation:

Profitability: the company’s adjusted operating profit of £78.3m implies a margin of 10.3% for the past year.

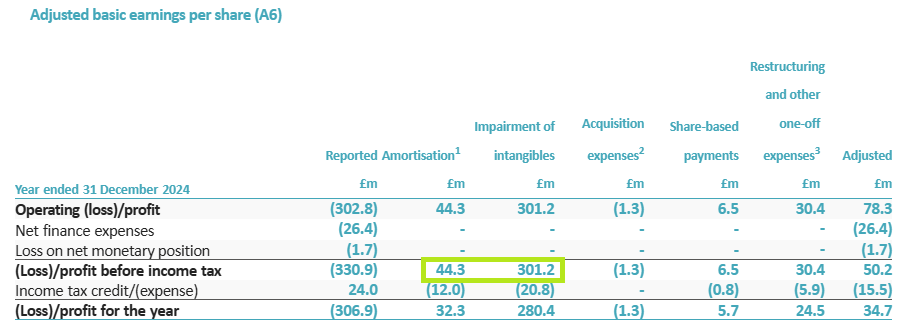

However, I can’t completely overlook £381.1m of adjusting items. These include a £301m impairment charge relating to past acquisitions, which are presumably no longer expected to deliver the hoped-for returns:

The most charitable view on profits I can get comfortable with is to ignore the impairment charge and also £44m of amortisation relating to acquired intangibles. The remaining adjustments look like real operating expenses to me.

Taking this approach gives me an adjusted operating profit of £42.7m, implying a margin of 5.7%.

My comfort with this estimate is increased because it’s also close to the group’s 2024 free cash flow of £37m.

This free cash flow supported a useful reduction in net debt to £142.9m last year (FY23: £180.8m). I estimate net debt/EBITDA leverage is now reduced to 1.6x, from 1.9x at the end of 2023.

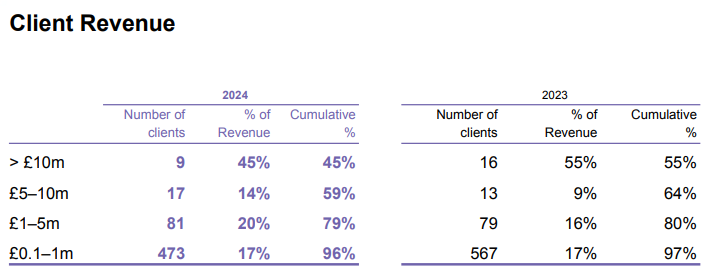

Customer concentration: Megan has previously flagged up S4’s customer concentration as a significant risk for investors. This remains the case – the company’s largest client contributed £148.1m of revenue last year (c.17.5%) and the top nine clients contributed 45% of revenue.

Frustratingly, the data in the chart below is presented in such a way as to make it difficult to compare customer concentration versus last year. I think we might wonder if this obfuscation is deliberate – it would have been more useful to compare revenue generated by top 10 clients in each year:

Outlook: the company says net revenue and operational EBITDA are expected to be broadly similar in 2025. The first quarter is expected “to be difficult” with an H2 weighting to profits.

Net debt is expected to reduce further to between £100m and £140m, targeting leverage of 1.5x operational EBITDA.

Dowgate Capital have provided updated estimates today suggesting adjusted earnings could fall by 7.7% to 4.8p per share this year, before recovering in 2026. This prices the stock on FY25E P/E of 7.5x.

Roland’s view

Today’s commentary makes repeated mention of a reduction in spending by key technology clients. For me, this highlights one of the risks of this business.

In an era of digital advertising and marketing, spending can be rapidly and continuously adjusted to suit business requirements. I worry this may leave S4 Capital and some others in this sector as middlemen, with limited control over their performance.

The company was at least profitable last year, at both a free cash flow and (reasonable) adjusted level.

I can see the argument that when external conditions improve, operating leverage could drive a sharp improvement in profitability. That could justify a further re-rating.

However, today’s H2-weighted guidance and updated broker forecasts suggest profits will remain under pressure this year. Given the group’s poor track record and limited profitability, I’m inclined to remain cautious.

Megan was RED on this in November. I think today’s results justify a slightly more positive view than this, so I’m going to step up a notch to AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.