Good morning and welcome to today's report.

Spreadsheet accompanying this report: link.

08:30 Agenda is complete.

13:50: today's report is now complete.

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

GSK (LON:GSK) (£58bn) | FDA has approved a prefilled syringe presentation of Shingrix, simplifying vaccine administration. | ||

Diageo (LON:DGE) (£42bn) | CEO departure and succession plan (y’day pm) | Debra Crew has stepped down with immediate effect and is thanked, CFO Nik Jhangiani is interim CEO. | |

SSE (LON:SSE) (£20.4bn) | Renewable output -4% due to weather, capex +70% to £0.5bn YoY. Financial guidance unch. | ||

Wise (LON:WISE) (£14.1bn) |

SP -10% FY26 guidance unchanged for 15-20% underlying income growth. | AMBER (Roland) Today’s Q1 update has triggered a c.10% share price drop and appears to show a slowdown in growth relative to last year. Underlying income growth during the first quarter was slightly below the company’s FY26 guidance as well, although this was left unchanged today. I don’t think there’s anything serious to worry about here and believe the long-term growth story remains intact – and potentially very impressive. However, Wise shares are trading on c.30x earnings in a sector where mishaps are not unprecedented. The company is also about to move its primary listing to the US. I’m going to maintain our neutral view. | |

Diploma (LON:DPLM) (£6.58bn) |

YTD total rev +12% YTD organic revenue growth +10% YTD acquisition revenue +4% FY25 outlook: FY organic revenue growth now expected to be 10% (prev 8%). | AMBER/GREEN (Roland) [no section below] I’m relieved to see I took a moderately positive view on Diploma when I reviewed its interim results in May. Today’s Q3 update includes upgraded revenue growth guidance for FY25, emphasising the contribution from organic growth while flagging up two recent bolt-on acquisitions totalling c.£39m. Diploma shares never look cheap and now trade on a P/E of c.30x FY25 earnings. But this is a well-run and high-quality business, in my view, and I am happy to maintain my previous view today. | |

Frasers (LON:FRAS) (£2.90bn) | FY25 rev -7.4%, adj PBT +2.8% to £560.2m. FY26: expect £50m extra costs, adj PBT £550-600m. | ||

RS (LON:RS1) (£2.74bn) | Q1 LFL rev -2%. EMEA trading softer, Americas and AsiaPac “more resilient”. FY outlook unch. | ||

Qinetiq (LON:QQ.) (£2.64bn) | Q1 order book c.£5bn, FY revenue cover 75%. Cost savings on track, trading in line, H2 weighting. | ||

Dunelm (LON:DNLM) (£2.3bn) | FY sales +3.8% to £1,771m, gross margin +0.6%. Furniture strong. FY PBT to be in line at c.£210m. | ||

Big Yellow (LON:BYG) (£1.79bn) | Rev +3%, rent/sq ft +5% YoY and costs stable. LFL occupancy +0.7% to 79.4% vs March 25. | ||

Premier Foods (LON:PFD) (£1.68bn) | Rev +0.3%, branded sales +1.2%. Sweet Treats branded +11.4%. FY26 profit exps unchanged. | ||

Coats (LON:COA) (£1.3bn) | Results of Capital Raise, Acquisition (y’day) & interim results (y’day) | H1 rev flat, adj op profit +5% to $140m. FY outlook unch. Acquiring OrthoLite insoles for $770m (10x EV/EBITDA). Part-funded using £250m (20%) placing, completed at 77p. | AMBER (Roland) Coats’ half-year results look fine to me, given the impact of tariff uncertainty and softer conditions in some markets. I’m confident the group’s core business is likely to remain a market leader and would probably have remained moderately positive, without the acquisition. However, the purchase of Ortholite looks a little expensive to me and seems to depend on a three-year programme of cost savings to deliver any meaningful margin benefits. Although the shares are now trading below last night’s placing price of 77p, I am not tempted to jump in given the execution risk commonly seen in larger acquisitions. |

FUTR (CVE:FTRC) (£742m) | US advertising +5%, UK ads -8%. Go.Compare slowed. On track to achieve FY25 market exps. | ||

IP (LON:IPO) (£511m) | Istesso has published results showing tissue repair using an oral medicine for the first time. | ||

NCC (LON:NCC) (£446m) | Sale process for Escode is continuing. Confirms that Cyber business is now also under review. | ||

Funding Circle Holdings (LON:FCH) (£404m) | Credit extended up 21% to £1.1bn, balances of £2.8bn Credit perf in line. Medium-term guidance unch. | ||

DFS Furniture (LON:DFS) (£386m) | FY adj PBT to be slightly ahead of guidance for £25-29m. H2 order intake +10% YoY. | ||

Ashtead Technology Holdings (LON:AT.) (£363m) | PW: H1 pro-forma revenue -6% to c.£99m, adj EBITDA margin c.27.3%. FY adj EBITA now to be “modestly below” exps, but FY adj PBT exps unch. | BLACK | |

Gore Street Energy Storage Fund (LON:GSF) (£322m) | NAV -4% to 102.8p (£519m), NAV Total Return +1.1%. FY operating revenue £35.3m, EBITDA £21m. Outlook: 0.75p quarterly dividend +3p special in H2 2025. | ||

RTW Biotech Opportunities (LON:RTW) (£317m) | “Hengrui Pharma, announced positive topline data from the China Phase 3 clinical trial of HRS9531 in individuals living with obesity or overweight. The trial met both primary endpoints, demonstrating superior weight loss and a greater percentage of participants achieving at least 5% body weight reduction compared to placebo. The safety profile was favourable and consistent with other GLP-1-based treatments…” | ||

Helical (LON:HLCL) (£274m) | “We continue to deliver on our strategy of developing best-in-class buildings in highly desirable central London locations, with further progress made across our three office schemes totalling over 460,000 sq ft, all of which are due for completion in 2026.” | ||

SolGold (LON:SOLG) (£206m) | Advancing early development activities, including securing project funding, drilling, and preparing for the commencement of long-lead construction works. Cascabel Copper-Gold Project in northern Ecuador. | ||

Capital (LON:CAPD) (£168m) | Q2 Revenue -2% y-o-y to $87.4m but +22% on 25Q1. Group revenue guidance increased to $320 - 340 million and MSALABS revenue guidance increased to $55 - 65 million (up from $300 - 320 million and $50 - 60 million, respectively. | AMBER (Mark) This is the first genuinely positive statement for a while from this company. However, the share price has been strong recently and on any near-term forecasts, this looks expensive. Today’s upgrade shows that there may be considerable scope for the 2026 estimates to be beaten. The discount to TBV means that there is upside if these assets can be made productive again. I’m keeping the neutral view for the moment, though. | |

Eurasia Mining (LON:EUA) (£146m) | Dual listing has been successfully completed. | ||

Avacta (LON:AVCT) (£126m) | 10,833,333 new shares at a price of 30p. 13% discount to last night's close. Net proceeds of approximately £3.1 million used to settle the July quarterly repayment of the unsecured convertible bond. | ||

Diaceutics (LON:DXRX) (£102m) | “The expanded agreement is expected to contribute incremental service revenue in FY2025 and further strengthens Diaceutics' position as a strategic partner in the precision medicine ecosystem.” | ||

Pharos Energy (LON:PHAR) (£87.3m) | 1H production 5,642 boepd net vs 2025 production guidance of 5,000 - 6,200boepd. H1 Revenue flat at $65.3m, net cash $22.6m (31 Dec 2024: $16.5m), Capex guidance unchanged at $33-40m. | ||

Ilika (LON:IKA) (£80.5m) | “continues to develop and commercialise its two solid state battery product lines: Stereax® batteries for miniature medical devices and wireless sensors for specialist applications, and large format Goliath™ batteries for electric vehicles and consumer appliances.” | ||

Churchill China (LON:CHH) (£63m) | PW: “hospitality markets remain challenging with reduced demand for our product, particularly in export. Following a late Easter, April performance was broadly in line, however, the financial performance in May and particularly June was materially below target, meaning that the Company will deliver profitability significantly below last year at the half year…will deliver revenue and profits for the full year significantly below the prior year.” | BLACK/AMBER (Mark) | |

Zephyr Energy (LON:ZPHR) (£63m) | Zephyr continues work to deliver the first stage of gas infrastructure for the Paradox project. | ||

KEFI Gold and Copper (LON:KEFI) (£50m) | Successful implementation of our plans will result in Tulu Kapi commissioning gold production in late 2027. | ||

Iofina (LON:IOF) (£50m) | Produced 305.5 MT of crystalline iodine in 25H1, +10.6% on H1 2024 (276.1 MT). slightly higher than revised production guidance for the Period of c.300 MT. 25H2 production to be in the range of 400-440 MT. Spot price firmly above $70/kg and is expected to stay at these levels for the foreseeable future. | ||

Audioboom (LON:BOOM) (£46.2m) | HY Results, Acquisition & Placing (y’day) | H1 Revenue +3% to $35.1m. Adj EBITDA $1.8m, (24H1:$0.3m). PBT $1.3m (24H1:$1.3m loss). Acquisition of Adelicious, a UK focused podcast network for up to £10m (£4.5 million initial consideration, to be settled 60% in cash and 40% in new Ordinary Shares + up to £3.0 million of deferred consideration, + Up to £2.5 million of contingent consideration.) Funded via £3m placing at 270p (6.8% of the share capital at 3.9% discount) | |

Artisanal Spirits (LON:ART) (£35m) | Adj. EBITDA performance in H1-25, broadly in line with the prior year loss of £1m. | ||

Majestic (OFEX:MCJ) (£25m) | Planned launch of a new 50,000 sq. ft. facility in Wrexham, Wales, integral to the strategy to increase the annual volume of processed materials to 100,000 tonnes by 2030. | ||

Transense Technologies (LON:TRT) (£24m) | Revenue +33% to £5.6m, Adj. PBT +8% to £1.6m, Net cash £1.1m (FY24: £1.3m). “well placed to deliver further growth in the upcoming financial year” | ||

James Cropper (LON:CRPR) (£22.5m) | Revenue -4% to £99.3m, flat adj. EBITDA, Adj. PBT +77% to £1.3m, Net debt -17% to £12.9m. Trading in the first quarter was ahead of the Board's expectations and at a similar level to the strong start recorded in FY25. | ||

Renalytix (LON:RENX) (£22m) | “Through this partnership, MVP and Renalytix will collaborate with physician groups across MVP's network, with the goal of introducing and implementing kidneyintelX.dkd advanced risk assessment testing.” | ||

Blencowe Resources (LON:BRES) (£13m) | Successful completion of its Stage 7 drilling program at the Orom-Cross Graphite Project in Uganda | ||

Westminster (LON:WSG) (£11.7m) | Extension of contract to provide a Parliamentary Broadcast System for the parliamentary debating chamber of an East African Parliament for an additional £1.15 million. Expected to be largely, if not completely, delivered in the current financial year. | ||

Argentex (LON:AGFX) (£3.3m) | Individual Liquidity Guidance Company expected that the Individual Liquidity Guidance would be satisfied via the provision of an additional secured Revolving Credit Facility, but has not been able to secure that additional funding, nor does the Company have any other source of alternative funding or liquidity. Argentex LLP is not able to operate. Ordinary Shares suspended. | RED (Mark) [No section below] This sounds terminal, and even the paltry 2.49p takeover over that looked like a done deal is now in doubt. How this could have gone so badly wrong is a cautionary tale that probably deserves to be written once the dust has finally settled. |

* Market caps at previous trading day’s close

Roland’s Section:

Wise (LON:WISE)

Down 10% to 1,024p (£10.5bn) - Q1 FY26 Trading Update - Roland - AMBER

Strong start to the year with continued cross-border volume and customer growth

Today’s first-quarter update has met with a downbeat reception despite seemingly strong growth in volumes during the first quarter.

My guess is that today’s share price drop means that growth was less strong than hoped – or that investors are disappointed at the sharp drop-off in the company’s take rate (essentially its fee margin).

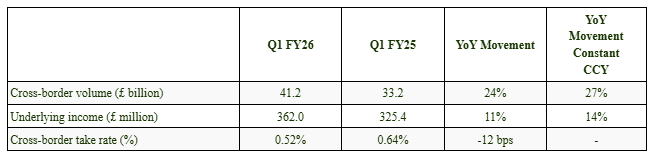

Q1 trading update - here are the key stats:

One other key metric not included in this table is customer growth:

Active customers in Q1: 9.8m (+17% YoY).

Looking at these individually and comparing growth rates to last year suggests a mixed picture to me, with a possible miss on underlying income:

Cross-border volume: 24% growth seen during Q1 is consistent with the 23% growth rate reported last year.

Active customers: this figure rose by 21% in FY25, split between Personal (+22%) and Business (+11%).

Drilling down into today’s increase of 17%, personal customers rose by 17% in Q1, while the number of business customers rose by 15%.

Personal customers still account for the majority of transactions and currency volumes, so this represents a slowdown in growth versus last year.

Underlying income (adjusted revenue): the slower rate of growth in personal customers is reflected in underlying income, which rose by +14% in constant currency. This is below the 16% rate achieved last year.

On a constant currency basis, these Q1 figures are also slightly below the 15-20% constant currency growth rate guidance included in last year’s results.

However, today’s update reiterates that this target is unchanged:

Continue to expect strong growth in underlying income in FY26, in line with our medium-term guidance of 15-20% on a constant currency basis

One quarter does not make a year and I don’t see today’s slight miss as a major concern. But perhaps it’s worth monitoring. Underlying income may also not be the truest measure of total income growth here.

The reason for this is that the underlying income metric is intended to represent the income that will be retained from customers. This includes the first 1% of any interest income earned on customer balances and any interest expense incurred.

The logic here is that Wise would like to pay surplus interest over 1% to its customers, but as I understand it does not always have the regulatory licences required to do so. Hence some of this cash is actually retained.

Last year’s results show the contrast between underlying income and real income:

Reported gross profit (includes all interest income): £1,307.8m

Underlying gross profit (includes 1% yield only): £1,025.1m

Lower interest rates could reduce this additional net interest income. Even so, I think it’s reasonable to assume that actual FY26 income and gross profit are again likely to be significantly higher than the underlying figure.

Cross-border take rate (%): Wise has always been open about its policy of passing economies of scale and other savings onto its customers. It’s probably also fair to say this is a competitive sector where cutting fees to support a land grab makes sense.

The Q1 drop of 12 basis points (0.12%) seems high, but this is a year-on-year figure and most of the reduction took place last year.

Checking back, the Q4 FY25 take rate was 0.53%, so there was only a 1bps sequential reduction in the take rate in Q1.

Outlook: Wise is perhaps taking a leaf out of the Amazon playbook by deliberately not trying to maximise its margins. Last year’s results showed an underlying pre-tax profit margin of 21%. However, the company’s medium-term guidance is for an underlying PBT margin of 13-16%, as it focuses on expanding market share and offering the most competitive pricing for its customers.

Today’s update reiterates this guidance and previous comments that FY26 margins are “expected to be around the top of this range”.

Roland’s view

I have been impressed by Wise since its 2021 IPO and remain so – this looks to me like a business with the potential to become a true platform, with massive scale and market share.

However, it’s fair to point out that in the UK at least, some companies in the currency transfer/FX sector have ended up running into problems periodically. So perhaps a measure of caution is prudent.

Wise was trading on c.30x forward earnings prior to today and 10x book value – so not exactly cheap. Even so, this relative reticence among UK investors seems to have persuaded Wise’s Board to shift its main listing to the US, leaving the UK with a secondary listing only. This plan was flagged up again today:

Last month we also announced our proposal to dual list our shares in the US and the UK, with the strategic and capital market benefits positively received by Owners. We believe the addition of a primary US listing will help us accelerate our journey to becoming 'the' network for the world's money, and ensure our mission and the interests of our customers and Owners remain deeply aligned over the long term.

Graham and Megan have both taken a neutral view of Wise at various points this year. Given that today’s growth rate appears to be at the lower end of guidance and the company is planning to move its listing abroad, I’m going to leave this view unchanged. AMBER

Coats (LON:COA)

Down 11% to 72p (£1.2bn) - Half-Year Report, Acquisition, Capital Raise - Roland - AMBER

Coats is a 250-year-old British business that’s one of the world’s leading suppliers of industrial thread for a wide range of applications, notably footwear and apparel.

The last 24 hours have seen a barrage of news flow from this business. Shortly after markets closed last night, Coats released its interim results and announced the $770m acquisition of insole specialist Ortholite and a £250m equity placing.

This morning we have confirmation that the placing completed at a moderate discount. However, investors seem to have taken a cautious view on either Coats’ results or the Ortholite deal. The firm’s share price is currently below last night’s placing level of 77p. This means that investors have the opportunity to buy shares below the level at which institutional shareholders were willing to invest last night.

Let’s try and unpick some of this news to see whether this situation could represent an opportunity.

Half-Year Results

These results cover the six months to 30 June 2025 and do not seem to flag up any serious concerns.

While sales growth was sluggish, profits were up and show an attractive level of profitability, suggesting Coats products are valued by its customers and carry a certain level of pricing power:

Revenue flat at $705m (+2% at constant exchange rates)

Operating profit up 6.4% to $128.4m

H1 operating margin: 18.2% (H1 24: 17.1%)

Adjusted EPS up 4% to 4.7c

Net debt down 6% to $501.5m

Net debt is a little higher than I’d like, but still within reasonable limits, in my view.

Divisional results

Apparel: revenue rose by 3% to $381m on a constant currency basis. This translated into an adjusted operating profit of $78m (+11%), giving a margin of 20.5%.

Coats says that demand softened in Q2 due to uncertainty around US tariffs, with Q3 expected to be similar and Q4 potentially stronger.

Pricing and a more favourable mix supported improved margins despite these headwinds and Coats believes it is continuing to gain market share.

Footwear: revenue rose by 1% to $199m. This dropped through to an unchanged adjusted operating profit of $48m and unchanged margin of 24.1%.

Again, management comments on softer demand due to US tariff uncertainty but believe that Coats strong relationships and market share will protect its longer-term position.

Growth rates are expected to improve to 7-9% CAGR over the medium term, outperforming the wider market thanks to “market share gains and organic expansion into adjacencies”.

Performance materials: revenue fell by 2% to $125m, leaving adjusted operating profit up by 4% at $14m. As a result, operating margin improved to 11.1% (HY 24: 10.6%).

This division provides treads used in PPE and composite products for telecoms/energy markets. The weaker revenue resulted from slower demand in Telecoms.

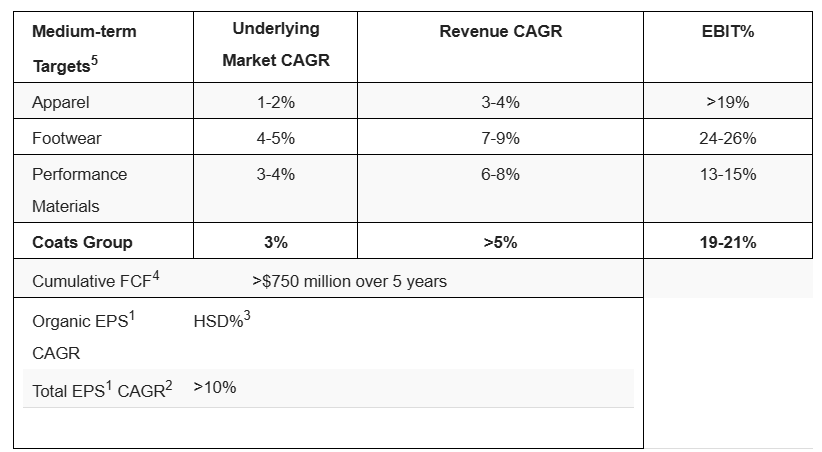

Medium-term expectations: looking into the future, Coats provides this useful table summarising its growth expectations for these three divisions:

Outlook

Management comments here seem clear and quite reassuring.:

The Group's full year outlook remains unchanged and is in line with current market expectations with a balanced weighting between first and second half trading overall.

With the stock trading on c.12x forward earnings prior to last night’s acquisition/today’s drop, I don’t think these results explain today's fall. Let’s move on to look at the acquisition.

Acquisition & Placing

Coats is buying US firm Ortholite Holdings LLC for an enterprise value of $770m. In addition to this, there will be a potential $10m earn-out payable based on FY25 EBITDA performance and a 5% royalty to Ortholite’s former owners on future sales of the new Cirql technology over the next five years. I have no idea whether this is likely to be a material amount.

Ortholite is described as the global market leader in premium insoles.

This acquisition is seen as a “compelling strategic fit” to help Coats become a “super tier 2” supplier of footwear components. I assume Coats and Ortholite have some customers in common, allowing them to gain a greater share of customer spend and perhaps achieve more favourable terms.

Valuation: we are told that Ortholite generated revenue of $258m and an adjusted EBITDA margin of 28% in calendar 2024. This translates to adjusted EBITDA of $72m.

That gives an EV/EBITDA valuation multiple of 10.7x, although management imply that further growth so far in 2025 has reduced this multiple to 10x.

Expected cost savings are expected to give a pro forma EV/EBITDA multiple of 8x based on $20m of cost savings to achieved by 2028. Personally, I am always very wary about relying on such assumptions, especially when they are going to take three years to realise.

Coats says that it expects the return on invested capital from this acquisition to exceed the company’s weighted average cost of capital by 2028 (i.e. probably not before). Similarly, operating margin gains of c.2% are not expected to be achieved until 2028.

On balance, this deal seems a little pricey to me, although perhaps not outrageous on a longer-term view.

Funding: Coats raised c.£250m in a placing at 77p last night. The remaining c.£340m required will come from new debt facilities with the company’s existing lenders.

As a result, the enlarged group’s net debt to EBITDA ratio is expected to be 2.2x at the end of 2025, falling below 2.0x by the end of 2026.

Roland’s view

I can see some logic in this deal.

But I can’t help feeling that in their ambition to take a step up in scale, Coats’ management are paying a fairly full price for Ortholite.

Personally, I can see why Coats shares are down today. While this deal could work out well in the long-term, in the near term it looks a little expensive and will result in elevated leverage. In my view, there is also some this deal may end up dragging on Coats’ near-term margins and returns on capital.

More broadly, large acquisitions always carry integration risk and do not always add up to more than the sum of their parts.

I think the Coats’ core threads business is proven and attractive, especially now that its historic pension liabilities have been resolved. But given the scale of this deal, I’m going to take a neutral view until we know more.

Mark’s Section:

Churchill China (LON:CHH)

Down 28% to 416p - Trading Update - Mark - BLACK/AMBER

It is a nasty profits warning here, with the company now guiding revenue and profits for the full year significantly below the prior year. Previous updates at the time of AGM and Final Results reported tough hospitality markets and did not specifically mention expectations so this should not perhaps be surprising that they have had to adjust expectations. However, the scale of the recent drop appears to have caught them by surprise:

Following a late Easter, April performance was broadly in line, however, the financial performance in May and particularly June was materially below target, meaning that the Company will deliver profitability significantly below last year at the half year. Whilst UK and USA sales have been robust, European and Rest of the World sales are tracking behind last year. The German market, in particular, has been difficult.

It has also caught shareholders by surprise, as the stock had rallied some 50% off the lows at one point. I had some inkling that the risk had increased and made a minor downgrade to our view following their AGM statement, where I said:

It’s a relatively short statement with little detail. To me it reads quite downbeat, perhaps understandably given the market backdrop. The shares have rallied quite strongly recently, together with many small caps. However, with little sign of any improvement in trading to match the 25% rise in share price, and a middling StockRank, I think this is now more of an AMBER/GREEN.

With hindsight, I wasn’t cautious enough. “Significantly” and “materially” tend to mean at least 20% in market speak. EPS was previously forecast to be flat in 2025, so taking 25% off that would now be around 44p:

We are largely flying blind here as there is no research available to us on Research Tree.

The company’s actions are what we would expect in this situation - cost cutting:

Capital projects initiated in the first half, focussed on increasing agility and improving our cost base are now broadly complete. We have also identified capital projects to pull forward to further reduce our cost structure. New product introductions, utilising inkjet and pressure cast, are being accelerated to restore growth exploiting our investment in these processes. We continue to review our cost base on an ongoing basis whilst being mindful of retaining skills required for growth.

However, I think that last sentence is important. In a downturn, shareholders often want a company to slash their costs to maintain profitability. However, shareholders like businesses that have a long-term mindset, as this tends to generate higher shareholder value. These two often conflict. It can be expensive to let experienced, long-term employees go in a downturn. Yet, if companies take no action and a downturn lasts longer than expected the extra costs can imperil a company’s survival. This is why many investors like companies with net cash, even though it is tax-inefficient. Churchill follows the more conservative route:

However, that net cash has been declining. The company increased its dividends in 2024, but this was paid out of balance sheet cash not free cash flow. It may not be as bad as it looks as 2024 turned out to be a year where working capital increased by around £5.3m:

The big questions are if that working capital will reduce due to the downturn in trading, and how big the capital projects that are being pulled forward are. They recognise that cost-saving often comes with a short term capital cost. Given the cash balance, the current dividend looks safe for another year, but perhaps not much longer if we don’t see an improvement in trading. In this update they say:

We continue to prioritise a healthy cash balance which we intend to retain. We expect our markets to recover in the medium term and see no change to the long-term potential of the business.

Which suggests that they won’t be going into debt purely to keep the dividend payout.

Mark’s view

The recent market enthusiasm for this stock has clearly been misplaced and the sell off today reflects that disappointment. However, this remains a conservatively-run cyclical business that is doing the right thing in very difficult conditions for the hospitality market. Until we have access to updated forecast numbers it is hard to judge whether today’s sell-off is an underreaction or an overreaction. One thing that is worth noting is that the company is back trading at a discount to TBV, which can indicate good value for investors that are willing to take the long-term view. However, the short-term outlook looks to be for no recovery, and with the most recent month’s trading being the worst the risk is that it declines further. It would seem to be a brave (foolhardy?) new investor who jumps in today. After all, the share price is close to the level it was trading at in April, and trading is materially below what the expectations were then. The Stockopedia research suggests that the share price will be weaker for sometime on such bad news. However, I can also see existing holders who bought for an eventual recovery being reluctant to sell at a discount to TBV due to a short-term setback. A large spread means that this is not a stock to be jumping in and out of regularly. AMBER feels the best balance between value and outlook.

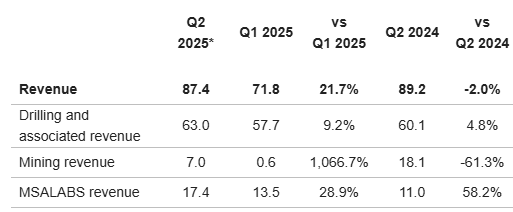

Capital (LON:CAPD)

Up 2% to 87p - Q2 2025 Trading Update & Increased Guidance - Mark - AMBER

The increase in guidance here is relatively minor:

Increasing 2025 Revenue Guidance: Group revenue guidance increased to $320 - 340 million and MSALABS revenue guidance increased to $55 - 65 million (up from $300 - 320 million and $50 - 60 million, respectively, as originally guided at our FY24 results);

But when your broker consensus looks like this, any increased guidance is good news!

his is driven by a recovery in Q2 results versus Q1, with expected momentum to continue into Q3. However, the revenue is still below Q2 last year. However, looking at the breakdown there is a significant variation between BUs:

MSALABS continues to grow very strongly, and drilling revenue is higher. Driven by small improvements in both utilisation and rates:

· Fleet utilisation for the quarter increased to 74%, from 73% in Q1 2025 and from 72% in Q2 2024. Utilisation remains broadly in line with our target rate of 75% across the fleet; and

· Average monthly revenue per operating rig ("ARPOR") was $198,000 in Q2 2025, up 8.8% on Q1 2025 ($182,000) and down 4.3% on Q2 2024 ($207,000).

The improvement in performance has largely been driven by management changes at their underperforming US operations. Something the CEO fell on his sword for, and founder and Executive Chair Jamie Boyton has stepped in to sort out.

Mining is still down significantly, but this reflects the redeployment of their fleet from Sukari in Egypt and Belinga in Gabon to the Reko Diq mine in Pakistan. This fleet is now with a long-term customer and mining revenue should be ramping up here, eventually reaching previous levels.

As expected in a strong gold price environment, their equity portfolio is very strong:

The total value of investments (listed and unlisted) was $49.5 million as at 30 June 2025 up from $30.3 million as at 31 December 2024, with the portfolio recording investment gains (realised and unrealised) of $20.3 million in H1 2025;

However, they have written down their Eco Detection stake, and the clock is ticking for their option on the Predictive Discovery takeover that expires at the end of the year.

Mark’s view

This is the first genuinely positive statement for a while from this company. I had sold out recently as this has never been a highly rated company due to its capital-intensity (pun intended!), the share price had been unusually strong and on any near-term forecasts, this looks expensive:

However, this may yet prove to be a mistake, as today’s upgrade shows that there may be considerable scope for the 2026 estimates to be beaten. The discount to TBV means that there is upside if these assets can be made productive again. I’m keeping the AMBER view for the moment, though.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.