Good morning - today's updates are thankfully more exciting than yesterday's!

1.30pm: we're out of time, thanks for dropping in!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Unilever (LON:ULVR) (£117bn) | Final Results | 2025 outlook: sales growth 3%-5%. Subdued growth in near term, to improve during the year. | AMBER/GREEN (Graham) |

Relx (LON:REL) (£76.4bn) | FY24 Results | 2025 outlook: another year of strong underlying growth in revenue and adj. operating profit. | |

British American Tobacco (LON:BATS) (£74.7bn) | Final Results | 2025: regulatory, fiscal headwinds. Committed to 3-5% rev growth, 4-6% adj. profit growth in 2026. | AMBER/GREEN (Graham - I hold) A large shock in terms of the Canadian class action lawsuit, and competitive pressures. But it still offers amazing cash generation despite its various problems. |

| Barclays (LON:BARC) (£44.3bn) | Final Results | 2025 guidance: RoTE c. 11%, progressive capital returns, £0.5bn efficiency savings, CET1 13-14%. | |

South32 (LON:S32) (£7.8bn) | HY Report | FY25 production guidance unchanged, except for aluminium in Mozambique (civil unrest) | |

Tate & Lyle (LON:TATE) (£2.8bn) | TU | Mild profit warning: rev mid single digit % lower, EBITDA growth at low end of 4%-7%. | |

Renishaw (LON:RSW) (£2.6bn) | HY Report | Rev +3%, EPS +2%, dividend flat. FY rev exp. £695-735m, Adj. PBT £105-135m. | AMBER/RED (Mark) |

Applied Nutrition (LON:APN) (£372m) | TU | Rev £47.6m ahead of £46m IPO guidance. EBITDA margin in line. | AMBER/RED (Graham) We have a new sports nutrition stock to look at and today's update is positive, beating revenue expectations set out at the IPO. At this early stage in its life as a listed company, I maintain scepticism. |

| Concurrent Technologies (LON:CNC) (£163m) | Commencement of trading on OTCQX | Trading under the ticker COTGF in the US. Will continue to trade on AIM too. | AMBER (Graham) I like dual-listings and a combined AIM/OTCQX listing for CNC strikes me as a positive step. This ambitious company is enjoying very strong share price momentum, and it has strong business momentum to help back this up. |

Avingtrans (LON:AVG) (£119m) | Contract Win | Booth Industries £4.5m contract win. | AMBER (Mark) |

Trifast (LON:TRI) (£104m) | TU | Expectations unchanged. |

AMBER (Mark) |

Ondo InsurTech (LON:ONDO) (£48m) | TU | Rev +70% to £4.5-5m. EBITDA +ve in FY26H2. | AMBER (MARK) |

Gattaca (LON:GATC) (£22m) | TU | In Line. NFI down 3% to £18.8m. Adj PBT £3m. Net Cash £16.7m. |

GREEN (Mark - I hold) |

Thruvision (LON:THRU) (£8m) | TU & Strategic Update | PW. £5 to £6 m vs prev. guidance of £9 m | RED (Mark) [no section below] |

Graham's Section

British American Tobacco (LON:BATS)

Down 7% to £31.40 (£69.4bn) - Final Results - Graham - AMBER/GREEN

At the time of publication, Graham has a long position in BATS.

The market dislikes these results, let’s try to break them down.

Revenues

Revenue fell 5.2%, “driven by the sale of our businesses in Russia and Belarus in September 2023 and translational FX headwinds”.

Reported revenue of £25.9bn for 2024 is less than the consensus forecast £26.1bn.

Organic revenue growth is 1.3% at constant exchange rates - this is the growth rate I always find to be the most meaningful.

Within this, “New Categories” revenue is up 8.9%.

The traditional “Combustibles” category isn’t really growing but is stable at +0.1%. Lower volumes but higher prices and a more expensive mix of products sold.

Profits

Reported operating profit £2.7bn includes a £6.2bn provision relating to Canada. This seems to have spooked the market the most today - there has been a class action lawsuit going on in Canada for many years, and it is reaching its conclusion.

Adjusted operating profit is much higher than the reported figure, at £11.9bn.

Let’s try to understand the discrepancy between these two numbers a little more.

I’ve found that the PDF for these results is much easier to navigate than the RNS; using the “data lake” at the end of the document I get the following breakdown of adjustments to the profit figure. Here they are ordered by size.

Ongoing litigation in Canada £6.2bn

Amortisation and impairment £2.3bn

Excise assessment in Romania £0.4bn

…. Plus some smaller items.

So apart from the Canadian litigation, and amortisation/impairment, there isn't much else of note.

However, this is the second year in a row when the company has had very large profit adjustments.

In 2023, there was a £23bn charge after it wrote down the value of its US brands.

So if investors want to think of BATS as a company with unclean accounts, I can’t argue against them. However, I still think it’s possible we can get clean accounts again soon.

Balance sheet

With intangible assets on the balance sheet being responsible for the enormous impairment charge in 2023, let’s check the latest state of play for the balance sheet in general.

Total equity: £50bn.

Intangibles: £94bn.

Tangible equity: minus £44bn.

The intangible assets are the largest item by far.

Next up we have borrowings: nearly £33bn of non-current borrowings (these are due in more than one year), plus £4bn of current borrowings.

Net debt (borrowings minus cash) is £31.3bn, down from £34bn a year ago - a nice reduction. Free cash flow was £7.9bn, which enabled the payment of nearly £3bn of dividends and the simultaneous reduction of net debt.

The leverage multiple (net debt to adjusted EBITDA) is 2.75x after taking into account the expected loss of cash in Canada, or 2.44x otherwise.

The company therefore argues that it has reached its target leverage multiple of 2.0-2.5x, but I think the 2.75x number is the correct one and so in my view they do need to keep working on debt reduction.

BATS still has its investment-grade credit ratings, e.g. BBB+ (with a stable outlook) at S&P.

CEO comments with a few snippets on the outlook. Unfortunately it will take another year before the company achieves its medium-term growth guidance:

"We are committed to Building a Smokeless World and becoming a predominantly Smokeless business by 2035…

2024 was an investment year with delivery in line with our guidance…

In 2025, while we expect significant regulatory and fiscal headwinds in Bangladesh and Australia to impact our combustibles performance, I am confident that we will progressively build on our delivery as we shift from investment to deployment and we remain committed to returning to our mid-term guidance of 3-5% revenue and 4-6% adjusted profit from operations* growth on a constant currency in 2026."

Graham’s view

I’ve been holding this one for a long time. I generally don’t invest for income and many of my shares pay no dividend at all, so it has been good to have at least one or two regular payers in the portfolio.

Peak pessimism was reached a year ago:

The word “illicit” is used 19 times in today’s results statement, as single-use vapour products remain a big problem for BATS, particularly in the US. Market share of the legal market has fallen but is still huge at 50.2%.

Internationally, vapour market share is 40% in what BATS refers to as the “Top Vapour markets”.

Another problem is that with pressure on consumer spending, there has been a rise in the “deep discounted category” in the US when it comes to cigarettes.

So there is no question at all that BATS is challenged. Not just in terms of regulations and lawsuits but also in terms of competition - from both regulated and unregulated competitors.

But against that, its financial performance remains spectacularly strong, when you look at the raw cash that it continues to generate.

And in the smokeless categories, it does have leadership in next generation products including vapes.

While I admit that I am biased by my status as a long-term shareholder, I think it’s worth having a moderately positive stance on this share, at this valuation:

I think real after-tax profitability is running at c. £8bn - this is in line with free cash flow and does accept the company’s version of adjusted profitability.

The enterprise value is c. £100bn, when we add £31bn of net debt to a £69bn market cap.

So adjusting for debt, the PER is about 12x, with an earnings yield of 8%.

That seems moderately attractive to me. There is just enough growth in new categories to offset the weakness in cigarettes and paint a picture of (very modest) underlying growth. Ethical concerns aside, I think this one adds up to an interesting proposition.

Concurrent Technologies (LON:CNC)

Up 3% to 196p (£168m) - Commencement of trading on OTCQQ - Graham - AMBER

CNC is now dual-listed on AIM in London and the OTCQX in the United States.

OTCQX is an “over-the-counter” marketplace, rather than a traditional exchange such as the NYSE.

It’s comparable to AIM in the sense that it’s driven by market makers.

And similarly in terms of market cap: it contains some companies worth more than $1 billion, but the vast majority are micro-caps.

The company says that this dual listing will help in terms of engaging with US investors/media and will help US-based employees to trade the shares.

The CEO says:

"We believe that having Concurrent's shares trade on both the AIM and OTCQX markets will enhance visibility of the business and expand our global reach. This decision follows an already increased level of interest from U.S. investors, driven by the excellent progress the Company is making across the Systems unit in the U.S."

Graham’s view

I like dual-listings because (in theory) they should help with market efficiency. When more investors are looking at a stock, it should be priced more accurately. It also gives me confidence that the company isn't hiding from exposure to the investing community in a country that it operates in.

From a UK perspective, the valuations given to some US-based tech stocks might seem excessive - of course I have a lot of sympathy with that view. And perhaps with US-based investors now able to trade CNC on their home turf, it will see an increase in valuation, compared to what it might have achieved otherwise..

I don’t see that as a bad thing - if it starts to look overheated, there is always the option for UK-based investors to sell. And any mismatch between the US and UK valuations should be mopped up by arbitrageurs.

CNC shares have been on a fantastic uptrend and made it into Ed’s November review of “The Top 20 clearest trending small caps”.

The company has not been shy about posting RNS announcements re: contract wins and other achievements. It is a “designer and manufacturer of leading-edge computer products, systems and mission critical solutions used in high-performance markets by some of the world's major OEMs”.

Serving a wide range of industries, but particularly defence and aerospace, CNC makes single-board computers and related systems and products that can survive harsh environments.

The recent trading update (Jan 16th) revealed that FY24 revenue would be up 25% vs. FY23, and 10% better than market expectations, which were £36m.

PBT would also be 10% better than market expectations, which were £4.7m.

My general impression of CNC is positive but I don’t have enough knowledge about the company to take a strong stance on it. It is expensive in P/E terms but for an ambitious and growing company that is turning a corner in terms of profitability, this might be a fair price to pay.

Applied Nutrition (LON:APN)

Unch. at 148.8p (£372m) - H1 FY25 Trading Update - Graham - AMBER/RED

Applied Nutrition plc, a leading sports nutrition, health and wellness brand, today announces an update on trading for the six months ended 31 January 2025 ("H1 FY25").

This one listed in November and has not been commented on before.

It offers ranges of protein, whey, creatine, etc., under the banners “Applied Nutrition”, “All Black Everything (ABE)”, “Bodyfuel” and “Endurance”.

In theory these could be valuable brands, but after monitoring SIS (NSI:SIS) and its lack of profits for a long time, I’m instinctively wary.

Today’s update from APN says that its revenue is “comfortably ahead of IPO guidance”. Good news but of course a company can easily tee itself up to beat expectations for its first trading update. So I wouldn’t read too much into this.

The Group has made good progress in the first half of the financial year, delivering revenue of £47.6 million, comfortably ahead of guidance provided at the time of the IPO of £46 million, representing a strong underpin for the full year guidance of £100 million. The Group continues to achieve a robust Adjusted EBITDA margin and cash conversion, both in line with market expectations.

Fans of I’m a Celebrity may be interested to know that Coleen Rooney wellness supplements have been added to the Applied Nutrition range. TV ads have been running.

Another tie-up involves a Vimto Isotonic Energy Gel (Vimto being the flagship product at Nichols (LON:NICL)).

A manufacturing extension will allow for future revenues of up to £160m, vs. £100m expected in the current financial year FY July 2025.

CEO comment:

Our successful IPO in October has had the positive impact we hoped for on the profile of Applied Nutrition and our industry recognition. I am pleased to report we have made strong progress in the first half, delivering performance ahead of our IPO guidance. Our growing global customer base highlights our appeal to a wide range of consumers, from everyday health-conscious individuals to professional athletes who rely on trusted sports nutrition products to fuel their performance…

Graham’s view

Experience teaches me to give IPOs a health warning. There is often a problem or a risk that hasn’t been revealed yet. My IPO rule is to assume it's overvalued for at least two years or until there is at least a 50% discount against the IPO price.

Perhaps this is one of the companies that breaks the rule. But Stockopedia isn’t seeing any value yet:

Hopefully they get to £160m of revenues before too long, and prove my scepticism ill-founded.

However, on the basis of the high valuation and the fact that it’s a recent issue, and also my experience with SIS (NSI:SIS), I’m taking a moderately negative stance on this one for now.

Unilever (LON:ULVR)

Down 6% to £44.64 (£110.6bn / €133bn) - Final Results - Graham - AMBER/GREEN

(At the time of publication, I have an indirect interest in ULVR.)

The market has taken a dislike to Q4 underlying sales growth at Unilever of 4.0%, marginally below consensus of 4.1% and dragging on the full-year result (4.2%).

There are contributions from both price and volume, with underlying volume up 2.9%.

Reported turnover for the year was €60.8bn, up 1.9% vs. 2023. The reasons for this lower growth rate (compared to underlying sales growth of 4.2%) are FX headwinds and business disposals.

Ice Cream was responsible for €8.3bn of revenue - it’s the most interesting segment right now because it’s being separated from the rest of the group.

We get an update on this. The former CEO of Heineken, who is currently Chair of Vodafone, Jean-Francois van Boxmeer, will be the Chair of the ice cream company:

The separation of Ice Cream is on track to complete by the end of 2025…

Ice Cream will be separated by way of demerger, through listing of the business in Amsterdam, London and New York, the same three exchanges on which Unilever PLC shares are currently traded. The Ice Cream business will be incorporated in the Netherlands and will continue to be headquartered in Amsterdam.

Amsterdam will be the primary listing, and UK business minister Jonathan Reynolds is quoted as telling reporters in relation to this, that Britain needs to do more to attract listings.

Capital allocation: €5.8 billion was returned to shareholders in 2024 via dividends and buybacks. With a €1.5bn buyback completed, the company announces a new one of the same size.

Net debt: €24.5bn, with a leverage multiple of 1.9x. This should be manageable without great difficulty. The company is only paying net finance costs of about 3% on this, although this is increasing as low-cost debt matures and is replaced by higher-cost debt.

Outlook: this has also hurt sentiment today. I think these bits are worth quoting in full:

We expect underlying sales growth (USG) for full year 2025 to be within our multi-year range of 3% to 5%. Market growth slowed throughout 2024. We anticipate a slower start to 2025 with subdued market growth in the near term. We expect the market and our growth to improve during the year as price increases, reflecting higher commodity costs in 2025. We expect a more balanced split between volume and price.

We anticipate a modest improvement in underlying operating margin for the full year versus 18.4% in 2024. We expect this improvement to be realised in the second half given the very strong first half comparator of 19.6%, which benefitted strongly from the combination of carry-over pricing and input cost deflation.

Graham’s view

When I look at enormous companies like this, I think it’s mostly about taking a view on whether this is the type of stock I want to own, rather than trying to come up with a prediction about its performance.

For me, this is the highest-quality large stock in the UK (vs. the likes of AstraZeneca, Shell, HSBC and Rio Tinto).

This is due to the terrific quality of its brands and its reliability of performance.

I see it as offering lower risk than the average stock, higher quality than the average, and I’m willing to pay for this sort of profile.

It gets a very high StockRank because the computers look at it and come to a similar conclusion as I do: that it’s probably worth this price.

I won’t go fully GREEN on it, as I acknowledge that growth is limited and this is going to put the brakes on returns. But as far as blue-chips go, this is one of my all-time favourites.

Mark's Section

Trifast (LON:TRI)

Up 2% to 76.5p - Trading Update - Mark - AMBER

Trifast is a well-known stock amongst individual investors, perhaps due to the interest of Harwood/Rockwood Strategic. The thesis is that if they can return to historical margins on rising sales, then the earnings will make the company look very cheap. Basically, it's the classic Value turnaround story. It is, therefore, not surprising that this trading update focuses on those ambitions. For example:

With our Recover, Rebuild and Resilience transformation roadmap delivering positive impact, the leadership team remains dedicated to executing its strategy and value proposition which is built around TR's core strengths of quality, service and technical engineering capabilities in selected markets and geographies where it can align both our customer expectations and deliver shareholder value.

However, having resilience as one of the pillars of your “transformation roadmap” shows how tough a market Trifast operates in! This is an update for Q3 trading, and the key line is:

Overall, the Group's performance in the Period and for the financial year to date underpins the Board's optimism that expectations for full year performance remain unchanged.

However, this in itself isn’t particularly impressive. Their broker, Zeus, have 5.8p EPS forecast for FY25, putting them on a forward P/E of 13.3x, with a net debt of £18.1m. The update itself is woefully short of actual figures to judge their progress on this. We are now six-weeks after the period end and I have to assume that if the figures looked great they would have included them in the update. We have to take the broker's forecasts out to FY27, to make them look reasonable value at 7.8x P/E and net cash. A lot can happen between now and 2027!

Mark’s view

While I wouldn’t necessarily bet against Harwood being able to drive the turnaround here, I don’t like the reliance on forecasts out to 2027 or beyond to make the company look reasonable value, and perhaps beyond the forecast window to really look cheap. Paul rated this AMBER in July, and I am minded to keep that rating until there are signs that the turnaround is accelerating and they can beat these modest forecasts rather than simply meeting them.

Gattaca (LON:GATC)

Up 5% to 75p - Trading Update - Mark - GREEN

Recruitment has been an incredibly tough sector for UK investors, and Gattaca is no different with its trading update to 31st January:

Group Net Fee Income1 ("NFI") expected to be £18.8m (H1 242 £19.4m), a decrease of 3% year-on-year ("YoY").

This doesn’t sound great, but they are actually doing well compared to other recruiters. Robert Walters saw NFI down 14% for a similar period. SThree had NFI down 9% in the year to 30 November 2024. Typically, recruitmnet is a scale business, and the larger operators trade on much higher ratings to reflect this. However, in current market conditions, Gattaca’s ability to be more nimble appears to have paid off, and its huge discount to the sector unwarranted.

These trends have been expected, and like many recruiters, they have been reducing costs and headcount:

Total Group headcount reduced by 12% YoY, with sales headcount reduced by 10% as the Group focused on operational efficiency and resource allocation with headcount investment targeted at sectors showing growth opportunities.

This means that PBT remains in line with expectations at around £3m. Cost-cutting is inherently the worst way of maintaining profitability as it is unsustainable. However, it is better than not cutting costs, and one of the factors that have separated the winners and losers in UK small caps this year has been those who saw the risks and have been cutting headcount and those who didn’t. The market has rewarded the former and punished the latter.

Paid-for research provider Equity Development turn this into an adjusted EPS of 6p, which makes the low-teens P/E seem expensive until you realise that a significant proportion of their market cap is in cash. Prior to this update, the company was trading at net cash, so it is slightly disappointing to see this fall in this update:

The Group expects to report statutory net cash as at 31 January 2025 of £16.7m (31 January 2024: net cash of £22.3m). Days sales outstanding (DSO) remains in line with recent reported trends, the decrease in net cash is primarily a reduction in trade creditors.

However, it remains significant, and they have large working capital flows, so this is a normal part of the business. I expect that their overall net tangible assets will remain the same or higher, despite a lower proportion being in cash, making them still look good value on this metric:

For what it’s worth, Equity Development calculates that this trades on an amazing 0.4xEV/EBITDA, falling to 0.2x for FY26. There are reasons for optimism as well as the trend in permanent recruitment. Statement of Work NFI was down due to delays linked to the public sector spending review. When this is finalised, any backlog of work could turn a headwind into a tailwind for Gattaca.

That cash doesn’t do shareholders any good if it simply sits on the balance sheet. The company is forecast to pay a 3p dividend this year but rising to 5.1p next year. The 7% FY26 yield seem reasonable, although I’d personally like them to do a bit more with the cash. Their EBT has a small purchase program in place to offset share dilution. However, the case for more extensive buybacks at this stage is surely a strong one?

Mark’s view

Having watched this company for a while, I had been buying recently as trading at net cash looked too cheap, despite what I thought was the risk of a profits warning. It’s not quite at net cash now, with the cash pile reducing due to lower payables. However, the lack of warning more than makes up for this. Paul rated it GREEN in mid-2024 when the share price was about 90p, on the basis that they were cheap and outperforming their sector. With the shares now trading at 75p, confirmation that the outperformance continues and that they are trading in-line on PBT, they look even better value today. GREEN

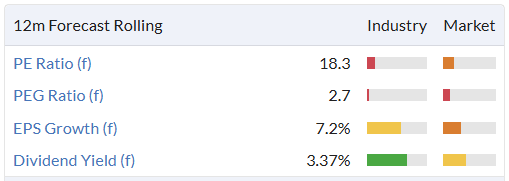

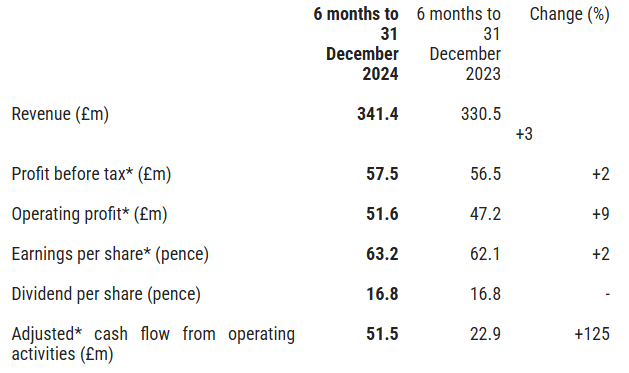

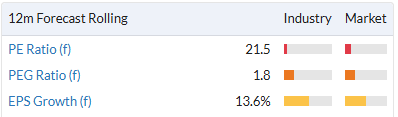

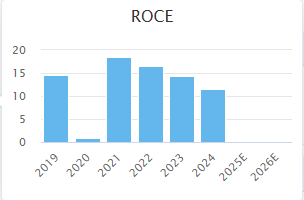

Renishaw (LON:RSW)

Down 8% to 3305p (£2.3bn) - Trading Update - Mark - AMBER/RED

These results aren’t particularly impressive:

This makes the rating here a complete mystery:

Even with a forecast of a better H2, this is still on PEG of 1.8.

Order intake recently improved, steady revenue growth expected to continue in H2;

There is a decent cash balance:

Strong balance sheet, with cash and cash equivalents and bank deposit balances of £233.2m (30 June 2024: £217.8m).

However, at less than 10% of the market cap, the valuation doesn’t change significantly.

Many investors may like the high gross margin, which suggests they have a good moat. They also have had a reasonable ROCE in the past. However, this has been trending down over time:

And, of course, this only creates shareholder value if they can grow the business. In terms of outlook, they say:

FY2025 revenue range: £695m to £735m; and

FY2025 adjusted profit before tax: £105m to £135m.

The current consensus in Stockopedia is for £725m revenue at the upper end of that range. PAT is a very wide range and works out as £83-107m based on the PBT figures above and their typical tax rate. The Stockopedia consensus is for £113m PAT so this appears to be a warning. The mid-point of the above range is some 16% below the Stockopedia consensus. It also makes those forecast growth rates in Stockopedia look too high and the forward multiple even worse.

Mark’s view

This is obviously a business with a decent moat, but this does shareholders little good unless they can grow the business. Perhaps there are multiple growth opportunities that are outside of the forecast window. However, these results and outlook give little confidence that this is the case. Instead, the most likely outcome is that growth rates will be low going forward, making this stock significantly overvalued. AMBER/RED

Ondo InsurTech (LON:ONDO)

Up 3% to 39p (£49m) - Trading Update - Mark - AMBER

Ondo InsurTech have an interesting sales strategy. Rather than trying to sell their leak detection systems to individuals, they are selling to the people who really bear the cost of leaky pipes: insurance companies. They have some water company customers, too. Although my understanding is that many water meters are capable of detecting leaks, so the drive toward metered water may reduce the demand here. Overall, I don’t think there is anything special about their technology. However, they have a system which is effective and easy to install. This strategy has been pretty successful so far, as the growth rates suggest:

Annualised Revenue Run-Rate: Projected to exceed £7.5m in Q4 FY2025, reflecting c.90% growth compared to Q4 FY2024 (£4.0m).

Full-Year Revenue to 31 March 2025: Estimated at £4.5m-£5m, ~70% growth versus FY 2024 (£2.7m).

This is impressive, but appears to be behind the consensus in Stockopedia:

The fastest growth is in the US:

Registered Customers: 27,000 in the U.S., reflecting 380% year-on-year growth. U.S. accounts for 65% of Registered Customer growth so far H2 FY2025.

But this is only 20% of their total registered customers so far. This is also their biggest opportunity. In terms of financials, they say:

Company remains on track to achieve EBITDA positive trading in H2 FY 2026

This is a year away, and with £6.2m of loan notes at 10% interest, this may not represent cash-positive trading. The good news is that they are receiving advanced payments for initial rollouts, relieving pressure on working capital. However, they will still need to fund the ongoing losses. I don’t see why they wouldn’t be able to raise fresh equity if required, but it remains a risk.

The repayment of the loan notes in January (£0.4m) and due in April (£0.6m) appears to come from the cash flow from the exercise of warrants:

Warrant Exercise: Since September 2024, warrant holders have exercised 10.9m new ordinary shares, generating £2.5m in cash inflows.

Around 900k warrants were exercised by the CEO this month. However, he funded these by selling 700k shares, meaning he likely didn’t put much fresh capital into his holding.

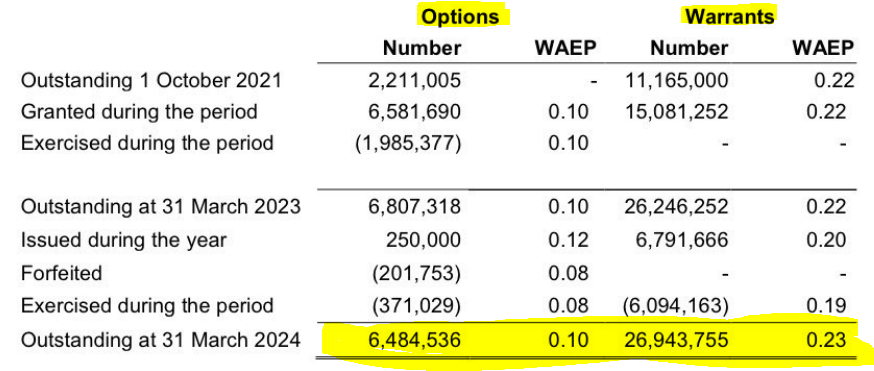

Here’s the full situation as of 31st March 2024:

And here is the issued share capital at the interim results in September 2024:

The Company had in issue 116,466,036 ordinary shares at 30 September 2024

So, the company has more capital to keep rolling out its leakbots, but it has come at the cost of dilution. The share count is now 127.4m, and the market cap is £49.7m. Fully diluted (since all options and warrants appear to be in the money), the share count is 149.9m, and the market cap is £58.5m. This is an eye-watering 12x forward sales, or 8x projected annualised revenue run-rate. Investors are paying a high price today for a company that is only projected to be EBITDA positive in a year’s time, even if the addressable market for their leakbots does seem to be huge.

Mark’s view

This looks to be a good revenue growth story based on a decent business model. However, at around 12x forward sales, this isn’t cheap. High forecast growth rates plus cash flow breakeven, likely being over a year away, means that there is a large amount of uncertainty regarding possible outcomes. I remain neutral on whether the growth will catch up with the rating. AMBER

Avingtrans (LON:AVG)

Up 4% to 375p - Contract Win - Mark - AMBER

Seeing this contract win by Booth Industries, I can’t help feeling a pang of regret. My only zero in over 20 years of investing (although several others came close) was Redhall. Avingtrans bought Booth, who makes fire and blast doors, from the administrators in 2019 for £1.8m. I believe far more was going on behind the scenes at Redhall than was ever publicly announced, but the result was that Avingtrans got a bargain. The contract size announced today is not particularly material for the company as a whole:

Booth Industries (Booth), has secured a new £4.5 million contract to supply pressure-rated fire doors for HS2.

That works out as less than 3% of forecast revenue. Nor does it seem material compared to previous orders for HS2-related work:

The contract expands upon Booth Industries' involvement in the HS2 project, following the £36 million contract secured in September 2020 to supply cross passage doors for the London-to-West Midlands segment of the route. Booth will begin mass production of the cross-passage sliding doorsets in its 600m², state-of-the-art production cell during 2025.

However, it highlights that Avingtrans is very good at acquiring niche engineering businesses cheaply and running them better than their previous owners. The problem is that at 25x forward earnings, this is probably in the price. 2026 earnings are forecast to grow significantly, but it really requires a detailed analysis of their order book to see if this is part of a new trend or simply a recovery from the FY25 dip in earnings.

Their broker, Cavendish, makes no changes to forecasts today but says:

Valuation: The shares offer strong intrinsic value as its engineering businesses such as Booth are successfully transformed, while group profitability is masked by the increasing opex investment in the exciting and transformative 3D x-ray and compact MRI systems that offer a huge potential medium-term value opportunity.

They have a 495p target price but without a lot of justification. It is normal for brokers to have a target price at a 30% or so premium to the current share price, so I’m not sure we can read too much into this.

Mark’s view

This contract win highlights what Avingtrans does best: buying niche engineering businesses and running them really well. However, I am neutral on the stock overall due to what appears to be a fairly full valuation. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.