Good morning! We have another large collection of year-end updates.

1pm: we're finished for today!

Spreadsheet accompanying this report (updated to 10/1/2025)

Companies Reporting

| Name (Mkt Cap*) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| Pearson (LON:PSON) (£8.6b) | TU | UL Sales +3%, Adj Op Profit +10%. FCF ahead of guidance. | |

| Wise (LON:WISE) (£15.0bn) | Q3 Results | +24% volume growth, U/L income +13%. | AMBER (Graham) |

Taylor Wimpey (LON:TW.) (£4.0bn) | TU | In line op. profit for 2024. Outlook: well placed to grow volumes. Increased build cost pressure. | |

| IG group (LON:IGG) (£3.6bn) | Acquisition of Freetrade | Freetrade purchased for £160m. | GREEN (Graham holds) |

| Dunelm (LON:DNLM) (£2.1bn) | H1 TU | Sales +2.4%, FY25 PBT within the range of market expectations | AMBER (Graham) |

Deliveroo (LON:ROO) (£2.0bn) | Q4 TU | 2024 adj. EBITDA towards top end of range (£110-130m). | |

Savills (LON:SVS) (£1.5bn) | Year End TU | 2024 in line. Year ahead: challenging conditions to continue but most markets are in recovery. | |

| Safestore Holdings (LON:SAFE) (£1.45b) | FY Results | EPRA Basic NTA per Share up 14.6% to 1,091p. | |

Trustpilot (LON:TRST) (£1.1bn) | TU | 21% constant currency bookings growth and adj. EBITDA to be ahead of consensus. | AMBER/GREEN (Graham) |

Bakkavor (LON:BAKK) (£810m) | Full Year TU | Ahead of market expectations. LfL Revenue up 5.1%. Net debt bottom end of 1-2x target range. | |

Ibstock (LON:IBST) (£661m) | TU | Adj. EBITDA £79m, “consistent with previous guidance”. Outlook: improved conditions. | |

Young & Co's Brewery (LON:YNGA) (£518m) | Q3 TU | Traded “exceptionally well” over Christmas/NY. LfLs up 11.6%. Optimistic about the year ahead. | |

Ab Dynamics (LON:ABDP) (£426m) | AGM TU | In line. Net Cash £23.2m. | |

Niox (LON:NIOX) (£235m) | Full Year TU | Adj. EBITDA slightly ahead of exps at £13.8m. | |

| Cab Payments Holdings (LON:CABP) (£169m) | Pre-close TU | Adj. EBITDA within range of analysts' consensus. Sales £105m (2023: £137m). | AMBER (Mark) |

MPAC (LON:MPAC) (£156m) | FY TU | In line. UL PBT £10.5m (FY23: £7.1m). Net debt £37m (FY23: net cash £2.1m). Order book £111m (FY23: £72.5m). | |

Smiths News (LON:SNWS) (£147m) | TU | In line. | AMBER/GREEN (Mark) |

Avingtrans (LON:AVG) (£127m) | TU | In line. | |

Concurrent Technologies (LON:CNC) (£119m) | TU | Rev & PBT 10% ahead of market expectations. | |

SRT Marine Systems (LON:SRT) (£114m) | TU | H1 PBT £2.5m on revenues of £25.5m (H1 last year revenues: £5.5m). £334m active order book. | |

| Carr's (LON:CARR) (£108m) | Sale of Engineering Division | £75m received, 7.1x Adj EBITDA. £70m to be returned via tender offer. | AMBER (Mark) |

Premier Miton (LON:PMI) (£97m) | Q1 AUM | £10.7bn AuM as of Dec 2024 (Sep 2024: £10.7bn). | AMBER/GREEN (Mark holds) |

Pebble Beach Systems (LON:PEBB) (£74m) | TU | In Line. Rev £125m (124.2m), Op Profit £8.4m (£8.0m). Cash generation slightly ahead. | |

Distribution Finance Capital Holdings (LON:DFCH) (£68m) | TU | FY24 adj. PBT >£14m as previously announced. £5m share buyback. New med-term guidance. | |

Real Estate Investors (LON:RLE) (£51m) | TU | £18.9m disposals in 2024, £15,3m debt reduction (“on track”) | AMBER (Mark) |

* Market caps at previous trading day’s close

Graham's Section

IG group (LON:IGG

Unch. at £10.26 (£3.7bn) - Acquisition - Graham holds - GREEN

(At the time of publication, Graham has a a long position in IGG.)

IG is a £3.7 billion company and so a £160m acquisition may or may not be enough to move the needle at this stage. But let’s explore this announcement.

IG is buying Freetrade, the commission-free trading platform.

Comment by IG’s CEO:

This is a rare opportunity to strengthen IG's UK trading and investments offering and broaden our target addressable marketFreetrade is one of the most successful emerging players in the UK direct-to-customer investment market, with a strong brand, highly scalable technology and delivering rapid growth. I am delighted that Viktor and his team will join IG and continue to lead Freetrade."

Freetrade has 720,000 customers and assets under administration (AUA) of £2.5 billion. AUA has apparently more than doubled over the past two years.

Valuation: IG is paying a premium price for this opportunity. Freetrade’s revenue in Q4 2024 was £8.3m (annualises to £33m) and its full-year EBITDA was £2.1m. IG is therefore paying a multiple of around 5x sales, a level that would be appropriate for a fast-growing tech company.

The plan: surprisingly hands-off, IG seems happy for the Freetrade brand to continue growing in its own right:

IG will operate Freetrade as a commercially standalone business with its own brand, existing management team and operational platform to support the successful execution of the strategy…

Freetrade is at a key stage in its development and IG will invest in expanding its product range, hiring talent, adding new features and increasing marketing activity to accelerate growth. IG plans to reinvest the majority of Freetrade's forecast profit in growing the business over the next two years.

Funding: IG tends to be cash-rich, and had over £900m of balance sheet cash as of the last annual report, with “own funds” (after adding and subtracting various items) of £1.1 billion. It has been using some of this cash to buy back its own shares under a £150m buyback programme. The purchase of Freetrade will also be paid for with IG’s own existing cash balance.

Graham’s view: I like this acquisition in theory, but I’m naturally going to be wary about the price paid.

I’m still slightly scarred from when IG paid $1 billion for the US-based tastytrade, a deal that seemed horribly overpriced and that also diluted shareholders.

At least this deal is much smaller, and so if IG has overpaid then the financial damage will be limited.

But I can see the attractions: Freetrade is a modern broker offering international shares, fractional share dealing and zero commissions, and so in that sense is comparable to the likes of US-based Robinhood ($HOOD). We could contrast it on the other hand against a conventional broker such as Jarvis Securities (LON:JIM), which offers none of those things.

Long-term, I wonder what this means for IG’s own share dealing product? IG Invest also now offers commission-free US shares on a modern app. Will it continue to compete with Freetrade? I’ll be curious to see how the relationship develops. But I’m sure IG must already have a very deep understanding of Freetrade, as they are competitors.

For context, IG’s own revenue from stock trading and investments was £40m in FY May 2024, vs. £27.5m generated by Freetrade in FY Dec 2024.

My overall view on IG at this time is naturally going to be positive: I’m a long-term shareholder here and I have positive views on both CMCX and PLUS. H1 results are due later this month. Even after a strong share price performance from IG over the last year, the stock only trades at a PER of about 10x. I think it’s fair that it has broken out to new highs:

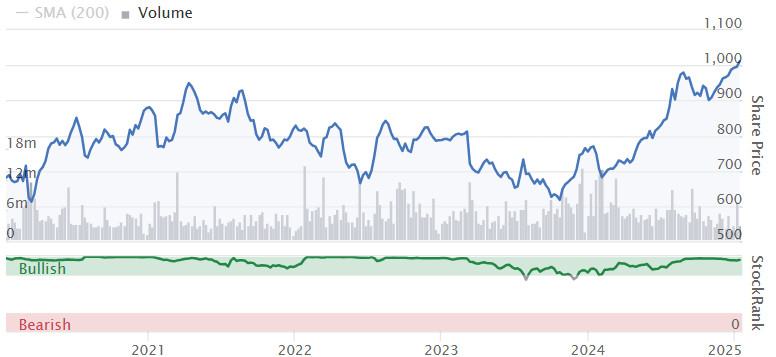

Trustpilot (LON:TRST)

Up 16% to 319.5p (£1.33bn / $1.62bn) - Trading Statement - Graham - AMBER/GREEN

The risk of removing this from my watchlist was that it would continue to go up, and it’s up strongly today, although this does follow some weakness in the first few weeks of 2024.

Here’s a 1-month chart:

The key points: annual recurring revenue is up 21% (at constant currencies) to $231m.

“Bookings”, a similar but slightly more forgiving metric, is also up 21% to $239m.

Revenue, the strictest measure of top-line performance, rose 18% at constant currencies. This is 2% ahead of consensus.

FX: gives a headwind of about 4% to the reported numbers. TRST reports in dollars and the dollar has been strong recently, so the value of non-dollar income has fallen..

Markets: Growth in the key North American market was strongest with bookings up 26%.

Net dollar retention rate: 103%. At the most recent H1 result, this was reported at 101%, so we have a slight improvement in the ability of the company to generate more revenues from existing customers.

Adj. EBITDA: will be ahead of the consensus figure of $22.2m.

CEO comment:

"The Trustpilot platform continues to expand, driving a growth flywheel as more consumers read and write reviews, and more businesses use our products to build trust, grow and improve. In 2024 we focused on B2B product innovation, launching new features combined with new pricing and product packages…

We made considerable strategic and operational progress in 2024 and remain confident in the significant growth opportunities ahead."

Graham’s view

I am nervous that TRST could jump another 100% this year, after I took it off my watchlist. However, I have to remember why I made that decision.

Price to sales (trailing): 7.8x. If it grows 20% this year that would fall to 6.4x. This might be a fair multiple but I don't think it stands out in terms of offering a bargain.

Price to EBITDA (trailing): if 2024 EBITDA is $25m for example, then P/EBITDA is 65x.

ValueRank: 3.

I was still GREEN on this in September at 210.5p. At over 300p today, while I still have tremendous admiration for what this company is doing, I have to moderate back to AMBER/GREEN in light of the stretched valuation.

Wise (LON:WISE)

Down 2% to £10.31 (£10.6bn) - 3rd Quarter Results - Graham - AMBER

I’ll briefly give this a mention today as it’s on Stockopedia’s “most viewed” widget, which suggests that people are interested!

I still think of this company as “Transferwise” but it has been “Wise” since 2021.

Here are the key points from Q3:

Cross-border volume +24% to £37.8 billion

“Underlying income” for Wise +13% to £349.5m, or +20% on a constant currency basis (I would focus on the latter).

The company has a big ambition:

We are making significant strides toward our long-term goal of becoming the network for the world's money as over 9m customers used Wise in Q3 to move or manage their money globally representing 20% growth YoY.

The “take rate”, or fee charged as a percentage of value, fell from 0.67% to 0.56% - this could be interpreted negatively, but Wise says it voluntarily lowered prices for customers and was able to do so thanks to “discipline and focus in reducing unit costs”.

Graham’s view

I don’t have a terribly strong view on this one: It’s clearly a big player in FX, and its growth in recent years has been terrific, but I’ll leave it to readers to investigate further for now. My own stance is neutral: I note that Roland was neutral in November at a share price of 800p, after careful consideration. With the shares already over £10, it would be brave of me to start getting bullish about this.

By way of comparison Revolut has been most recently valued at $45bn (£37bn) in private market transactions, nearly four times the market cap of Wise, and I’m inclined to think that it has a stronger chance of becoming “the network for the world’s money”. Revolut is used habitually for small, instant transfers and people are even increasingly trusting it with their monthly salaries, due to its ability to offer a wide range of applications (budgeting, loans, savings, investments).

So Revolut offers a more complete solution, while Wise is more specialised in FX. I think both companies have a bright future, but personally I’m more excited about where Revolut is going.

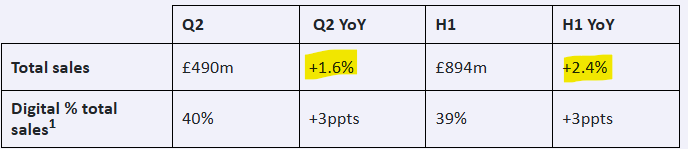

Dunelm (LON:DNLM)

Down 5% to 975.5p (£1.98bn) - Second quarter and first half trading update - Graham - AMBER

The UK’s leading homewares retailer provides a Q2/H1 update.

Q2 is a little weaker than H1 as a whole, due to a “challenging market”. They think they gained market share:

5 new superstores are to be opened in H2, and 13 small stores have been acquired in Ireland, where Dunelm products were already being sold..

Guidance: it sounds like investors should prepare for an outcome most likely at the lower end of expectations, based on the following comment:

Against the market backdrop and ongoing cost challenges facing our sector, PBT for FY25 is still expected to be within the range of market expectations.

Market expectations: FY25 PBT of £207 - 217m.

In a more encouraging comment, gross margin for the year should be in the upper half of the range of 51 - 52%.

As noted by Ken Mitchell in the comments thread below, there is a warning re: National Insurance:

…we are mindful of the impact of the Autumn Budget announcement on our business, suppliers and customers. As a large employer, with over 11,500 colleagues, we have previously highlighted the impact of ongoing wage inflation. Whilst the National Living Wage increase was largely anticipated, the increase in employer National Insurance Contributions is an additional cost headwind. Initiatives to drive productivity across the business are underway, and as these initiatives mature, we anticipate mitigating the upward pressure on costs over the medium term.

Graham’s view

With a financial year-end in June, DNLM is only going to face higher NICs for three months of the current financial year. The real test will be in FY June 2026, when the company might face a continuation of the current difficult market conditions and a major increase in costs. Based on today’s update, it sounds like profitability will be impaired, in the short-term at least, while the company attempts to mitigate upward cost pressure.

I treat the retailing sector very cautiously, as a rule, but I have been willing to go AMBER/GREEN on electronics retailer Currys in recent months.

DNLM is a much higher-margin business, earning gross margins of up to 52% while Currys only earns 17%. But Currys quantified the likely cost of the recent Budget, told us how much of the cost they had anticipated, and gave an overview of how they planned to mitigate it. Dunelm hasn’t done any of this. So I can’t take a positive stance and will instead agree with the AMBER posted by Paul in October. I’m even tempted to turn AMBER/RED as the company’s lack of disclosure re: its plan for higher NICs leads me to worry that there might not be much of a plan in place.

Mark's Section

Premier Miton (LON:PMI)

Unch. at 60p - Q1 AuM update - Mark (I hold) - AMBER/GREEN

Many investors will know this company due to the small and microcap funds it runs, with some well-known fund managers in this space. However, this investment firm does much more than this. UK Equities make up only around 17% of their assets under management. While they continue to see outflows totalling £33m for the quarter, there are some notable details in this update:

Uncertainty ahead of the UK budget was evident during October and this resulted in net outflows during the month. However, it was pleasing to note that flows turned slightly positive in both November and December.

While UK continues to see some weakness, the rest of the strategies are offsetting this:

This was largely driven by positive flow into our US equity, Diversified multi-asset, fixed income and absolute return strategies alongside continued outflows from our UK equity strategies.

With some modest performance gains, the result is AuM flat over the quarter. This doesn’t sound great. However, when compared to the likes of Liontrust that Graham reported on yesterday, which had £1.6bn of outflows, or Impax, which had £2.4bn of outflows even prior to the impact of losing the SJP mandate, this should be considered a strong result.

Importantly, flat AuM means that the company’s 6p dividend is likely covered by EPS:

So, unlike Impax or Liontrust, they aren’t maintaining their dividend by paying it out of capital on the balance sheet. The headline yield of 10% may not be as headline-grabbing as Liontrust’s 17%, but it is still very respectable and appears to be covered by earnings. The share price today is unchanged. However, they also went ex-dividend today for a 3p payout, so this could be considered a modest rise.

Mark’s View

All UK asset managers are cheap at the moment, but many with good reason. Premier Miton stands out from the sector by not facing severe redemptions over the last quarter and a dividend that appears covered by earnings. Hence the GREEN/AMBER rating.

Real Estate Investors (LON:RLE)

Up 5% to 31p - Trading Update - Mark - AMBER

This is a fund that is effectively in wind-down, so the progress here is good news:

During 2024, REI completed 20 targeted disposals of £18.9 million, at an aggregate uplift of 6.95% (pre-costs) to 31 December 2023 year end book value

While it is good news that the company is receiving proceeds ahead of book value, we need to be careful about assuming that this carries through to the rest of the portfolio. The first sales are likely to be the most desirable and, hence, most likely to be sold at a premium. There is a decent discount to tangible book value which provides a margin of safety::

Like all such funds this figure is the difference between a definite debt figure and the estimated value of the assets. The real value of the assets depends on what they can get for them on the open market and market conditions still aren’t particularly favourable at the moment:

Whilst the first six months of this year are likely to see a continuation of the trends and activity levels we observed in 2024, we are cautiously optimistic about the second half of 2025 as we expect momentum to build particularly if interest rates continue to gradually reduce and sentiment improves.

So far, these proceeds are used to reduce debt:

Debt reduction of £15.3 million during the year, with total debt reduced to £39.1 million as at 31 December 2024 (FY 2023: £54.4 million)

But the company pays also pays a decent dividend:

Better market conditions would accelerate disposals and allow some capital return as well as simply debt repayment:

This should pave the way for more favourable market conditions and investor optimism which would allow us to accelerate our disposals programme, repay debt more rapidly and commence our capital return to shareholders, all whilst continuing to pay a fully covered dividend.

One way to accelerate the progress would be a block sale. They say:

We remain open to exploring a corporate transaction, including the potential sale of the entire portfolio, in order to maximise shareholder returns.

While this would undoubtedly be good news if it happens, it reads more like hope than a more definite opportunity.

Mark’s view

The discount to TBV looks compelling for a fund in wind-down. However, some doubts remain over the valuation of the remaining assets and how quickly they can be sold, given current market conditions. In the past, I have had concerns over management alignment. Some related party transactions during the fund formation, and the very high remuneration prior to entering into wind-down suggested that incentives were not always aligned. While the fund entering wind-down assuages some of these, I go for an AMBER rating overall to reflect both the risks and opportunity.

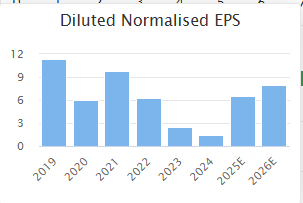

Carr's (LON:CARR)

Up 11% to 127.7p (£121m) - Sale of Engineering Division - Mark - AMBER

This reads like a fairly normal disposal of a non-core division until you realise the figures involved:

Sale of the Engineering Division (which, for the avoidance of doubt, excludes Chirton Engineering, which is subject to a separate sale process as outlined in further detail below) on a cash free, debt free basis representing an enterprise value of £75m and multiple of 7.1x FY24 Adjusted EBITDA

The sale of the division was known, but not what they would get for it. The market cap prior to this update was £108m, so this represents 69% of the market cap at last night’s close. There are other asset sales on the way, too:

A separate sale process for Chirton Engineering, which forms a part of the Wider Engineering Division and which is a wholly owned subsidiary located in North Tyneside, UK, specialising in the precision machining of highly complex components and assemblies, is underway and progressing positively;

Completion of the disposal of six non-core properties since 31 August 2024, generating proceeds of approximately £4.0m, with two remaining property sales in progress and expected to complete in FY25;

Of the amount received, £70m is going to be returned via a tender offer. No details are given as to price, but this is largely irrelevant to the outcome. I assume it will be priced to get a reasonable take up from all holders. Carr’s broker, Cavendish, says:

This is an encouraging announcement with a good valuation achieved on the disposed businesses. Our previous sum-of-the-parts valuation had £80m ascribed to the Engineering division. With Chirton still to be sold, this indicates we were broadly correct in our calculation, supporting our target price of 180p. The £70m tender offer represents c74p per share, valuing the continuing business currently at c£35m, or 38p per share, which offers good recovery value.

Adjusting this for today’s rise and excluding the 74p of cash, which will be returned via a tender offer, we have around 54p for the remaining business. Cavendish are already forecasting on a continuing business basis and have 3.0p EPS in for FY25. The forward P/E of 18 isn’t immediately attractive. However, Cavendish are forecasting £84.3m net cash at the end of FY25, or £14.3m after the tender offer. This is around 15.1p per share, which brings that P/E down to a more reasonable 13x. Still not sure how Cavendish manage to get to a 180p SOTP valuation without some pretty aggressive growth assumptions that are outside of their forecast window. The plan is to invest for growth in the agriculture division where they say:

The 'Agriculture Strategy' is comprised of three elements:

1. Improve operating margin across the global portfolio;

2. Deliver profitable commercial growth in the core business; and

3. Expand into new, extensive, grazing based growth geographies.

Mark’s view

While getting 69% of the market cap in cash for the engineering division is undoubtedly good news, I am left a bit underwhelmed by the valuation of the remaining agricultural division. At 18x FY25 earnings, there is a lot of work to do to grow the remaining business into a reasonable valuation. I wouldn’t necessarily bet against them achieving this aim. After all, they now have the capital to invest. However, I’d either need specialist knowledge of the sector or some estimates from the broker that indicate what is possible in the medium term. So far, their broker only seems willing to forecast the current financial year. As such, I am going for an AMBER rating.

Smiths News (LON:SNWS)

Up 1% to 60.4p - Trading Statement - Mark - AMBER/GREEN

A pretty short update today:

The Board confirms that trading for the year ending 30 August 2025 ("FY25") remains in line with market expectations

This means a continued decline in revenue:

But EPS maintained:

I am consistently impressed with management’s ability to take costs out and maintain profitability in a declining market. The company has an effective geographical monopoly, which enables it to generate good returns despite the obvious headwinds.

However, I have been consistently unimpressed by the diversification efforts here. There have been some good ideas, such as taking back recycling from newsagents or distributing sports drinks. However, the problem is that while these are complementary to their core business, they rely on the core business of existing early-morning deliveries. This isn’t so much a melting ice cube but more a van full of newspapers heading towards a cliff. Sooner or later, publishing physical media will become uneconomic for newspaper publishers. When one goes to digital-only, then this will place higher distribution costs on the remaining ones, which will quickly follow suit. I have no idea whether this will be in 2030 or 2035, but it's coming. What Smiths News needs is a new business that can be grown and doesn't rely on newspaper distribution to make it economic. While comments like this show management are aware of the need to diversify:

Furthermore, the Company continues to leverage its leading early-morning, end-to-end supply chain market capabilities and management look forward to providing an update at the half year results.

I’m just not convinced that they understand that the diversification they need is something that utilises their warehouse space and capabilities, without relying on the early morning distribution of newspapers, which will go completely at some point in the future.

Mark’s view

I can’t be too harsh on the company given how well management are managing the revenue decline here and paying out excess cash to shareholders. However, there is no escaping that physical newspapers will be gone at some point in the future. Unless, the company has a new business model in place at that time, it will be no more. Graham rated this GREEN following the last trading update, but for me, without concrete plans in place for diversification, there has to be an element of AMBER. Perhaps AMBER/GREEN then, overall.

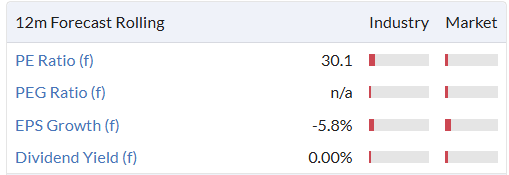

Cab Payments Holdings (LON:CABP)

Unch. at 69.7p - 2024 Pre-close Trading Update - Mark - AMBER

When first reading this update, it read like a profits warning:

Since the trading update in October 2024, the Company continued to be negatively impacted by a stronger dollar, reduction in aid flows and political uncertainty affecting the demand for cross-border payments, impacting both client volume and margin. This trend continued throughout Q4 and as indicated previously, the Company did not benefit from a usual seasonal uplift in revenue in the second half of 2024.

However, they appear to have managed to deliver an in line performance, largely due to cost-cutting:

Operating costs have been rigorously reviewed and immediate action is being taken to right-size the cost base for 2025. H2 2024 operating costs were well controlled with Adjusted EBITDA for 2024 likely to be within the range of analyst consensus estimates.

It is worth noting that adjusted EBITDA leaves a lot of scope for simply excluding the bad stuff, and within range could, of course, mean at the bottom! They say volume held up:

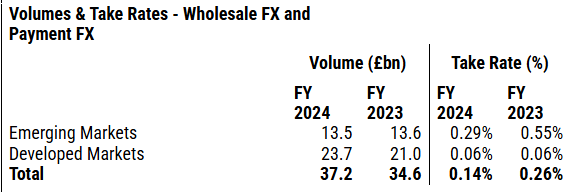

Total Group volumes for 2024 grew approximately 7% to £37.2 billion, in the context of market-wide SWIFT payment flows around the world dropping 4% year-on-year and flows into its core Sub-Saharan Africa market dropping 2% as the Company continues to take market share and deliver for its clients.

But must be facing margin-pressure as:

Gross Income for the financial year-ended 31 December 2024 is expected to be approximately £105 million (2023: £137 million) with performance in the second half of 2024 marginally declining versus the first half.

Which is a miss versus consensus:

Much lower take rates in Emerging Markets appears to have done the damage:

They clearly don’t see this trend reversing soon, as there is a huge headcount reduction on its way:

It is therefore commencing a programme to reduce its head count by approximately 20% including a redundancy program subject to consultation, while also driving higher performance within the organisation.

This restructuring is expected to take place during the first quarter of 2025. It is expected that the impact of headcount reduction savings will counteract the annualisation of strategic hires made throughout 2024, inflation and national insurance rises, resulting in broadly flat growth of staff costs in 2025.

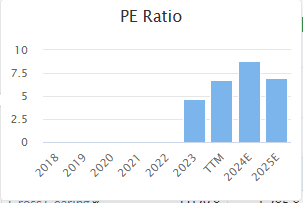

It seems strange that a 20% headcount reduction only gets them to flat costs year-on-year. The saving grace is that the P/E is pretty undemanding:

Mark’s view

I’m surprised the market hasn’t taken a more negative view on this trading statement today. While technically an in-line statement, it leaves a lot of wriggle room. Whereas the rest of the update perhaps asks more questions than it answers. H2 weaker than H1, Emerging Market take rates plummeting, a miss on revenue and a huge headcount reduction that doesn’t actually cut costs. The low P/E may yet reveal a bargain if the company can overcome these issues and return to growth. I’d want to see more sign of this before considering anything more than an AMBER at the moment, though.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.