Good morning! The Agenda is now complete.

1.30pm: let's wrap it up there, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Prudential (LON:PRU) (£20.3bn) | FY24 Results | 2024 performance: in line. New business profit +11%. Dividend +13%. Outlook: growth of 10%+. | |

Investec (LON:INVP) (£3.3bn) | Trading Statement | Adj. EPS -4% to +4%. Basic EPS -30% to -36% (previous year saw gain from merger with Rathbones). | |

Cranswick (LON:CWK) (£2.6bn) | Upgraded Targets | TU: in line. New targets include mid single digit organic growth, upper teens ROCE, <2x leverage. | AMBER (Megan) This is a wonderfully high quality company with ambitions to tighten up the quality metrics even further. But with slower growth forecasts than we’ve seen of late, I am worried that the valuation has become a bit stretched. |

Energean (LON:ENOG) (£1.54bn) | FY Results | Production +24% to 153kboed. Revenue +25%. All 2025 operations guidance reiterated. | |

Bloomsbury Publishing (LON:BMY) (£472m) | Trading Update | FY Feb 2025 ahead of consensus. | AMBER/GREEN (Graham) A great little update with all of Bloomsbury's divisions trading well. I leave my moderately positive stance unchanged. |

Wickes (LON:WIX) (£407m) | Full Year Results | Adj. PBT of £43.6m at upper end of exps. Weak consumer demand. Outlook: in line. £20m buyback. | AMBER (Mark) |

Crest Nicholson Holdings (LON:CRST) (£390m) | Trading Update | Encouraging start. Outlook: in line. Housing sector remains susceptible to weak consumer. | |

| Petrotal (LON:PTAL) (£340m) | FY Results | 2024 sales & production 17,558 & 17,785 bopd, slightly above guidance. Excellent start to 2025. | |

Costain (LON:COST) (£285m) | Framework award | Chosen to deliver infrastructure for Urenco (uranium enrichment). Contracts over at least 3 years. | GREEN (Graham) [no section below] No numbers are given in relation to this project. Some indication of likely revenues would have been helpful, and/or that it might have a positive impact on forecasts. The CEO says " this new role is an example of our strategic focus on growth in strong markets and building a resilient customer mix." But it was already known that Costain provides services like this in the civil nuclear sector. Without any indication of the specific significance of this award, I'm afraid the announcement comes across as being purely a PR exercise. |

Central Asia Metals (LON:CAML) (£278m) | FY Results | Rev +5% to $214.4m. EBITDA flat at $102m. Net cash $67m. 2025 production guidance in line with 2024 results. | AMBER/GREEN (Mark) |

James Fisher And Sons (LON:FSJ) (£165m) | Full Year Results | Revenue falls 11.8% to £437.7m. Adjusting for disposals and closures, revenue up 8.6%. Underlying PBT was £12m, forecast to improve to c. £14m in the current year. Net debt £56.1m. YTD trading in-line. See our coverage of the full year trading update in February. | AMBER (Graham) [no section below] No reason to change the neutral stance I gave last time. It's impressive that the company has pulled through several years of losses without resorting to shareholder dilution. Leverage is below 1.5x, i.e. within target range and in compliance with covenants. However, it is exposed to cyclical demand and I would be surprised if it deserved a valuation much higher than the current level. |

Hostelworld (LON:HSW) (£156m) | Preliminary Results | Net Rev -1% to €92m, Adj. EPS +42% to €13.97c (slight beat?), net cash €2.0m. Confident in strategy. | GREEN (Graham) I'm starting to think that this could be a big winner over time. Adjusted PER is only 10x. It does need some analysis to figure out how it's adjusting its numbers. |

Eurocell (LON:ECEL) (£147m) | Preliminary Results | Rev -2% to £357.9m. Profits in-line. Adj. EPS up 31% to 14.4p. Net debt excl. IFRS16 £3.1m (excl. recently announced £29m acquisition). New £5m share buyback.Confident of “good progress” in 2025. | AMBER/GREEN (Mark) |

Focusrite (LON:TUNE) (£101m) | Trading Update | Rev. not less than $80m. Lower GMs due to freight costs & mix. 25H1 EBITDA lower than 24H1. Expectations for first 12m of 18m reporting period unchanged. | AMBER (Mark) |

Touchstone Exploration (LON:TXP) (£57m) | Financial & Operating Results | Prodn +44% to 5,734 boe/d. Rev +19% to $57.47m. Earnings $8.27m, 4c/share. | |

Argo Blockchain (LON:ARB) (£23m) | Hosting Update | By end April 2025, 69% of c.23,000 miners previously hosted at Helios to be operational. | RED (Graham) [no section below] The reconfiguration of operations after Argo lost its previous host continues, and I remain very worried about shareholders’ prospects. The company abruptly parted ways with their CEO in January (he only joined in November 2023). It has significant debts outstanding, amounting to c. $40m as of the Sep 2024 update although it did raise GBP £4m in December. Recent talks to issue new debt of up to $40m broke down - discussions continue with other interested parties. I have doubts that the equity here is worth anything at all. |

Pressure Technologies (LON:PRES) (£14m) | Trading Update | Outlook for FY25 remains unchanged. | AMBER/RED (Mark) |

Graham's Section

Bloomsbury Publishing (LON:BMY)

Up 7% to 619.4p (£505m) - Trading Update and Board Appointment - Graham - AMBER/GREEN

It’s a lovely little update from this publishing house:

Bloomsbury's trading for the year ended 28 February 2025 is ahead of consensus expectations* following a strong performance in the second half. Success within the Consumer division was broadly based across our portfolio. The acquisition of Rowman & Littlefield in May 2024, where integration is progressing very well, drove growth in the Non-Consumer division. Bloomsbury Digital Resources grew for the full year despite the budgetary pressures, highlighted at the interim results, in our core academic markets.

As a result of the strong trading, $7.5m of debt has been paid down ahead of schedule. Bloomsbury had borrowed half of the upfront cost to buy Rowman & Littlefield last year ($38m borrowed to pay $76m upfront).

Estimates: as the company already told us in January, consensus expectations for FY February 2025 were for revenue of £333.4m and adjusted profit before taxation of £39.6m.

Graham’s view

I downgraded our stance on this in January to AMBER/GREEN, on valuation grounds.

The share price has been a little weak since then, and is lower now than it was a few months ago (even after today’s gains):

I think I can leave my AMBER/GREEN stance unchanged today. This is a fine company but can we get excited about it at this valuation? Maybe yes, if its M&A activity turns it into a compounding machine?

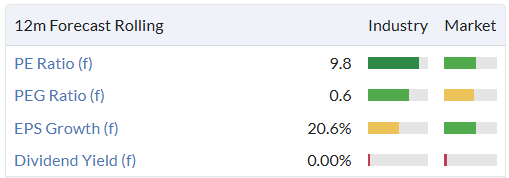

Hostelworld (LON:HSW)

Unch. at 125p (£156m / €186m) - Preliminary Results - Graham - GREEN

20 March 2025: Hostelworld, a leading global OTA focused on the hostel market, is pleased to announce its preliminary results for the year ended 31 December 2024.

It has been a while since we checked up on this one; I’m pleased to see continued strengthening of the balance sheet with the company now having net cash of €2m (end of 2023: net debt of €12m).

Revenue is down 1% due to the ongoing theme of travellers choosing cheap Asian hostels. So even with net booking up 6%, revenue declined.

The CEO suggests that this trend might be turning around:

Pleasingly, booking values returned to growth in the last quarter of 2024, with encouraging trends continuing into the first quarter of 2025 supported by bed price inflation in Asia.

And the outlook statement is confident:

"Looking ahead, we are confident that our distinctive social strategy will continue to be a key differentiator in the online travel market. We will continue to invest in our technology and expand our social features to enhance the customer experience and drive future growth.

The social strategy is something we’ve touched on before - the attempt to create a social network for travellers. This strategy appears to be meeting with success and helping to encourage users to make bookings through the Hostelworld app (app bookings growth +16%).

More app bookings and the use of a social app are also designed to help reduce the company’s reliance on its marketing budget, and marketing expenses declined in 2024, which helped to boost the bottom line.

Some key financials:

Operating costs (excluding marketing) were unchanged year-on-year, and marketing costs were down.

Adj. EBITDA +19% to €21.8m

Profit after tax +78% to €9.1m

Adjustments

Investors can use the €9.1m profit after tax figure, which is reasonably clean.

But adjusted profit for 2024 is €17m. I think it’s good to understand what is going on here, with an €8m difference between the two numbers.

The main figure being adjusted out is c. €5m of intangibles amortisation. As usual, I think it might be fine to adjust this out, if you also adjust the balance sheet to write down all of its intangible assets to zero. Hostelworld’s balance sheet does still have a positive value even if we assume that all of its intangibles are already worthless.

There are also nearly €2m of share-based payments (SBPs). I would definitely not adjust these out.

So this is how I might take a first stab at calculating the “real” profits at Hostelworld:

Adjusted profit after tax: €17.4m, which excludes the cost of amortising acquired intangible assets (this is a separate category to the intangible assets generated by the company itself).

Share-based payments €1.8m

“Real” after-tax profit in 2024: €15.6m. Equivalent result for 2023: €10.3m.

A further adjustment needed?

A complicating factor is that the company capitalises internal spending on development costs - if we are going to say that intangibles aren’t worth anything, then perhaps we can’t allow the company to capitalise these costs, many of which are staff salaries.

So the next step might be to make an adjustment for the fact that the company is capitalising its internal spending on development costs, boosting profits, and only deducting a fraction of this cost as an expense through amortisation.

For example in 2024, the company accepted a change of €0.6m under “amortisation of development costs”. But it had added €5.5m to its profits, by capitalising spending. The net boost to its profits from this was therefore nearly €5m.

The net boost to profits last year from this source was €3m.

So if we wanted to take a conservative view, we might write down profits in 2024 by €5m and profits in 2023 by €3m (both pre-tax numbers).

Graham’s view

I was already impressed by how they repaired their balance sheet after getting into some difficulty after Covid.

Today, I’m impressed by its improved profitability despite lower revenues. It leaves me wondering what sort of profit growth we might witness this year if we get some decent revenue growth - and this is currently baked into forecasts. The company is forecast to see revenues of €101m and adjusted profit of €19m.

There is the outside chance that the company develops a thriving social network for hostel travellers.

While formerly I was agnostic on the question of whether Hostelworld’s social app would succeed, a little bit of reading online suggests to me that social activity is picking up and travellers have noticed this. The company itself seems very pleased with the growth it’s experiencing.

This might not be a particularly valuable social network compared to others - for one thing, I presume that most hostel travellers don’t stay hostel travellers forever. I’ve only ever stayed in hostels when I was 18!

But if they do create this network and it does become a thriving community, then I am starting to see how it could benefit their business enormously.

I’m going to go GREEN on this as I’m seeing multiple attractive features and it’s only trading at an (adjusted) PER of 10x. Although I acknowledge that the real PER will be higher, considering the adjustments involved and the issue of capitalised spending.

The StockRank style is neutral, but Momentum is starting to turn positive:

In summary: this requires some work to understand its numbers and its plans, but I think there’s a real chance that it could turn into a big winner over time. Booking.com is probably the main competitor but I’m not aware that it faces any serious hostel-specific competition.

Megan's Section

Cranswick (LON:CWK)

Up 2% to 4960p (£2.65bn) - Trading update and capital markets day - Megan - AMBER

We’ve had a high quality update this morning from high quality pig breeder Cranswick (which, incidentally, is a fabulously high quality company).

In 2025 Cranswick will turn 50 and the company is celebrating by updating its strategy to help deliver increasingly ambitious growth targets. In this morning’s capital markets day, chief executive Adam Couch (who has been with the business for 35 years) will discuss opportunities for profit-generating investment including its pork and poultry processing facilities and its poultry supply chain. The company is also looking to increasingly leverage its genetic capabilities to breed even higher quality pigs. It’s already the UK’s largest pig supplier, producing more than 34,000 pigs a week, but continued investment will keep improving the efficiency of the company’s supply.

With these strategic objectives in mind, management expects to deliver mid-single digit organic revenue growth (excluding any impact of M&A activity) in the medium term and adjusted operating margins of 7.5%. That compares to the company’s five year revenue compound annual growth rate of 12.6% (which includes M&A) and a five year average operating margin of 6.3%.

Recently, the company’s reported earnings growth has lacked consistency - either benefiting from acquisitions or suffering amid wider market challenges. In the year to March 2024, earnings rose 14% and they’re forecast to rise 16% in the current financial year. Brokers have been upgrading earnings forecasts consistently over the last couple of months.

In the medium term, management is now targeting mid-single digit EPS growth. Indeed, forecasts for FY2026 are for 5% EPS growth, which is perhaps not exciting enough to justify a forecast price to earnings ratio of 18x.

Megan’s view

Cranswick is a phenomenally high quality company, with ambitions to improve two important quality metrics (operating margin and ROCE) in the next couple of years. It has a market leading position in the UK with plans to expand and improve its product offering. But however impressive this company is, the growth on offer no longer justifies the PE ratio for me. Senior directors including the CEO and CFO have been profiting handsomely from the share price momentum in the last few years by making big share sales. It doesn’t bring huge confidence in the ongoing growth opportunity. I’m moving to AMBER.

Mark's Section

Pressure Technologies (LON:PRES)

Down 3% to 34p - Trading Update - Mark - AMBER/RED

This trading update doesn’t really say much:

With key defence and hydrogen contracts either already secured in the first half of the financial year or expected early in the second half, and with continued growth expected in Integrity Management services, the Board confirms that the outlook for FY25 remains unchanged from the FY24 full-year results announcement made on 5 February 2025.

It means even less when you realise that in the Singer note published yesterday, they have forecast losses for FY25 and FY26. The price has been strong here recently on a significant contract win. But for this, Singer say “Manufacturing is set to begin in 3Q25 with completed systems scheduled for delivery in early 2026.” which is presumably why they finally estimate a profit in 2027.

The other big news since this was last reviewed on the DSMR is that they have sold off their Precision Machined Components division. However, a look at the latest results reveals contrasting performance for these businesses:

Precision Machined Components:

Revenue increased 52% to £17.1 million (2023: £11.3 million), delivering an Adjusted EBITDA of £1.5 million (2023: £0.1 million)

Chesterfield Special Cylinders:

Revenue of £14.8 million (2023: £20.7 million) was weaker than expected due to delayed order placement and the deferral of defence revenues into FY25

They appear to have kept the wrong business!

Along with the strategy change comes a name change at today’s AGM to Chesterfield Special Cylinders. This seems strangely unambitious, with the company saying they are now only ever going to produce Special Cylinders, and they will only do it in one modest Northern town. If the past and near-term forecasts are any guide, they will regularly lose money doing this very specific activity.

Mark’s view

Prior to the sale of PMC their balance sheet looked a little perilous. With this sale, the financial situation looks better, but this appears to be a case of selling off the well-performing division to fund the losses at the poor-performing one. With any break into profitability at the reduced group over two years away, why take the risk of holding the shares today? AMBER/RED.

Focusrite (LON:TUNE)

Down 4% to 165p - Trading Update - Mark - AMBER

This is a trading update for the six months to 28 February 2025. They say:

The Group's performance for the period was in line with expectations.

And:

While broader economic conditions remain fluid, the Group has plans in place to navigate potential challenges and the Board's expectations 1 for the first twelve months of the current eighteen-month period remain unchanged.

Helpfully giving those expectations:

Market expectations are understood to be a range for EBITDA for the 12 months to 31 August 2025 of between £24.5 million and £26.0 million.

[In October last year, they announced a change in year end to “align better with industry cycles, especially around the key holiday season sales”. However, end of February and August surely already means Christmas trading is in the middle of the period. So I am not entirely sure why shifting the HY-end to the FY-end makes that much difference.]

The increase in revenue from £76.9m to “not less than £80m” isn’t the whole story. There is a minor acquisition, but also margin pressure due to “ongoing elevated freight costs and product mix”.

They had previously flagged an H2-weighting due to an easing of “the current de-stocking trend in the US”, but now, with the possible impact of tariffs, they are getting “A revenue benefit of the planned increase in stock in the US sales channel to mitigate potential tariffs.” They say the underlying effect is revenue in Content Creation up 5%, and Audio Reproduction down 6%.

What this reveals as well is that they expect US tariffs will impact them. So far, it has been related to (temporary) working capital increases:

Net debt stands at approximately £18 million as at 28 February 2025 (31 August 2024: net debt of £12.5 million), reflecting the payment of the final dividend and an increase in stock and working capital in anticipation of the expected US tariffs.

However, the cost of their products will go up in a key market as they have communicated to customers effective from 1st May. On top of this, it seems their plan for rebuilding margins is pricing adjustments (i.e. rises) and new products. This may well be the right thing to do and something that competitors are forced to do as well. However, even if the prices of all similar products go up, there will be a marginal buyer who doesn’t replace their old models due to higher prices. Increasing prices into a US market that looks teetering on the edge of a consumer recession looks a risky strategy. What the hand of increased margins gives may be taken away by the hand of reduced revenue. In light of this, there looks a reasonable chance to me that the flagged H2 weighting becomes a miss.

Mark’s view

This is the sort of business I would love to own at the right price. The problem is that every time the price falls, it is accompanied by further bad news that makes the right price lower than previously expected. The current metrics are starting to look reasonable value:

But this is only true if I assume they really will hit their current EPS forecasts. An assumption that is increasingly looking like it is going to make an ass out of them (and me, if I bought shares now.) I retain the AMBER rating.

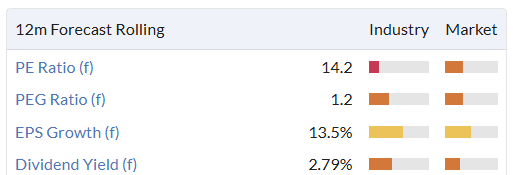

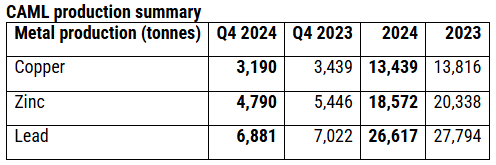

Central Asia Metals (LON:CAML)

Up 4% to 166p - FY Results - Mark - AMBER/GREEN

Production figures were announced in the Ops update on 9th January so these are already known:

As was the net cash ($67.6m), production guidance for 2025 and capex guidance, which are re-iterated in these results:

Production guidance for FY2025:

copper of 13,000 to 14,000 tonnes

zinc-in-concentrate of 19,000 to 21,000 tonnes

lead-in-concentrate of 27,000 to 29,000 tonnes

Capital expenditure in 2025 is expected to be in the range $18 million to $21 million

Overall, production guidance for 2025 looks up slightly vs 2024 and is more in line with 2023. The new news with these results, is how production and pricing have impacted profitability:

Group earnings before interest, tax, depreciation and amortisation (EBITDA2) of $101.8 million (2023 restated: $101.0 million)

As investors know, EBITDA is not always a great measure for a capital-intensive business, so it is a little disappointing to have to scroll down many pages to find the EPS:

Group profit before tax from continuing operations increased by 18% versus 2023, to $76.7 million (2023 restated: $64.9 million), reflecting an increase in profitability driven by a positive foreign-exchange swing of $9.0 million caused by the strengthening of the US dollar against the local currencies. EPS from continuing operations was therefore higher than the previous year, at 28.90 cents (2023 restated: 20.40 cents). Additionally, EPS has increased due to a reduced weighted average number of shares versus 2023 to reflect that the employee benefit trust (EBT) is now being consolidated into the Group and therefore these shares are excluded, in line with treasury shares.

This looks like a beat on the 26.4c EPS consensus on the StockReport. Stronger commodity pricing has clearly helped them overcome a slight reduction in production.This bodes well for 2025, as the combination of stronger commodity pricing and higher production (assuming the mid-point of their guidance) should lead to further growth in EPS. However, it should be noted that the $9m swing in FX due to the stronger US dollar may be starting to reverse in 2025. Here is the chart of the Kazahkstani Tenge vs the dollar for their copper production:

Although this is less pronounced for the North Macedonian Denar (Zinc & Lead)::

In terms of commodity pricing, copper looks strong compared to 2024 averages and especially 2023, zinc similar and lead a little weak:

Copper

Zinc

Lead

In terms of valuation, although the algos like it, the P/E isn’t necessarily stand out for such a miner. The other factor is the life remaining in the mines. With 15 years remaining life for their Sasa Zinc/Lead mine in North Macedonia it is perhaps reasonable to use a P/E as a short-hand valuation metric. With only 9 years left at the Kounrad Copper mine in Kazakhstan, this is more borderline. However, the yield is excellent:

With operating cash flow regularly exceeding EPS, modest capex commitments and net cash, I don’t see why this dividend won’t continue to be paid for the foreseeable future.

Mark’s view

Anyone considering investing in this company really needs to have their own DCF model that includes all the various inputs to profitability: production, commodity pricing, FX and costs. Despite not having done that detailed work, my initial impression is positive. There looks to be scope for EPS to rise further in 2025 based on current production guidance and spot commodity/FX prices, making the P/E mid-single figures. Unlike many miners, they pay a very decent dividend, and the cash flow and net cash suggest this can continue while mining operations are ongoing. Overall, I am going for a tentative AMBER/GREEN, with the caveat that a miner in risky jurisdictions probably shouldn’t be a large amount of anyone’s portfolio.

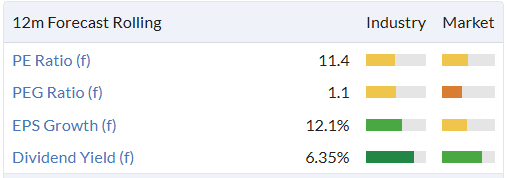

Wickes (LON:WIX)

Up 8% to 185p - FY Results - Mark - AMBER

The headline of the RNS reads well:

Strong market outperformance in FY24 with Adjusted PBT at upper end of market expectations

But the details are a little underwhelming:

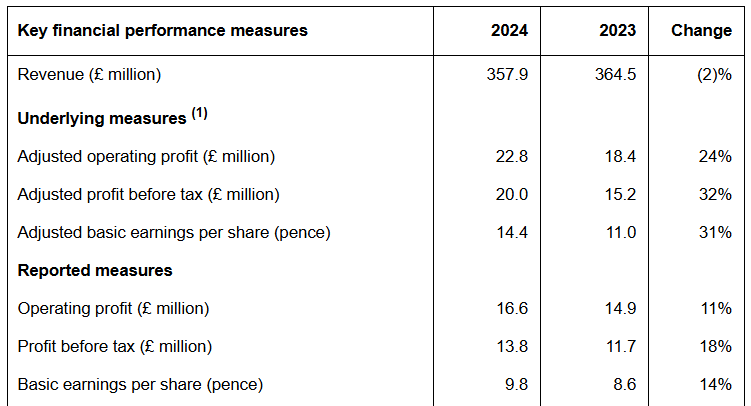

Total revenue of £1,538.8m (2023: £1,553.8m) down 1.0% year-on-year…

Adjusted profit before tax of £43.6m (2023: £52.0m), due to weaker consumer demand for larger ticket items and operating cost inflation

This EPS figure is a small beat on the 13.5p Stockopedia consensus, but is still down 6.6% on the previous year.

In terms of outlook, they say:

Trading in the first 11 weeks of 2025 has been in line with our expectations. Positive LFL sales growth continues in Retail. In Design & Installation, while delivered revenue growth remains negative, ordered sales are in positive growth for the second quarter in a row.

The actions we have taken across the business to invest in our growth levers and productivity position us well for 2025, notwithstanding the uncertain market outlook for larger ticket purchases and the continued cost headwinds. We remain comfortable with current consensus expectations for adjusted PBT for 2025.

It is good that they specifically mention consensus expectations and PBT, but it is worth noting that the EPS figure has been trending down recently, presumably as they fight to offset NI increases with productivity gains.

Apart from the dividend, which is maintained in today’s results, the rating here doesn’t immediately scream bargain:

However, there are a couple of reasons to be more positive. The first is that this rating is almost certainly close to trough earnings, given the general consumer backdrop. The second is that they have a significant cash balance:

There was £86.3m of cash on balance sheet at the end of the period (2023: £97.5m), after the net initial payment for the acquisition of a 51% controlling stake in Solar Fast18, the completion of the £25.0m share buyback programme19 and the sale and leaseback of our Braintree store, which raised £6.2m. Average cash across the year was £144.3m, reflecting our normal cycle of working capital.

This may not be immediately obvious from the StockReport, which includes their large lease liabilities in the EV:

Investors will have their own view on how to account for these in valuations, but my own is that net lease liabilities are more important than the gross figure. In these results, the lease assets are given as £562.5m, with current lease liabilities of £80.4m and non-current lease liabilities of £624.5. This works out to be a net lease liability of £142.4m, up slightly from the £138m the year before. Suddenly, this makes the financial situation much worse. Some will point out that these figures are based on models. Indeed, when discussing the quite significant adjustments, the company points out that the bulk of these are non-cash ROU impairment charges. Here are the details:

The problem is that they may be non-cash now, but those now-impaired leases will still be paid in the future. Their models currently say that the NPV of the cash they will pay out in lease payments over the length of their current leases exceeds the NPV of the cash generated from those store assets by £142m. There is some scope for these assets to be written back by stronger trading conditions, but it still suggests the company expects significant cash outflow to leaseholders in the future.

The market seems sanguine about this today, with the shares rising 8%, but this appears to be more about the announcement of a £20m buyback today, than the results themselves.

Mark’s view

The shares aren’t expensive, but having risen 23% YTD, they no longer look good value compared to other Repair, Maintenance, and Improvement-related stocks, which will benefit from similar tailwinds when market conditions improve. The net cash is significant but so are the net lease liabilities and the two more cancel each other out in any valuation exercise. AMBER

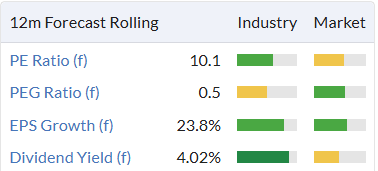

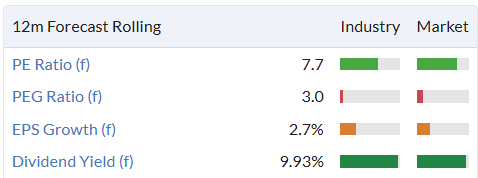

Eurocell (LON:ECEL)

Up 3% to 150p - Preliminary Results - Mark - AMBER/GREEN

This is another company where flat or slightly declining revenue turns into a big increase in profitability, at least on an adjusted basis:

The big benefit comes from “Proactive gross margin management combined with the benefit of lower input costs”. Here’s the details:

Gross margin for the year was 52.6%, up from 47.7% in 2023. Although increased competition for limited demand continues to drive pressure on selling prices in the branch network, we have benefited from a reduction in input cost pricing, including electricity, recycling feedstock, and PVC resin prices.

We operate a rolling 12-month forward hedging policy for electricity. In 2023 we were paying rates locked in during 2022, when wholesale prices peaked. We are now benefiting from the lower wholesale prices experienced in 2023.

For our recycling business, in 2023 a weaker RMI market and fewer window replacements restricted feedstock availability, resulting in a significant increase in purchase prices. However, we have made good progress securing additional sources of feedstock, which, alongside reduced demand and lower virgin resin prices, saw prices ease in 2024.

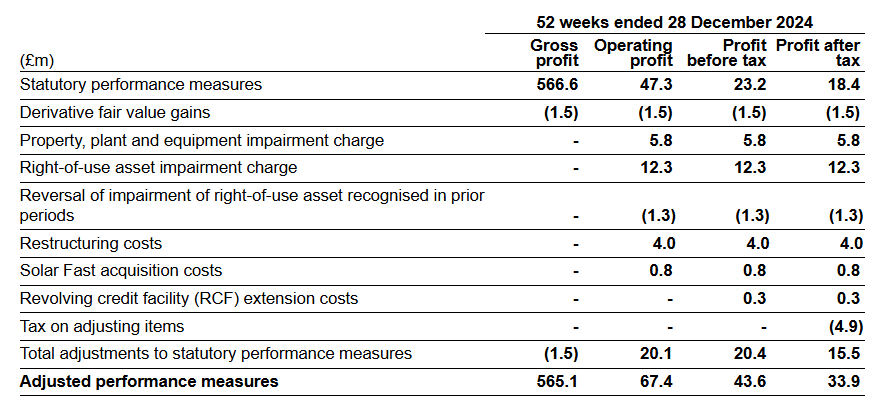

When we get a big gap between statutory and adjusted items, it is worth looking into the details. Here they say:

Non-underlying items for 2024 of £6.2 million include £2.2 million of strategic IT project costs, including cloud computing costs involving 'Software as a Service' arrangements and internal resourcing costs, which are expensed as incurred rather than being capitalised as intangible assets, a £3.2 million non-cash right-of-use asset impairment charge plus £0.8 million of acquisition costs in relation to Alunet.

None of these look particularly exceptional to me! Especially the IT projects:

Our strategic IT projects comprise a new customer-facing website and an employee management system (both now substantially complete) and, most significantly, the replacement of our Enterprise Resource Planning ('ERP') system. The expected cost of the system replacement is in the region of £10 million over the 2024-26 period. The implementation is on track and, as previously reported, we estimate the transition will be completed around mid-2026.

The letters ERP typically fill investors with dread as they tend to cost more and have far fewer benefits than planned. Looks like there are more significant costs that they will adjust out in the future. I’m guessing that if this new system saves money, after implementation in 2026, they are not going adjust out those savings! In the meantime, the implementation remains a risk to operations.

Plus, our old friend, the lease impairment charge is here. However, in this case, it seems to be genuinely a one-off:

The right-of-use asset impairment charge arises following a dispute with the landlord at a secondary warehouse in Derbyshire, where there was significant deterioration to the flooring. Following legal advice, we terminated the lease. The landlord has contested the termination and issued proceedings for unpaid rent. We will shortly begin a mediation process, with the potential for a court case to follow. With the site not currently in condition for use and the outcome of the dispute uncertain, the lease asset has been impaired in full.

Overall, there are only around £2m of net lease liabilities, excluding this impaired warehouse, so this isn’t a big impact on valuation. The rest of the balance sheet looks reasonable, with a net debt of £3.1m excluding leases. Although a post-period end acquisition for £22m + £7m deferred consideration means they now have modest gearing.

In terms of outlook, they say:

Demand in our core RMI market remains sluggish. We have seen some early signs of an improving picture in new build housing, albeit from a very low base. We will therefore continue to focus on cost reduction and operational improvements to drive efficiencies, to mitigate against the impact of a slower market recovery. We are confident in delivering another year of good progress in 2025, as we continue to execute on our growth strategy.

This is vaguely positive. However, it would be nice if they explicitly said how they are trading against expectations rather than the general hand-waving. If they are indeed in line, this looks very cheap for this stage of the market cycle:

The further £5m share buyback announced today appears to be a response to a share price that looks cheap rather than an attempt to support the price.

Mark’s view

Although I am wary about the IT adjustments, and the growth here is largely due to acquisitions in the short-term, the rating looks undemanding for a well-run business. Weak end markets, the mention of competitive pressures and an ERP implementation are why I am going for AMBER/GREEN vs Roland’s previous GREEN rating.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.