Good morning! It's a very busy day for results. Our Agenda is now complete.

1pm: today's bumper report is finished!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Reckitt Benckiser (LON:RKT) (£35.5bn) | FY Results | Lfl sales growth in line with guidance. Adj op profit +9% with margin improvement to 25%. | |

Informa (LON:INF) (£10.8bn) | FY Results | Revenue +11%, adj op profit +17% driven by underlying growth and acquisitions. | |

Rentokil Initial (LON:RTO) (£9.7bn) | Final Results | Revenue flat and operating profit down 12% in line with forecasts which were revised down in September. Weakness in North America. | |

Melrose Industries (LON:MRO) (£8.7bn) | FY Results | PBT +36% at the top end of guidance. Big increase in net debt to £1.3bn amid ongoing supply chain challenges. | |

Admiral (LON:ADM) (£8.6bn) | Annual Financial Report | Customers +1.4m (+14%), UK insurance customers +19%. Turnover +28% and group profits +90%. Market softening in 2025. | |

Schroders (LON:SDR) (£5.9bn) | Strategy Update and Annual Results 2024 | AUM +4% to £779bn, net new business down. Operating profit -3% but ahead of previous expectations. Launch of a 3yr strategy which aims to deliver £150m of annual savings. | |

Entain (LON:ENT) (£4.7bn) | FY Results | Net gaming revenue +6% at the top end of guidance, after a return to organic sales growth. Margin expansion in online sales ahead of expectations. | |

Harbour Energy (LON:HBR) (£3.1bn) | FY Results | Major acquisition completed in Sept. Production volumes +40%. Loss making after effective 108% tax rate. | AMBER (Mark) An accounting loss due to a very large tax charge appears to have spooked the market today. However, this probably isn’t the most important metric, as the prodigious free cash flow funds a large dividend. However, FCF seems highly dependent on the oil price. |

ITV (LON:ITV) (£2.6bn) | FY Results | Increase in advertising revenue offset by the expected fall in ITV Studios revenue. Adj EBITA +11% thanks to improving margins. | AMBER/GREEN (Megan) It’s a decent set of numbers, but not enough to light the fire that the turnaround investment case so desperately needs. I am mollified by the dividend (yielding 7%) and the untapped value in the Studios business. |

Smithson Investment Trust (LON:SSON) (£1.9bn) | Annual Financial Report | NAV total return +2.1%, comparator index total return +11.5%. | AMBER (Graham) Despite heavy buybacks in recent years, the shares traded at an average discount of over 10% during 2024. After a poor year, at least the first two months of 2025 have shown some outperformance against benchmark indexes. My main reason for caution is to do with valuation. The portfolio's average free cash flow yield is only 3.3% which strikes me as very low. I calculate the median forecast PER of its top ten holds as 27.5x. Turnover is also very high at 35.9% - below the sector average but still too high for long-term investors. |

Grafton (LON:GFTU) (£1.6bn) | Final Results | Slightly ahead of exps. Adj. op profit £177.5m (2023: £205.5m). Cautious on timing of recovery. | |

Lancashire Holdings (LON:LRE) (£1.5bn) | Final Results | Profit after tax unchanged at $321m . ROE in 2025 to fall to mid-teens (California wildfires). | |

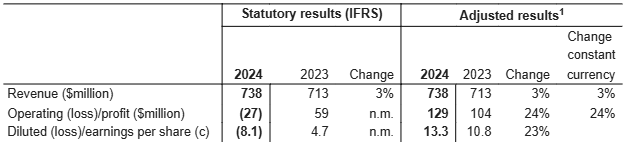

Coats (LON:COA) (£1.4bn) | FY Results | Rev +9%, adj. EBIT +18% (at constant FX). 2025 to be in line with exps. New med-term targets. | |

Pagegroup (LON:PAGE) (£1.1bn) | FY Results | Rev -9.8%, op profit -54% (constant FX). Outlook: uncertainty in UK, France, Germany.. | |

Vesuvius (LON:VSVS) (£1.0bn) | FY Results | Underlying rev -1.8%, “trading profit” -0.2%. Outlook: cautious. Trading profit to be broadly similar. | AMBER (Mark) |

Spire Healthcare (LON:SPI) (£904m) | Final Results | Rev +6.2%, adj. EBITDA +9% (LfL). Outlook: mid-single digit rev growth, adj. EBITDA £270-285m. | RED (Megan) Just like the market, I am unimpressed by the numbers from this private healthcare group, which is failing to take advantage of the demand in the market. It’s too expensive for such low growth. But patient investors might be rewarded with a takeover offer at some stage. |

Elementis (LON:ELM) (£901m) | Preliminary Results | Rev +3%, adj. op profit +24% (constant FX). “Solid start to 2025 amid challenging demand.” | AMBER/RED (Mark) A forward P/E of 14 looks daft for a company that has failed to grow its top line for a decade, and looks to have little chance of growing it in the future. |

Hunting (LON:HTG) (£486m) | FY Results | Rev +13%, EBITDA +23%, adj PBT +51% to $75.6m. Cash $104.7m. FY25: steady growth in rev & adj. earnings. | GREEN (Graham) Happy to leave our positive stance unchanged despite a large impairment charge (due to lower growth expectations at a segment) and wobbly earnings forecasts. The cash position has improved and on current forecasts the PER will fall to 7x next year. |

FW Thorpe (LON:TFW) (£352m) | Interim Results | Rev +1.4%, EPS +4.7%, in line with the Board's expectations. Order book remains strong, marginal improvement in profit for FY. | AMBER (Mark) |

Kenmare Resources (LON:KMR) (£245m) | Statement regarding possible offer | Proposal received at 530p (latest share price: 275p). Rejected it but offered due diligence information. | PINK (Mark) |

Robert Walters (LON:RWA) (£178m) | FY Results | Rev -16%, PBT -98% to £0.5m, Net cash £53.5m, dividend maintained. New FY trading continues to be muted. Basic EPS -9.0p. | AMBER (Mark) |

Hansard Global (LON:HSD) (£69m) | Interim Results | New business sales +36%, PBT -88% to £0.5m, AUM steady at £1.2b, “profit pressures” for the next two years. | AMBER (Mark) |

Assetco (LON:ASTO) (£52m) | Preliminary Results | Operating loss of £3.3m | GREEN (Graham) I'm taking a GREEN stance on this on the basis that the "independent valuation" of Assetco's stake in Parmenion (£75-90m) should have at least a loose connection with reality, and the growth at Parmenion is genuinely impressive. This means that Assetco's operating business is being thrown in "for free". From tomorrow, the operating business and the stake in Parmenion will trade separately and Assetco will be known as River Global. |

Northern Bear (LON:NTBR) (£7m) | Trading Update | EBIT to exceed market expectations, in the range of £3.15m - £3.45m | AMBER/GREEN (Mark) [No section below] |

Graham's Section

Hunting (LON:HTG)

Down 2% to 301.9p (£498m / $643m) - Results for the year ended 31 December 2024 - Graham - GREEN

The first rule of financial highlights is that if a percentage growth figure is missing, it’s negative.

Sales order book $508.6m.

The corresponding figure last year was $565m (and it was given along with a growth rate!).

We mentioned Hunting’s declining order book at the time of the January trading update, here.

Similarly:

Revenue increased by 13% to $1,048.9m.

Non-oil and gas revenue $75.1m.

No growth figure is given for the non-oil and gas revenue, because it is negative!

More positively, EBITDA is up 23% to $126.3m. The January trading update said that EBITDA would be within the range of $123-126m. So it is slightly ahead of that.

For 2025, EBITDA guidance is unchanged at $135-145m.

Restructuring: cost savings from restructuring are now expected to c. $8-9m (we were previously told it could be up to $10m). North Sea oil and gas activity is on the decline and Hunting’s focus is in other regions such as Kuwait (enormous contracts signed with the Kuwait Oil Company) and the United States.

Outlook: sounds positive.

2025 should see steady growth in revenue and adjusted earnings as all market indicators point to further progress due to prevailing energy demand. The Directors anticipate an acceleration in activity in the second half of the year and into 2026, as market and geopolitical tail winds increase with robust commodity supply and demand dynamics supporting activity in the year ahead.

The new administration in the US “is indicating robust support for oil and gas”, although there may be unforeseen challenges arising from tariffs.

Hunting's financial targets include an EBITDA margin of 15%+ and ROCE of 15%+ (2024: 12% and 9% respectively).

Impairment of Hunting Titan: this large segment makes perforating systems and generates about a fifth of Hunting’s total revenues but it generated a loss ($8m) in 2024, vs. a profit ($13m) in 2023.

Clicking into the financial statements document and the footnotes, we get the details on an enormous impairment charge for over $100m of goodwill at this segment.

The trading performance at Hunting Titan continued to decline through the second half of 2024 following decreased activity in the US onshore well completions market and a resulting fall in demand for its Perforating Systems products. As a result of this, management has reassessed its short and medium-term forecasts. The compound annual growth rate for revenue for Hunting Titan from 2024 to 2029 was 3% (2023 – 2023 to 2028 was 8%). EBITDA margin is expected to reach low double digits by 2029.

Lower growth expectations, combined with higher interest rates which also influence these calculations, resulted in a lower calculated value of the goodwill for this segment.

Graham’s view

I think it’s fine to ignore the impairment charge but I do not think it’s fine to ignore the reasons behind this charge: lower growth expectations and weaker profitability at one of the company’s major segments, in a higher interest rate environment.

But there are still reasons to be positive. The balance sheet shows net assets of $902m with the intangible element of this only $85m now, following the impairments. Investors might also wish to exclude the value of the deferred tax asset (>$100m). But even then, the shares are still trading at a discount to book value.

We’ve been GREEN on this before and I’m inclined to remain positive on it today as the company has delivered attractive growth in recent years and continues to trade at a level that may offer some value, both in terms of its earnings potential and its assets.

Estimates: thanks to Canaccord for a new broker note out today. Consistent with what I said above, they observe that there is now “a much cleaner balance sheet” following the large impairment charge. They say that “the outlook for 2025 is in aggregate unchanged” which I think refers only to EBITDA and cash.

They have nudged their revenue forecasts down slightly. EPS gets cut from 46 cents to 42 cents (2025) and from 58 cents to 55 cents (2026).

The share price is equivalent to 390 cents and so the earnings multiple on 2026 forecast earnings is only 7x. Let’s see if forecasts can stabilise here! EPS estimates haven’t been all that steady:

The instability of the earnings forecasts is a worry. However, I am going to leave the GREEN stance unchanged with the deciding factor being the company's improved year-end cash position - which I hope has not been excessively window-dressed. According to Canaccord, net cash has increased from zero at the end of 2023 to $118m at the end of 2024. The figure that I get from the financial statements is a little different but paints a similar picture. According to my calculations, net cash excluding leases has moved from zero at the end of 2023 to $100m at the end of 2024.

With a more tangible, cash-rich balance sheet at the end of the year, I can leave our positive stance on this unchanged with a clean conscience.

Assetco (LON:ASTO)

Up 1% to 37p (£51m) - Preliminary Results Announcement for 2024 - Graham - GREEN

AssetCo plc ("AssetCo" or the "Company"), the agile asset and wealth management company, today announces its results for the year ended 30 September 2024.

We rarely give this much coverage but let’s change that today.

Martin Gilbert, founder of Aberdeen, took over Assetco in 2021 with the plan to take over and consolidate small asset managers and wealth managers.

Today’s results show AUM of £2.8bn (2023: £2.4bn).

Checking the business review I see that client net flows were negative (c. £400m net outflow) but they were offset by an acquisition, a new joint venture, and positive returns.

The operating loss reduces to £3.3m (2023: £7.7m).

Martin Gilbert comment:

"The financial year ended 30 September 2024 was a challenging one for both the industry and AssetCo. Nonetheless our results for the year show us continuing to close the gap towards profitability with a significantly reduced operating loss for continuing business of £3.3m.

Reorganisation (first announced last year)

Shareholders have been asked to approve some big changes.

Assetco is being renamed River Global and will have two share classes: A and B.

The A shares will represent the existing operating business and will stay on AIM.

The B shares will represent Assetco’s 30% stake in Parmenion. According to the original plans these would not have been listed on AIM. But that has changed and now it is planned that the B shares will trade on AIM, too.

Assetco’s stake in Parmenion has been independently valued at between £75m and £90m.

The idea is to “provide greater flexibility for our shareholders and in our ability to deal with these two distinct lines of business”.

The two share classes should begin trading tomorrow.

Operational highlights

€400m was added to AUM in a joint venture with fund manager Jonathan Knowles. Mr Knowles and employees of his new firm “now operate under the existing River Global regulatory and operational framework”.

There are also advanced discussions with an (unnamed) offshore wealth manager, which could see River Global becoming the investment manager for a new range of funds.

Market Commentary

This is confirmation for my existing beliefs but I think it’s pertinent:

Over the last few years, the performance of global equity markets has been increasingly dominated by a small number of mega-cap stocks that have benefitted from escalating price momentum as they become ever larger percentages of global indices, drawing in passive and index-following capital and even some active managers who fear missing out on the growth themes that they represent. Investors have been overtly focused on price momentum to the exclusion of other factors and as a result of this many investor portfolios have become increasingly concentrated in a narrow range of stocks and the themes that these stocks represent. Consequently, the breadth of market returns is now nearly as narrow as it was in 1999-2000. In addition, the dominance of mega-caps has led to increasing underperformance of mid and smaller sized companies, a trend that is a global, not just a regional phenomenon.

Graham’s view

If we believe the “independent valuation” of Assetco’s interest in Parmenion (£75-90m), then it’s almost unavoidable to conclude that Assetco is undervalued at a market cap of £51m.

Parmenion is a sizable platform with assets under management or advice of £12.6bn as of Sep 2024.

According to pro-forma numbers given today, their 30% investment in Parmenion generated an operating profit of £2.4m for Assetco this year, with net assets of £27m.

Those numbers don’t immediately scream at me that they could be worth £75-90m, but its AUM has grown by nearly 20% in a single year, which I think was fully organic growth. Operating profit grew 30%. It wouldn’t take very many years growing at that rate to justify the independent valuation.

Even if the independent valuation is wrong and the Parmenion stake is only worth £50m, that still leaves the operating business of Assetco thrown in “for free” at this market cap.

So I’m happy to a GREEN stance on this. Please bear in mind that this might be considered a special situation, given the spin-off plans. And there are still very few signs of a recovery in the UK’s active fund management industry. Assetco’s net outflows in 2024 were more than a sixth of their starting AUM.

So this might not be one for the faint-hearted.

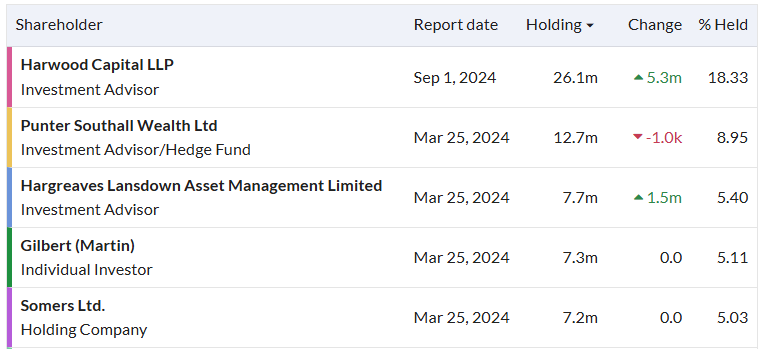

As an aside, there are some familiar names on the shareholder register. They include Harwood Capital and Somers Ltd. Bermuda-based Somers were the majority owners of the ill-fated PCF Bank that we used to cover in this report.

Megan's Section

ITV (LON:ITV)

Up 5% to 73p (£2.8bn) - Final Results - Megan - AMBER/GREEN

The headline numbers for ITV’s 2024 financial year are as expected.

Media and Entertainment (48% of the group total) up 1%. Advertising revenue rose strongly thanks to the impact of the Euros last summer, which means sales in the Media and Entertainment division were up slightly at £2.1bn.

Subscription sales from the company’s streaming services (mostly ITVX), which make up the remainder of revenues in the M&E division, were down sharply. It was always going to be a hard sell to convince Brits to pay for a streaming service which offers content that many of them feel like they have already paid for via their TV licence. Especially set alongside the reams of content being pumped out by streaming giants in America.

The division has also gone through another big year of ‘efficiencies’. The word is mentioned 42 times in this morning’s announcement, but it’s not entirely clear what those efficiencies might be. An organisational redesign and operational efficiencies sounds a lot like a nice way of saying redundancy. Staff costs decreased slightly in 2024. There’s also been a decrease in transmission costs. Overall, heavily adjusted operating profits in the division rose 22% to £250m.

ITV Studios (52% of the group total) down 6%. As expected, the company’s more promising Studios division (which creates content both for ITV’s channels and external partners) was hit by the 2023 actor and writer strikes in Hollywood. This slimmed the production pipeline in 2024 meaning the company sold fewer scripted shows.

This did mean the balance of scripted and non-scripted shows tipped further in the direction of the latter, which are easier and cheaper to produce. Margins in the Studios business rose thanks to this different sales mix and £25m of ‘efficiencies’. Adjusted operating profits were 5% higher than the previous year at £299m.

The outlook. Management is looking to 2025 with optimism, especially in the Studios business where organic revenue growth is currently forecast at 5% thanks to an impressive roster of new productions. The M&E business is likely to struggle without a major sporting event to compare with last year’s Euros. But expect more of the ever present ‘efficiencies’ to keep profits just about ticking in the right direction.

Financial strength. This is the first set of annual results from ITV which have not included deficit contributions to the company’s large pension scheme. The scheme is now fully funded, which removes the burden which had previously been a drain on cash inflows.

Still, free cash inflows in 2024 were slightly lower than the previous year at £325m, owing to an increase in working capital outflows after Hollywood actors and writers came back to work after strikes in 2023. This represents free cash conversion from net profits of 80%.

The balance sheet is in decent shape with £431m of net debt at the end of the year, equivalent to net gearing of 26%.

Megan’s view:

ITV is a difficult company to take a view on and there are a few different lenses which can be applied.

First up, this is a turnaround play which is taking a very long time to turn. ITV is currently ranked highly for both value and momentum (the hallmarks of a turnaround company). Its shares are trading on just 7.7 times forecast earnings and the current price represents 1.38x its book value (although there is an argument to be made that the current book value doesn’t quite do justice to the Studios business, but more on that later).

The company’s shares peaked in 2015 and, despite momentary surges, remain 72% below their highs. Indeed, without a proper catalyst for recovery I worry that investors waiting for the turnaround to kick in might have a lot longer to wait.

Second, there is the income case. Despite cutting its dividend in 2018 and pausing it during the pandemic, ITV has generally been a reliable income stock. For 2024 it has announced another 5p dividend, which was well covered by both earnings and cash flow. If the payout is held firm at 5p again this year, the shares are currently yielding 7%.

And finally, there is the ‘sum-of-parts’ value case, which could lead to more takeover speculation. Roland wrote about sum-of-parts valuation here and I think an argument could be made in the case of ITV’s Studios business. Just over £2bn in annual sales is not insignificant for a production company. It’s more than the annual revenue being generated by Dreamworks, MGM or Entertainment One prior to their respective takeovers. Those acquisitions were completed at price to sales ratios ranging from 2.1x to 5.8x.

The trouble here is that while a takeover offer might provide huge piles of cash to the business, what’s left will be a broadcaster struggling in a particularly bruising market.

On balance, I am staying positive because I think the income and takeover potential are enough to satisfy long-suffering shareholders. But I am unconvinced about the turnaround potential unless management is willing to take more drastic action. AMBER/GREEN

Spire Healthcare (LON:SPI)

Down 16% to 187p (£752m) - Final Results - Megan - RED

Private healthcare provider Spire has provided what is, in print, a decent set of numbers for the financial year to December 2024.

After adjusting for the disposal of Spire Tunbridge Wells (which was sold to the local NHS Trust in March) and the acquisition of Vita Health completed at the end of 2023, sales rose 6% to £1.5bn.

The company is benefiting from increased outsourcing from the NHS (where revenues rose 9% to £448m) as well as more private referrals (revenues up 3.7% to £1bn).

The hospital business remains at the core of the Spire operating model. The company runs 38 private hospitals with a specialty in orthopaedics - a division of healthcare where NHS wait times are at their worst. In 2024, the company saw NHS orthopaedic referrals rise ahead of expectations.

The more promising division of Spire’s offering is its primary care services, which were bulked up by the acquisition of Vita Health Group in late 2023. This company has a strong offering in mental health, which is another health need in which the NHS struggles to keep up with demand.

Group operating profit rose 9% to £138m, representing an operating margin of 9% (in line with the last few years). Pre-tax profits, after taking into account adjustments, were up 29%. Cash inflows from operating activities were £236m.

And yet the market was not impressed.

There are a few theories circulating about why these numbers sparked an immediate 20% decline in the share price (which has tempered somewhat at 11am, but the shares are still down quite heavily).

The first is that these numbers came slightly below the consensus sales forecasts, while adjusted EBITDA was at the bottom of the previously stated range (£255bn-£275bn).

Then there is the fact that Spire really should be doing better. It is no secret that NHS waiting times are deeply problematic and public sector outsourcing has become the chosen government strategy to help deal with the burden. Investors in our community have commented that 6% sales growth during a period when demand is so high is absolutely not good enough.

What’s worse is the fact that management is only guiding to a similar level of sales growth next year, which is behind the longer-term average. Management has said that insurers are reporting a strong increase in the number of healthcare policies written which, combined with higher NHS referrals, should probably lead to more impressive sales growth than "mid-single digit”.

The 2025 financial year will also feel the burden of increased national insurance contributions. This is the first time that management has admitted that these higher costs will trim £30m of EBITDA in 2025. Adjusted EBITDA for the year is now expected at between £275m and £280m, that compares to £260m in these numbers.

Investors might also have been spooked by rising capital expenditure following major refurbishments at two of the company’s hospitals. Free cash flow has fallen to £39m.

Megan’s view:

An attractive end market is all well and good, but not if a company fails to take advantage of the opportunity on offer. I have been positive about Spire in the past because of that opportunity, but following these numbers I am uninspired.

This wasn’t a profit warning, but it’s definitely a profit disappointment and the major share price sell-off can be a bit of a red flag in and of itself (something that Ed found in his research into trading statements). Fidelity, whose funds own just under 10% of the shares, has also been trimming its position of late which isn’t a great sign and though chief executive Justin Ash injected some confidence when he spent £50k on the shares in September last year, that hasn’t been enough to convince the market that the company can take advantage of the opportunity.

There’s a potential takeover bid lurking somewhere in the wings. South Africa-headquartered Mediclinic currently owns 30% of the company and is no stranger to acquisition. But there’s not a lot for investors to get excited about while they await a bid. RED

Mark's Section

Kenmare Resources (LON:KMR)

Up 45% to 400p - Statement re-possible offer - Mark - PINK

I’ve written about Kenmare Resources (LON:KMR) several times over the last few years as it has consistently appeared on my low P/TBV and high-yield screens. Heavy Mineral Sands, that Kenmare produces, looks like one of the best capital market cycle plays out there, as growing demand and constrained supply should lead to stronger pricing.

However, I don’t currently hold shares in the company. Two things put me off. The first was the political risk, with all of their production from a single mine in Mozambique. The second was when I asked the then-CEO Michael Carvill on the last investor call he led why a larger miner doesn’t swoop in and buy them given the discount to TBV, he said that their current capex moving one of their major wet concentrator plants made them risky at the moment and any offeror would likely wait until that is out of the way. This makes today’s announcement doubly interesting:

…notes the recent press speculation and confirms that it has received a non-binding proposal from Oryx Global Partners Limited and Michael Carvill (together the “Consortium”) regarding a possible all cash offer for the entire issued and to be issued ordinary share capital of Kenmare.

This may mean that Carvill believes the move of the wet concentrator plant is going well. Or perhaps simply the price had got too cheap, and the market was never going to recognise the value here in the short term:

The price considered:

The most recent proposal received was at a price of 530 pence per Kenmare ordinary share (the “Proposal”).

This is quite some premium but also less than tangible book value. This is perhaps why the board say:

The Board of Kenmare, together with its advisers, considered the terms of the Proposal and unanimously rejected it on the basis that it undervalued Kenmare’s business and its prospects.

The main bidder, Oryx Global Partners, is an investment firm, which opens up the door for mining companies to perhaps join the fray.

Mark’s view

It has clearly been a mistake for me to be put off holding this obviously cheap company based on the political and execution risk. The board clearly understand the value of the business as they are rejecting a bid for an almost 100% premium. It does beg the question of why they weren’t buying back shares in the market recently if they knew they were buying £1 coins for 50p. Given the strategic and financial benefit of owning one of the largest Heavy Mineral Sands mines in the world, I can easily see Oryx returning with an offer that is acceptable to the board, or a larger mining company being willing to do so now the company is “in play”. PINK

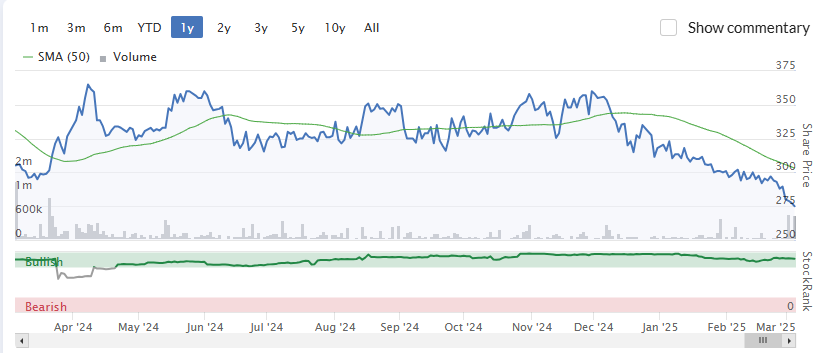

Robert Walters (LON:RWA)

Down 1% to 244p - 2024 FY Results - Mark - AMBER

In current economic conditions, contract recruitment tends to outperform permanent hiring. The reason isn’t just fewer corporate positions, but that permanent candidates don’t want to give up their employment rights for two years in order to switch companies. Unfortunately, Robert Walters has a focus on the latter. This makes them less efficient as candidates may go through the full recruitment process before deciding the offer isn’t generous enough to risk accepting it. They clearly understand this, as they say:

During the year we began to embed more robust behaviours on managing the sales funnel into our specialist professional recruitment business. This will ensure we are maximising the new job flow at the top of the funnel, and more actively influencing each key stage of the process such that we improve conversion into placements. The 5% decline in this volume productivity measure year-on-year reflected our decision not to let fee earner headcount fall further. Overall productivity, as measured by net fee income per fee earner, was up 1%* - underpinned by continued stable fee rates and benefits from wage inflation.

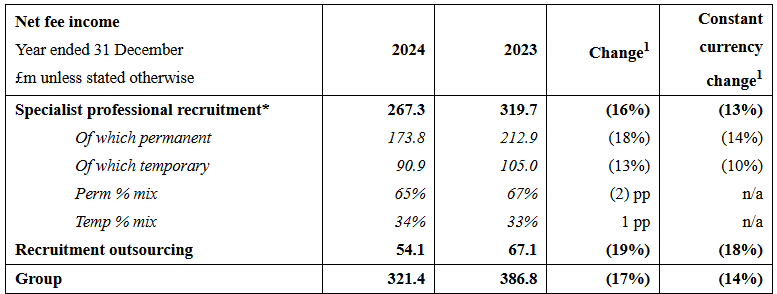

Despite these efforts, it is disappointing to see Net Fee Income in all three of their segments falling by double-digit percentages:

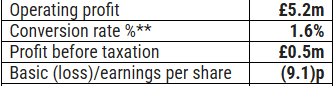

These figures were revealed at the trading statement earlier this year, so the new news today is the impact on profitability. A modest operating profit becomes a 9.1p EPS loss:

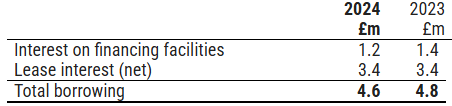

The reasons are that they have a £6.5m tax charge, presumably as losses in some parts of the business cannot be offset against profits in others, plus £3.9m of net finance charges. This seems strange as they report £52.5m of net cash at year-end. Either this means they have a very variable working capital profile during the year, or like many recruiters, they are factoring their receivables on a non-recourse basis and hence moving these off-balance sheet under current accounting regs. In addition, a proportion of the lease costs are classified as interest under IFRS16:

Their broker, Panmure Liberum describes these results as “in line”, which must mean that they are making their own adjustments. To their credit, the company themselves don’t report adjusted figures. We only find out in the commentary that:

Included in operating costs is £2.8m of redundancy costs incurred during the year.

This cost-cutting should have a positive impact on future profitability. However, it seems that the bulk of the savings have already been made early in this year. Admin costs were about 13% lower year-on-year, and they say that their year-end headcount is down 17%. So, a return to profitability really requires a recovery in their markets, where they say:

The Board's planning assumption remains that, at the earliest, an improvement in end markets is unlikely to be seen before the latter part of 2025, and as such the business will continue to ensure its cost base is appropriate for the current conditions.

Give the cash balance, they maintain the dividend for this year, making it an almost 10% yield. However, their capital allocation section gives rather mixed signals. Firstly:

The Board continues to recognise the value of a strong balance sheet, and therefore targets year-end net cash of at least £50m.

But by paying the 17p final dividend, they will almost certainly fall below that level at the end of 2025. Then they say:

Secondly, the Group's policy is to maintain a dividend cover ratio of 1.75-2.25x through the cycle. The Group also has the latitude to allow cover to fall outside this range at points in the cycle - as has been the case over the last two years - whilst seeking a clear route to return to the range. Looking ahead, the Board continues to be mindful of this aspect of the policy, particularly given the extended period of challenging market conditions whereby dividend cover has been outside the range.

Which makes it sound like a cut is on the way. So, I don’t think investors can bank on that high level of payout continuing. They then say excess capital above the £50m level may be returned via special dividends or buybacks. However, this would mean that they buy back shares when trading is good and the price is high, and not when the shares are low. The opposite of what will create long-term shareholder value.

Mark’s view

When Graham looked at this following recent trading statement, he rated it GREEN/AMBER given the strength of the balance sheet and the potential for a sector-wide recovery. However, I see little here that marks it out as different to the larger recruiters at the moment. It also seems to be underperforming some of the smaller sector peers, such as Gattaca (which I hold). With little sign of any recovery in the short term, meaning it looks expensive on any medium-term earnings forecast, and the risk of a dividend cut looking much higher, I can only get to AMBER.

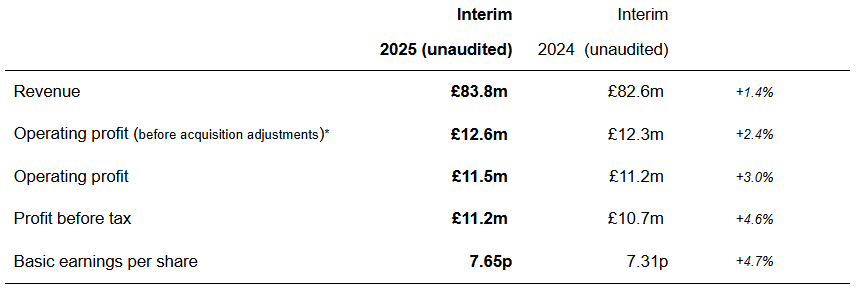

FW Thorpe (LON:TFW)

Up 4% to 313p - 2024 FY Results - Mark - AMBER

With no forecasts in the market, these results have to be judged on a standalone basis:

Revenue is almost certainly behind inflation. However, PBT and EPS both rise around 5%. This is due to slightly higher H1 operating margins, which move from 13.6% to 13.8%, and higher finance income on their cash balance. There is a clear H2-weighting to this business, so the H2 outlook matters as much as these results:

At the time of writing, the Group's order book remains strong, and revenue is marginally ahead of last year. Forecast rising costs, mainly due to wage and National Insurance increases, will be offset by certain material cost reductions and efficiency improvements. As a result, the Board anticipates a marginal improvement in profit for the financial year ending June 2025.

That sounds a little uninspiring to me. This has been a reasonable growth company in the recent past, with 10% CAGR 5-year revenue growth, turning into around 14% CAGR normalised EPS growth, and they have a consistent mid-teens return on capital. However, none of that matters if they don’t manage to grow in the future. For every flat year, as FY25 is forecast to be, they need to have a bumper year to maintain those growth rates.

They have around £53m of cash versus a market cap of around £350m, which makes the c.14 P/E a bit better value than it first seems. There are also no accounting gimmicks. Less conservative companies would try to persuade investors that they should ignore share-based payments or FX movements. Despite this, the rating doesn’t stand out in a UK market where mid-single-digit P/Es look more normal for companies struggling with short-term growth in tough market conditions.

In terms of uses for that cash, they say:

The Board continues to assess the opportunities to maximise returns from the Company's strong balance sheet, which may include share buybacks where it considers that the share price significantly undervalues the Company's current position and future prospects.

While the shares may be down around 30% over the last year, it seems tricky to argue that they are significantly undervalued at current levels unless they can grow more rapidly in the future. Acquiring more cheaply-rated businesses where they can take out cost and add value with their operational experience would seem a better strategy to me.

Mark’s view

I certainly wouldn’t bet against such a conservatively run, well-financed, family-owned business. However, there is no escaping the reality that they have to return to double-digit EPS growth rates in the medium-term to justify the current rating, let alone anything higher. AMBER

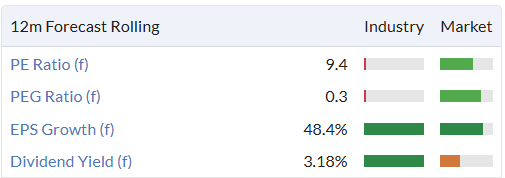

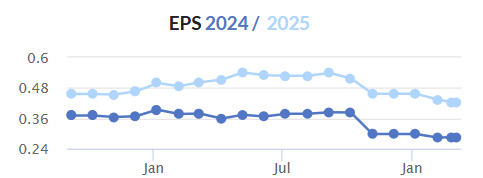

Elementis (LON:ELM)

Flat at 152p - Preliminary Results - Mark - AMBER/RED

I struggle with the rating of this company. Revenue has gone nowhere in the last 5 years or so:

Neither has EPS:

And the ROCE suggests that any growth, if it did occur, would destroy shareholder value:

Yet the rating remains stubbornly high on almost all metrics:

Perhaps these results will reveal something the algorithms and I are missing:

This is another year of flat revenue. However, the EPS is looking much better after $18m of cost savings in the year, at least on an adjusted basis. Looking at the adjustments, there is a big write-down in assets:

However, the rest look to be a normal part of running a struggling business. The good news is that net debt has come down from $202m to $157.2m, and at 1.0x adj. EBITDA looks perfectly manageable.

There seems to be little in the way of forward guidance given in these results, so we can assume they're in line, with further cost savings offsetting a lack of revenue growth.

Mark’s view

There is nothing inherently wrong with this business; it just seems to have gone nowhere over the last decade, and there is no sign of it going anywhere in the future. Cost-savings will continue to offset weakness in end markets. However, cost-cutting is no substitute for increasing sales in the long term. On a forward P/E of 14 and yield of 2% it simply looks overvalued compared to historical or future growth rates. AMBER/RED

Vesuvius (LON:VSVS)

Flat at 410p - FY Results - Mark - AMBER

These look in line with the Stockopedia consensus, at least on an adjusted basis:

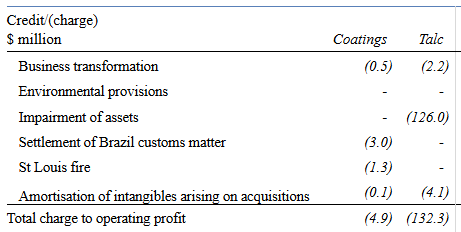

This is another company that would like investors to credit them with the benefits of their cost-reduction program but not include the cost of actually implementing it:

In 2024, we delivered cost savings under this programme of £13m with an annualised exit run-rate of £18m. Of the savings delivered in-year, slightly under half were in the Foundry Division, reflecting swift action taken to address costs in a challenging environment. The cost savings achieved to date have been weighted towards headcount reductions. We expect to deliver incremental in-year cost savings of £12m - £14m in 2025.

The one-off costs to deliver these savings are shown as separately reported items, and in FY24 were £14.6m charged to the income statement with a cashflow impact of £7.9m. We anticipate one-off costs in 2025 in the region £7-10m and retain our guidance that the total programme will cost c. £40m, including associated capex costs.

Net debt is up, despite free cash flow, as the company has chosen to slightly increase their dividend and do a share buyback:

Net debt on 31 December 2024 was £329.2m, a £91.7m increase compared to £237.5m on 31 December 2023, due to free cash flow of £60.8m offset principally by dividends of £61.1m, share buybacks of £63.4m and purchases of shares for our ESOP trust of £17.1m.

Despite this being on an undemanding P/E of around 10, I’m not sure this is the best use of capital. After all, increasing debt has been the downfall of many companies when they face an unexpected downturn. In the short term, this seems unlikely as they are at 1.3x EBITDA versus a covenant of 3.25x. However, it is worth keeping a close eye on this as banks generally don’t like funding shareholder returns.

In terms of the current outlook, they say:

We currently anticipate that our trading profit in 2025 will be at a broadly similar level to 2024 on a constant currency basis and including the contribution from the PiroMET acquisition.

This looks like a miss to me versus a net profit figure that was forecast to rise. There is also likely to be increased finance charges from the higher debt levels:

So this means the company trades on a forward P/E of around 10.

Mark’s view

The outlook statement here suggests that this is a miss. However, the lack of share price reaction means that it may have already been in the price. Either way, a forward P/E of around 10 looks about right for a business that is not growing in the short to medium term. AMBER

Harbour Energy (LON:HBR)

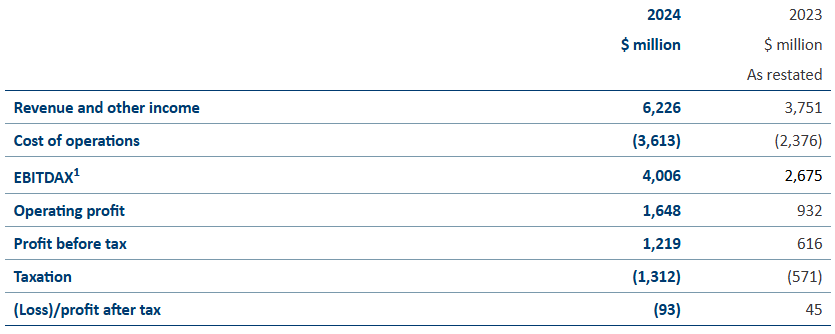

Down 10% to 191p - Final Results - Mark - AMBER

A move to an operating loss appears to have spooked the market here:

This is driven by an unusually large tax charge. However, this probably isn’t the most important metric. This is another company where the outlook is complex due to a very large acquisition in the period, which has seen net debt balloon:

As at 31 December 2024, net debt of $4,424 million (2023: $207 million, as restated).

The asset side is also transformed with significant free cash flow generation expected:

At Brent oil prices of $80/bbl and UK and European natural gas prices of $13/mscf, we expect to generate free cash flow of c. $1.0 billion1 in 2025. With a $5/bbl change in Brent oil prices or $1/mscf change in European natural gas prices impacting free cash flow by c.$115 million, we still expect to generate material free cash flow at current prices.

With Brent oil now closer to $70/bbl, this is more like $800m of FCF. However, this more than covers the generous dividend payout:

The Board has declared a final dividend of $227.5 million in respect of the 2024 financial year to be paid in May 2025 equating to 13.19 cents per ordinary share, subject to shareholder approval. This is in line with the Board's commitment at the time of acquisition announcement to increase the annual dividend to $455 million and signals the Board's ongoing confidence in the scale and longevity of our free cash flow generation.

This works out at more than 10% yield and may appeal to income investors, especially those who expect the current politically driven oil price weakness to be temporary.

Mark’s view

The scale of the debt-funded transactions here make this a bit riskier than the average company in the sector but also accelerates the upside for those who are bullish on oil. The 10% yield is attractive but perhaps not out of line with the rest of the sector either. It is an AMBER for me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.